- Healthcare Services

- Telestroke Services Market

Telestroke Services Market Size, Share, and Growth Forecast, 2026 – 2033

Telestroke Services Market by Stroke Type (Ischemic Stroke, Others), Deployment Type (Cloud-Based, On-Premises, Web/Mobile-Based), Application (Counseling, Diagnosis, Monitoring, Emergency Services, Treatment, Post-Stroke Follow-Up & Rehabilitation, Others), and Regional Analysis for 2026 - 2033

Telestroke Services Market Share and Trends Analysis

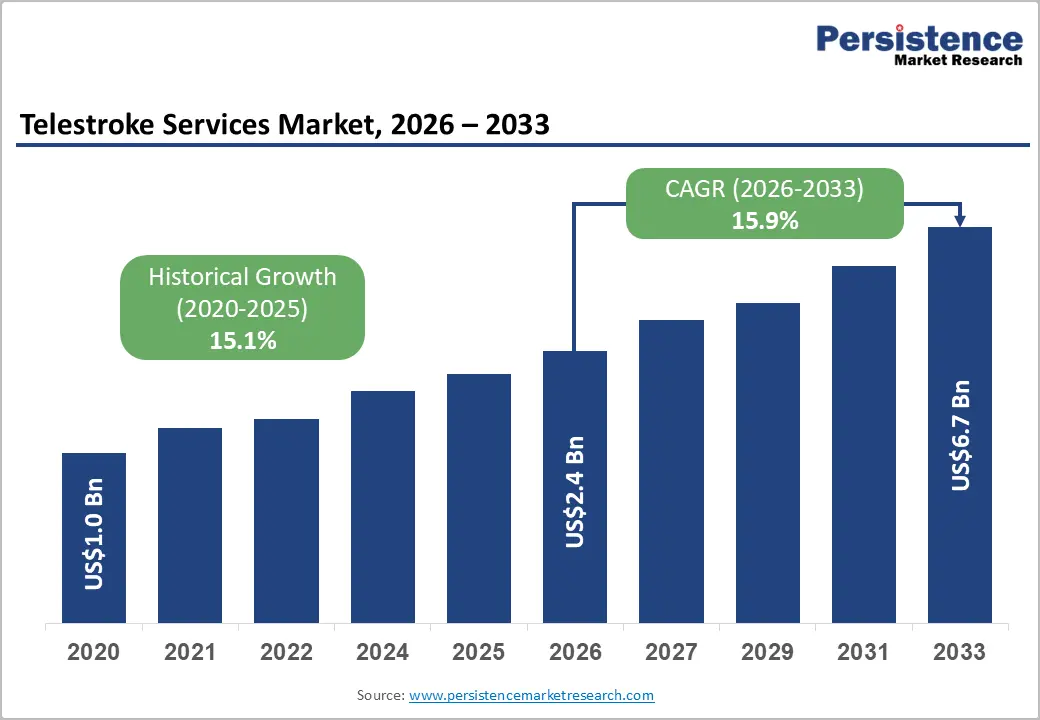

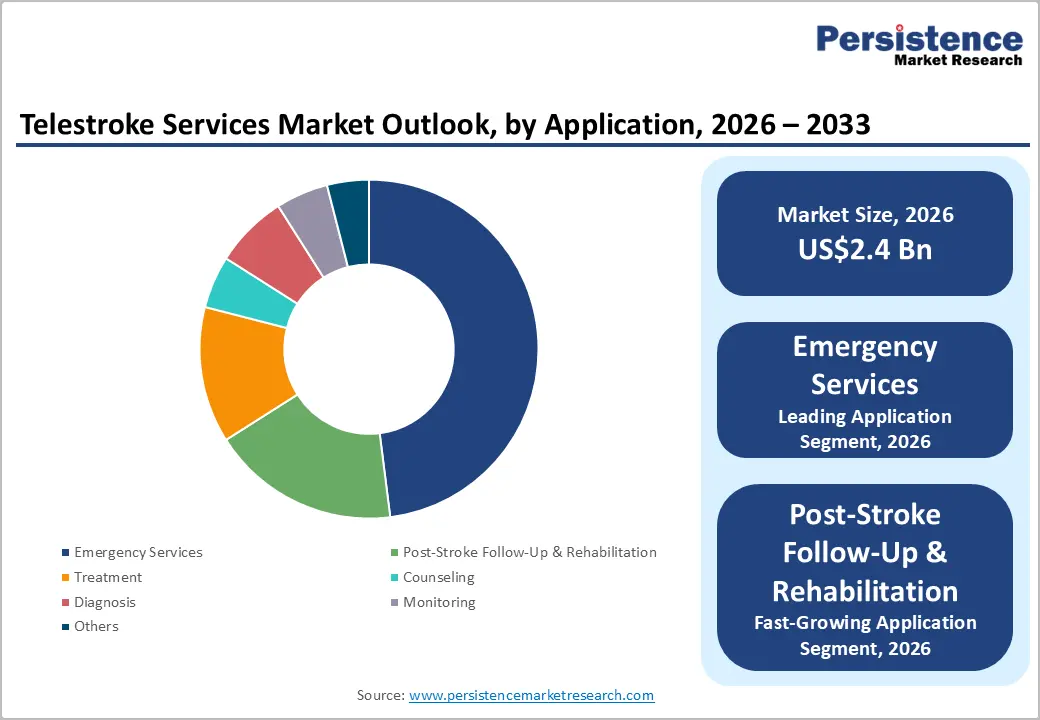

The global telestroke services market size is likely to be valued at US$2.4 billion in 2026 and is estimated to reach US$6.7 billion by 2033, growing at a CAGR of 15.9% during the forecast period from 2026 to 2033, driven by rising stroke incidence, expanding telehealth reimbursement frameworks, and rapid integration of remote neurological assessment technologies.

Growing aging populations and increasing prevalence of ischemic stroke are accelerating demand for rapid specialist access across emergency care networks. Cloud-enabled imaging transfer systems and artificial intelligence-supported triage platforms are improving treatment decision timelines in acute stroke management.

Key Industry Highlights

- Leading Stroke Type: Ischemic stroke is set to hold around 72% market share in 2026, driven by elevated global disease prevalence and the critical clinical need for rapid thrombolytic evaluation.

- Fastest-Growing Stroke Type: Transient ischemic attack is projected as the fastest-growing segment, supported by an increasing clinical focus on preventive neurology and secondary prevention frameworks.

- Leading Application: Emergency services are estimated to hold roughly 48% market share in 2026, due to the urgent nature of acute cerebrovascular treatments.

- Fastest-Growing Application: Post-stroke follow-up & rehabilitation is forecast to record the fastest growth, driven by the rising adoption of continuous remote patient monitoring and long-term restorative care models.

