- Medical Devices

- Serum Separation Gel Market

Serum Separation Gel Market Size, Share, and Growth Forecast 2026 - 2033

Serum Separation Gel Market by Product Type -Serum Separation Gel with Integrated Tubes, Serum Separation Gel Without Integrated Tubes), End-user -Hospitals & Clinics, Diagnostic Laboratories, Blood Banks, Pharmaceutical & Biotechnology Companies, Others), and Regional Analysis, 2026-2033

Serum Separation Gel Market Share and Trends Analysis

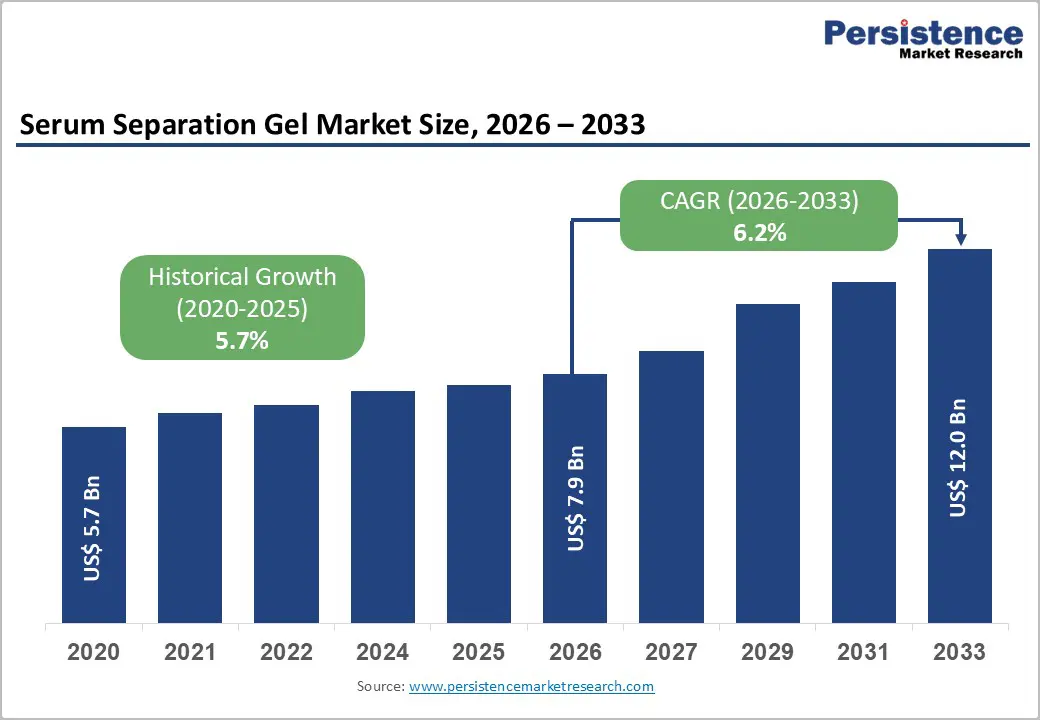

The global serum separation gel market size is expected to be valued at US$ 7.9 billion in 2026 and projected to reach US$ 12.0 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. Increasing demand for accurate blood sample processing in clinical diagnostics and laboratory testing. These gels are widely used in blood collection tubes to create a stable barrier between serum and blood cells during centrifugation, improving sample integrity and test reliability.

The rising prevalence of chronic diseases, growing routine health screenings, and expansion of diagnostic laboratories are major growth contributors. Technological advancements in gel formulations, including non-toxic and high-stability products, are further supporting adoption. Emerging healthcare infrastructure and preventive care trends continue to strengthen long-term market potential.

