- Smart Packaging

- Premium Packaging Market

Premium Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Premium Packaging Market by Material (Paper & Paperboard, Plastic, Others), Packaging Type (Rigid Packaging, Flexible Packaging, Others), End-user Industry, Distribution Channel, and Regional Analysis for 2026 - 2033

Premium Packaging Market Size and Trends Analysis

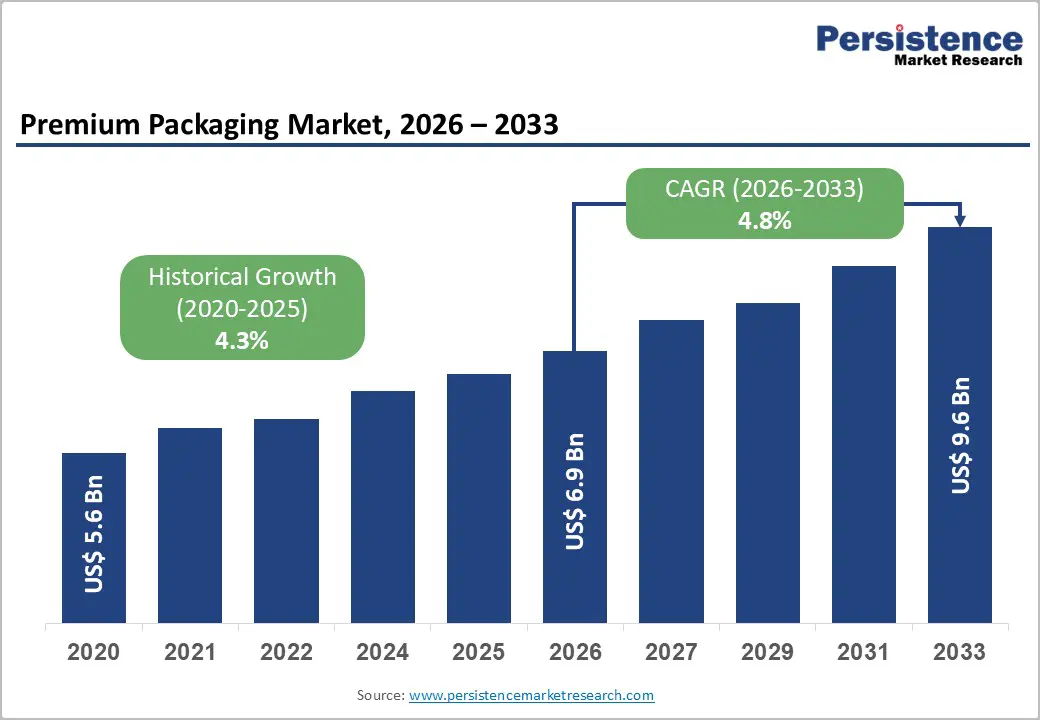

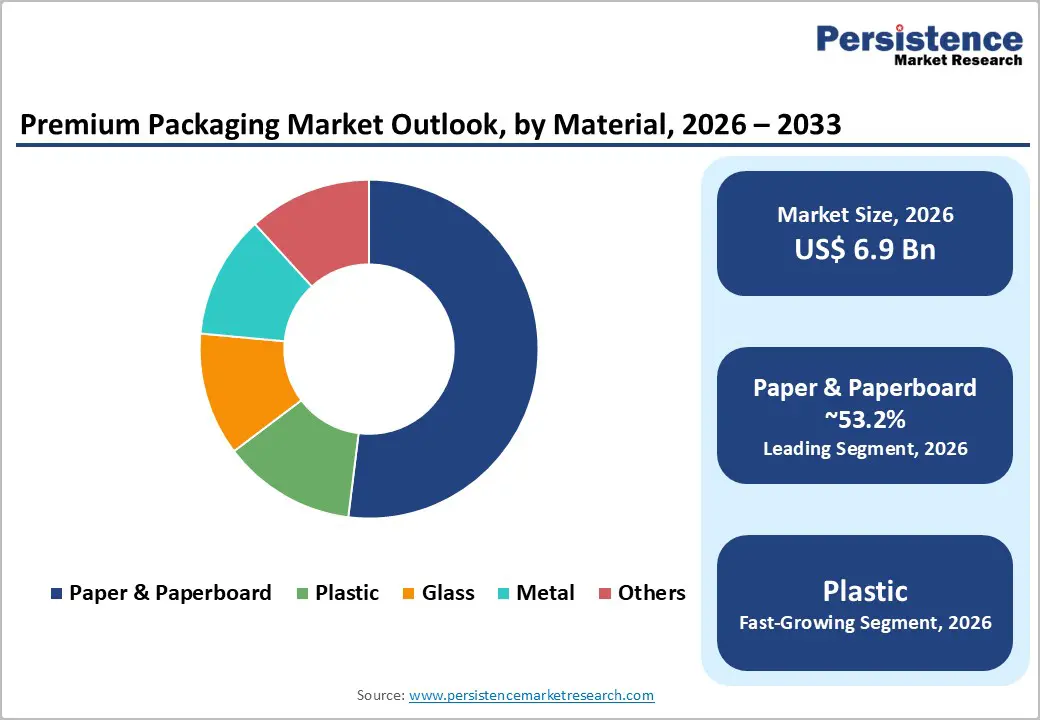

The global premium packaging market is likely to be valued at US$6.9 billion in 2026 and is expected to reach US$9.6 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by accelerating premiumization across cosmetics, beverages, and luxury goods, coupled with rising consumer willingness to pay for differentiated unboxing and brand experiences.

Regulatory pressure for recyclable materials is driving investment in premium paperboard and glass packaging. Sustainability and smart packaging are lifting value per unit despite stable volumes, while raw-material cost volatility and limited specialty capacity remain key risks.

