- Automotive Components & Materials

- Suspension Ball Joint Market

Suspension Ball Joint Market Size, Share, and Growth Forecast, 2026 - 2033

Suspension Ball Joint Market by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Others), Material Type (Steel, Aluminum, Composite Materials, Alloy), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2026 - 2033

Suspension Ball Joint Market Share and Trends Analysis

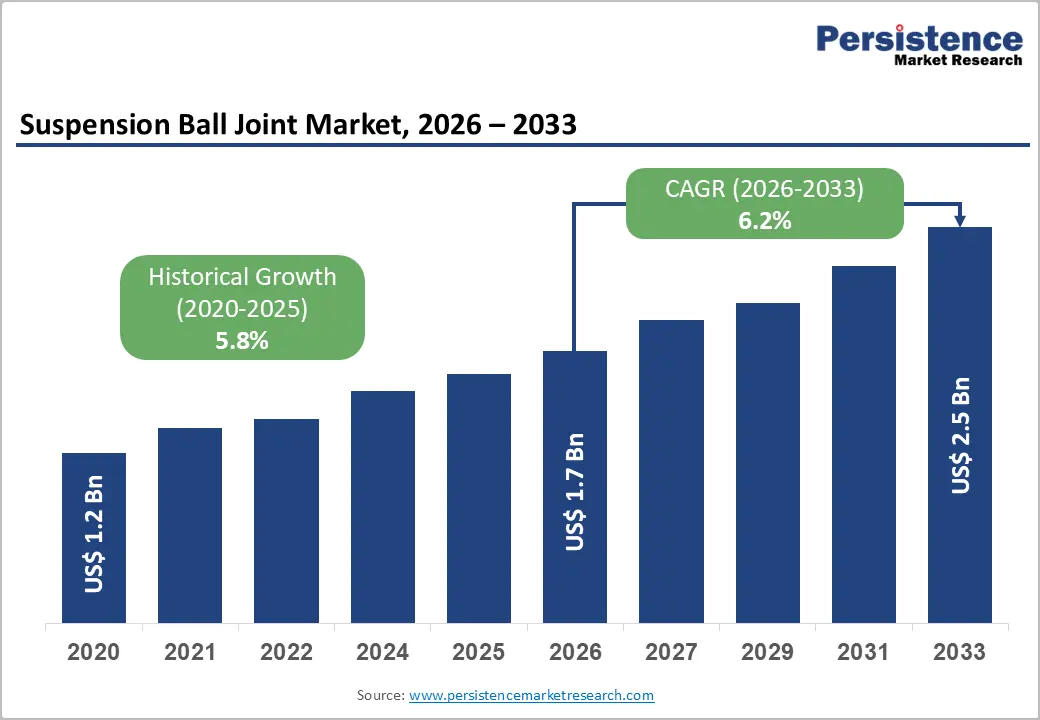

The global suspension ball joint market size is likely to be valued at US$1.7 billion in 2026 and is estimated to reach US$2.5 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026 - 2033, driven by increasing global vehicle production and the growing aging vehicle fleet, which drives steady demand for replacement of wear-sensitive chassis and suspension components.

Rapid urbanization has also led to more frequent short-distance driving conditions, contributing to accelerated wear and mechanical fatigue in steering and suspension linkages. Stringent vehicle safety and roadworthiness regulations imposed by organizations such as the National Highway Traffic Safety Administration are also encouraging timely maintenance and component replacement.

The increasing adoption of lightweight alloy materials in electric vehicle platforms further strengthens demand for high-precision suspension ball joints capable of supporting higher battery loads while maintaining vehicle stability and performance.

