- Food and Beverages

- Seafood Base Market

Seafood Base Market Size, Share, and Growth Forecast, 2026 - 2033

Seafood Base Market by Source (Fish-based, Crustacean-based, Mollusk-based, Seaweed), Form (Liquid, Paste, Powdered, Freeze-dried), End-User (Food & Beverage, Foodservice, Processed & Packaged Foods), and Regional Analysis for 2026 - 2033

Seafood Base Market Share and Trends Analysis

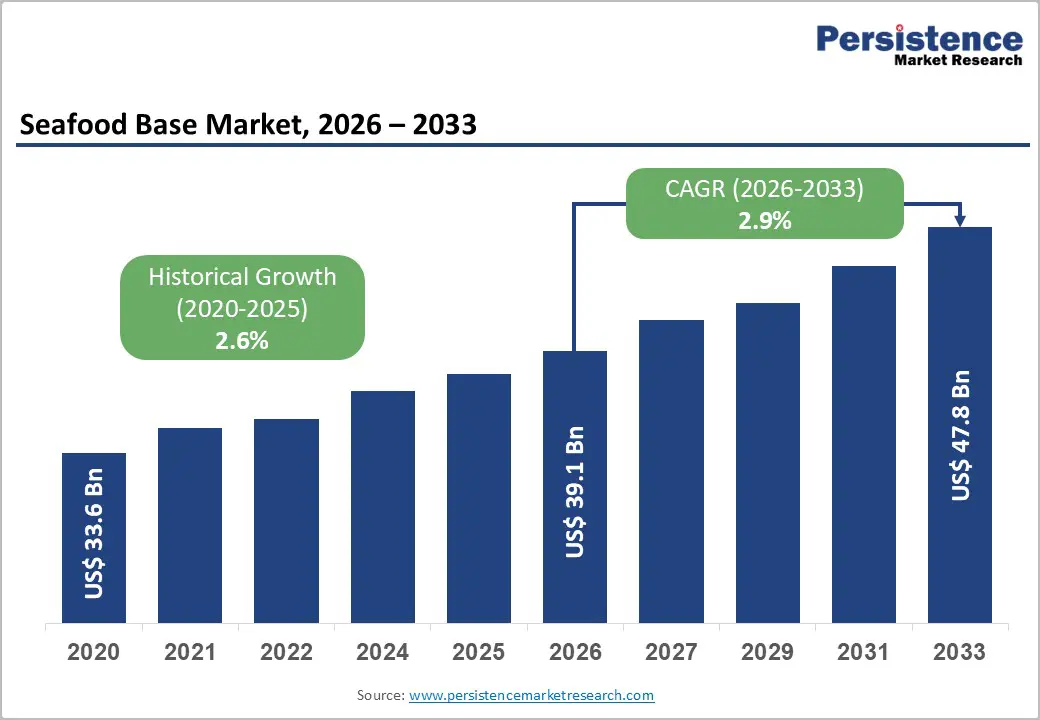

The global seafood base market size is likely to be valued at US$ 39.1 billion in 2026 and is estimated to reach US$ 47.8 billion by 2033, growing at a CAGR of 2.9% during the forecast period 2026−2033. Increasing global demand for protein-rich food sources is driving consistent seafood-based consumption.

Urbanization, rising disposable incomes, and evolving dietary preferences for nutrient-dense foods are driving demand for seafood extracts, flavor bases, and ready-to-use culinary ingredients derived from marine sources. Nutrition guidelines issued by health authorities recognizing marine proteins and micronutrients are reinforcing adoption across food manufacturing, foodservice, and retail channels. Government programs that promote sustainable fisheries and aquaculture further enhance supply stability for seafood derivatives, enabling deeper market penetration.

