- Rail

- Railway Shock Absorber Market

Railway Shock Absorber Market Size, Share, Trends, Growth, Regional Forecasts 2025 - 2032

Railway Shock Absorber Market by Product (Hydraulic Shock Absorbers, Pneumatic (Air) Shock Absorbers, Mechanical (Spring/Coil) Shock Absorbers), Function (Primary Suspension, Secondary Suspension, Yaw Dampeners), Train Type (High Speed Train, Intercity Train), and Regional Analysis 2025 - 2032

Railway Shock Absorbers Market Share and Trends Analysis

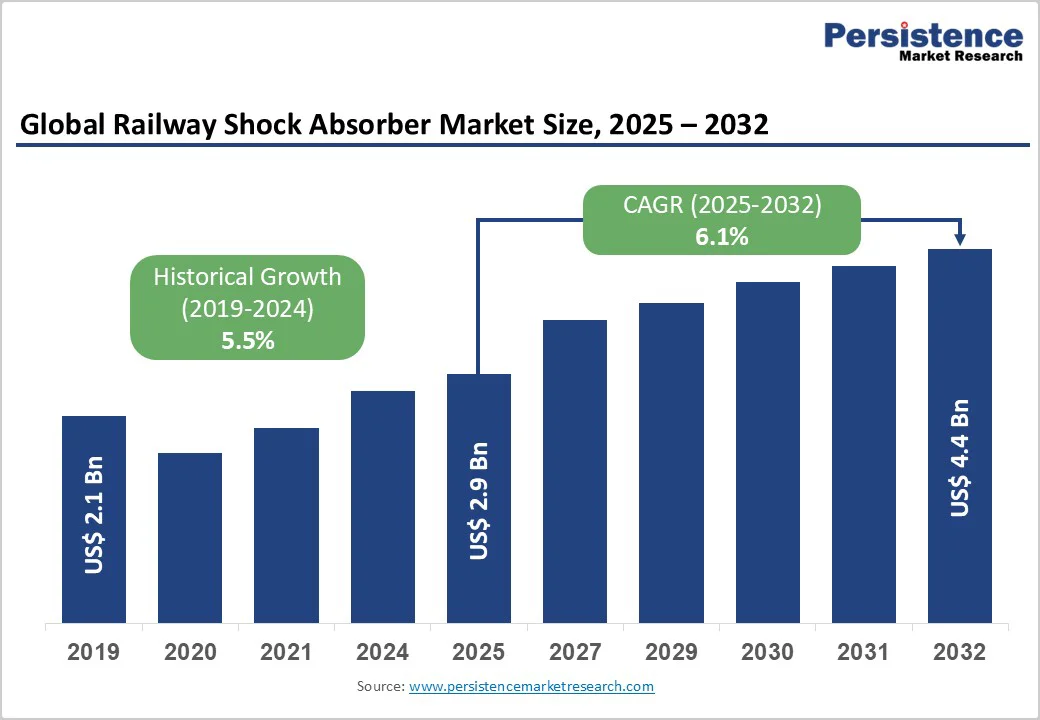

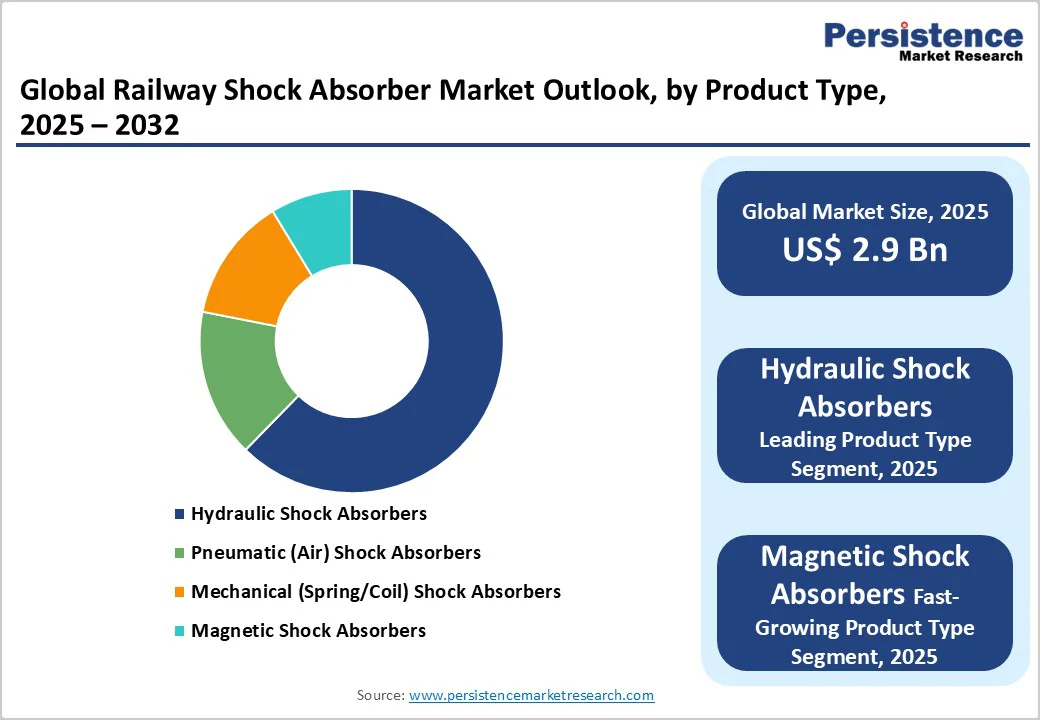

The global railway shock absorber market size is valued at US$2.9 billion in 2025 and is projected to reach US$4.4 billion, growing at a CAGR of 6.1% between 2025 and 2032.

The market expansion is propelled by accelerating railway infrastructure investments across the Asia Pacific and Europe, particularly in high-speed rail expansion and urban metro system modernization. Rising demand for enhanced passenger comfort, stringent safety regulations, and technological advancements in damping systems are creating sustained momentum. The shift toward electrification and environmental sustainability further reinforces market growth trajectories across both developed and emerging economies.

Key Industry Highlights:

- Hydraulic Shock Absorbers dominate with a 62% market share, maintaining technology leadership across all rail applications.

- Magnetic Shock Absorbers fastest-growing at 8.5% CAGR, emerging as preferred choice for metro and high-speed applications.

- Primary Suspension systems command 36% share, while Pantograph Dampers accelerate at a 7.3% CAGR, reflecting electrification trends.

