- Pharmaceuticals

- Stroke Diagnostics and Therapeutics Market

Stroke Diagnostics and Therapeutics Market Size, Share, and Growth Forecast, 2026 – 2033

Stroke Diagnostics and Therapeutics Market by Solution Type (Diagnostics, Therapeutics), Application (Ischemic Stroke, Hemorrhagic Stroke, Others), and Regional Analysis for 2026-2033

Stroke Diagnostics and Therapeutics Market Share and Trends Analysis

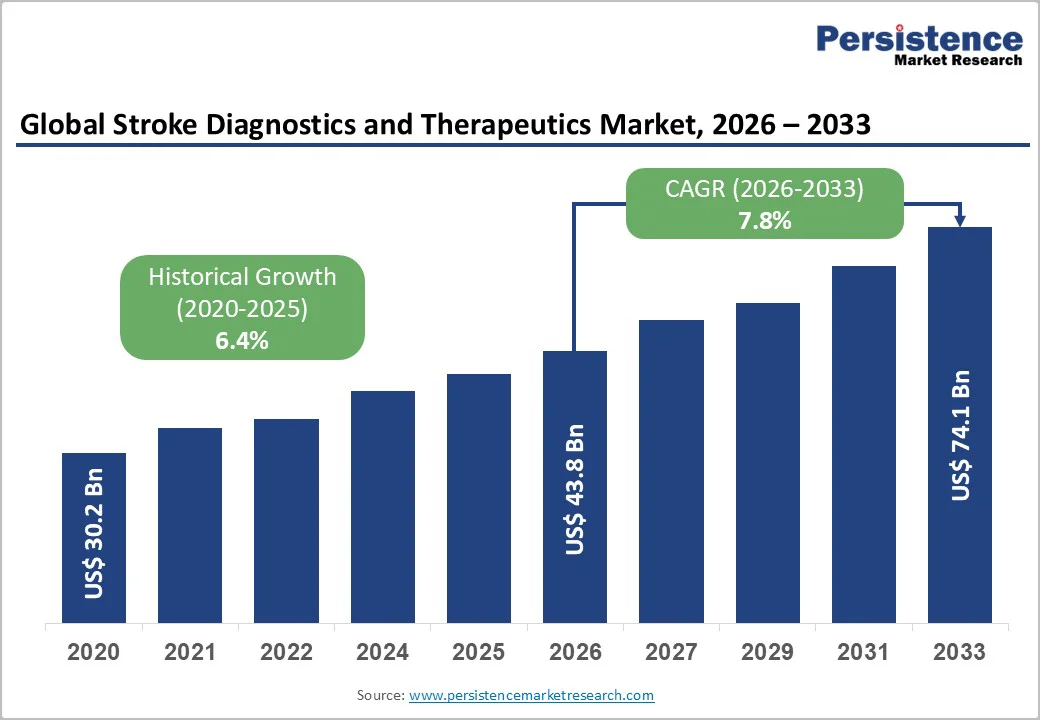

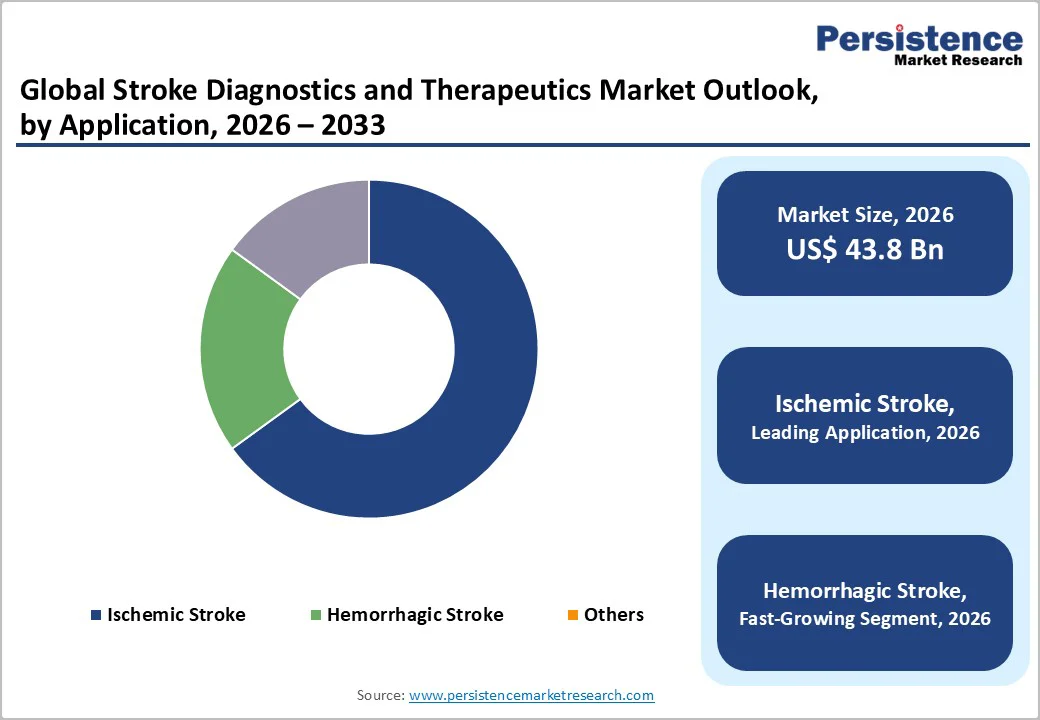

The global stroke diagnostics and therapeutics market size is likely to be valued at US$ 43.8 billion in 2026, and is projected to reach US$ 74.1 billion by 2033, growing at a CAGR of 7.8% during the forecast period 2026-2033. The market is expanding due to the rising global incidence of stroke, particularly ischemic stroke. Growth is fueled by increasing demand for rapid diagnostic imaging, advanced therapeutics, and the adoption of integrated care