Key Industry Highlights

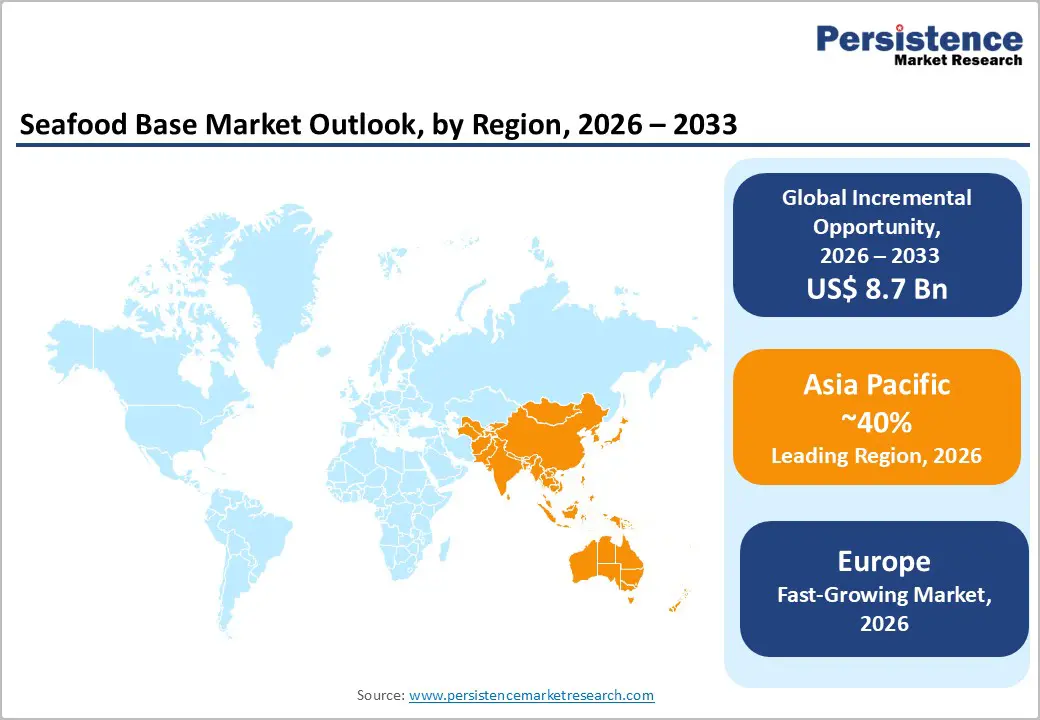

- Dominant Region: Asia Pacific is projected to dominate with about 38% market share in 2026, supported by high seafood consumption and strong aquaculture production.

- Fastest-growing Market: Europe is forecasted to be the fastest-growing market between 2026 and 2033, driven by premium seafood flavour demand and gourmet product adoption.

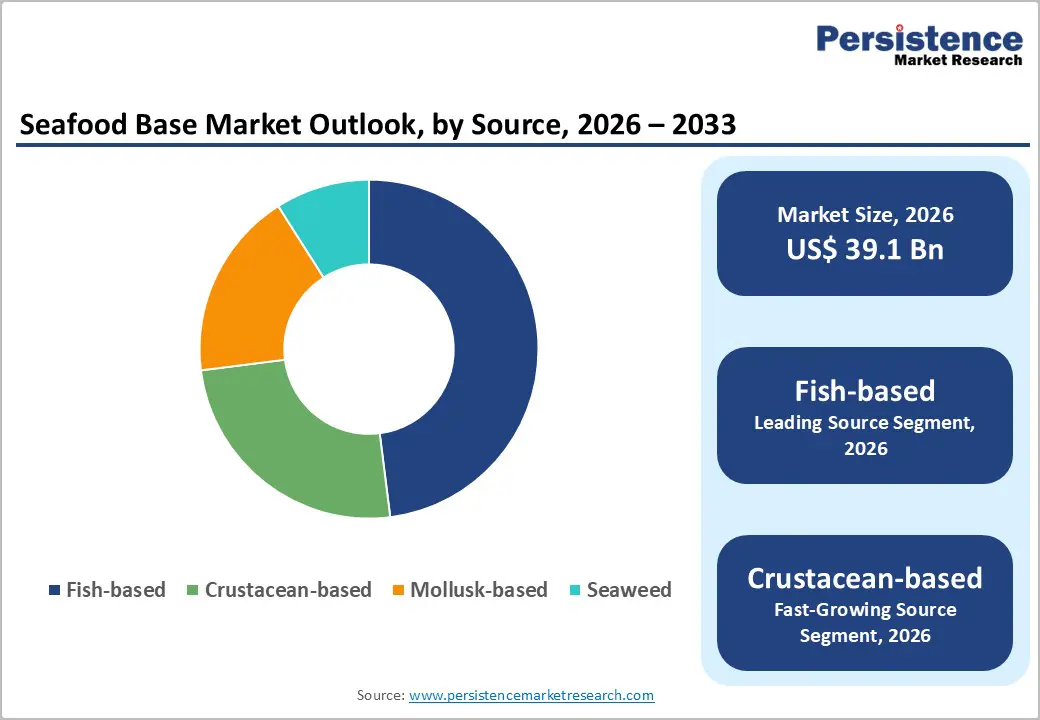

- Leading Source: The fish-based segment is slated to lead with about 48% revenue share in 2026, fueled by strong supply chains and broad culinary use.