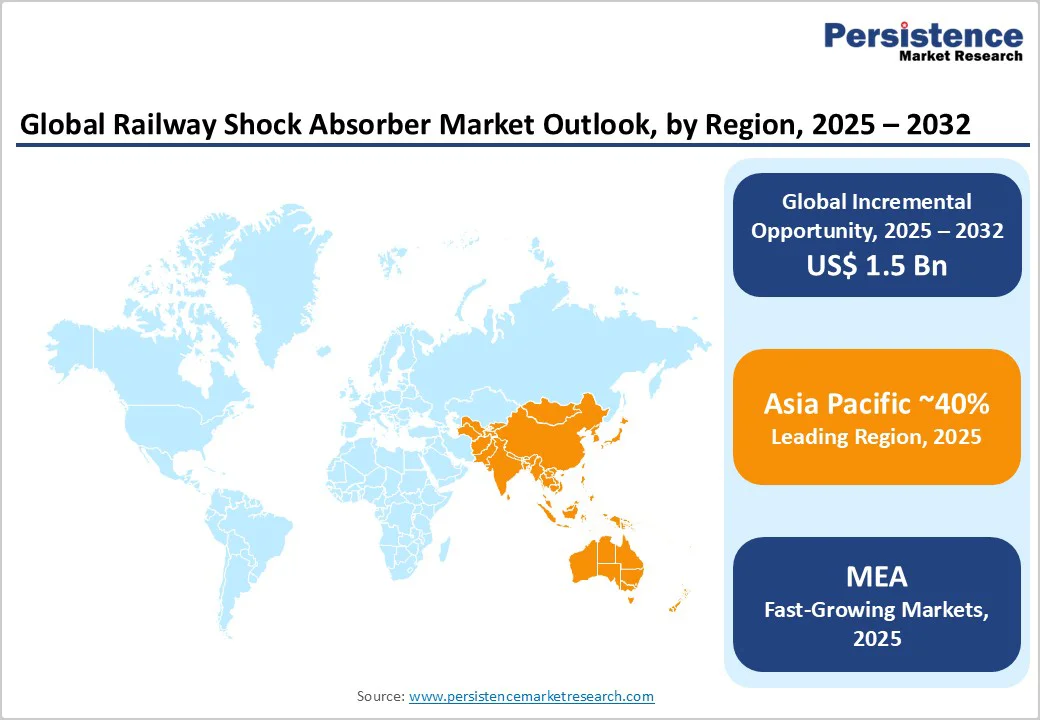

- Asia Pacific dominates with 40% global market share and 6.7% CAGR, driven by China's HSR expansion and India's infrastructure modernization.

- North America holds an 18% share, driven by freight modernization and locomotive electrification initiatives.

- Siemens-Knorr-Bremse partnership (March 2025) establishes standardized HSR damper specifications, creating OEM lock-in advantages.

- ZF's India localization (October 2025) demonstrates 20-30% cost reduction potential through domestic manufacturing, enabling competitive penetration of emerging markets.

| Key Insights | Details |

|---|---|

|

Railway Shock Absorber Market Size (2025E) |

US$2.9 billion |

|

Market Value Forecast (2032F) |

US$4.4 billion |

|

Projected Growth CAGR (2025-2032) |

6.1% |

|

Historical Market Growth (2019-2024) |

5.5% |

Market Dynamics Analysis

Drivers - Accelerating Railway Infrastructure Investment and Modernization

Global governments are committing unprecedented capital to railway infrastructure development, recognizing rail transport MRO as a sustainable alternative to road congestion. The European Commission's High-Speed Rail Action Plan (November 2025) targets connecting major nodes at 200+ km/h by 2040, with investments aimed at significantly reducing journey times across cross-border corridors. India's ambitious National Rail Plan Vision 2030 targets 100% electrification and 160+ kmph speeds on various routes, coupled with the Mumbai-Ahmedabad High-Speed Rail project, which requires around US$17 billion in investment.

Similarly, China continues to expand its HSR network, which now spans over 40,000 kilometers, driving demand for advanced shock-absorption systems across the passenger and freight rail segments. Asia-Pacific countries are collectively investing billions in rail modernization, creating sustained demand for high-performance hydraulic and pneumatic shock absorbers to handle higher operational speeds and loads. The compounding effect of these infrastructural investments multiplies shock absorber demand, as every kilometer of new rail infrastructure requires appropriately engineered damping systems.

Technological Advancement and Adoption of Semi-Active Damping Systems

The railway industry is transitioning from passive to semi-active and adaptive damping technologies, enabling real-time performance optimization. Magnetorheological (MR) dampers and electronically controlled systems are gaining traction, offering superior vibration isolation compared to conventional hydraulic systems. Industry leaders are investing heavily in IoT-enabled condition monitoring and predictive maintenance capabilities, with integrated sensors enabling real-time performance tracking and extending component lifecycle.

Market innovations include variable damping characteristics, compact twin-tube designs with reduced maintenance requirements, and customizable performance curves tailored to specific rail applications. ZF Friedrichshafen's recent launch of locally produced dampers in India, featuring maintenance-free twin-tube designs and high dynamic stiffness, exemplifies the technological convergence across the sector. The integration of smart technologies for vibration control directly enhances passenger safety, reduces operational downtime, and justifies premium pricing for advanced absorber solutions.

Restraint - High Initial Capital Investment and Complex Maintenance Requirements

Advanced shock absorber systems represent substantial capital expenditures for railway operators, particularly in resource-constrained regions. Retrofitting existing rail fleets with hydraulic or semi-active dampers requires significant engineering interventions, including civil modifications and integration testing, thereby substantially increasing total project costs. Cost-conscious developing nations frequently opt for mechanical spring-based alternatives despite inferior performance characteristics, limiting the addressable market in price-sensitive segments.

