- Automotive

- Motorized Quadricycle Market

Motorized Quadricycle Market Size, Share, Trends, Growth, Regional Forecasts, 2026 - 2033

Motorized Quadricycles Market by Valve Type (Gate, Globe, Ball, Butterfly, Plug, Check, Safety Relief, Other Customized), Material Type (Cast Steel, Brass, Carbon Steel, Stainless Steel, Bronze, Other Alloys), Function (Manual, Automatic), End-user (Oil & Gas, Chemical, Water & Wastewater Treatment, Power Plants, Paper & Pulp, Other Industrial), and Regional Analysis from 2026 - 2033

Motorized Quadricycle Market Share and Trends Analysis

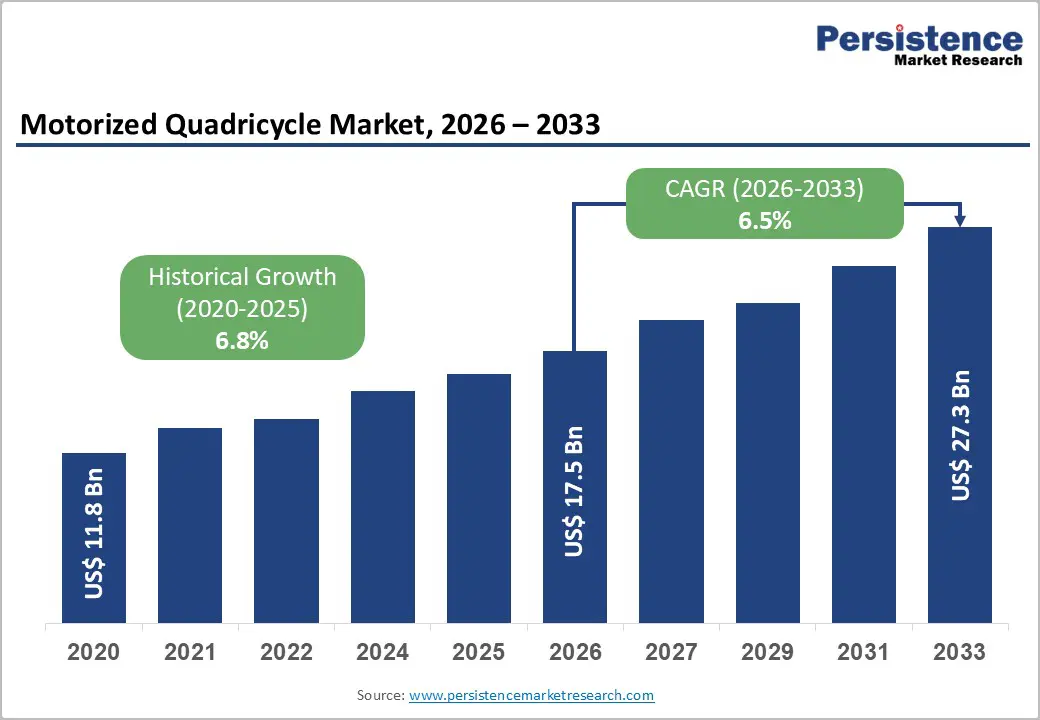

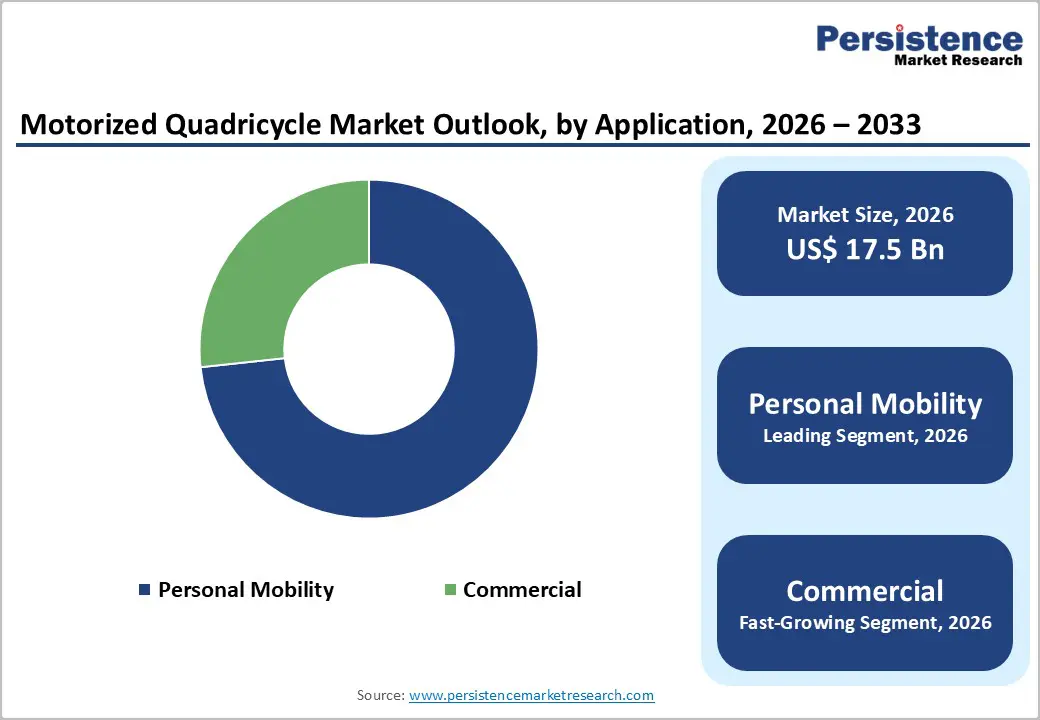

The global motorized quadricycle market size is likely to be valued at US$17.5 billion in 2026 and is projected to reach US$27.3 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033. Market expansion is fundamentally driven by accelerating urbanization and traffic congestion in metropolitan centers globally, compelling consumers and municipalities to adopt compact, fuel-efficient urban mobility solutions.

The transition toward electric propulsion systems, supported by stringent emission regulations including European Union L6e/L7e standards and government incentives for zero-emission vehicles, is transforming product development strategies across the industry.

Key Industry Highlights:

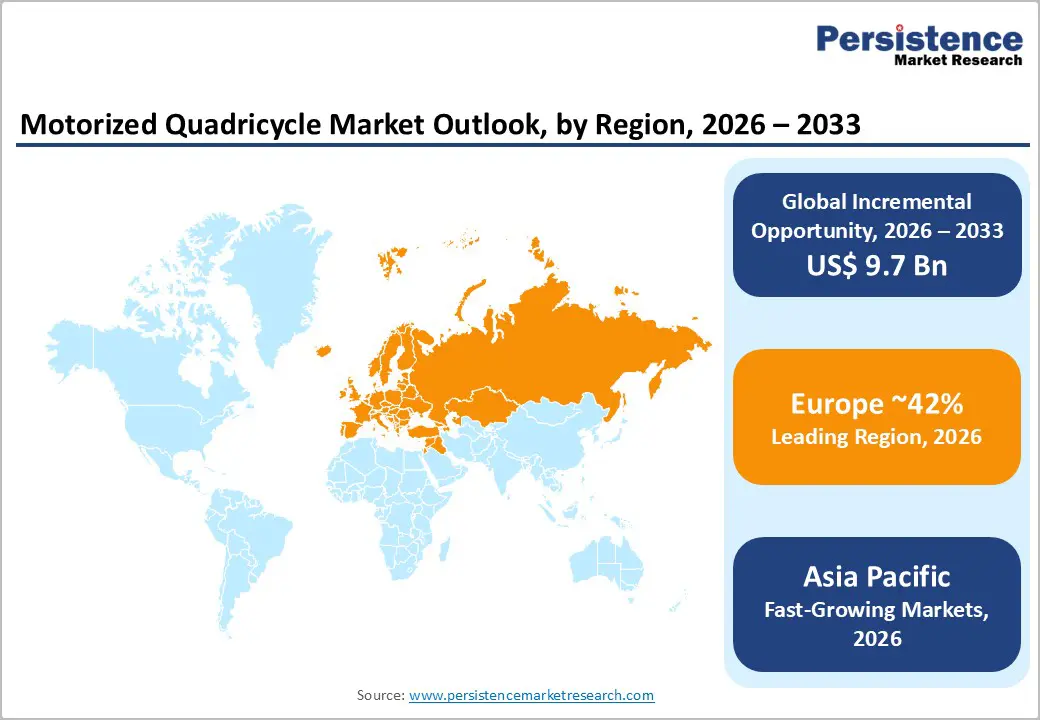

- Europe retains a dominant 42% global market share with mature regulatory frameworks, comprehensive L6e/L7e classifications, and established consumer acceptance, representing approximately USD 6.9 billion market value in 2025.

- Asia Pacific demonstrates the strongest growth momentum at a 7.3% CAGR, driven by rapid urbanization in China, India, and ASEAN nations, manufacturing cost advantages, and government electric vehicle incentive programs that support market development.

- Light quadricycles dominate with 62% market share, serving personal mobility applications, while heavy quadricycles grow at a 5.7% CAGR, driven by commercial last-mile delivery and enhanced payload capacity requirements.

- Electric propulsion holds a significant 58% market share. It dominates growth trajectory, while internal combustion engine variants maintain a steady 2.5% CAGR, reflecting market transition toward zero-emission mobility solutions and regulatory pressures favoring electric powertrains.

- Personal mobility applications command 73% market share as the dominant segment, while commercial applications emerge as the fastest-growing at 7.1% CAGR, driven by e-commerce logistics expansion and shared mobility platform adoption.

- Citroën launched the redesigned 2025 Ami model at the Paris Motor Show (October 2024), following 65,000+ cumulative sales, demonstrating a sustained commitment to the quadricycle segment and market leadership consolidation strategies.

| Key Insights | Details |

|---|---|

|

Motorized Quadricycles Market Size (2026E) |

US$ 17.5 Billion |

|

Market Value Forecast (2033F) |

US$ 27.3 Billion |

|

Projected Growth CAGR (2026-2033) |

6.5% |

|

Historical Market Growth (2020-2025) |

6.8% |

Market Dynamics Analysis

Drivers - Rapid Urbanization and Metropolitan Traffic Congestion Solutions

Global urbanization trends are driving unprecedented demand for compact, efficient alternatives to traditional automobiles. According to the United Nations Department of Economic and Social Affairs, urban populations are projected to reach 68% of the total global population by 2050, intensifying traffic congestion and parking constraints in metropolitan centers worldwide. Motorized quadricycles, with vehicle dimensions typically measuring 2.3-3.0 meters in length and 1.2-1.5 meters in width, offer substantial advantages in navigating congested urban environments where conventional automobiles face operational limitations.

European cities, including Paris, Rome, and Barcelona, have witnessed electric quadricycle registrations increase by 30-40% between 2020 and 2023, reflecting consumer adoption of micro-mobility solutions that address urban transportation challenges. Quadricycles classified under European Union categories L6e (light quadricycles with a maximum speed of 45 km/h) and L7e (heavy quadricycles with a maximum speed of 90 km/h) provide regulatory frameworks enabling streamlined vehicle approval processes compared to conventional automobiles. The compact form factor enables quadricycles to utilize motorcycle parking spaces and navigate narrow urban streets inaccessible to standard vehicles, creating compelling value propositions for urban commuters facing limited parking availability and traffic congestion constraints.

E-Commerce Boom and Last-Mile Delivery Logistics Transformation

The exponential growth of e-commerce and on-demand delivery services is creating substantial commercial demand for compact, maneuverable delivery vehicles optimized for urban logistics operations. The last-mile delivery vehicle market is projected to grow at a 7.6% CAGR through 2032 with electric quadricycles capturing an increasing market share for urban delivery applications. Leading logistics providers, including Amazon India, DHL, and regional courier services, are deploying electric quadricycle fleets for last-mile delivery operations, capitalizing on lower operational costs, superior maneuverability in congested environments, and zero direct emissions. Heavy quadricycles (L7e category) with payload capacities reaching 450-600 kg provide optimal solutions for package delivery, food distribution, and small-scale commercial transportation within urban centers.

