- Home Care & Utilities

- Suspension Packaging Market

Suspension Packaging Market Size, Share, and Growth Forecast, 2026 – 2033

Suspension Packaging Market by Material Type (Plastic Suspension Packaging, Paper Suspension Packaging, Others), Product Type (Blister Packs, Clamshells, Trays, Pouches, Wrapping Films), and Regional Analysis for 2026 – 2033

Suspension Packaging Market Size and Trends Analysis

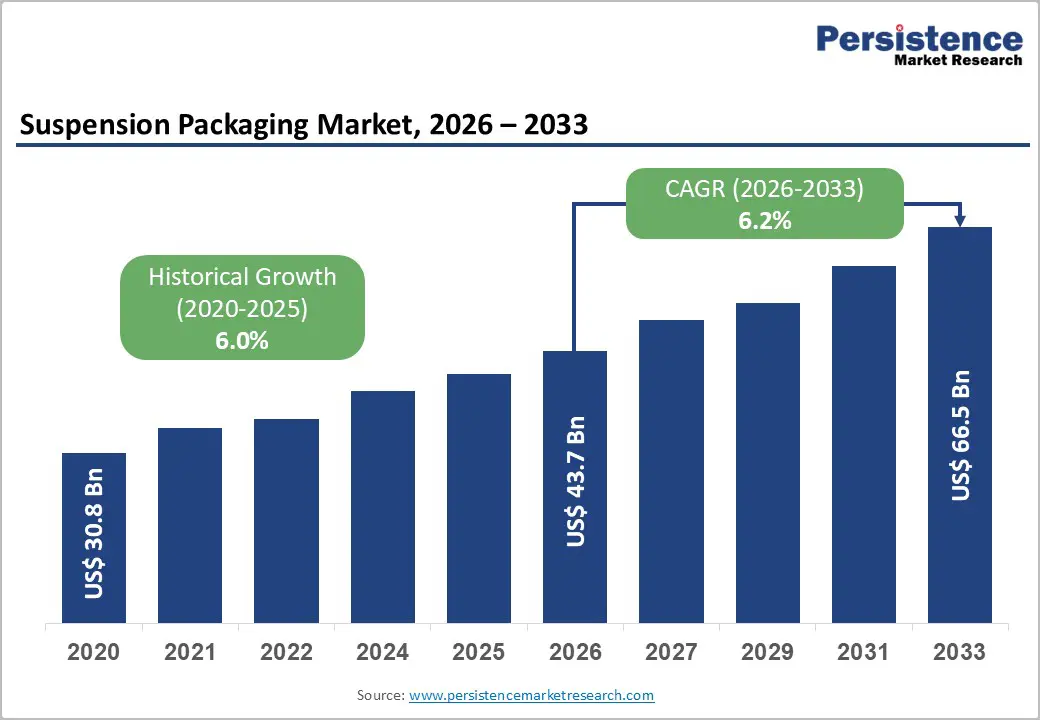

The global suspension packaging market size is likely to be valued at US$43.7 billion in 2026 and is expected to reach US$66.5 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by the rapid expansion of e-commerce, increasing demand for safe transport of fragile and high-value goods, rising adoption of sustainable and recyclable packaging materials, and growing focus on reducing product damage, returns, and logistics losses across supply chains. Increasing focus on product safety and return reduction has encouraged manufacturers and logistics providers to adopt suspension packaging solutions that ensure product integrity throughout the supply chain. Sustainability initiatives and regulatory pressures are accelerating the shift toward paper-based, recyclable, and environmentally friendly materials, prompting continuous innovation in packaging design and material composition.

Key Industry Highlights:

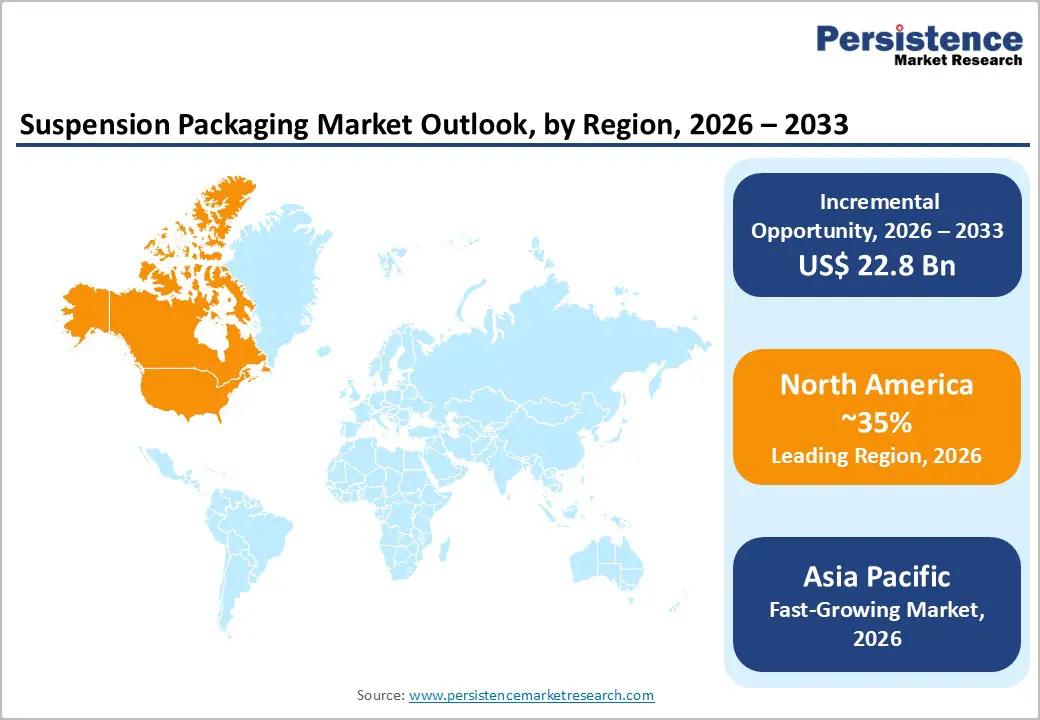

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong e-commerce penetration, advanced logistics infrastructure, and high standards for product protection and packaging quality.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in suspension packaging in 2026, supported by strong manufacturing activity and accelerating e-commerce adoption across the region.

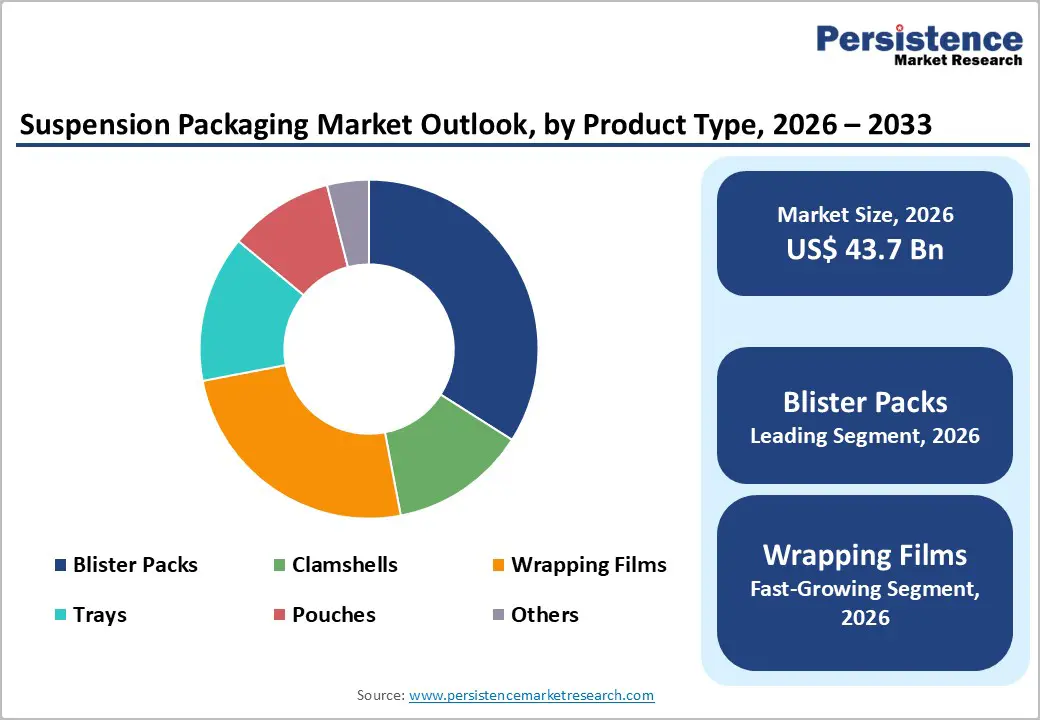

- Leading Material Type: Plastic suspension packaging is projected to represent the leading material type in 2026, accounting for 50% of the revenue share, driven by its flexibility, durability, cost efficiency, and strong adoption across electronics and e-commerce applications.