Specialized maintenance requirements for hydraulic systems, including fluid monitoring, seal replacement, and pressure calibration, demand trained technician availability and spare parts inventory, creating persistent lifecycle cost burdens. The complexity of integrating advanced damping technologies into aging rail infrastructure compounds implementation challenges and extends deployment timelines.

Supply Chain Vulnerabilities and Raw Material Price Volatility

The global shock absorber manufacturing sector faces persistent supply chain disruptions and cost inflation affecting specialized hydraulic fluid, precision-engineered seals, and specialty metals. Fluctuating commodity prices for steel, aluminum, and rare-earth elements (critical for electromagnetic dampers) introduce cost unpredictability and margin compression. Geographic concentration of manufacturing capabilities in specific regions creates bottleneck risks, as demonstrated during pandemic-related supply chain disruptions affecting global rail projects. Raw material scarcity for advanced damper technologies, particularly specialty elastomers and precision components, constrains production scalability and limits market expansion potential in high-growth regions.

Opportunity - High-Speed Rail Expansion in Emerging Markets

Emerging Asian economies, particularly India, Indonesia, and Southeast Asian nations, are initiating large-scale HSR projects requiring specialized shock absorber systems capable of managing extreme dynamic loads at elevated speeds. India's high-speed rail corridor investments, supported by Japanese concessional financing, present multi-year procurement opportunities for advanced damping technologies.

ASEAN countries are developing regional rail connectivity initiatives, creating consolidated demand for harmonized damper specifications across borders. The projected CAGR of 6.7% in Asia Pacific markets outpaces global averages, indicating superior growth trajectories in emerging rail infrastructure segments. Localized manufacturing capabilities, such as ZF's Pune-based operations in India—enable market penetration through reduced costs and regulatory compliance advantages, expanding addressable markets by 15-20% compared to imported alternatives.

Upgrade of Legacy Rail Infrastructure and Fleet Modernization

Developed nations possess aging rail fleets requiring systematic modernization to meet contemporary safety and efficiency standards. Europe's €15.5 billion rail investment allocation (2021-2023) prioritizes electrification and line speed improvements, necessitating compatible damping system upgrades. North American freight operators are investing in locomotive modernization programs, with companies such as Wabtec securing major contracts for brake and damping system integration. These fleet upgrades represent consolidated multi-year purchasing commitments, creating predictable revenue streams and enabling manufacturers to justify R&D investments in next-generation technologies. The estimated market size for European rail upgrades alone exceeds US$3 billion annually, representing 18% of global opportunities.

Category-wise Analysis

Product Type Insights

Hydraulic shock absorbers hold a 62% market share and are the dominant product category across all railway applications. These systems deliver superior damping performance, precise pressure control, and reliability across diverse operating conditions, making them the preferred choice for primary suspension systems (wheelset-to-bogie interfaces) and secondary suspension applications. Established manufacturers, including ITT KONI, ZF Friedrichshafen, and Alstom Dispen, have optimized hydraulic designs over decades, creating technical barriers to market entry. The mature hydraulic technology segment benefits from standardized specifications across European and Asian rail operators, facilitating economies of scale and cost optimization. Hydraulic systems account for approximately 35-40% of total suspension system costs, underscoring their critical value contribution.

Magnetic damping systems represent the fastest-growing product category with an 8.5% CAGR, driven by technological maturation and cost reduction in magnetorheological (MR) fluid formulations. These systems offer superior vibration isolation, reduced maintenance requirements (eliminating oil leakage concerns), and enhanced response characteristics compared to conventional hydraulic alternatives. The emerging adoption of magnetic dampers in high-speed and metro applications reflects recognition of their performance advantages in demanding operational environments. While current market penetration remains modest relative to hydraulic systems, accelerating technology adoption in Asia Pacific and European metro systems suggests magnetic dampers will capture 15-20% market share by 2032.