pathways, including stroke rehabilitation. Aging populations, higher prevalence of risk factors such as hypertension and diabetes, and growing healthcare investments in both developed and emerging regions are supporting this upward growth trajectory.

Key Industry Highlights

- Leading Solution Type: Diagnostics are expected to dominate the market with around 56% share in 2026, driven by strong MRI and CT adoption, while therapeutics are set to remain the fastest-growing segment through 2033.

- Leading Application: Ischemic stroke is likely to hold about 74% of the revenue share in 2026, with hemorrhagic and other categories gaining traction as emergency care capabilities rise.

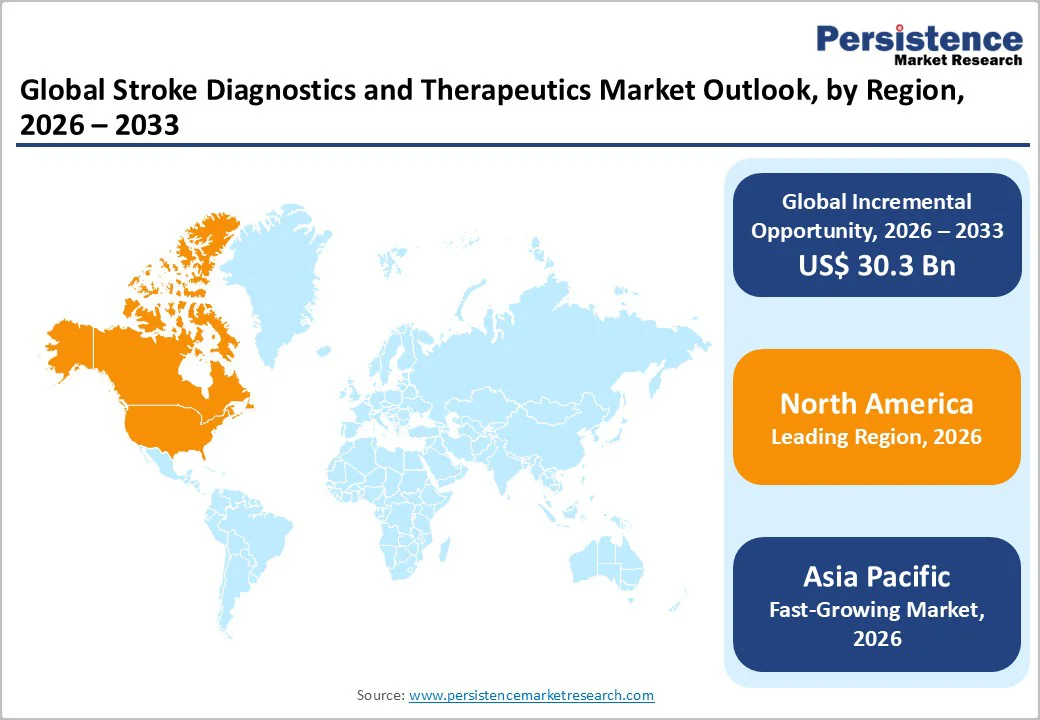

- Regional Dominance: North America is poised to dominate the market share in 2026, while the Asia Pacific market is slated to grow the fastest from 2026 to 2033 due to rising disease burden and healthcare expansion.