- Leading Product Type: Blister packs are anticipated to be the leading product type, accounting for over 45% of the revenue share in 2026, supported by their excellent product visibility, tamper-evident properties, strong protective performance, and widespread use across pharmaceutical, electronics, and retail packaging applications.

| Global Market Attributes | Key Insights |

|---|---|

| Suspension Packaging Market Size (2026E) | US$43.7 Bn |

| Market Value Forecast (2033F) | US$66.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-commerce and Last-Mile Delivery Growth

Online retail platforms increasingly ship fragile, high-value, and customized products directly to consumers. Electronics, cosmetics, pharmaceuticals, and premium consumer goods require advanced protective solutions to withstand multiple handling points, long transit distances, and complex last-mile delivery networks. Suspension packaging minimizes shock, vibration, and compression damage, reducing product returns and replacement costs. As same-day and next-day delivery models grow, brands prioritize packaging that ensures product integrity while maintaining lightweight and cost-efficient shipping, strengthening demand for suspension packaging solutions.

Last-mile delivery growth amplifies the need for reliable protective packaging, as parcels face a higher risk of drops, stacking pressure, and uneven handling in urban and semi-urban environments. Suspension packaging provides consistent protection regardless of package orientation, making it ideal for automated sorting and courier-based delivery systems. The rise of direct-to-consumer brands also fuels adoption, as brand reputation increasingly depends on damage-free delivery experiences. With e-commerce volumes continuing to surge, suspension packaging plays a critical role in supporting scalable, efficient, and customer-centric logistics operations.

Sustainability Regulations and Corporate ESG Commitments

Governments across major economies are implementing stricter regulations on single-use plastics, waste reduction, and recyclability, compelling packaging manufacturers to redesign materials and structures. Brands are under increasing pressure to comply with extended producer responsibility frameworks and environmental labeling requirements. Suspension packaging solutions are being reengineered to reduce material usage, improve recyclability, and lower carbon footprints while maintaining protective performance.

Corporate ESG strategies accelerate this shift, as companies commit to sustainability targets across their supply chains. Many brands are replacing conventional plastic-heavy packaging with paper-based, recyclable, or bio-based suspension packaging to align with environmental goals and consumer expectations. Suspension packaging supports these initiatives by enabling lightweight designs that reduce transportation emissions and packaging waste. This convergence of regulatory enforcement and voluntary ESG commitments ensures sustained demand for innovative, sustainable suspension packaging solutions across industries.

Barrier Analysis - Recycling Infrastructure Limitations and Material Complexity

Despite growing sustainability efforts, recycling infrastructure limitations pose a significant restraint on the suspension packaging market. Many suspension packaging solutions use multi-material structures, combining films, coatings, or composites to achieve shock absorption and durability. These complex material combinations are difficult to separate and recycle using existing waste management systems, particularly in developing regions. Recyclability claims may not always translate into real-world recycling outcomes, limiting adoption among environmentally conscious brands.

Uneven recycling infrastructure across regions creates compliance challenges for packaging suppliers. While advanced markets support paper and plastic recycling, many regions lack facilities to process specialized suspension packaging materials. This gap increases disposal costs and undermines sustainability objectives. Until recycling systems evolve to handle advanced packaging formats, material complexity will continue to restrain the widespread adoption of certain suspension packaging solutions.

Supply Chain Disruptions and Material Shortages

Volatility in raw material availability, particularly for plastics, specialty papers, and barrier films, affects production continuity and pricing stability. Events, logistics bottlenecks, and energy cost fluctuations can disrupt supply chains, making it difficult for manufacturers to meet demand consistently. These disruptions increase lead times and reduce flexibility for packaging suppliers and end users. Inconsistent material supply complicates long-term contracts with e-commerce and industrial customers, impacting planning efficiency and delivery reliability.

Material shortages also hinder innovation, as manufacturers struggle to secure consistent quality inputs for advanced suspension packaging designs. Smaller players are particularly affected, as they lack diversified sourcing networks. In price-sensitive markets, higher material costs may push customers toward simpler or less protective alternatives. This shift can compromise product safety and increase damage rates during transit. As long as supply chain instability persists, it remains a restraint on market scalability and cost optimization.

Opportunity Analysis - Expansion of Sustainable and Bio-Based Materials

Growing environmental awareness and regulatory pressure are encouraging manufacturers to invest in renewable fibers, compostable films, and recyclable mono-material designs. Paper-based suspension packaging made from recycled or responsibly sourced fibers is gaining traction, especially in e-commerce and consumer goods applications where sustainability is a purchasing factor. Brands are increasingly using sustainable packaging as a differentiator to enhance customer trust and brand loyalty. This shift also supports corporate ESG goals and compliance with evolving environmental regulations across major markets.