Key Industry Highlights:

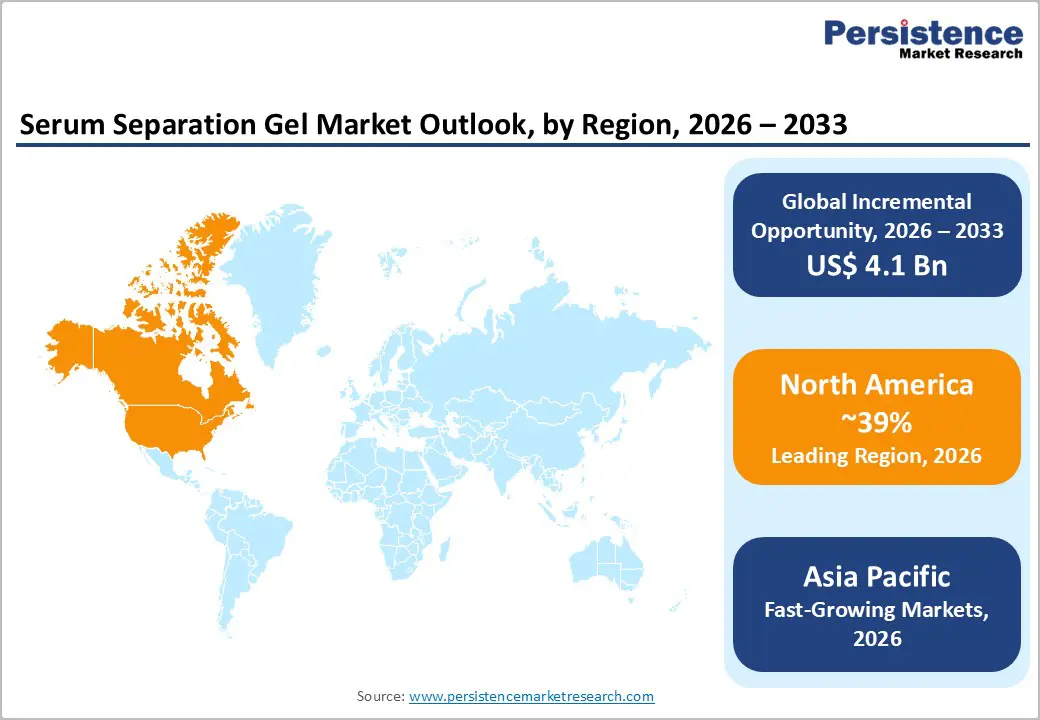

- Leading Region - North America commands 39% of the global Serum Separation Gel market in 2025, driven by the U.S.'s 13 billion+ annual clinical lab test volumes, world-leading biopharmaceutical R&D serum consumption, and BD Vacutainer SST's near-universal adoption across U.S. hospital laboratory networks.

- Fast-Growing Market- Asia Pacific is the fastest-growing market, driven by China's 33% regional share under ISO 15189 standardization, India's diagnostic laboratory chain expansion under Ayushman Bharat, and Southeast Asia's CDMO manufacturing growth, consuming pharmaceutical-grade serum separation gel products.

- Dominant Segment - Serum separation gel with integrated tubes is likely to lead with a 68% share in 2026, driven by CLSI guideline recommendations, automated specimen processing compatibility, and BD Vacutainer SST's dominance in global hospital laboratory procurement for routine clinical chemistry and immunoassay testing.

- Fast-Growing End-user Segment - Hospitals & clinics are the fast-growing end user, fueled by global healthcare infrastructure investment exceeding US$ 9 trillion annually -World Bank), Ayushman Bharat-driven tier-2 hospital laboratory upgrades, and the Middle East's hospital expansion programs standardizing on integrated SST tube workflows.

- Key Opportunity - Sustainable Bio-Based SST Tube Innovation: Bio-based and reduced-plastic serum separation tube formulations represent a premium innovation opportunity, with EU circular economy mandates and ISO 14001 procurement requirements in European hospital networks creating first-mover advantage for manufacturers developing validated sustainable serum separator tube systems.