| Key Insights | Details |

|---|---|

| Stroke Diagnostics and Therapeutics Market Size (2026E) | US$ 43.8 Bn |

| Market Value Forecast (2033F) | US$ 74.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8 % |

| Historical Market Growth (CAGR 2020 to 2024) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Global Stroke Burden Driven by Aging and Lifestyle Risks

The most recent Global Burden of Disease (GBD) 2021 estimates show that among non-communicable disorders (NCDs), stroke remains the second leading cause of death, resulting in about 7 million, and the third leading cause of death and disability combined in the world. Given the massive burden of strokes around the globe, the demand for timely diagnosis and treatment continues to escalate. The GBD 2019 revealed that ischemic strokes accounted for nearly 63% of all stroke cases worldwide in 2019, further intensifying the need for rapid imaging and acute intervention. As aging populations expand and lifestyle-related risk factors such as hypertension, diabetes, and obesity rise, healthcare systems face increasing pressure to deploy advanced diagnostic tools and therapeutic options, accelerating overall market growth.

Rapid progress in imaging technologies, including high-resolution MRI, multi-slice CT, and AI-assisted stroke detection, is improving diagnostic speed and precision. This enables early and more accurate identification of ischemic and hemorrhagic events so that patients receive the right treatment sooner. As the treatment delays reduce, the adoption of effective therapies such as tissue plasminogen activators (tPA) and anticoagulants increases. Investments in specialized stroke centers, emergency response networks, mobile stroke units, and public health initiatives are expanding access to care in both developed and emerging markets. Therefore, technology innovation and infrastructure expansion are significantly enhancing clinical outcomes and driving sustained market growth.

High Cost Barriers and Limited Access to Specialized Stroke Care

The market faces a significant constraint due to the high cost of advanced diagnostic systems such as MRI, multi-slice CT, and angiography, and therapeutic options including thrombolytics, thrombectomy procedures, and long-term neurorehabilitation. These cost affects the low- and middle-income regions, where funding and reimbursement systems remain limited. Acute shortage of trained neurologists, radiologists, and rehabilitation experts, along with uneven distribution of stroke-ready facilities, further restrict access. These structural barriers reduce the utilization of advanced stroke solutions, slowing market expansion despite a rising global disease burden.

Expansion Potential in Emerging Markets and Underserved Regions

Rising stroke incidence in Asia Pacific, Latin America, and parts of the Middle East and Africa, driven by aging populations and increasing prevalence of hypertension, diabetes, and obesity, is creating substantial unmet demand for advanced stroke care. Several of these markets still lack widespread access to high-resolution imaging, acute therapies, and structured rehabilitation services. As governments and private providers expand stroke centers, emergency care capacity, and public health outreach, these regions represent a major growth frontier for diagnostics, therapeutics, and integrated stroke management solutions over the next decade.

Opportunities are expanding through innovations such as mobile stroke units, telemedicine-enabled diagnostics, and emerging point-of-care tools that support faster evaluation and treatment decisions. In parallel, next-generation neurorehabilitation solutions are gaining traction. For instance, the U.S. Food and Drug Administration (FDA)-approved Vivistim Paired VNS System uses a small implanted device that stimulates the vagus nerve in the neck during physical therapy. By pairing mild electrical pulses with targeted movements, this technology enhances neuroplasticity and helps chronic stroke survivors regain motor function beyond what standard therapy typically achieves. Such advanced rehabilitation technologies are poised to strengthen long-term recovery outcomes and create new value streams across stroke care.

Category-wise Analysis

Solution Type Insights

Diagnostics are likely to remain the leading segment, capturing approximately 56% of the stroke diagnostics and therapeutics market revenue share in 2026. The segment’s dominance is driven by the essential role of MRI, CT, cerebral angiography, ECG, and carotid ultrasound in the rapid identification of stroke type and severity. Improving imaging capacity, rising number of stroke admissions in emergency departments at hospitals, and greater integration of advanced imaging protocols continue to reinforce diagnostics as the primary revenue-generating category worldwide.

