- Automotive Components & Materials

- Steering Column Locks Market

Steering Column Locks Market Size, Share, and Growth Forecast, 2026-2033

Steering Column Locks Market by Product Type (Mechanical Locks, Electronic Locks, Hybrid Locks), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), Sales Channel (OEMs, Aftermarket), and Regional Analysis for 2026-2033

Steering Column Locks Market Share and Trends Analysis

The global steering column locks market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 6.3% during the forecast period of 2026–2033.

This growth is expected to be driven by increasing focus on vehicle safety standards, and connected vehicle architecture is accelerating the transition from mechanical to hybrid and electronic steering column lock systems. The trajectory of the market also reflects structural shifts in automotive design, where steering column locks are increasingly integrated into broader vehicle access and immobilization systems. Automakers are embedding electronic steering locks within body control modules to enhance theft prevention and ensure compliance with evolving safety regulations. Emerging markets are implementing stricter homologation standards, making factory-installed locking systems mandatory across vehicle categories. The expansion of connected vehicle ecosystems is encouraging system-level security upgrades, thereby raising the value contribution of advanced steering lock technologies within modern vehicle platforms.

Key Industry Highlights

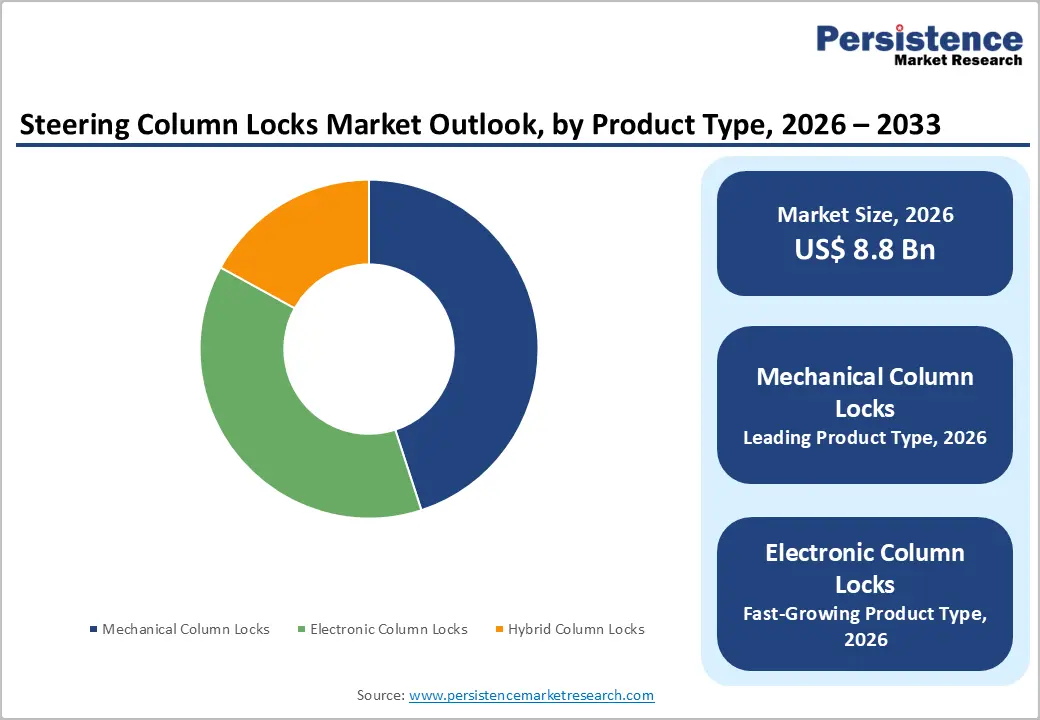

- Dominant Product Type: Mechanical locks are set to command around 45% revenue share in 2026, while electronic locks are likely to register an approximate 2026-2033 CAGR of 8%, driven by increasing connected vehicle integration.

- Leading Vehicle: Passenger vehicles are projected to account for nearly 70% of market revenues in 2026, supported by high production volumes and mandatory anti-theft compliance.

- Dominant Sales Channel: Original equipment manufacturer (OEM) installations are expected to hold over 80% revenue share in 2026, while the aftermarket segment is likely to grow steadily through 2033 due to vehicle parc expansion.