Key Industry Highlights:

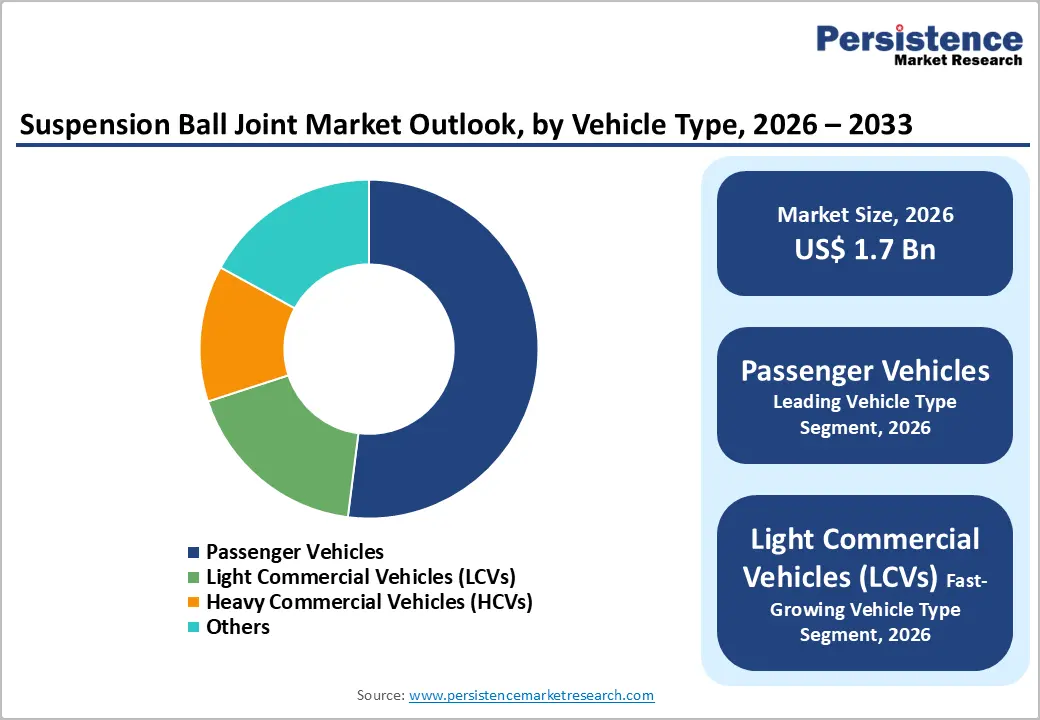

- Leading Vehicle Type: Passenger vehicles are set to hold around 52% market share in 2026, driven by high global passenger car manufacturing volumes.

- Fastest-growing Vehicle Type: Light commercial vehicles (LCVs) are projected as the fastest-growing segment, supported by expanding urban e-commerce delivery fleet operations.

- Leading Sales Channel: Aftermarket is estimated to hold roughly 58% market share in 2026, due to predictable component wear cycles across aging vehicle populations.

- Fastest-Growing Sales Channel: Original equipment manufacturers (OEMs) are forecast to grow the fastest, driven by rapid integration into next-generation electric vehicle assembly architectures.