Therapeutics are set to represent the fastest-growing segment through 2033, supported by an estimated CAGR of around 7.8%. The demand for stroke therapeutics is increasing for tPA administration, anticoagulants and antiplatelets for secondary prevention, antihypertensives for risk control, and neurorehabilitation solutions as global stroke survival improves. Clinical guideline updates, expanding acute stroke centers, and improved access to post-stroke rehabilitation contribute to rapid adoption, gradually narrowing the gap between therapeutics and diagnostics.

Application Insights

Ischemic stroke is poised to be the leading application, accounting for about 63% of the global stroke cases, as per GBD 2019, translating into the largest share of diagnostic and treatment demand. Its dominance stems from the high prevalence of thrombotic and embolic events, necessitating CT, MRI, angiography, and evidence-based therapies such as tPA, thrombectomy, and antithrombotic regimens. With an enormous market share, this segment anchors the majority of clinical and commercial activity, and is likely to continue during the 2026-2033 forecast period.

Hemorrhagic stroke, though representing only about 15% of all stroke cases, is expected to grow at a notable pace in market terms due to an improved awareness of symptoms, faster emergency response systems, and wider adoption of imaging-based diagnostic protocols. These improvements allow more cases to be identified and treated promptly, driving higher utilization of diagnostics, interventions, and post-acute care services. As countries expand acute stroke infrastructure, the hemorrhagic segment shows accelerating uptake relative to prior years, outpacing growth in other application areas.

Regional Insights

North America Stroke Diagnostics and Therapeutics Market Trends

North America is likely to command an estimated 37.5% of the stroke diagnostics and therapeutics market share in 2026. The United States drives this dominance due to high stroke incidence among aging populations and strong access to advanced diagnostic tools such as MRI, CT, and cerebral angiography. The regional market benefits from a well-established network of certified stroke centers, rapid emergency medical services, and widespread adoption of thrombolytics, thrombectomy procedures, and comprehensive neurorehabilitation services. High healthcare spending and continuous investments in hospital capacity further reinforce North America’s leadership in the global stroke diagnostics and therapeutics landscape.

Supportive reimbursement policies and a mature regulatory environment help accelerate the adoption of new technologies, including AI-driven imaging analysis, portable diagnostic tools, and minimally invasive treatment options. Major medical device manufacturers and pharmaceutical companies operate extensive R&D and commercialization activities in the region, strengthening competitive intensity. Continuous updates to clinical guidelines and growing penetration of mobile stroke units enhance early treatment rates. Innovation-driven ecosystem, high per-capita healthcare spending, and strong infrastructure of North America ensure it remains the largest and most advanced market globally.

Europe Stroke Diagnostics and Therapeutics Market Trends

Europe is likely to hold around 27% of the global market share in 2026, aided by the robust and well-functioning healthcare systems of Germany, the United Kingdom, France, and Spain. Healthcare facilities in these countries are known for their wide adoption of CT and MRI imaging, evidence-based stroke protocols, and structured rehabilitation programs. Germany and France lead in diagnostic imaging capacity, while the U.K. and Spain contribute significantly through expanding stroke care networks and systematic investment in post-acute rehabilitation. Europe’s strong public health infrastructure and standardized clinical guidelines support steady utilization of both diagnostic and therapeutic solutions across diverse healthcare environments.

European Union (EU)-wide regulatory harmonization enables faster adoption of medical technologies, including AI-enabled imaging platforms and portable diagnostic tools. Public health campaigns focusing on prevention, early detection, and rehabilitation are improving stroke outcomes and driving consistent demand for stroke care services. However, growth remains moderate due to budget limitations in public reimbursement systems and differences in access between urban and rural areas. Despite these constraints, Europe continues to emphasize integrated care pathways, preventive screening, and improved rehabilitation availability, supporting a stable long-term growth outlook across the region.

Asia Pacific Stroke Diagnostics and Therapeutics Market Trends

Asia Pacific is expected to be the fastest-growing regional market for stroke diagnostics and therapeutics, accounting for around 28.5% of the global market demand in 2026. This growth is bolstered by rising stroke incidence, aging populations, and increasing prevalence of risk factors such as hypertension and diabetes. The regional market is expected to expand speedily as local healthcare systems scale up stroke diagnostics, emergency care, and rehabilitation capacity. China, India, and Southeast Asian nations are strengthening hospital infrastructure, adding new stroke units, and adopting CT/MRI-based early diagnostic technologies. The growing use of telemedicine and AI-powered imaging tools is particularly important for reaching underserved and rural populations, further accelerating market uptake.