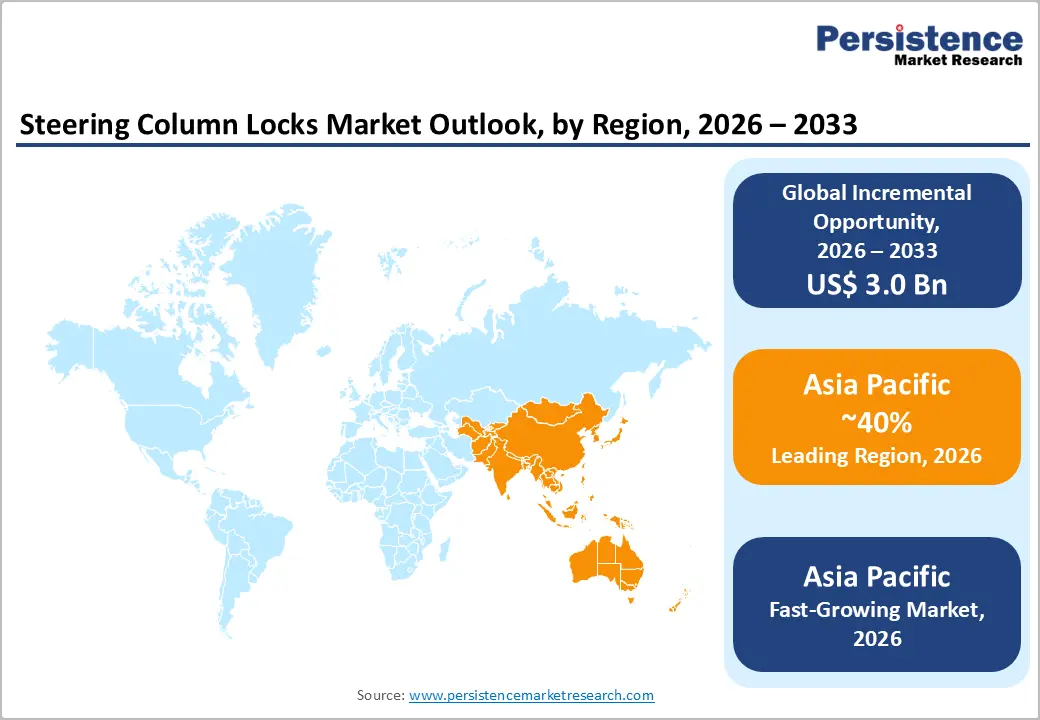

- Regional Leadership: Asia Pacific is anticipated to capture about 40% market share in 2026 and record the fastest growth through 2033, backed by strong automotive manufacturing output.

- Competitive Environment: Player strategies focus on electronic integration, EV platform alignment, capacity expansion in Asia and Europe, and long-term OEM supply agreements.

