- Clothing, Footwear, & Accessories

- Athletic Socks Market

Athletic Socks Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Athletic Socks Market Analysis By Product Type (No-shows, Ankle Socks, Quarter Socks, Mid-calf Socks, Knee-high Socks, Crew Socks, Specialty Socks), By Material (Natural Fiber Blends, Synthetic Fiber Blends, Specialized Materials), By Application Sport, and Regional Analysis 2025 - 2032

Athletic Socks Market Share and Trends Analysis

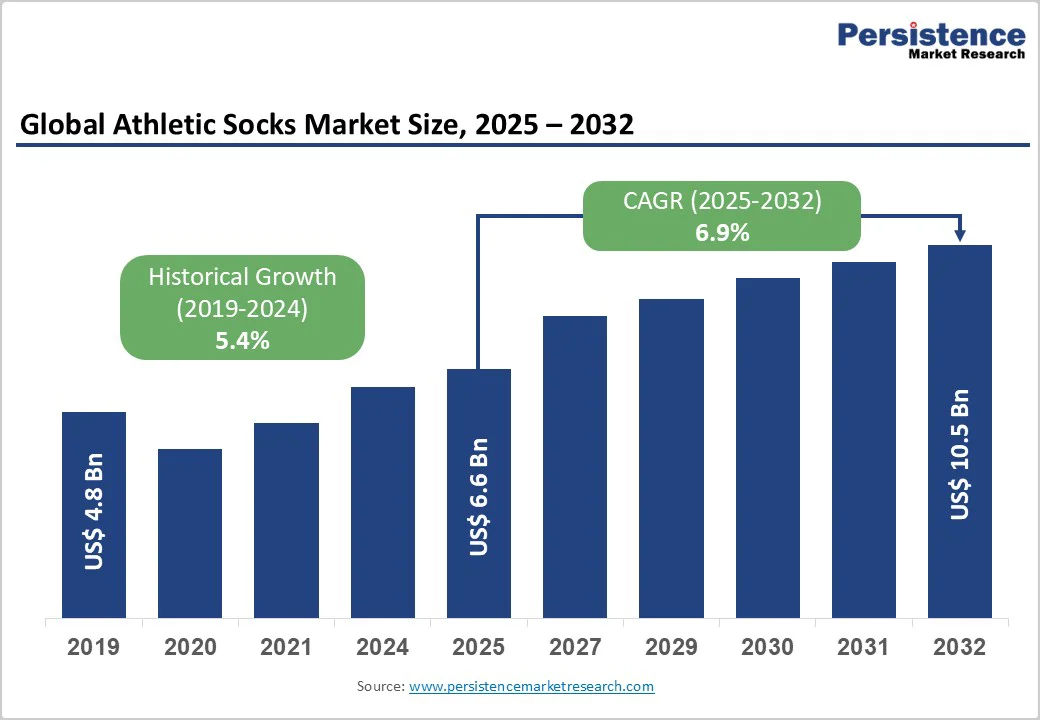

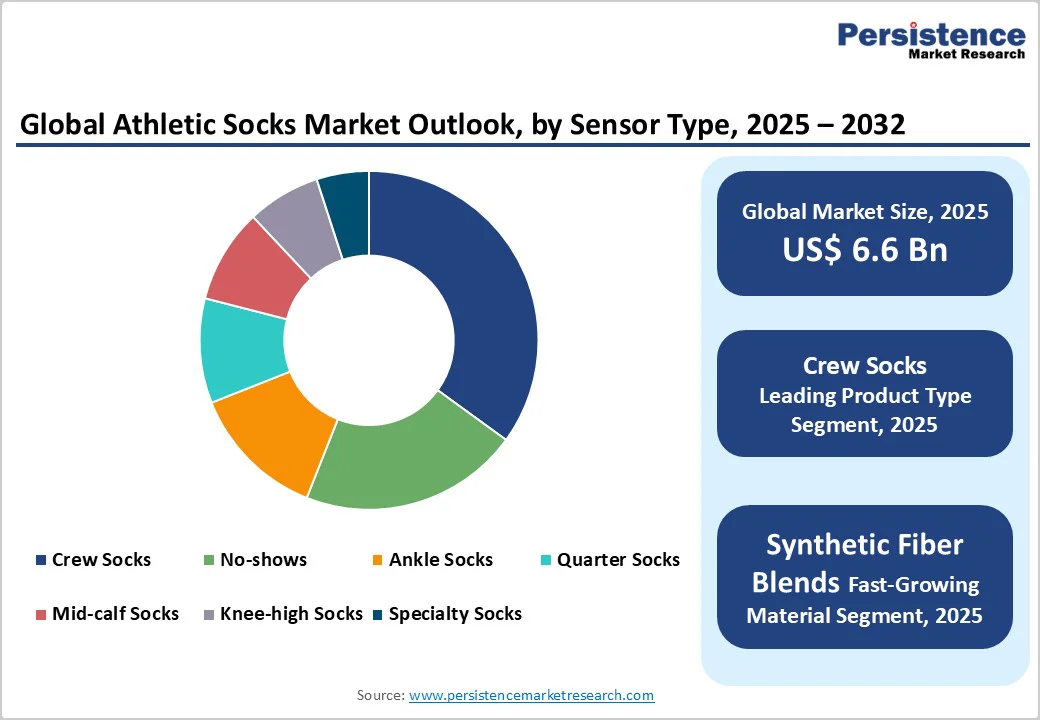

The global athletic socks market size is likely to be valued at US$6.6 billion in 2025 and is projected to reach US$10.5 billion by 2032, growing at a CAGR of 6.9% between 2025 and 2032.