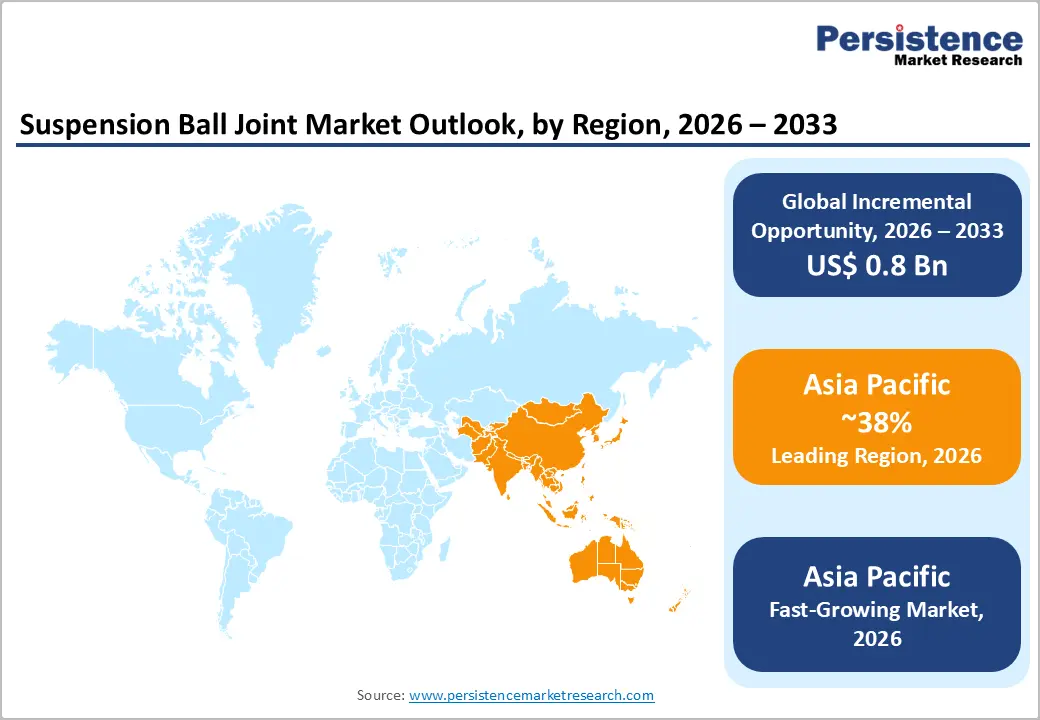

- Regional Leadership: Asia Pacific is projected to capture roughly 38% of the market share by 2026, and is also forecast to record the fastest growth due to expanding vehicle production in China.

- Competitive Environment: The market is moderately fragmented, with players such as ZF and Tenneco leveraging technical innovation and broad distribution networks to maintain market positions.

- Innovation Trends: Advancements in lightweight material science, particularly the use of forged aluminum, and the integration of wear-monitoring sensors are shaping the future of chassis engineering.

DRO Analysis

Driver - Growth in Global Vehicle Parc and Aging Fleet Maintenance

The continuous expansion of the global automotive parc creates a substantial recurring revenue stream for aftermarket components. As the average age of vehicles in operation increases, the structural integrity of original equipment suspension parts inevitably declines due to environmental exposure and mechanical stress. Data from the European Automobile Manufacturers Association (ACEA) in 2025 indicates the average age of passenger cars in the European Union reached 12.3 years. This longevity necessitates multiple replacement cycles for ball joints to ensure steering precision and passenger safety.

Increased vehicle utilization rates in ride-sharing and commercial logistics sectors further intensify component wear. High-frequency operation over diverse road surfaces depletes internal lubricants and degrades protective dust boots. Service disclosures from major automotive maintenance providers confirm a direct correlation between rising odometer readings and the frequency of chassis-related repairs. The resulting need for reliable replacement parts stabilizes demand for manufacturers focusing on high-durability aftermarket solutions.

Restraint - Shift toward Advanced Suspension Technologies

Increasing adoption of air suspension and electronically controlled systems is reducing reliance on traditional ball joint configurations. Premium vehicle segments are integrating alternative systems that minimize mechanical linkage usage. This transition is gradually impacting demand in specific vehicle categories.

Original Equipment Manufacturer (OEM) integration of maintenance-free suspension components is reducing replacement frequency. Sealed systems limit aftermarket intervention, which affects recurring revenue streams. High integration levels reduce component replacement accessibility, creating challenges for independent service providers and restricting scalability in conventional component segments.

Opportunity - Expansion of Lightweight Material Adoption in Chassis Engineering

The urgent need to reduce vehicle mass directly incentivizes the integration of aluminum and composite materials into steering systems. Replacing traditional steel components with lightweight alternatives significantly lowers unsprung weight, improving suspension responsiveness and tire contact. Official data from the United States Department of Energy in 2025 indicates that a 10% reduction in vehicle weight can improve fuel economy by up to 7%. This efficiency gain attracts manufacturers seeking to comply with environmental regulations.

Adoption of these advanced materials enables the optimization of electric vehicle range by reducing the weight of battery packs. Aluminum alloys provide superior corrosion resistance, extending the operational lifespan of pivot points in diverse climates. The transition toward high-strength, low-density materials creates a premium market segment for specialized forging technologies. Precise engineering of these components ensures structural integrity under high vertical loads. This shift generates high-margin revenue streams for innovative parts producers.