Market Dynamics

Drivers - Surging Global Diagnostic Testing Volumes Driving Serum Separation Gel Consumption

The exponential growth of global diagnostic testing volumes is the most powerful structural demand driver for serum separation gel products. The American Clinical Laboratory Association -ACLA) estimates that U.S. clinical laboratories perform over 13 billion laboratory tests annually, the vast majority of which require serum samples obtained through blood collection tubes containing serum separation gel.

Post-pandemic normalization of routine preventive health testing, combined with aging populations requiring increasingly frequent chronic disease biomarker monitoring for conditions including cardiovascular disease, diabetes, and cancer, has expanded baseline serum testing volumes. The WHO's Global Health Observatory data indicates that laboratory diagnosis now underpins over 70% of all clinical decision-making. As integrated serum separation gel tube systems from Becton Dickinson & Company -BD Vacutainer SST) and F. Hoffmann-La Roche Ltd. become the standard of care in clinical laboratories globally, consumable consumption volumes grow proportionally with diagnostic test throughput.

Biopharmaceutical Industry Expansion Generating High-Purity Serum Demand for Drug Development

The global biopharmaceutical industry's rapid expansion is creating significant incremental demand for pharmaceutical-grade serum separation gel products used in cell culture media preparation, drug formulation quality control, and preclinical research applications. The Pharmaceutical Research and Manufacturers of America -PhRMA) reported that the U.S. biopharmaceutical industry invested over US$ 102 billion in R&D in 2022, with biologics development programs requiring high-purity serum samples free from cellular contamination.

Serum separation gel products, particularly those classified as pharmaceutical grade under USP <1> and EP standards, command significant price premiums in the biotech and pharma end-user segment. Contract development and manufacturing organizations -CDMOs) globally are scaling serum processing capacity, directly increasing demand for gel-integrated separation systems from Qiagen N.V., Merck KGaA, and Bio-Rad Laboratories that ensure consistent, high-purity serum yields across large-scale bioprocessing workflows.

Restraints - Stringent Regulatory Requirements and Lot-to-Lot Variability Concerns in Pharmaceutical Applications

Pharmaceutical and biotechnology companies face significant challenges in maintaining consistent serum separation gel performance across production lots, as variability in gel density, thixotropy, and serum recovery rates between manufacturing batches can compromise experimental reproducibility in cell culture and drug development applications. The U.S. FDA's 21 CFR Part 211 current Good Manufacturing Practice regulations require extensive lot testing and documentation for laboratory materials used in pharmaceutical manufacturing, increasing supplier qualification costs and limiting competitive entry. These regulatory compliance burdens create supply concentration risks and add procurement complexity for pharma customers, potentially delaying product introductions and creating operational friction.

Growing Environmental and Sustainability Concerns Over Single-Use Plastic Blood Collection Tubes

The dominant integrated serum separation gel tube format is inherently single-use, generating significant volumes of plastic laboratory waste with every clinical blood draw. Growing regulatory and institutional pressure for sustainable laboratory practices, including the European Commission's circular economy action plan targeting single-use plastic reduction, is creating scrutiny around blood collection tube waste management. Hospitals and diagnostic laboratories in Germany, the Netherlands, and Scandinavia are increasingly evaluating the total environmental impact of consumable procurement decisions, creating reputational and compliance headwinds for manufacturers of conventional PET-based serum separation tube systems and incentivizing costly material innovation.

Opportunities - Hospitals and Clinics: Fastest-Growing End User Driven by Healthcare Infrastructure Expansion

Hospitals and clinics represent the fastest-growing end-user segment for serum separation gel, driven by global healthcare infrastructure expansion, rising hospitalization rates for chronic diseases, and the increasing integration of point-of-care and central laboratory testing workflows that require standardized pre-analytical blood collection systems. The World Bank reports that global healthcare expenditure has grown consistently to over US$ 9 trillion annually, with hospital laboratory expansion a priority investment across Asia Pacific, the Middle East, and Latin America. The transition of hospital laboratories from manual serum separation centrifugation to integrated SST -Serum Separator Tube) systems from Becton Dickinson & Company and Cardinal Health Inc. is accelerating, reducing turnaround time and pre-analytical errors simultaneously. As Ayushman Bharat and similar national health infrastructure programs expand hospital laboratory capacity across India and Southeast Asia, volume-driven hospital serum tube procurement is creating a structurally growing market channel through 2033.