| Report Attribute | Details |

|---|---|

|

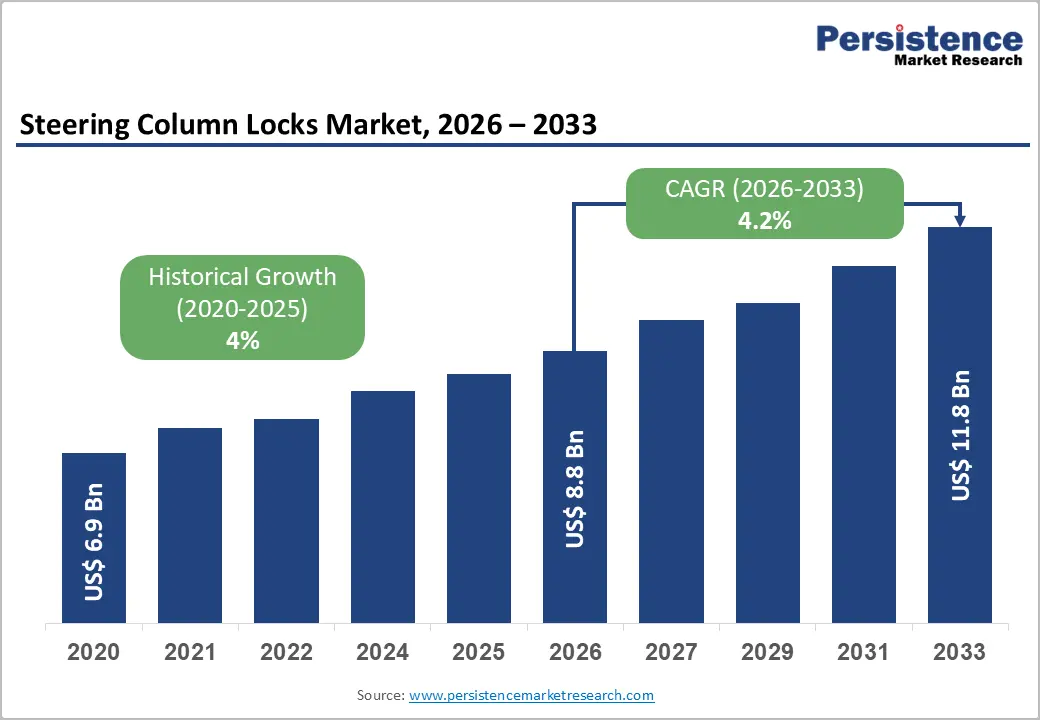

Steering Column Locks Market Size (2026E) |

US$ 8.8 Bn |

|

Market Value Forecast (2033F) |

US$ 11.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Vehicle Production and Strengthening Safety Regulations

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production recovered to over 93 million units in 2023, reflecting structural recovery post-pandemic. Regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) and the European Commission (EC) mandate anti-theft compliance under Federal Motor Vehicle Safety Standards (FMVSS 114) and UN Economic Commission for Europe (UNECE) regulations. These frameworks require vehicles to incorporate mechanisms that prevent unauthorized movement when the ignition key is removed. As emerging economies harmonize with global homologation standards, compliance requirements increasingly influence design specifications across segments. This regulatory consistency sustains baseline demand for steering column lock systems across both legacy and modern platforms.

During 2025–2026, regulatory movements have reinforced safety priorities. For example, China’s Ministry of Industry and Information Technology issued new draft automotive safety regulations emphasizing physical safety and control system robustness, directly affecting steering systems and associated safety hardware (including locking-related controls) from 2027 onward. Pakistan’s Ministry of Industries and Production enforced updated vehicle quality and safety standards that include enhanced control and structural requirements applicable to locking mechanisms installed in both locally manufactured and imported vehicles. These government-backed moves illustrate a global regulatory trend toward increasingly rigorous safety enforcement, further solidifying steering column lock integration as a key compliance element for OEMs.

Transition Toward Electronic Locking and Rising Anti-Theft Security Focus

The shift toward electronic steering locks aligns with broader vehicle electrification and digital architecture. Over 70% of new passenger vehicles sold in developed markets now incorporate electronic key or keyless entry systems. Electronic and hybrid steering locks integrate with body control modules (BCM), enabling remote locking, immobilization, and theft detection. This increases system value per vehicle by 1.5x–2x compared to mechanical systems. As connected vehicles are projected to exceed 400 million globally by 2030, integration-driven revenue expansion is expected to outpace vehicle production growth. The move toward software-enabled vehicle platforms is reinforcing the relevance of advanced locking mechanisms as part of holistic vehicle cybersecurity architecture.

Major vehicle theft data in the United States shows persistent high rates of theft for popular models, prompting heightened attention on anti-theft solutions and vehicle security features. Additionally, public safety initiatives such as the Colorado State Patrol’s distribution of free steering wheel locks reflect growing awareness and community-level demand for effective lock-based deterrents. These developments, supported by official data and enforcement actions, highlight how elevated awareness of theft risk continues to drive adoption of enhanced security systems, particularly electronic locking, as OEMs and regulatory bodies respond to both threats and consumer expectations.

Climbing Electronic Component Costs and Supply Chain Volatility

The automotive semiconductor shortages continued to affect Tier-1 suppliers. Electronic steering column locks require microcontrollers and actuators, increasing bill-of-materials costs by 20–30% compared to mechanical locks. Cost pressure is particularly evident in price-sensitive markets such as India and ASEAN, limiting rapid electronic penetration in entry-level vehicles. Volatile lead times and export restrictions have further tightened component availability. In 2025, supply disruptions linked to semiconductor trade controls in Europe and China were widely reported by Reuters, with automakers warning about production instability. Such uncertainties increase procurement costs, extend planning cycles, and constrain margin flexibility for electronic lock manufacturers.