- Fastest-growing Source: The crustacean-based segment is anticipated to be the fastest-growing through 2033, due to premium shellfish flavour demand and aquaculture expansion.

| Key Insights | Details |

|---|---|

|

Seafood Base Market Size (2026E) |

US$ 39.1 Bn |

|

Market Value Forecast (2033F) |

US$ 47.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Protein Demand and Health-Driven Consumption Patterns

Global dietary trends are shifting towards protein-rich foods as awareness of the nutritional benefits of balanced diets grows. Consumers seek foods that support muscle development, immune system strength, and overall well-being. Seafood bases, derived from fish, shellfish, and marine extracts, offer a concentrated source of protein and essential amino acids while enhancing flavor in culinary applications. The versatility of these bases allows integration into soups, sauces, ready meals, and processed foods, enabling manufacturers to meet consumer expectations for high-protein options without altering preparation processes.

Shifts in health-oriented consumption patterns are influencing product formulation and innovation strategies. Clean-label, natural, and minimally processed ingredients are increasingly preferred, and seafood bases align with these preferences by offering authentic marine flavors and nutrient density. Urbanization and changing lifestyles further amplify demand for convenient protein-enhancing solutions, where ready-to-use bases simplify meal preparation while maintaining nutritional value. Culinary professionals and food manufacturers leverage these products to efficiently deliver health-oriented offerings that address both taste and dietary requirements.

Advancement in Processing Technologies and Cold-Chain Infrastructure

Improvements in processing technologies enable precise control over temperature, time, and hygiene during handling of perishable marine ingredients, directly enhancing product quality and safety. Advanced freezing methods, automated temperature monitoring, and digital traceability tools reduce spoilage and microbial risk associated with traditional handling. Real-time sensors and IoT-enabled systems provide continuous visibility of conditions at every stage from harvest to final preparation, strengthening compliance with food safety standards enforced by regulatory authorities.

Cold-chain infrastructure ensures preservation of freshness during transport and storage, maintaining organoleptic properties valued by end users and reducing product losses. Integrated refrigerated storage, transportation, and distribution networks allow efficient handling of high-volume production while maintaining consistent quality. Government programs supporting fisheries and aquaculture have prioritized the development of such infrastructure to improve supply chain efficiency and facilitate domestic and international distribution of marine products.

Sustainability Challenges and Resource Constraints

Marine resource availability underpins all downstream activities that rely on seafood ingredient inputs, but current extraction and management practices impose meaningful constraints on long-term supply volumes. An assessment by the Food and Agriculture Organization (FAO) on fish stocks sustainability indicates that in 2025, only 64.5% of fishery stocks are within biologically sustainable levels, while 35.5% remain overfished. Overexploitation of key species and insufficient recovery periods reduce accessible biomass, tightening the supply of raw materials for downstream processors and manufacturers.

Resource constraints further compound operational challenges where government management systems, environmental variability, and illegal fishing dynamics intersect. Many coastal jurisdictions enforce seasonal closures and protected zones to maintain ecological productivity, but enforcement capacity varies significantly across regions, leading to uneven compliance and ongoing erosion of critical spawning populations. At the same time, climate-induced shifts in marine ecosystems, such as altered migration patterns and habitat degradation, reduce the predictability of harvest yields and increase the risk in procurement planning for supply chain actors. Limited data infrastructure and inconsistent stock-monitoring frameworks across numerous fisheries jurisdictions further weaken the ability to forecast sustainable extraction rates and to build resilient sourcing strategies.