Bio-Based and Sustainable Serum Separation Gel Formulations Addressing Green Laboratory Demand

The development of bio-based, biodegradable, or reduced-plastic serum separation gel formulations represents a significant product innovation opportunity, as laboratory sustainability mandates intensify across Europe and North America. Leading laboratory products manufacturers, including Becton Dickinson & Company and Danaher Corporation, are investing in next-generation tube materials including plant-derived polymers and recycled PET formulations that maintain equivalent serum separation performance while reducing environmental impact.

The ISO 14001 Environmental Management certification framework is increasingly a procurement requirement for hospital laboratory supply contracts across European Union member states. Companies developing validated sustainable tube-gel systems that meet CLSI GP34-A performance standards will command significant premium pricing and early-mover competitive advantage in green laboratory procurement programs, representing a durable revenue differentiation opportunity through the forecast period.

Category-wise Analysis

Product Type Insights

The serum separation gel with integrated tubes segment is likely to lead the product type, commanding approximately 68% share in 2026. Integrated serum separator tube -SST) systems, where the thixotropic gel is pre-loaded into a vacuum blood collection tube with a clot activator, dominate due to their superior operational convenience, elimination of manual gel addition steps, reduced contamination risk, and compatibility with automated specimen processing systems in high-throughput hospital and reference laboratories.

Becton Dickinson & Company's BD Vacutainer SST and F. Hoffmann-La Roche's integrated tube systems have achieved near-universal adoption in major clinical laboratory networks globally. The Clinical and Laboratory Standards Institute -CLSI) guidelines recommend standardized SST tube systems for routine serum chemistry and immunoassay testing, cementing integrated tube formats as the clinical standard of care. Serum Separation Gel Without Integrated Tubes serves the pharmaceutical and research segment requiring customizable gel formulations.