Electronic lock systems also depend on precision motors, sensors, and integrated circuit boards vulnerable to logistics bottlenecks and currency fluctuations. Media reports in 2025 highlighted how global chipmakers rerouted automotive shipments due to regulatory disputes, raising sourcing complexity for OEMs. These conditions force suppliers to maintain higher inventory buffers, increasing working capital requirements. OEMs in cost-competitive segments often delay electronic upgrades to preserve pricing stability. As a result, adoption in entry and mid-segment vehicles progresses more gradually. Persistent supply chain fragility therefore remains a structural restraint on accelerated electronic lock penetration.

Vehicle Electrification Architecture Reducing Mechanical Dependencies

Battery electric vehicles (BEVs) increasingly adopt shift-by-wire and electronic steering architectures. Some next-generation platforms integrate centralized electronic immobilization systems, potentially reducing reliance on traditional column lock hardware. This structural shift may moderate long-term mechanical segment growth, especially in premium EV platforms launched in 2025. EV architectures emphasize software-driven control and reduced mechanical linkages. As domain controllers consolidate multiple vehicle functions, discrete mechanical locking components face reduced design priority. This architectural transformation reshapes component demand patterns.

In 2025, major automakers accelerated platform standardization strategies to support EV scalability and software integration, as reported by leading financial news outlets. National EV incentive frameworks in the U.S. and China increasingly emphasize advanced electronic control and cybersecurity compliance. This regulatory and technological alignment favors integrated electronic immobilization over purely mechanical mechanisms. While anti-theft requirements remain mandatory, compliance pathways are evolving toward digital authentication systems. Consequently, mechanical-focused suppliers must diversify into electronic integration to remain competitive. Without adaptation, long-term growth prospects for traditional mechanical lock systems may gradually moderate.

Expansion in Emerging Automotive Markets and Aftermarket Replacement Demand

India and ASEAN vehicle production expanded by over 7% year-on-year in 2024, as per industry associations. Surging middle-class vehicle ownership presents incremental OEM installation opportunities. Asia Pacific is projected to contribute over 45% of incremental market revenue between 2026–2033, representing a significant opportunity for cost-optimized hybrid lock systems. In February 2026, for example, Tata Motors inaugurated its Ranipet facility in Tamil Nadu, expanding EV-ready manufacturing capacity and strengthening domestic component demand, as reported by The Times of India. Such capacity additions reinforce OEM sourcing requirements for steering column lock systems across vehicle categories.

Vehicle parc expansion globally supports aftermarket lock replacement. Average vehicle age in the U.S. surpassed 12.5 years in 2024, increasing mechanical lock wear and replacement frequency. In 2026, ahead of the Union Budget, the Government of India expanded funding under the PM E-DRIVE scheme, allocating Rs 2,000 crore to accelerate EV infrastructure development, as reported by Moneycontrol. Infrastructure expansion typically stimulates overall vehicle ecosystem growth, including service networks and repair markets. As older vehicles remain in operation longer, replacement demand for steering lock systems strengthens recurring revenue streams. This dual OEM-aftermarket dynamic enhances long-term growth visibility.

Integration with Connected Vehicle and Electronic Security Platforms

Automakers increasingly integrate steering locks with telematics and remote immobilization systems. Partnerships between Tier-1 suppliers and EV startups in 2025 accelerated system-level integration, embedding locking functionality within broader electronic control architecture. Electronic locks are expected to grow at 8–9% CAGR, outpacing overall market growth through 2033. In early 2026, the U.S. NHTSA conducted public discussions on automated vehicle safety and electronic control systems, highlighting regulatory attention toward digitally integrated vehicle safety frameworks. This regulatory emphasis strengthens demand for advanced electronic locking mechanisms within connected vehicle platforms.

Connected vehicle deployment continues to receive institutional support. The U.S. Department of Transportation (DOT) previously awarded nearly US$ 60 million in grants to advance connected and automated vehicle technologies, reinforcing telematics integration across new vehicles. Government-backed EV expansion policies in India and the United States further encourage centralized electronic architectures compatible with remote access control. As vehicle software ecosystems mature, steering column locks evolve from standalone mechanical devices to integrated security nodes. This convergence of connectivity, cybersecurity focus, and electrification presents sustained technology-driven growth opportunities for advanced lock manufacturers.