Bio-based materials also offer long-term differentiation, enabling brands to reduce dependence on fossil-based plastics while maintaining performance standards. Innovations in coatings, molded fiber technologies, and hybrid designs are closing the performance gap between sustainable materials and traditional plastics. These advancements improve moisture resistance, strength, and cushioning performance, expanding usability across sensitive product categories. As material science advances, sustainable suspension packaging is increasingly supporting a wider range of applications across e-commerce, electronics, cosmetics, and consumer goods, while helping brands meet environmental compliance requirements and strengthen their market positioning.

Smart Packaging Integration

The incorporation of sensors, tracking elements, and condition-monitoring technologies enables real-time visibility into shipment handling, shock exposure, and environmental conditions. For high-value goods such as electronics, medical devices, and pharmaceuticals, smart suspension packaging enhances supply chain transparency and risk management. It also supports better accountability across logistics partners by providing data on handling quality during transit. This capability is particularly valuable in cross-border shipments and temperature or impact-sensitive deliveries.

As digitalization accelerates across logistics and warehousing, smart packaging aligns with automation and data-driven decision-making. Suspension packaging formats are well-suited for embedding smart features without compromising protection. These systems enable predictive analysis of damage risks and support continuous improvement in packaging performance. The integration helps reduce damage-related losses, improve regulatory compliance, and optimize packaging design across high-value and mission-critical supply chains.

Category-wise Analysis

Material Type Insights

Plastic suspension packaging is expected to lead the suspension packaging market, accounting for approximately 50% of revenue in 2026, driven by its superior elasticity, transparency, and cost-to-performance efficiency in high-volume protective packaging applications. Its ability to securely suspend products between flexible films makes it highly effective in absorbing shock, vibration, and compression during transportation. For example, the widespread use of plastic suspension packaging for shipping consumer electronics such as smartphones and computer components, where visibility, durability, and cushioning are essential to prevent transit damage and ensure a premium unboxing experience.

Paper suspension packaging is likely to represent the fastest-growing segment in 2026, supported by increasing sustainability commitments from brands and rising demand for recyclable and eco-friendly packaging solutions. While holding a smaller share compared to plastics, paper-based suspension packaging is gaining traction as companies aim to reduce environmental impact and comply with regulatory and corporate ESG requirements. For example, the growing adoption of molded fiber suspension packaging by online cosmetic brands, which use paper-based solutions to protect glass bottles while reinforcing their sustainable brand image.

Product Type Insights

Blister packs are projected to lead the market, capturing around 45% of the revenue share in 2026, supported by their strong combination of protection, product visibility, and tamper-evident features. These formats are widely favored in pharmaceutical, electronics, and retail applications where both product safety and consumer confidence are critical. Blister packs integrate suspension functionality that securely holds products in place, minimizing movement and damage during handling and transit. For example, pharmaceutical blister packaging is used for tablets and medical devices, where suspended placement ensures product integrity while meeting strict regulatory and safety requirements.

Wrapping films are likely to be the fastest-growing product type in 2026, driven by their flexibility, lightweight design, and adaptability to modern e-commerce and automated fulfillment environments. Unlike rigid formats, wrapping films can accommodate irregularly shaped products while still providing effective suspension and cushioning. This versatility makes them particularly suitable for high-volume parcel shipping, where space efficiency and material reduction are priorities. For example, the use of suspension wrapping films in e-commerce warehouses to protect consumer electronics accessories, where films adjust to varying product sizes while ensuring damage-free delivery and efficient packaging operations.

Regional Insights

North America Suspension Packaging Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by advanced e-commerce infrastructure and sophisticated logistics networks. The region demands packaging solutions that can protect diverse product categories, including consumer electronics, medical devices, and industrial components. A rising trend is the integration of lightweight, high-performance materials that reduce transportation costs and carbon footprint while maintaining protective integrity. Stringent quality standards from regulatory bodies and heightened consumer expectations for damage-free delivery reinforce the adoption of suspension packaging across retail and B2B segments.

Innovation and sustainability have become defining trends with major players investing in recyclable materials and smart packaging solutions. Regulatory emphasis on reducing single-use plastics and extended producer responsibility has encouraged packaging manufacturers to develop alternatives that offer similar performance with lower environmental impact. For example, Smurfit Kappa Group has expanded its portfolio of recyclable and fiber-based suspension packaging solutions to cater to brands seeking sustainable yet protective formats.