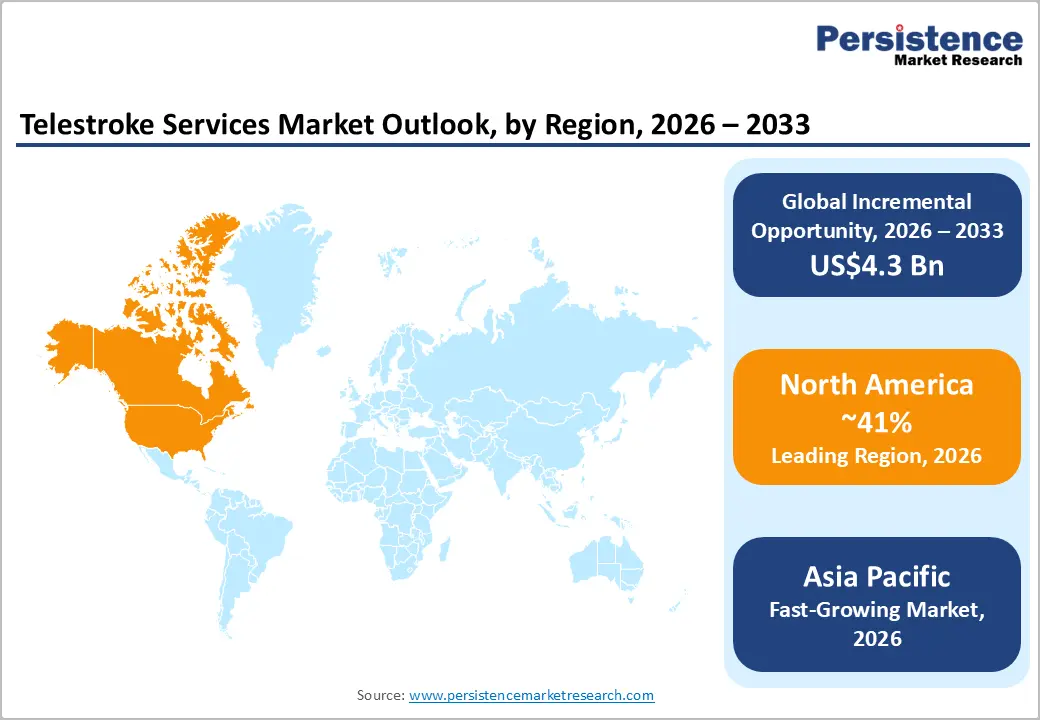

- Regional Leadership: North America is projected to capture roughly 41% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding rural healthcare infrastructure and proactive digital health policies.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Access TeleCare, LLC, and TeleSpecialists, LLC leveraging specialized physician networks, software compatibility, and deployment scale to maintain competitive positioning.

- Innovation Trends: Technological advancements in automated neuroimaging evaluation algorithms, mobile stroke unit connectivity, and cloud-native application programming interfaces are shaping long-term market evolution and investment direction.

DRO Analysis

Driver - Expansion of Stroke Burden and Time-Critical Care Requirements

Stroke prevalence continues to increase due to aging demographics, hypertension, obesity, and cardiovascular disorders, creating substantial demand for rapid neurological consultation systems. According to the Centers for Disease Control and Prevention (CDC), more than 795,000 individuals experience stroke annually in the U.S., while nearly 87% of cases are ischemic stroke. Rising emergency admissions are compelling hospitals to implement continuous remote neurologist availability to reduce door-to-needle treatment intervals.

Emergency departments located in rural and mid-sized healthcare facilities often face neurologist shortages, limiting immediate stroke diagnosis capabilities. Telestroke platforms improve specialist accessibility through remote imaging interpretation and real-time consultation support, leading to faster thrombolytic intervention decisions. Integration of video-enabled clinical workflows with emergency response infrastructure is improving treatment standardization across distributed healthcare systems. Healthcare providers are increasingly prioritizing virtual neurological care expansion to reduce long-term disability costs and intensive care utilization.

Restraint - Limited Neurologist Availability and Workforce Distribution Challenges

Specialized neurologist shortages continue to restrict the scalability of continuous telestroke consultation networks, particularly across smaller hospitals and rural healthcare facilities. Many providers struggle to maintain 24/7 stroke specialist coverage due to workforce limitations and high operational costs. Insufficient staffing availability increases consultation turnaround times, affecting treatment efficiency and clinical responsiveness during emergency stroke cases.

High compensation requirements for vascular neurologists and emergency consultation specialists increase operational expenditure for healthcare systems implementing remote stroke programs. Smaller hospitals face margin pressure due to subscription fees, technology integration expenses, and specialist contracting costs. Limited reimbursement consistency across private insurance networks also creates uncertainty regarding long-term scalability and investment returns.