Operating cost advantages are substantial, with electric quadricycles demonstrating 40% lower last-mile delivery costs compared to conventional light commercial vehicles, driven by reduced fuel expenses, simplified maintenance requirements, and exemption from congestion charges in multiple European cities. Companies like Bolt introduced Bajaj Qute quadricycle rides in Johannesburg in 2023, demonstrating commercial viability for ride-hailing applications. The commercial application segment is projected to grow at 7.1% CAGR, reflecting sustained adoption by logistics operators, food delivery services, and shared mobility platforms leveraging quadricycles' operational efficiency advantages.

Restraints - Safety Concerns and Limited Crash Protection Standards

Safety concerns from quadricycles’ compact size, lightweight construction, and limited passive protection create major adoption barriers, especially in safety-conscious developed markets. L6e and L7e regulations allow manufacturers to bypass stringent crash standards, excluding side-impact protection, ADAS, and full airbag systems. Euro NCAP tests show poor performance, with models like Tazzari Zero receiving one-star ratings. Studies indicate higher fatality risks, frequent head and neck injuries, and weak occupant protection. Regulatory inconsistencies and family safety concerns restrict use mainly to urban commuting and delivery segments.

Competition from Alternative Electric Mobility Solutions and Market Cannibalization

Electric quadricycles face rising competition from alternative urban mobility solutions, including electric bicycles, e-scooters, electric three-wheelers, and compact battery electric cars offering similar or superior value. Asia Pacific electric two-wheeler markets growing rapidly highlight shifting preferences toward lighter mobility options. E-bikes and e-scooters cost significantly less, undercutting quadricycle pricing. Compact EVs such as Renault Zoe and Fiat 500e provide better safety, weather protection, and highway capability. Shared micromobility reduces personal vehicle demand. Battery electric vehicle cost parity may further erode quadricycle price advantages for consumers.

Opportunity - Electric Quadricycle Adoption Accelerating Market Transformation

Electric propulsion dominates quadricycle market growth trajectories, with electric variants projected to capture 58% market share in 2025 and accelerating adoption driven by regulatory mandates, operational cost advantages, and consumer environmental preferences. Electric quadricycles eliminate tailpipe emissions, reduce noise pollution, and deliver substantially lower operational costs compared to internal combustion engine equivalents, with electricity costs typically 70-80% lower than gasoline on a per-kilometer basis.

Battery technology advancements, including lithium-ion energy density improvements and declining battery pack costs (falling from USD 1,200/kWh in 2010 to approximately USD 150/kWh in 2024), are enhancing electric quadricycle range capabilities while reducing purchase price premiums. Leading manufacturers, including Citroën (Ami), Renault (Twizy successor Mobilize Duo), Fiat (Topolino), and Bajaj (Qute) are prioritizing electric powertrains in new product development, with internal combustion engine variants projected to experience steady but slower 2.5% CAGR growth. Manufacturers developing swappable battery systems, solar charging integration, and vehicle-to-grid (V2G) capabilities create differentiation opportunities supporting premium positioning and enhanced customer value propositions.

Commercial Applications and Fleet Deployment Expansion

Commercial applications, particularly last-mile delivery and shared mobility services, represent the fastest-growing market segment with a 7.1% CAGR projection through 2032. E-commerce logistics providers are deploying electric quadricycle fleets for urban delivery operations, leveraging vehicles' compact dimensions, zero-emission operation, and lower total cost of ownership. Shared mobility platforms, including ride-hailing services, car-sharing programs, and tourism operators, are adopting quadricycles for specialized applications, including resort transportation, airport campus mobility, and urban tourism services.