Category-wise Analysis

Vehicle Type Insights

Passenger vehicles are expected to capture around 52% of the suspension ball joint market share in 2026, reflecting high vehicle production volumes and strong consumer reliance on personal transportation. Automotive manufacturers integrate multiple suspension ball joints per vehicle to improve steering precision and ride stability, exemplified by multi-link front suspension systems widely utilized in modern sedans and crossover vehicles. This extensive integration sustains consistent production demand across global component manufacturing facilities.

Light Commercial Vehicles (LCVs) are expected to be the fastest-growing segment, propelled by the expansion of e-commerce delivery networks that increase urban fleet utilization. Vehicles such as urban delivery vans experience frequent stop-and-go driving conditions across uneven road surfaces, accelerating wear on steering and suspension assemblies. This intensive operating environment increases inspection frequency and shortens replacement cycles across commercial fleet maintenance programs.

Material Type Insights

Steel is poised to dominate with a forecast market share of over 60% in 2026, powered by high tensile strength, durability, and established manufacturing efficiency. Standard passenger vehicles widely use forged carbon-steel suspension ball joints due to their cost-effective production and reliable performance under continuous mechanical stress. This broad affordability ensures steel remains the primary material across high-volume automotive assembly operations.

Aluminum is estimated to be the fastest-growing segment, driven by corporate fuel-efficiency standards that require weight-reduction strategies. Premium electric sedans increasingly incorporate lightweight aluminum suspension assemblies and integrated ball joints to reduce unsprung chassis mass. This material transition improves handling performance while enabling extended electric driving range.

Sales Channel Insights

The aftermarket segment is likely to be the leading segment, with a projected 58% share of the suspension ball joint market in 2026, driven by continuous wear and degradation of suspension components throughout a vehicle's operating life. Independent repair facilities frequently install certified replacement assemblies in aging vehicles that have exceeded their original warranty periods. This recurring replacement cycle maintains stable sales demand despite fluctuations in new-vehicle production volumes.

Original equipment manufacturers (OEMs) are anticipated to be the fastest-growing segment, fueled by the expansion of global vehicle assembly operations and the rapid deployment of next-generation electric vehicle architectures. Automotive manufacturers require high volumes of precision-engineered suspension assemblies delivered through just-in-time supply chain systems for factory installation. This integrated procurement structure supports stringent quality compliance across new vehicle production platforms.

Regional Insights

North America Suspension Ball Joint Market Trends

The North America market focuses on high-performance components for light trucks and SUVs. The U.S. NHTSA updated safety protocols in 2025, emphasizing the importance of chassis integrity in crash prevention. Technological advancements in electronic stability control drive the need for precision-engineered ball joints capable of rapid adjustment.

U.S. Suspension Ball Joint Market Insights

The U.S. is projected to maintain a significant share of the regional market, with a massive vehicle parc exceeding 280 million units in 2026. According to the 2025 Bureau of Transportation Statistics report, total vehicle miles traveled increased by approximately 0.9%, which, combined with deteriorating road conditions, contributes to accelerated vehicle component fatigue.

Canada Suspension Ball Joint Market Insights

Canada is likely to see steady growth driven by the harsh climatic conditions that accelerate component corrosion. Provincial transport safety inspections in 2025 noted a higher frequency of suspension failures due to road salt exposure. This environmental factor drives robust demand for corrosion-resistant, high-quality aftermarket ball joints nationwide.

Europe Suspension Ball Joint Market Trends

European market growth is influenced by strict regulatory frameworks governing vehicle safety and inspection. European Commission mandates on periodic vehicle testing are increasing the frequency of vehicle replacements. The presence of companies such as ZF Friedrichshafen AG and Schaeffler AG supports innovation. Electrification trends are driving design modifications, increasing demand for advanced and durable suspension components.

Germany Suspension Ball Joint Market Insights

Germany is expected to remain the technological hub for suspension innovation in Europe. The 2025 annual reports from German OEMs indicate record investments in active chassis technologies to enhance high-speed stability on the Autobahn. Companies such as ZF Friedrichshafen AG leverage this domestic expertise to export premium suspension solutions globally.