Opportunity - Artificial Intelligence Integration in Stroke Triage and Imaging

Artificial intelligence-supported stroke imaging analysis is creating major opportunities for improving clinical decision speed and treatment prioritization. Automated large vessel occlusion detection tools and imaging triage systems can accelerate neurologist evaluation workflows, enabling hospitals to manage higher consultation volumes efficiently. Integration of predictive analytics within telestroke platforms can improve prioritization of emergency interventions and optimize thrombolytic treatment pathways.

Technology providers are expanding partnerships with hospitals to integrate artificial intelligence-enabled imaging software into remote neurological consultation systems. Cloud-native architectures are enabling scalable deployment across multi-hospital networks without extensive hardware investment. Regulatory focus on reducing stroke disability rates is encouraging the adoption of advanced diagnostic automation tools within emergency care environments. Commercial vendors are also developing mobile-enabled physician collaboration interfaces to improve specialist accessibility during critical care scenarios.

Category-wise Analysis

Stroke Type Insights

Ischemic stroke is anticipated to secure around 72% of the telestroke services market share in 2026, reflecting elevated global disease prevalence and the critical clinical need for rapid thrombolytic evaluation. Local hospitals utilize remote networks to clear patients for tissue plasminogen activator injections within narrow therapeutic windows. The high volume of blockages ensures dominant resource allocation.

Transient ischemic attack (TIA) is expected to be the fastest-growing segment, propelled by an increasing clinical focus on preventive neurology and secondary prevention frameworks. Outpatient clinics deploy remote monitoring services immediately following minor events to prevent full-scale secondary neurological injuries. Early proactive monitoring prevents severe long-term institutional burdens.

Deployment Type Insights

Cloud-based deployments are poised to dominate with a forecast market share of over 55% in 2026, powered by structural demands for enterprise elasticity, rapid image transfer, and lower upfront capital expenses. Multi-facility healthcare systems utilize centralized cloud infrastructure to route diagnostic data securely to remote specialists. Cloud setups eliminate localized server infrastructure limitations.

On-premises deployment is estimated to be the fastest-growing segment, fueled by strict institutional data privacy regulations and security requirements within major hospital groups. Large public medical centers invest in internal server networks to retain absolute control over sensitive patient records. Local hosting mitigates external network dependency vulnerabilities.

Application Insights

Emergency services are likely to be the leading segment with a projected 48% of the telestroke services market share in 2026 due to the urgent nature of acute cerebrovascular treatments. Community emergency rooms connect with remote stroke centers to execute immediate diagnostic protocols during initial admissions. Acute stabilization remains the primary driver of institutional spending.

Post-stroke follow-up & rehabilitation is anticipated to be the fastest-growing segment, fueled by the rising adoption of continuous remote patient monitoring and long-term restorative care models. Specialized rehabilitation centers utilize remote video links to guide physical therapy sessions within patients' homes. Continuous oversight improves long-term functional recovery metrics.

Regional Insights

North America Telestroke Services Market Trends

North America is expected to lead with an estimated 41% of the telestroke services market share in 2026, supported by established hub-and-spoke clinical structures and favorable public reimbursement frameworks. Widespread technology integration across regional hospital groups optimizes acute consultation delivery workflows. Advanced health informatics regulations ensure high data standards across public and private provider systems.

U.S. Telestroke Services Market Insights

The U.S. market is projected to capture around 86% of the North American regional market share in 2026 due to consistent updates in federal reimbursement pathways for remote critical care interventions. High commercial investments from private healthcare groups facilitate the deployment of artificial intelligence software across rural emergency networks.

Canada Telestroke Services Market Insights

The Canada market is forecast to account for nearly 11% of the regional market share in 2026, as provincial healthcare systems prioritize remote clinical options to serve geographically isolated populations. Public health funding increases targeted technology integration within community hospitals lacking on-site neurological specialists. Government initiatives standardize emergency triage procedures nationwide.

Europe Telestroke Services Market Trends

Europe is expected to secure the second-largest global position with an estimated 28% market share in 2026, driven by structural adjustments aimed at harmonizing cross-border digital emergency medicine frameworks. National health initiatives prioritize the reduction of door-to-needle times through remote diagnostic support networks.