Heavy quadricycles with enhanced payload capacity (450-600 kg) and extended range capabilities (120-160 km) address commercial operator requirements for sustained daily operations and cargo transportation. Manufacturers developing specialized commercial variants with telematics integration, fleet management systems, and customized cargo configurations capture premium commercial segments. Market sizing estimates indicate commercial applications could represent USD 5-7 billion of total market value by 2032, with fleet operators providing predictable, high-volume purchase commitments supporting manufacturer production planning and economies of scale achievement.

Category-wise Analysis

Product Type Insights

Light quadricycles (L6e) dominate the global market with a 62% share, supported by favorable regulations, affordability, and alignment with urban mobility trends. Defined under EU standards, they feature lightweight construction, limited power, and capped speeds, enabling simplified approvals and reduced licensing barriers. Models like Citroën Ami, Renault Twizy, and Fiat Topolino demonstrate mass acceptance, with accessible pricing appealing to cost-conscious consumers. Compact size, low operating costs, and youth accessibility further drive metropolitan adoption.

Heavy quadricycles (L7e) grow at around 5.7% CAGR, driven by commercial uses including last-mile delivery and shared mobility. Higher payloads, longer range, and faster speeds support logistics efficiency, with models like Bajaj Qute and Aixam Pro meeting urban transport demands.

Propulsion Type Insights

Electric propulsion leads the global motorized quadricycle market with a commanding 58% share, supported by regulations, cost efficiency, and rising environmental awareness. Electric quadricycles deliver zero tailpipe emissions, qualify for subsidies, and offer up to 70% lower operating costs than gasoline models. Popular vehicles like Citroën Ami, Renault Twizy, and Fiat Topolino show strong adoption, especially in Europe. Improved lithium-ion batteries extend driving ranges to 120–160 kilometers, while standard outlets enable convenient charging for urban commuters daily.

Internal combustion quadricycles hold 42% share in regions with limited charging access. Efficient engines suit rural and extended-range use in Asia. However, tightening emission rules and zero-emission mandates restrict growth, shifting investment toward electric models while ICE remains relevant for affordability-focused buyers.

Application Insights

Personal mobility applications lead the motorized quadricycle market with a commanding 73% share, driven by urban commuting demand, affordability, and rising environmental awareness. These vehicles serve individuals seeking compact, efficient transport for short trips and daily travel. Light quadricycles such as Citroën Ami and Renault Twizy dominate due to low running costs, easy parking, and minimal licensing. Adoption is strongest across France, Italy, Germany, and Spain, supported by incentives and sustainable urban infrastructure.

Commercial applications are the fastest-growing segment with 7.1% CAGR, driven by e-commerce logistics, last-mile delivery, and shared mobility. Heavy quadricycles provide higher payloads, lower operating costs, zero-emission compliance, and efficient urban access for fleet operators globally.

Regional Market Insights

North America Motorized Quadricycles Market Trends

North America exhibits notable 5.9% CAGR growth through 2032, though market share remains below Europe due to fragmented regulations and limited consumer familiarity. The United States faces inconsistent classifications and lacks standardized L6e/L7e categories, with most quadricycles treated as NEVs restricted to low speeds and non-highway use. Despite barriers, opportunities expand across resorts, campuses, retirement communities, and last-mile delivery. Federal credits and state incentives improve affordability, while manufacturers adapt compliant models.

Regulatory fragmentation persists, yet states like California, Florida, and Arizona support low-speed vehicle adoption. Partnerships with European firms, venture capital interest, connected technologies, and sustainable mobility demand position North America for steady quadricycle market development.

Europe Motorized Quadricycles Market Trends

Europe retains its dominant global position, commanding nearly 42% of the motorized quadricycle market valued around USD 6.9 billion in 2025, supported by robust regulations, mature consumer adoption, and advanced urban infrastructure. EU Regulation 168/2013 standardizes L6e and L7e classifications, enabling scalable multi-country certification. France leads registrations, followed by Italy, Germany, Spain, and the United Kingdom. Urban congestion, sustainability awareness, and incentives continue driving demand across major European cities.