Function Insights

Primary suspension systems (wheelset-to-bogie interfaces) represent the largest functional category, with 36% market share, and manage vertical, horizontal, and longitudinal forces resulting from track irregularities and dynamic loads. These systems directly affect ride quality, comfort, and component longevity, underscoring the need for continuous technology investment and market focus. Advanced primary suspension dampers must withstand extreme operational pressures while maintaining precise damping characteristics across diverse speed ranges and load conditions. The standardized nature of primary suspension requirements creates competitive advantages for established manufacturers with proven performance histories across global rail operators.

Pantograph dampers for current collection systems represent the fastest-growing functional segment with a 7.3% CAGR, driven by increasing electrification rates across global rail networks. These specialized dampers isolate vibrations transmitted from catenary systems, protecting electrical contact quality and extending equipment lifespan. As European and Asian railways accelerate electrification initiatives, demand for pantograph dampers grows disproportionately compared with overall market trends. The specialized nature of pantograph applications creates market opportunities for niche manufacturers with focused expertise in the dynamics of electrical pantograph systems.

Train Type Insights

Passenger trains represent the dominant train category with 25% market share, reflecting passenger comfort priorities and extensive urban metro deployments across developed economies. Passenger train dampers must balance ride comfort optimization with operational efficiency, creating demand for advanced semi-active systems capable of real-time performance adjustment. European passenger train fleets, particularly in Germany, France, and the UK, have established high comfort standards, creating competitive benchmarks for global markets.

Light rail systems (including trams and urban transit) represent the fastest-growing train category with a 7.9% CAGR, with closely competitive growth from high-speed trains and monorails. Rapid urbanization across the Asia Pacific and emerging markets is driving massive light rail deployment, with China, India, and ASEAN nations initiating coordinated metro expansion programs. These systems require compact, maintenance-efficient damping solutions optimized for urban operating environments with frequent acceleration-deceleration cycles. The projected expansion of light rail networks by 15,000+ kilometers globally through 2032 is expected to sustain demand for specialized shock absorbers.

Regional Market Insights

North America Railway Shock Absorber Market Trends

North America holds approximately 18% of the global market share, with mature rail infrastructure prioritizing freight transportation. The locomotive market in the region is growing significantly, accounting for 2-3% of the total costs of locomotive systems related to shock absorbers. The United States' increasing emphasis on electric and autonomous locomotives for emissions reduction creates differentiated damping requirements, as evidenced by Wabtec's $100+ million in battery-electric locomotive orders, indicating significant market momentum. Government initiatives, including the Infrastructure Investment and Jobs Act allocate substantial capital to rail modernization, supporting steady shock absorber demand growth.

North American competitive dynamics are characterized by technological sophistication, with established players investing heavily in IoT-enabled monitoring systems and predictive maintenance platforms. The region's regulatory framework emphasizes safety and environmental compliance, driving continuous product evolution. Freight train applications dominate North American demand, requiring robust shock absorbers capable of handling 150+ ton loads at sustained operating speeds. The region's focus on operational efficiency and reduced maintenance costs incentivizes the adoption of advanced damping technologies despite higher initial capital requirements.

Europe Railway Shock Absorber Market Trends

Europe represents a growth market with a 5.8% CAGR, driven by ambitious rail modernization initiatives under European Union sustainability mandates. The region's rail investment allocation for 2021-2023 and the High-Speed Rail Action Plan aiming for 2040 implementation, offer substantial multi-year procurement opportunities. Germany, France, Spain, and the UK together account for around 60% of European rail spending, with a focus on electrification, line speed enhancements, and cross-border connectivity.

European manufacturers, including Knorr-Bremse, Trelleborg, and regional players, maintain strong competitive positions through technology leadership and established relationships with major OEMs, including Alstom, Siemens, and Bombardier. The region's stringent noise-reduction regulations and passenger comfort standards drive continuous product innovation, with semi-active and adaptive damping systems gaining market share. Regulatory harmonization through EU standards enables manufacturers to achieve economies of scale while serving multiple national rail operators, supporting stable margins and enabling technology investment.