Germany Telestroke Services Market Insights

Germany is expected to generate approximately 24% of the European market revenue in 2026, driven by the implementation of standardized digital health applications within institutional emergency pathways. Investments from municipal hospital groups accelerate the deployment of secure on-premises data setups. Public-private partnerships expand technical capabilities within metropolitan stroke centers.

U.K. Telestroke Services Market Insights

The U.K. market is likely to contribute around 19% of the European market revenue in 2026, influenced by National Health Service modernizations focusing on centralized remote emergency routing systems. Structural realignments optimize acute neurological interventions via regional virtual consultation centers. Staff shortage pressures accelerate the integration of automated image analysis tools.

Asia Pacific Telestroke Services Market Trends

Asia Pacific is forecast to be the fastest-growing market for telestroke services, stimulated by expanding rural healthcare infrastructure and proactive digital health policies. Rising investments in telecommunication networks enable consistent real-time diagnostic audio-visual feeds. Expanding middle-class demographics increase total utilization rates of private emergency medical facilities.

China Telestroke Services Market Insights

The China market is anticipated to claim about 32% of the Asia Pacific regional market share in 2026, due to centralized government mandates focused on upgrading tier-two and tier-three rural medical centers. Significant capital allocations from state bodies drive the deployment of cloud-based emergency diagnostic networks. Local software developers expand domestic market footprints through enterprise platform rollouts.

India Telestroke Services Market Insights

The India market is expected to achieve around 22% of the Asia Pacific regional market share in 2026, as private hospital networks expand specialized clinical access into tier-two and tier-three cities. High mobile network penetration allows the implementation of low-bandwidth remote assessment applications. Private healthcare systems drive investment in affordable hub-and-spoke setups.

Competitive Landscape

The global telestroke services market is moderately fragmented, with specialized virtual care organizations and diversified digital health systems competing for institutional emergency network contracts. Market participants focus on software compatibility, diagnostic speed, and compliance with data security laws to secure multi-year hospital system partnerships.

The competitive landscape features a distinct mix of dominant players, including Access TeleCare, LLC, TeleSpecialists, LLC, Eagle Telemedicine, Amwell, and Sevaro Health, Inc. Strategic positioning depends heavily on the scale of available specialist networks and the integration of advanced image processing algorithms. Companies expand their market presence by connecting local community clinics to centralized pools of board-certified vascular neurologists.

Key Industry Developments:

- In February 2026, Intermountain Children’s Health launched the nation’s largest pediatric telestroke network across 24 hospitals in Utah and southern Idaho, reinforcing rapid remote stroke diagnosis and emergency neurological care access for children.

- In May 2025, TeleSpecialists, LLC achieved a perfect National Committee for Quality Assurance reaccreditation score, reinforcing clinical quality standards and operational excellence within telestroke and telemedicine service delivery.

Companies Covered in Telestroke Services Market

- Access TeleCare, LLC

- TeleSpecialists, LLC

- Eagle Telemedicine

- Amwell

- Sevaro Health, Inc.

- AmplifyMD

- Teladoc Health, Inc.

- Blue Sky Telehealth

- RapidAI

- Viz.ai, Inc.

- Brainomix

- Chanyxo Telehealth

Frequently Asked Questions

The telestroke services market is projected to reach US$2.4 billion in 2026.

Rising global stroke incidence, increasing neurologist shortages, expanding telehealth reimbursement policies, and growing adoption of cloud-based emergency consultation platforms are driving the telestroke services market.

The telestroke services market is poised to witness a CAGR of 15.9% from 2026 to 2033.

Expansion of artificial intelligence-enabled stroke triage, rural telemedicine networks, mobile neurological consultation platforms, and remote post-stroke rehabilitation services is creating key opportunities in the telestroke services market.

Some of the key market players include Access TeleCare, LLC, TeleSpecialists, LLC, Eagle Telemedicine, Amwell, and Sevaro Health, Inc.