Harmonized regulations allow single-type approvals, providing strong competitive advantages. Governments promote electric quadricycles through subsidies, tax benefits, and congestion charge exemptions. Tightening emission norms accelerate zero-emission adoption, while Aixam, Ligier, Citroën, Renault, Tazzari, and Casalini dominate, with electric variants gaining majority share in France.

Asia Pacific Motorized Quadricycles Market Trends

Asia Pacific demonstrates the strongest regional expansion, registering a robust 7.3% CAGR through 2032, supported by rapid urbanization, a growing middle-class population, and government initiatives promoting sustainable mobility. China, India, and ASEAN nations dominate quadricycle growth, representing major emerging opportunities. China leads through manufacturing scale and expanding domestic demand despite regulatory fragmentation. India shows exceptional momentum from urbanization, Smart Cities projects, and electric mobility incentives, while Japan and South Korea sustain premium technology-driven segments across advanced markets.

The region holds a competitive EV manufacturing edge through low costs, strong policy support, and efficient supply chains. Chinese and Indian players develop cost-effective electric quadricycles. Programs like FAME, NEV subsidies, and ASEAN green mobility initiatives boost adoption, though infrastructure gaps and regulatory inconsistencies require localized strategies and partnerships.

Competitive Landscape

The global motorized quadricycle market remains moderately fragmented, with European leaders such as Renault, Citroën (Stellantis), Aixam-Mega, and Ligier Group holding prominent shares through strong branding, dealer networks, and electric innovation. Stellantis dominates France with around an 80-86% share via Citroën Ami and Fiat Topolino models, showcasing platform synergies. Asian players such as Bajaj Auto, Mahindra & Mahindra, and emerging Chinese brands are rapidly expanding in cost-sensitive markets across India, Southeast Asia, and Africa through competitive pricing and scalable production. Niche firms such as Tazzari EV and Casalini target premium and customized applications, reflecting a dynamic yet consolidating global landscape.

Strategic Developments

- In August 2024, Flowserve completed USD 290 million acquisition of MOGAS Industries severe service valves provider, doubling mining and mineral extraction market exposure while expanding aftermarket revenue opportunities and supporting geographic diversification beyond traditional oil and gas sector focus.

- In August 2024, IMI Critical Engineering unveiled a new Fractionator Inlet Valve design improving safety and refinery operational efficiency by reducing turnaround time by 12 hours, enabling reactor isolation during procedures without removing large rings, and addressing critical safety risks.

Companies Covered in Motorized Quadricycle Market

- Renault Group

- Citroën (Stellantis Group)

- Aixam-Mega

- Ligier Group

- Bajaj Auto Ltd.

- Fiat (Stellantis Group)

- Mahindra & Mahindra

- Tazzari EV

- Club Car (Polaris Inc.)

- Toyota Motor Corporation

- Casalini

- GEM (Global Electric Motorcars)

- Automobiles CHATENET

- Bellier Automobiles

- Loncin Motor Co.

Frequently Asked Questions

The global motorized quadricycle market is likely to be valued at US$ 17.5 Billion in 2026 and is projected to reach US$ 27.3 Billion by 2033.

The motorized quadricycle market is primarily driven by rapid urbanization and metropolitan traffic congestion, e-commerce boom and last-mile delivery logistics transformation, and stringent government emission regulations and electric vehicle incentive programs supporting accelerated electric propulsion adoption.

The motorized quadricycle market is projected to grow at a 6.5% CAGR between 2026 and 2033.

Key market opportunities include electric quadricycle adoption, accelerating market transformation, commercial applications, and fleet deployment expansion, and Asia Pacific emerging markets growth through urbanization, manufacturing localization, and government electric vehicle promotion initiatives.

Key global market players include Renault Group, Citroën (Stellantis Group), Aixam-Mega, Ligier Group, and Bajaj Auto Ltd., collectively commanding significant global market share through established European distribution networks and emerging market penetration, supplemented by Stellantis Group, Mahindra & Mahindra, Tazzari EV, Club Car (Polaris), Toyota Motor Corporation, and Casalini.