Intense Competition from Plant-based and Synthetic Flavor Alternatives

The seafood-based market faces mounting pressure from plant-based and synthetic flavor alternatives, which deliver comparable umami and seafood flavors while offering lower production costs and extended shelf life. Plant-derived extracts and synthetic compounds allow manufacturers to replicate traditional seafood flavors without relying on raw marine sources, reducing dependency on fluctuating seafood supplies and mitigating sustainability concerns. These alternatives provide consistent taste profiles, which are crucial for large-scale food production and processed food applications that demand uniform flavor. Rapid innovation in flavor chemistry enables the creation of highly concentrated solutions that match the sensory characteristics of conventional seafood bases while improving storage stability and reducing spoilage risk.

Consumer trends toward vegetarian, vegan, and clean-label diets amplify the adoption of these alternatives, particularly in markets with rising awareness of environmental and ethical considerations. Foodservice providers and packaged food manufacturers increasingly prioritize ingredients that align with dietary preferences and regulatory scrutiny over allergens, heavy metals, and contamination risks associated with marine-derived products. The flexibility of synthetic and plant-based flavors in formulation also supports diverse applications, including snacks, sauces, soups, and plant-based seafood analogs, thereby enhancing their appeal compared to traditional seafood bases.

Product Innovation through Sustainable and Alternative Offerings

Rising consumer demand for natural, clean-label, and ethically sourced ingredients is reshaping the seafood base industry. Manufacturers increasingly focus on developing formulations derived from responsibly harvested seafood, seaweed, and plant-based analogs to align with environmental and nutritional expectations. These alternative offerings address concerns related to overfishing, marine ecosystem depletion, and food safety, enabling companies to meet both regulatory requirements and consumer preferences. The adoption of sustainable raw materials also supports brand differentiation in competitive markets, allowing businesses to position their products as premium, environmentally conscious, and health-oriented.

Shifts in culinary trends and the expansion of plant-forward diets are creating significant opportunities for innovation in seafood flavor solutions. Reformulating bases to include plant-derived or hybrid ingredients permits the creation of products suitable for vegetarian, vegan, and flexitarian consumers, broadening market reach. Technological advancements in flavor extraction and concentration ensure that these alternatives replicate traditional seafood taste and aroma, maintaining product quality while reducing reliance on finite marine resources. Companies leveraging sustainable and alternative offerings can capture emerging demand across foodservice, processed foods, and home cooking segments, thereby supporting scalability and long-term growth aligned with global sustainability agendas.

Penetration into Emerging Markets with Rising Disposable Incomes

Rising disposable incomes in emerging economies underpin shifts in dietary preferences and consumption patterns, especially in food sectors linked to animal-source proteins and related ingredients. Growth of per capita intake of fish and other animal-derived foods is projected to increase significantly in lower-middle-income countries as household spending power strengthens, with a projected 24% jump in calorie intake from such foods in these markets over the next decade compared with the global average, according to evidence from the Organisation for Economic Co-operation and Development (OECD) and the FAO forecasts by 2034. This increase reflects not just population growth but also a structural rise in urbanization and disposable income, enabling consumers to shift from staple diets toward more diverse, higher-value foods that require complementary ingredients and bases in food preparation and processing.

Retail and commercial food sectors in emerging economies are responding to this trend as rising affluence and urban lifestyles expand demand for convenient, flavor-rich products. Public policy and economic data show that consumers in middle-income countries allocate a growing share of their income to higher-quality and processed foods, driven by stronger wage growth and broader market access. As disposable income rises, food consumption patterns shift toward products that offer taste, convenience, and perceived nutritional value. Government initiatives in several emerging economies aim to stimulate domestic consumption through wage support, tax incentives, and infrastructure development, thereby further enhancing household purchasing power and market accessibility.

Category-wise Analysis

Source Insights

Fish-based is poised to lead with a forecasted 48% of the seafood base market revenue share in 2026, owing to broad consumer familiarity with fish flavors, established global supply chains for finfish, and high utilization in culinary and processed food applications. The segment’s dominance is reinforced by its widespread incorporation into traditional and modern recipes, spanning soups, sauces, ready meals, and snacks. Fish-based bases are perceived as a reliable source of protein and omega-3 fatty acids, appealing to health-conscious consumers. Strong logistics networks, including cold chain and aquaculture expansion, ensure consistent supply, supporting adoption across retail and foodservice markets.