Europe Suspension Packaging Market Trends

Europe is likely to be a significant market for suspension packaging in 2026, due to strong environmental regulations, elevated consumer expectations for sustainable packaging, and a mature industrial base emphasizing product protection across diverse sectors. Regulatory frameworks such as the European Green Deal and the single-use plastics directive have accelerated the shift toward recyclable, reusable, and bio-based suspension packaging solutions, prompting manufacturers and brands to innovate beyond traditional plastic-heavy formats. This transition is particularly visible in industries such as pharmaceuticals, luxury retail, and consumer electronics, where protective packaging must balance performance with environmental compliance.

Innovation in material science and design is a key trend in the European suspension packaging market, as companies develop advanced solutions to address both performance and sustainability objectives. Packaging manufacturers are exploring coated papers, molded fiber suspensions, and hybrid formats that offer cushioning comparable to plastics while being fully recyclable. For example, DS Smith has expanded its sustainable packaging portfolio with paper-based suspension systems tailored for electronics and fragile goods, responding to demand from major retail and logistics players seeking eco-friendly alternatives.

Asia Pacific Suspension Packaging Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by expanding manufacturing hubs, robust e-commerce adoption, and increasing demand for protective packaging across electronics, automotive parts, and consumer goods. Countries such as China, India, Japan, and ASEAN nations contribute significantly due to their large industrial bases and growing middle-class consumer markets, which elevate parcel volumes and require reliable damage prevention solutions. This region’s cost-competitive production environment also attracts brands and packaging innovators seeking scalable and efficient suspension packaging.

In the Asia Pacific region, sustainability and innovation are increasingly shaping suspension packaging strategies, as environmental awareness and regulatory frameworks gain prominence. Manufacturers and brands are progressively adopting recyclable and eco-friendly materials to align with circular economy goals, responding to both domestic environmental policies and sustainability commitments. For example, Ranpak Holdings Corp. has expanded its presence with paper-based and renewable fiber suspension packaging solutions in key markets such as China and Southeast Asia, catering to customers looking for sustainable alternatives to traditional plastics while maintaining protective performance.

Competitive Landscape

The global suspension packaging market exhibits a moderately fragmented structure, driven by a mix of large multinational corporations and specialized regional manufacturers competing across product innovation, sustainability, and geographic reach. Established players continuously invest in research and development, advanced materials, and automated packaging technologies to meet evolving demand from e-commerce, electronics, healthcare, and industrial sectors.

With key leaders including Sealed Air Corporation, Smurfit Kappa Group, DS Smith Plc, Pregis Corporation, and Storopack Hans Reichenecker GmbH, the market reflects both scale and innovation in protective packaging offerings. These players compete through expansion of sustainable product lines, strategic acquisitions, and footprint enhancements to secure long-term contracts with major brands and e-commerce platforms.

Key Industry Developments:

- In February 2025, Mondi partnered with Zwiesel Glas to create a premium fiber-based suspension packaging solution for mouth-blown glassware. Produced at Mondi’s Grünburg plant, the bespoke packaging replaced plastic with recyclable materials, enhancing both protection and the unboxing experience. This move reflected a wider industry shift toward sustainable packaging for fragile, high-value goods.

- In January 2024, SEE (Sealed Air) implemented digital die-cutting technology for its Korrvu® suspension packaging, reducing production lead times from months to weeks. The new process enabled smaller order quantities, on-demand production, and customization without physical tooling, improving supply chain efficiency and reducing storage needs.

Companies Covered in Suspension Packaging Market

- Sealed Air Corporation

- Pregis Corporation

- Storopack Hans Reichenecker GmbH

- Smurfit Kappa Group

- Ranpak Holdings Corp.

- Intertape Polymer Group Inc.

- Automated Packaging Systems, Inc.

- Polyair Inter Pack Inc.

- Inflatable Packaging, Inc.

- Aeris Protective Packaging Inc.

- Free-Flow Packaging International, Inc.

- Max Packaging

- A E Sutton Limited

- Macfarlane Group PLC

- Veritiv Corporation

- Shorr Packaging Corp.

- Atlantic Packaging

- Packsize International LLC

- Pro-Pac Packaging Limited

Frequently Asked Questions

The global suspension packaging market is projected to reach US$43.7 billion in 2026.

The suspension packaging market is driven by rapid e-commerce growth, increasing demand for damage-free transport of fragile and high-value goods, and rising adoption of sustainable protective packaging solutions.

The suspension packaging market is expected to grow at a CAGR of 6.2% from 2026 to 2033.

Key market opportunities lie in the expansion of sustainable and paper-based suspension packaging, smart packaging integration, and growing demand from e-commerce, electronics, and healthcare sectors.

Sealed Air Corporation, Pregis Corporation, Storopack Hans Reichenecker GmbH, and Smurfit Kappa Group are the leading players.