Growth is also driven by strong national health strategies and regional public-health commitments. For example, India’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS), active since 2010, continues to evolve, with experts recommending that it emphasize broader collaboration with local physicians and expanded public–private partnerships to improve stroke detection and treatment access. Similarly, the World Health Organization (WHO) South-East Asia Region (SEAR) NCD Action Plan supports member countries in working toward a 25% reduction in premature NCD mortality by 2025, with stroke prevention and management embedded as a priority. These initiatives, combined with manufacturing advantages and improving regulatory pathways, position the Asia Pacific as a high-potential region for integrated acute and post-acute stroke care solutions.

Competitive Landscape

The global stroke diagnostics and therapeutics market landscape is dominated by major global players such as Siemens Healthineers, Philips Healthcare, Abbott Laboratories, GE Healthcare, Medtronic, Stryker, Boston Scientific, and MicroTransponder. These companies lead through a combination of advanced imaging solutions, innovative thrombolytic and anticoagulant therapies, and comprehensive neurorehabilitation technologies. Strengths include integrated product portfolios, strong R&D pipelines, and regulatory approvals across multiple regions, and partnerships with hospitals and healthcare networks to ensure widespread adoption. Continuous innovation in AI-enabled imaging, minimally invasive interventions, and evidence-based therapeutic protocols reinforces their competitive positioning.

In Asia Pacific, inchoate players, including Mindray, Shenzhen Mindray Bio-Medical, Terumo, and local neurorehabilitation device manufacturers, are expanding capacity to meet growing regional demand. Advantages include lower operational costs, local manufacturing, and proximity to emerging patient populations. Many are investing in portable diagnostics, AI-assisted imaging platforms, and telemedicine-enabled stroke care solutions to enhance market presence. Increased public and private healthcare spending, infrastructure expansion, and collaborations with international technology providers are strengthening competition and accelerating the adoption of advanced stroke diagnostics and therapeutics across the region.

Key Industry Developments

- In December 2025, Brainomix published a landmark study in Lancet Digital Health that demonstrated that its AI imaging platform (Brainomix 360 Stroke) doubled endovascular thrombectomy (EVT) rates at deployment sites compared to a 63% increase at non-deployment sites. The AI software was associated with improved patient outcomes (reduced disability at discharge), faster treatment decisions, and a 99% increase in intravenous thrombolysis rates.

- In November 2025, Lumosa Therapeutics’ Odatroltide (LT3001), an investigational drug combining thrombolytic and neuroprotective mechanisms, demonstrated safety and efficacy in Phase 2b trials with a 7.3% higher rate of functional independence at 90 days, most notably providing treatment benefit within an extended 24-hour window. The drug showed no treatment-related symptomatic intracranial hemorrhage and delivered particularly strong results in patients with disabling strokes with arm motor drift.

- In October 2025, Prolong Pharmaceuticals announced positive Phase 1/2 data (HEMERA-1 trial) for PP-007, a PEGylated carboxyhemoglobin bovine product used adjunctively with standard thrombectomy in anterior large vessel occlusion (A-LVO) acute ischemic stroke patients. The drug received FDA Fast Track Designation and showed improved functional outcomes and reduced mortality compared to mechanical thrombectomy alone, supporting advancement to the Phase 2b HEMERA-2 pivotal trial.

Companies Covered in Stroke Diagnostics and Therapeutics Market

• Siemens AG

• GE Healthcare

• Koninklijke Philips N.V. (Philips Healthcare)

• Medtronic plc

• Stryker Corporation

• Boston Scientific Corporation

• Abbott Laboratories

• Cordis Corporation

• MicroTransponder

• Merck and Co., Inc.

• Genentech, Inc.

Frequently Asked Questions

The global stroke diagnostics and therapeutics market is projected to reach US$ 43.8 billion in 2026.

Key market drivers include increasing stroke prevalence, adoption of advanced imaging, thrombolytic and anticoagulant therapies, and expanding neurorehabilitation services.

The market is poised to witness a CAGR of 7.8% between 2026 and 2033.

Expansion of advanced stroke care solutions in emerging markets, AI-enabled diagnostics, portable imaging solutions, and integrated acute-to-long-term stroke care are key market opportunities.

Siemens, GE Healthcare, Philips, Medtronic, Stryker, and Boston Scientific are some of the key players in the market.