The crustacean-based segment is anticipated to be the fastest-growing segment between 2026 and 2033, driven by expanding demand for premium shellfish flavors in foodservice and specialty retail. Consumer interest in lobster, shrimp, and crab flavor profiles is rising, driven by culinary trends that emphasize gourmet and international dishes. Investment in aquaculture for decapod species has improved year-round availability and product consistency. Distribution networks and cold chain solutions are maturing, reducing supply volatility and enabling high-quality flavor delivery to restaurants and retail outlets.

Form Insights

Liquid is likely to command a projected 41% revenue share in 2026, driven by superior versatility, ease of integration with existing manufacturing processes, and strong adoption in foodservice applications. The format allows chefs and manufacturers to achieve consistent flavor distribution quickly, supporting large-scale production of soups, sauces, gravies, and ready meals. Liquid bases also enhance mouthfeel and texture while blending seamlessly with other ingredients. Advances in preservation technologies, such as pasteurization and aseptic packaging, combined with well-established logistics networks, ensure year-round availability and reliability, reinforcing preference among both institutional buyers and retail consumers.

Powdered is expected to grow the fastest between 2026 and 2033, driven by cost-efficient shipping, extended shelf stability, and compatibility with dry mix and convenience food applications. Powdered formats enable food manufacturers to standardize flavor intensity and dosing with minimal waste, supporting consistent product quality. Reduced reliance on cold-chain infrastructure lowers transportation and storage costs, while ease of incorporation into seasonings, bouillons, and ready-to-prepare mixes encourages innovation. Growing demand for portable, shelf-stable ingredients in both emerging markets and developed economies further accelerates the adoption of powdered bases across retail, industrial, and foodservice segments.

Regional Insights

North America Seafood Base Market Trends

North America maintains a stable position through advanced distribution networks and a focus on clean-label products, particularly in the United States and Canada. Stability is supported by widespread adoption of seafood bases in retail, foodservice, and industrial applications, where liquid, powdered, and paste formats are used in soups, sauces, ready meals, and seasoning blends. Consumers increasingly seek convenience, consistent flavor, and transparency in ingredients, driving demand for concentrated solutions that deliver uniform taste and texture. Efficient cold chain infrastructure and logistics ensure reliable supply, reduce spoilage, and enable broader distribution across urban and semi-urban markets. Culinary innovation in commercial kitchens and institutional food preparation reinforces adoption, while high-quality seafood extracts contribute umami, nutritional value, and premium taste across multiple product categories.

Advanced processing technologies and regulatory oversight strengthen market resilience. Compliance with safety standards and traceability protocols enhances confidence in clean-label and prepared food offerings. Investment in sustainable sourcing and aquaculture efficiency secures a consistent supply of finfish, crustaceans, and mollusks, supporting high-value culinary applications. Retail and online channels facilitate accessibility, enabling manufacturers to introduce innovative product formats and tailored solutions aligned with evolving taste preferences. Rising consumer awareness of nutrition, health, and ethical sourcing further reinforces the adoption of concentrated seafood ingredients, maintaining stable demand in commercial and retail applications.

Europe Seafood Base Market Trends

Europe is forecasted to be the fastest-growing market for seafood-based products between 2026 and 2033, stimulated by rising demand for premium seafood flavors and evolving culinary trends. Expansion is driven by the adoption of high-value ingredients in gastronomy, including bisques, sauces, and ready-to-eat gourmet products. Consumers increasingly prioritize authenticity, taste consistency, and nutritional quality, encouraging integration of concentrated bases in both commercial kitchens and retail-ready meals. Advanced processing technologies, such as precision extraction and pasteurization, enable manufacturers to maintain flavor intensity while ensuring product safety and extended shelf life. Sophisticated distribution networks facilitate efficient delivery across urban and semi-urban areas, supporting rapid market penetration and adoption.

Key factors driving accelerated growth include regulatory compliance, sustainability initiatives, and innovation in product formats. Quality and safety standards enforce traceable and controlled production processes, improving consumer confidence and acceptance of high-value products. Sustainable aquaculture investments and responsible sourcing practices reduce supply volatility for crustaceans and mollusks, enabling consistent availability for premium culinary applications. Introduction of concentrated bases into plant-forward and hybrid seafood preparations expands the addressable market and meets emerging dietary trends. Growing adoption in hotels, catering, and institutional foodservice drives volume, while consumers demonstrate a willingness to pay for convenience and authentic taste experiences.