U.K. Suspension Ball Joint Market Insights

The U.K. is forecast to experience moderate growth supported by a strong automotive aftermarket and classic car restoration sector. The 2025 Driver and Vehicle Standards Agency (DVSA) Ministry of Transport (MOT) data revealed that steering and suspension issues remain a leading cause of vehicle inspection failures. This high failure rate ensures a steady demand for replacement parts across professional garage networks.

Asia Pacific Suspension Ball Joint Market Trends

Asia Pacific is expected to lead with 38% of the suspension ball joint market share in 2026, and it is also forecast to be the fastest-growing regional market. Massive automotive production in China and India, coupled with government EV incentives, drives this dominance. Rising middle-class income and urbanization in Southeast Asia accelerate vehicle ownership, while high-volume exports and established supply chains solidify its global leadership.

China Suspension Ball Joint Market Insights

China is projected to account for the largest share of the regional market, driven by its status as the world's largest vehicle producer. The China Association of Automobile Manufacturers (CAAM) reported a 10.4% increase in automotive output in 2025, significantly boosting OEM component demand. Domestic players are rapidly improving quality standards to compete in international markets.

Japan Suspension Ball Joint Market Insights

Japan is likely to focus on high-precision chassis components to stabilize its domestic automotive output. Reports from the Ministry of Economy, Trade, and Industry (METI) in late 2025 indicated that motor vehicle production contributed significantly to a 1.4% monthly increase in the industrial production index. Japanese manufacturers prioritize metallurgical excellence and automated assembly to maintain a competitive edge in global component quality.

Competitive Landscape

The global suspension ball joint market is moderately fragmented, with a mix of global tier-1 suppliers and specialized regional manufacturers competing on price and technical specifications. Key players include ZF Friedrichshafen AG, Magna International Inc., Tenneco Inc. (DRiV), Mevotech LP, and Central Automotive Products Ltd.

The presence of numerous aftermarket-focused brands in Asia and North America creates a highly competitive pricing environment. Large-scale manufacturers leverage their OEM partnerships to gain early access to vehicle design data, providing a strategic advantage in the secondary market. Strategic consolidation through mergers and acquisitions remains a common trend to expand the geographic footprint.

Key Industry Developments:

- In April 2026, Mevotech secured a U.S. patent for adaptive boot lip technology designed to reduce contamination and extend ball joint service life, reinforcing durability and performance in suspension components.

- In February 2026, Magna International secured new EV platform contracts and advanced AI-driven manufacturing capabilities, reinforcing demand for precision-engineered suspension components aligned with next-generation vehicle architectures.

- In October 2025, Tenneco DRiV showcased expanded aftermarket offerings and new suspension-focused components under brands such as MOOG and Monroe at AAPEX 2025, reinforcing product availability and performance improvements for steering and suspension systems.

Companies Covered in Suspension Ball Joint Market

- ZF Friedrichshafen AG

- Magna International Inc.

- Tenneco Inc. (DRiV)

- Mevotech LP

- Central Automotive Products Ltd.

- Delphi Technologies (BorgWarner)

- Sankei Industry Co., Ltd.

- FAG (Schaeffler Group)

- TRW Automotive (ZF Group)

- RTS S.A.

- Mando Corporation

- Hyundai Mobis Co., Ltd.

Frequently Asked Questions

The global suspension ball joint market is projected to reach US$1.7 billion in 2026.

Rising vehicle production, stricter safety inspection regulations, and increasing demand for durable suspension systems driven by higher road usage and fleet expansion in the suspension ball joint market.

The suspension ball joint market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Electric vehicle platform redesign, expansion of predictive maintenance ecosystems, and growing aftermarket replacement demand driven by aging vehicle fleets and digital service networks in the suspension ball joint market.

Some of the key market players include ZF Friedrichshafen AG, Magna International Inc., Tenneco Inc. (DRiV), Mevotech LP, and Central Automotive Products Ltd.