Category-wise Analysis

Product Type Insights

Mechanical steering locks are projected to account for about 45% of market share in 2026, remaining the dominant choice in entry- and mid-range vehicles due to their cost effectiveness and widespread adoption. Their continued relevance is evident in 2025 launches such as the Mahindra Bolero Neo facelift, which retained traditional mechanical systems while updating safety and infotainment features, aligning with value-oriented consumer expectations. Mechanical systems also benefit from regulatory mandates that require physical anti-theft devices across basic vehicle classes in many emerging markets. Their straightforward integration and proven reliability support sustained volume demand. However, value creation through advanced connectivity and digital safety features is limited compared with electronic alternatives, tempering growth potential in higher-end segments as automotive technology evolves.

Electronic steering locks are expanding rapidly, with an estimated 8% CAGR through 2033, underpinned by increased adoption of keyless entry and integrated vehicle electronics. The 2025 Tata Harrier EV launch in India exemplifies this shift: as a next-gen EV platform, it includes advanced electronic systems and connected car features, making electronic lock integration a standard safety and security component. The higher unit value of electronic systems, combined with stronger alignment to vehicle control units and telematics, drives value growth. OEMs increasingly specify these advanced mechanisms in mid- to premium vehicles as part of digital access and immobilization strategies. Emerging in-vehicle software ecosystems and remote safety updates further reinforce their growth prospects, positioning electronic locks ahead of traditional mechanical counterparts in long-term segment expansion.

Vehicle Type Insights

Passenger vehicles are set to lead with around 70% of the steering column locks market revenue share in 2026, driven by stable production volumes and strong consumer demand. A recent example is the Maruti Suzuki Victoris subcompact SUV, launched in 2025 with advanced safety ratings and connected features, reflecting the broader trend toward integrating security and convenience technologies in new passenger models. Urbanization and rising disposable incomes in Asia Pacific and other key markets continue to fuel private car sales, with OEMs embedding steering column locks as standard safety equipment. Regulatory frameworks in major markets also prioritize comprehensive anti-theft systems in passenger vehicles. This segment’s sheer volume ensures it remains the primary driver of market revenue, with continued opportunities in both mechanical and electronic lock adoption as vehicle technology evolves.

Commercial vehicles, while representing a smaller share, are slated to show steady expansion alongside logistics and fleet modernization trends. The emergence of dedicated electric and purpose-built commercial platforms, such as the Kia PV5 electric van in 2025, highlights the segment’s evolution toward electrification and advanced vehicle electronics, which includes higher-spec locking and immobilization systems. As businesses emphasize cargo security and operational efficiency, demand for reliable steering lock systems, both mechanical and electronic, strengthens across commercial fleets. Integration with telematics and fleet management systems adds value beyond basic theft prevention. These developments encourage incremental volume growth in the commercial segment, supporting diversification of demand beyond passenger vehicles and reinforcing the overall resilience of the steering column lock market.

Regional Insights

North America Steering Column Locks Market Trends

North America remains a mature and technologically advanced market for steering column locks, led by the United States. Regulatory oversight by the NHTSA mandates strict anti-theft compliance, ensuring consistent integration across vehicle categories. High vehicle ownership levels and an average vehicle age exceeding 12 years support both OEM installations and steady aftermarket demand. Electronic steering lock penetration is notably higher than the global average due to the region’s strong premium vehicle mix. The presence of established Tier-1 suppliers with vertically integrated operations further strengthens supply stability.

Investment trends increasingly focus on smart electronic lock modules integrated with telematics and connected vehicle platforms. Federal industrial policies encouraging domestic EV production are reinforcing demand for advanced security components. Growth is projected to remain stable through 2033, driven primarily by technological upgrades rather than volume expansion. While North America is not the fastest-growing region, it stands out for its high-value product mix and strong regulatory framework supporting electronic lock adoption.

Europe Steering Column Locks Market Trends

Europe represents a structurally stable market for steering column locks, supported by well-established and legacy automotive manufacturing hubs in Germany, the United Kingdom, France, and Spain. Regulatory harmonization under the UNECE ensures consistent enforcement of anti-theft and safety standards across the region. Germany anchors OEM demand with its extensive vehicle production base, while the U.K. contributes significantly through its well-developed aftermarket sector. Compliance-driven adoption ensures steady baseline demand for steering column locking systems across vehicle segments.