Asia Pacific Seafood Base Market Trends

Asia Pacific is expected to dominate with an estimated 38% share of the global seafood market in 2026, reflecting strong demand for marine-based flavors driven by deeply entrenched dietary patterns and high per capita seafood consumption. The region benefits from a sophisticated aquaculture ecosystem producing finfish, crustaceans, and mollusks at scale, ensuring consistent supply for both domestic consumption and industrial processing. Culinary traditions favor concentrated seafood flavors in soups, sauces, ready-to-cook meals, and snacks, encouraging widespread adoption of liquid, paste, and powdered bases. Integration into retail and foodservice channels, including supermarkets, restaurants, and institutional kitchens, further supports penetration. The presence of established supply chains, cold chain logistics, and processing expertise enables manufacturers to maintain quality, extend shelf life, and meet growing demand across urban and semi-urban areas.

Dominance is reinforced by technological innovation and evolving consumption trends that prioritize convenience and consistency. Urban populations increasingly seek ready-to-use products that deliver uniform flavor intensity, supporting the use of bases in processed foods and culinary applications. Investments in preservation technologies and efficient distribution networks reduce spoilage and expand market accessibility. Expertise in seafood processing allows the development of tailored extracts aligned with local taste profiles, enabling high-value applications in both premium and mass-market segments. Availability of diverse species, combined with scalable harvesting and processing methods, strengthens product offerings and positions the region for sustained growth.

Competitive Landscape

The global seafood base market is characterized by a mix of multinational flavor and ingredient suppliers, marine processing enterprises, and specialty base producers, creating a moderately concentrated competitive environment. Leading players, including Thai Union, Mowi, Cermaq Group AS, Lerøy, Grieg Seafood, and Nissui, command significant shares through vertically integrated supply chains, spanning aquaculture, harvesting, processing, and distribution. Diversified product portfolios enable these companies to serve multiple end-use applications such as soups, sauces, ready meals, and industrial food production, while maintaining consistent flavor quality and nutritional content.

Mid-tier participants contribute to regional supply dynamics by catering to niche markets, specialty flavours, and emerging culinary trends, while smaller innovators focus on sustainable sourcing and alternative base formats, including plant-enhanced or hybrid seafood solutions. Competitive advantage stems from the ability to meet evolving consumer preferences for convenience, umami intensity, and high-quality, traceable ingredients. Strategic collaborations, co-manufacturing arrangements, and partnerships with foodservice operators allow companies to expand reach and strengthen brand presence. Continuous emphasis on research and development supports innovation in both form and flavour, ensuring responsiveness to shifting taste profiles and regulatory standards.

Key Industry Developments

- In January 2026, SmartGreen Aquaculture launched an inland trout seafood recirculating aquaculture system (RAS) facility in Hyderabad with a US$ 6 million, 1,200-metric-ton capacity, while planning global seafood exports and future expansion into salmon production.

- In December 2025, Japan-based Maruha Nichiro Corporation acquired the remaining shares of Netherlands-based Seafood Connection, increasing its stake from 81.96% to 100% to make it a wholly owned subsidiary and strengthen its European seafood distribution network.

- In August 2025, Bengaluru-based B2B seafood platform Captain Fresh confidentially filed IPO papers with the Securities and Exchange Board of India (SEBI), aiming to raise US$ 350–400 million to support global expansion and strengthen its technology-enabled seafood supply chain platform.

Companies Covered in Seafood Base Market

- Thai Union Group PCL.

- Mowi

- Cermaq Group AS

- Lerøy.

- Grieg Seafood

- Nissui

- Charoen Pokphand Foods Public Company Limited

- Cooke Aquaculture

- Mitsubishi Corporation.

Frequently Asked Questions

The global seafood base market is projected to reach US$ 39.1 billion in 2026.

Rising global seafood consumption, aquaculture expansion, increasing demand for value-added seafood products, and advancements in cold-chain and processing infrastructure are driving the market.

The market is poised to witness a CAGR of 2.9% from 2026 to 2033.

Development of sustainable and traceable seafood solutions, growth in ready-to-cook and ready-to-eat seafood products, and technological integration in aquaculture and processing present key market opportunities.

Some of the key market players include Thai Union Group PCL., Mowi, Cermaq Group AS, Lerøy, Grieg Seafood, and Nissui.