Demand is bolstered by rising health awareness and increased participation in sports, which fuel the need for performance-enhancing features such as moisture-wicking and compression. The athleisure trend further amplifies adoption, as consumers seek socks that combine functionality with style, while technological advancements in fabric innovation support premium pricing and higher margins.

Key Market Highlights

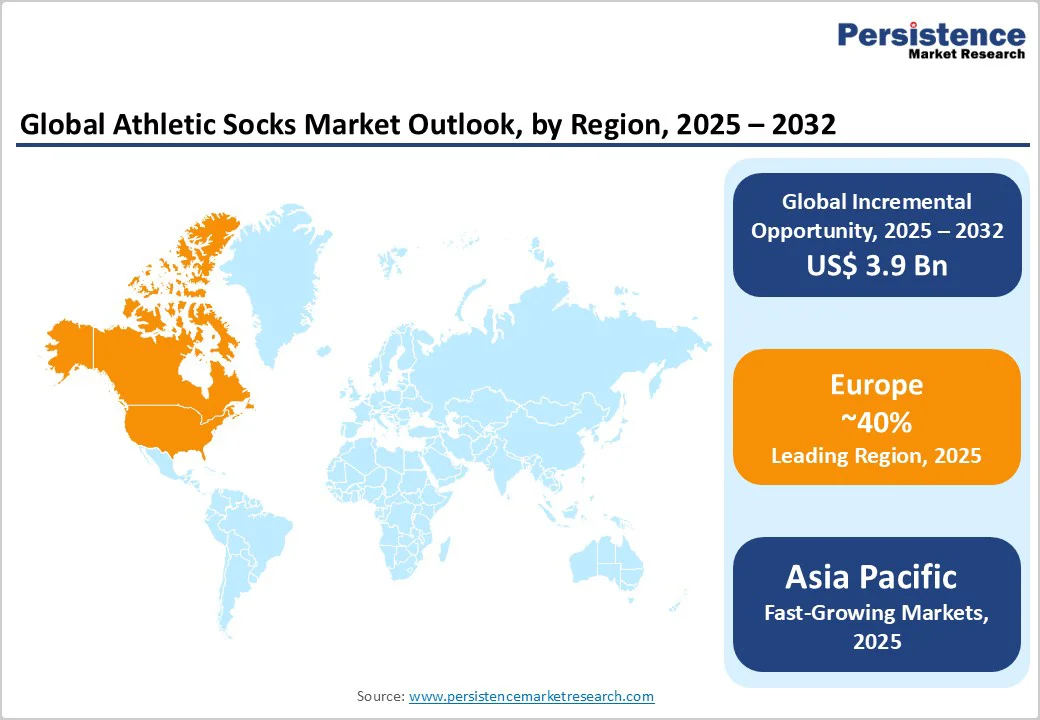

- Leading Region: Europe dominates the global market, underpinned by regulatory harmonization, high disposable incomes, and athleisure adoption.

- Fastest Growing Region: Asia Pacific is expected to grow at a CAGR of 7.8%, driven by urbanization, fitness initiatives, and e-commerce expansion.