End-user Insights

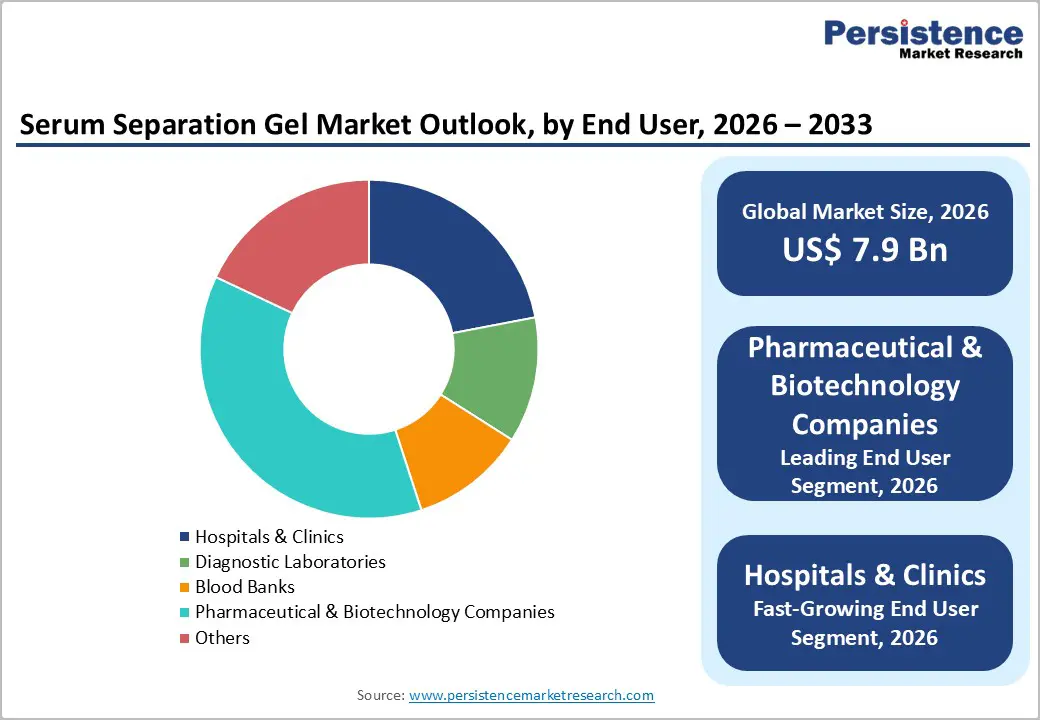

Pharmaceutical and biotechnology companies are the leading end-user segment in the serum separation gel market, likely to command approximately 37% share in 2026. This leadership reflects the high unit value of pharmaceutical-grade serum separation gel products used in cell culture media preparation, biologic drug formulation quality control, and preclinical toxicology studies, which command price premiums of 3-5x above clinical-grade products.

Large biopharma companies, including Pfizer, Novartis, AstraZeneca, and Gilead Sciences, procure significant volumes of certified serum separation products for their global R&D and manufacturing quality control laboratories. Hospitals & Clinics are the fastest-growing end-user segment, driven by global healthcare infrastructure expansion, rising diagnostic test volumes in tier-2 and tier-3 hospital networks across Asia Pacific, and the standardization of integrated SST tube systems in institutional laboratory procurement programs.

Regional Insights

North America Serum Separation Gel Market Trends and Insights

North America leads the global Serum Separation Gel market with 39% share in 2026, anchored by the U.S.'s 13 billion+ annual clinical laboratory test volume per ACLA, the world's largest biopharmaceutical R&D sector consuming pharmaceutical-grade serum products, and comprehensive FDA 21 CFR Part 211 and CLSI regulatory frameworks standardizing SST tube adoption across hospital and reference laboratory networks.

U.S. Serum Separation Gel Market Size

The U.S. accounts for approximately 87% of North America's serum separation gel revenue, driven by its dominant clinical laboratory sector, 900+ late-stage biologics in development per PhRMA, consuming pharmaceutical-grade serum separation products, and Becton Dickinson & Company and Cardinal Health commanding extensive distribution networks across U.S. hospital and reference laboratory systems.

Europe Serum Separation Gel Market Trends and Insights

Europe is the second-largest serum separation gel market, characterized by harmonized EU IVDR -Regulation 2017/746) standards driving SST tube quality requirements, a strong pharmaceutical manufacturing sector demand in Germany, Switzerland, and the UK, and growing sustainability mandates pushing manufacturers toward bio-based tube material innovation. Centralized hospital laboratory procurement programs favor integrated SST systems from established suppliers.

Germany Serum Separation Gel Market Size

Germany holds approximately 22% of European serum separation gel revenues, driven by its dense hospital network, major pharmaceutical manufacturers including Merck KGaA and Bayer consuming pharmaceutical-grade serum products, and ISO 14001-driven sustainability procurement policies in hospital laboratory supply chains, accelerating demand for eco-certified serum separation tube systems.

UK Serum Separation Gel Market Size

The UK contributes approximately 17% of European serum separation gel revenues, supported by NHS England's large centralized laboratory network processing millions of serum samples annually, MHRA-regulated pharmaceutical QC laboratory demand, and UK Research and Innovation -UKRI)-funded biomedical research institutes consuming high-purity serum separation gel products for preclinical studies.

France Serum Separation Gel Market Size

France accounts for approximately 14% of European serum separation gel revenues. France's extensive AP-HP -Assistance Publique - Hopitaux de Paris) public hospital laboratory network, combined with its significant pharmaceutical sector anchored by Sanofi and Servier, sustains consistent serum separation gel demand across both clinical and pharmaceutical-grade product categories.