Asia Pacific Railway Shock Absorber Market Trends

Asia Pacific dominates global markets with 40% of market share and 6.7% CAGR, positioning the region as the primary growth engine for the worldwide railway shock absorber sector. China's dominance in HSR deployment, coupled with India's ambitious infrastructure initiatives and ASEAN urbanization trends, creates substantial consolidated demand. China's continued expansion of its HSR network and modernization of freight logistics create persistent demand for advanced damping technologies across all applications. India's high-speed rail project and metro system deployments represent emerging opportunities, with companies like ZF establishing localized manufacturing to capture market share.

ASEAN nations, including Thailand, Indonesia, and Malaysia, are initiating light rail and metro projects, creating incremental demand opportunities. The region's manufacturing cost advantages enable competitive pricing while supporting margin sustainability through operational efficiencies. Strategic localization investments by global manufacturers, including production facilities in Pune (ZF), Hosur (Wabtec), and Bangalore, indicate confidence in Asia Pacific's long-term growth prospects and create competitive barriers through established supply chain relationships.

Competitive Landscape

The global railway shock absorber market exhibits moderate concentration with approximately 55-60% market share held by the leading players (ITT KONI, Alstom Dispen, ZF Friedrichshafen, KYB, Dellner Dampers, & Others). The market remains sufficiently fragmented to accommodate regional specialists and niche technology providers, with 12-15 significant competitors maintaining viable market positions. Market entry barriers stem from stringent safety certifications, established OEM relationships, and significant R&D investments required for technology validation.

Leading players leverage scale economies, diversified product portfolios, and global manufacturing networks to sustain competitive advantages. Competitive positioning reflects technology leadership, regulatory compliance capabilities, and customer relationship depth rather than price competition alone, supporting relatively stable margin profiles across market cycles.

Strategic Developments:

- In March 2025, Siemens AG and Knorr-Bremse AG entered a strategic partnership to co-develop advanced noise-reduction dampers for high-speed rail applications. The collaboration unites Siemens’ systems integration expertise with Knorr-Bremse’s leadership in damping technology, aiming to set new performance benchmarks for next-generation HSR platforms. This initiative not only advances ride comfort and acoustic efficiency but also establishes standardized damper specifications, strengthening long-term relationships with major OEMs across the global high-speed rail market.

- In October 2025, ZF Friedrichshafen AG unveiled its locally produced advanced railway dampers at the International Railway Equipment Exhibition (IREE) 2025 in New Delhi. The new maintenance-free twin-tube damper range, engineered with customized characteristic curves for Indian track conditions, marks a major step in ZF’s regional localization strategy. With a US$20–30 million investment in its Chakan facility near Pune, ZF reinforces its commitment to India’s rapidly expanding high-speed rail and metro segments, offering cost-efficient, compliant, and supply chain–optimized solutions tailored for domestic OEMs.

Companies Covered in Railway Shock Absorber Market

- ITT KONI

- Alstom Dispen

- ZF Friedrichshafen AG

- KYB Corporation

- Dellner Dampers

- Knorr-Bremse AG

- Parker Hannifin Corporation

- Wabtec Corporation

- CRRC Corporation

- Escorts Limited

- Suomen Vaimennin

- Trelleborg AB

- SKF

Frequently Asked Questions

The global Railway Shock Absorber Market size is valued at US$ 2.9 Billion in 2025 and is projected to reach US$ 4.4 Billion by 2032.

The Railway Shock Absorber Market is primarily driven by accelerating government railway infrastructure investments, technological advancement in semi-active and magnetorheological dampers, stringent regulatory mandates for passenger safety and environmental compliance, and rising passenger comfort expectations driving adoption of advanced suspension technologies across freight, passenger, and metro rail segments.

The Railway Shock Absorber Market is projected to grow at a 6.14% CAGR between 2025-2032.

Key market opportunities include expanding high-speed rail in emerging Asian markets, modernizing outdated rail infrastructure in North America and Europe, integrating AI-driven predictive maintenance and IoT-based condition monitoring, and promoting localized manufacturing in developing regions.

Leading market players include ITT KONI, Alstom Dispen, ZF Friedrichshafen, KYB Corporation, Dellner Dampers, Knorr-Bremse AG, Parker Hannifin Corporation, and SKF, collectively commanding significant market share supporting competitive positioning across global rail segments.