- Dominant Segment: Crew socks hold the largest product-type share at 35%, favored for versatile performance and style adaptability.

- Fastest Growing Segment: Smart textile integration in performance socks is the fastest-expanding niche, projected at above 8% CAGR.

- Key Market Opportunity: The adoption of sensor-enabled and antimicrobial fabrics presents significant growth potential across professional and consumer segments.

| Key Insights | Details |

|---|---|

|

Sports and Athletic Socks Size (2025 E) |

US$6.6 Bn |

|

Market Value Forecast (2032 F) |

US$10.5 Bn |

|

Projected Growth CAGR (2025 – 2032) |

6.9% |

|

Historical Market Growth (2019 – 2024) |

5.4% |

Market Dynamics

Driver - Rising Health and Fitness Participation

A clear surge in global fitness-conscious behavior underpins demand for specialized athletic socks offering arch support, cushioning, and moisture management. According to data from the World Health Organization and national fitness councils, over 1.2 billion individuals worldwide participated in organized sports or physical activities, marking a record high in global sports participation.

This trend is particularly strong in developed economies, where the percentage of the population engaging in regular exercise has climbed above 65% in regions such as North America and Europe. Such growth drives demand for high-performance socks designed to reduce fatigue and prevent injuries.

Athleisure and Performance Trend

The convergence of athletic and casual wear has led to athleisure’s mainstream acceptance, with consumers seeking versatile socks that transition seamlessly from workouts to everyday use. Industry reports indicate that sportswear fabrics and accessories experienced a 9% increase in retail sales in 2024, outpacing overall apparel growth. Brands like Nike, Inc., and Adidas AG have leveraged this by launching hybrid sock lines integrating performance mesh panels with lifestyle-driven colorways. The result is a premium segment commanding price points 20 – 25% above standard athletic socks, contributing significantly to market value expansion.

Restraint - Price Sensitivity Among Consumers

While premium performance socks offer enhanced features, a sizeable consumer base in emerging markets remains price-oriented. In regions such as South Asia Pacific and Latin America, private-label and unbranded athletic socks account for over 50% of total unit sales, limiting the penetration of high-end offerings. Surveys conducted by textile associations reveal that 68% of sports apparel purchasers in these markets cite cost as the primary factor in their buying decisions, which presents a barrier to the growth of the branded sock segment.

Raw Material Price Volatility

The athletic socks industry relies heavily on both natural fibers (cotton, wool) and synthetics (nylon, polyester, elastane). Cotton prices spiked by 18% in 2023 due to supply constraints and weather disruptions in major growing regions, while crude oil–linked synthetic fiber costs rose by 12% over the same period. These fluctuations squeeze manufacturers’ margins and necessitate strategic sourcing or passing costs to end users—both of which can dampen demand and profitability.

Opportunity - Expansion in Asia Pacific Through Sports Infrastructure

Rapid urbanization and government-driven sports infrastructure projects in China, India, and Southeast Asia are creating substantial demand for athletic footwear and socks. For example, China’s Ministry of Sports reported a 15% annual increase in registered sports venues over the past three years, which has fueled equipment and apparel consumption. Coupled with rising disposable incomes—household spending on sportswear in India reached US$5.4 billion in 2024—this positions the Asia Pacific as the fastest-growing region.

Smart Textile Integration

The integration of smart sports accessories such as sensor-embedded socks represents a high-potential niche. Early adopters include professional athletes in endurance sports, leveraging real-time data on foot pressure and temperature to optimize performance. Market pilots have demonstrated a 12% reduction in injury risk among participants using sensor-enabled socks during training sessions. As technology costs decline and partnerships between textile mills and IoT providers expand, the smart sock segment is expected to grow at over 8% annually.

Category-wise Insights

By Product Type Analysis

Crew Socks dominate the product type category with an estimated 35% share in 2025, owing to their universal applicability across sports such as basketball, football, and running. The mid-calf design provides superior ankle support and protection against abrasions, which is critical in high-impact sports. Compounded by consumer preference for athleisure-style crew socks—often featuring bold branding and color accents —this segment has seen double-digit value growth. Notably, crew socks saw an 11% revenue increase, reflecting both performance and fashion drivers.