Asia Pacific Serum Separation Gel Market Trends and Insights

Asia Pacific is the fastest-growing regional serum separation gel market, propelled by rapid diagnostic laboratory infrastructure expansion, growing biopharma manufacturing investment, and rising clinical testing volumes. China represents approximately 33% of Asia Pacific serum separation gel revenues, with national laboratory quality standards harmonizing with ISO 15189 driving integrated SST tube adoption across its expanding hospital and independent laboratory networks.

India Serum Separation Gel Market Size

India contributes approximately 13% of Asia Pacific serum separation gel revenues and is among the region's fastest-growing markets. Diagnostic laboratory chain expansion, including Dr. Lal PathLabs, SRL Diagnostics, and Metropolis Healthcare, combined with Ayushman Bharat-driven hospital laboratory upgrades, is driving rapid SST tube adoption as laboratories standardize on integrated separation systems.

Competitive Landscape

The global serum separation gel market is moderately competitive, supported by rising demand from clinical diagnostics, blood collection, and laboratory testing applications. Market participants focus on improving gel stability, separation efficiency, and compatibility with advanced blood collection tubes to strengthen product performance. Innovation in non-toxic formulations, enhanced centrifugation properties, and longer sample preservation remain key competitive factors. Strategic expansion into emerging healthcare markets, partnerships with diagnostic laboratories, and investments in manufacturing capacity further shape market dynamics.

Key Developments:

- In May 2024, KBMED launched its FDA 510-k)-cleared vacuum serum-separating tubes in the U.S. market to expand its presence and competitiveness in the North American diagnostic sector.

- In May 2023, Greiner Bio-One launched the VACUETTE CAT Serum Fast Separator to enhance laboratory efficiency by significantly reducing blood coagulation time.

Global Serum Separation Gel Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value -2020) | US$ 5.7 Billion |

| Current Market Value -2026) | US$ 7.9 Billion |

| Projected Market Value -2033) | US$ 12.0 Billion |

| CAGR -2026-2033) | 6.2% |

| Leading Region | North America, 39% market share -2026) |

| Dominant Category-1 -Product Type) | Serum Separation Gel With Integrated Tubes, ~68% market share -2026) |

| Top-ranking Category-2 -End User) | Pharmaceutical & Biotechnology Companies, 37% market share -2026) |

| Incremental Opportunity | US$ 4.1 Billion -2026-2033) |

Companies Covered in Serum Separation Gel Market

- Qiagen N.V.

- Cardinal Health Inc.

- Medtronic PLC

- Bio-Rad Laboratories

- Microfluidics International Corporation

- BioVision, Inc.

- Danaher Corporation

- Becton Dickinson & Company

- F. Hoffmann-La Roche Ltd.

- Merck KGaA

Frequently Asked Questions

The global serum separation gel market is projected to reach US$ 7.9 billion in 2026.

The primary demand drivers in the Serum Separation Gel market include the rising volume of blood tests for disease diagnosis, increasing prevalence of chronic and infectious diseases, and growing demand for accurate laboratory results.

North America leads the global market with 39% of market share in 2025. The U.S. anchors this leadership through its dominant clinical laboratory infrastructure processing 13 billion+ annual tests, the world's largest biopharma R&D sector consuming pharmaceutical-grade serum products, ACLA, CLSI, and FDA 21 CFR-established quality standards, and market leaders Becton Dickinson & Company and Cardinal Health with extensive U.S. healthcare distribution networks.

Rising prevalence of chronic diseases, increasing routine health screenings, and growing adoption of automated laboratory systems are driving the need for reliable serum separation products.

Leading companies include Becton Dickinson & Company -BD Vacutainer SST), F. Hoffmann-La Roche Ltd., Danaher Corporation, Merck KGaA, Qiagen N.V., Bio-Rad Laboratories Inc., Cardinal Health Inc., Sarstedt AG & Co. KG, Greiner Bio-One International GmbH, Medtronic PLC, Microfluidics International Corporation, BioVision Inc., and Improve Medical Instruments Co. Ltd., among others.