Rapid electrification across European markets is accelerating integration of electronic steering lock modules within next-generation vehicle platforms. Sustainability regulations and digital transformation initiatives are encouraging innovation in lightweight and electronically controlled security systems. Growth in Europe remains moderate, aligned with steady vehicle production levels and strong regulatory oversight. Although not the largest regional contributor, Europe remains highly influential due to its regulatory leadership and concentration of advanced automotive R&D capabilities.

Asia Pacific Steering Column Locks Market Trends

Asia Pacific is forecasted to secure approximately 40% of the steering column locks market share in 2026. China, Japan, India, and ASEAN countries collectively drive large-scale vehicle production and component manufacturing. China’s extensive automotive ecosystem supports high-volume mechanical and hybrid lock production, while India’s expanding passenger vehicle base generates incremental OEM demand. Japan continues to lead in electronic lock innovation and integration within advanced vehicle systems. Strong domestic manufacturing incentives further enhance regional competitiveness.

Asia Pacific is also poised to be the fastest-growing regional market for steering column locks, projected to expand at an estimated 8% CAGR through 2033. Cost competitiveness, localized supply chains, and rising vehicle ownership underpin sustained volume growth. Rapid electrification in China and India is accelerating electronic lock adoption, while ASEAN markets contribute emerging demand. The combination of production scale, regulatory evolution, and growing consumer purchasing power positions Asia Pacific as the primary growth engine of this market over the 2026-2033 forecast period.

Competitive Landscape

The global steering column locks market structure is moderately consolidated, with leading Tier-1 automotive suppliers such as Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, and DENSO Corporation controlling a significant share of global OEM revenue. These companies leverage long-standing relationships with global automakers, integrated electronic architecture expertise, and vertically aligned manufacturing capabilities. Their competitive strength lies in delivering both mechanical and electronically controlled steering lock modules aligned with evolving vehicle security standards. Continuous investment in R&D enables integration with keyless entry systems, body control modules, and EV-specific platforms.

Specialized and regional players such as Mitsubishi Electric Corporation and Valeo focus on electronic immobilization systems and advanced vehicle access technologies, particularly in Europe and Asia Pacific. Entry barriers remain high due to strict automotive validation processes, OEM approval cycles, and functional safety compliance requirements. However, increasing vehicle digitalization is encouraging collaboration between traditional hardware manufacturers and software-focused automotive security firms. Over the forecast period, competitive intensity is expected to rise as global suppliers expand electronic portfolios, pursue platform-based standardization, and strengthen partnerships with EV manufacturers.

Key Industry Developments

- In January 2026, Harman International agreed to acquire ZF Friedrichshafen AG’s ADAS division, strengthening Harman’s automotive safety electronics, sensor integration, and in-vehicle computing portfolio, while also supporting deeper convergence between centralized control systems and advanced vehicle security modules.

- In September 2025, VicOne partnered with Sasken Technologies to deliver full-stack cybersecurity solutions for connected and electric vehicles. The collaboration integrates intrusion detection, electronic control unit (ECU) protection, and UNECE compliance, enabling OEMs and Tier-1 suppliers to accelerate deployment of secure, audit-ready vehicle platforms.

- In April 2025, Infineon Technologies AG completed the US$ 2.5 billion acquisition of Marvell Technology’s Automotive Ethernet portfolio, strengthening its position in high-speed in-vehicle networking for software-defined vehicles (SDVs). The move enhances Infineon’s secure communication capabilities across ECUs and centralized vehicle architectures.

Companies Covered in Steering Column Locks Market

- Continental AG

- Robert Bosch GmbH

- Valeo

- Denso Corporation

- ALPHA Corporation

- Mitsubishi Electric

- ZF Friedrichshafen AG

- Huf Hülsbeck & Fürst

- Tokai Rika

- Lear Corporation

- Aptiv PLC

- CIE Automotive

Frequently Asked Questions

The global steering column locks market is projected to reach US$ 8.8 billion in 2026.

Surging vehicle production, mandatory anti-theft regulations, and increasing adoption of electronic and keyless locking systems are driving the market.

The market is poised to witness a CAGR of around 4.2% from 2026 to 2033.

Opportunities lie in EV platform integration, Asia Pacific vehicle expansion, and growing aftermarket replacement demand.

Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, DENSO Corporation, and Valeo are a few among the leading players in the market.