By Material Analysis

Natural fiber blends account for roughly 55% of market value, driven by consumer emphasis on comfort, breathability, and sustainability. Organic and recycled cotton variants are gaining traction, supported by European textile regulations mandating minimum recycled content. Conversely, synthetic fiber blends-including polyester-elastane mixes-offer enhanced durability and moisture-wicking properties, capturing a 30% share in performance-focused applications like Running and Winter Sports.

By Application Sport Analysis

Running socks lead the application segment with approximately 30% share, bolstered by global participation in recreational running events and marathons, which attracted over 50 million finishers in major races across North America and Europe. These socks feature strategic padding in the heel and forefoot, as well as ventilation channels, aligning with Sports Equipment Market expectations for performance optimization. Football and Basketball follow, each securing over 15% share, driven by professional league partnerships and demand for customization.

Regional Insights

North America Sports and Athletic Socks Trends

North America leads in innovation, with brands integrating smart textiles and sustainable materials into athletic socks. E-commerce penetration exceeded 35% of total apparel sales in 2024, enabling direct consumer engagement and rapid product launches. Partnerships with professional sports leagues, such as the NFL and NBA, enhance brand visibility, while health-focused policies and corporate wellness programs bolster demand for performance socks. The U.S. Consumer Product Safety Commission’s textile standards ensure quality and safety, further cementing North America’s position at the forefront of high-performance sock adoption.

Europe Sports and Athletic Socks Trends

Europe dominates the market share, driven by stringent regulations such as the EU Textiles Regulation (EU) 2020/2151, which mandates transparent labeling and disclosures of recycled content. Germany’s athletic footwear and accessories market reported a 6% year-on-year growth in 2024, while the U.K. witnessed a 10% uptick in athleisure sock sales. France’s professional football clubs are increasingly collaborating with sock manufacturers for co-branded, performance-tuned products. Across Southern Europe, emerging sports such as padel tennis are creating niche demands for specialized socks, further diversifying the regional portfolio.

Asia Pacific Sports and Athletic Socks Trends

Asia Pacific exhibits the highest growth trajectory, thanks to government initiatives promoting fitness-such as China’s “National Fitness Program”-and India’s “Fit India Movement.” Local manufacturers benefit from lower labor costs and proximity to raw materials, with domestic sock production capacity expanding by 12% annually. International brands are establishing regional hubs and licensing partnerships to cater to local preferences. Additionally, rapid e-commerce growth in the region, projected to reach US$4 trillion by 2025, enhances market accessibility for both premium and value-oriented athletic socks.

Competitive Landscape

The global athletic socks market is moderately consolidated, dominated by global giants Nike, Inc., Adidas AG, and PUMA SE, which collectively hold over 45% of market value. These leaders emphasize innovation-such as moisture-management technologies and sustainable materials-and leverage direct-to-consumer and omni-channel strategies. Regional players and private labels cater to cost-sensitive segments, while niche brands focus on specialized applications like compression or smart textile integration. Emerging business models include circular economy programs, such as sock recycling initiatives, and co-branded partnerships with sports teams and events.

Key Market Developments

- In March 2025: Launch of Nike, Inc. Dri-FIT Elite sock line featuring targeted compression zones and moisture-wicking mesh panels.

- In July 2024, PUMA SE introduced a recycled-material performance sock collection across European markets, achieving 30% recycled content.

- In January 2025, Under Armour, Inc. partnered with the Tokyo Marathon to supply sensor-embedded smart socks for elite runners, offering real-time foot pressure analytics.

Companies Covered in Athletic Socks Market

- Nike, Inc.

- Adidas AG

- VF Corporation

- PUMA SE

- Jockey International Inc.

- Drymax Technologies Inc.

- Hanesbrands Inc.

- Under Armour, Inc.

- Skechers U.S.A., Inc.

- ASICS Corporation

- Wolverine World Wide, Inc.

- THORLO, Inc.

- New Balance Athletics, Inc.

- Others

Frequently Asked Questions

The global Athletic Socks Market is likely to value at US$ 6.6 Bn in 2025 and is expected to reach US$ 10.5 Bn by 2032, at a CAGR of 6.9%.

Rising participation in sports and health consciousness, coupled with athleisure trends, drive demand for performance socks offering moisture-wicking and compression features.

Crew socks lead the product type category with approximately 35% share, due to their versatility and support across major sports.

Europe commands the largest share, driven by high disposable incomes, regulatory support, and strong athleisure adoption.