Key Industry Highlights

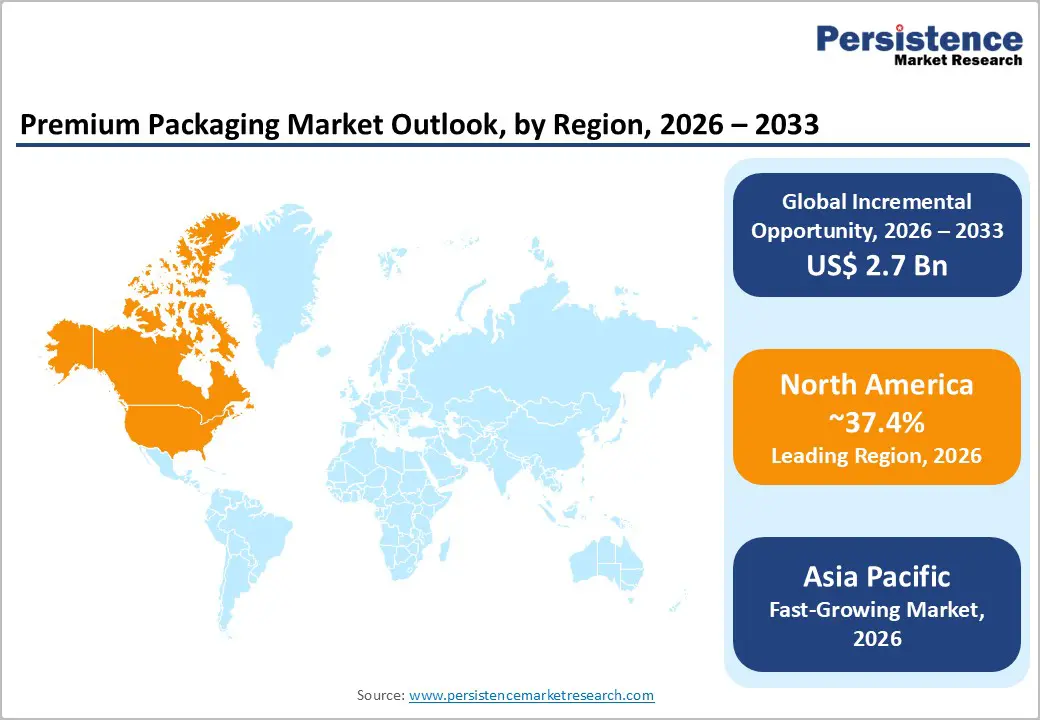

- Leading Region: North America is projected to dominate the market with an estimated 37.4% share, supported by a strong luxury retail ecosystem, high spending on cosmetics and premium beverages, and advanced direct-to-consumer channels.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid premiumization in beauty, rising disposable incomes, and strong e-commerce and social-commerce influence in China, India, and Southeast Asia.

- Investment Plans: Packaging manufacturers are prioritizing digital printing, short-run finishing, recyclable paperboard, PCR plastics, and nearshoring capacity, with a growing share of capital expenditure directed toward sustainable premium materials and smart-packaging features to support customization and faster go-to-market.

- Dominant Material: The paper & paperboard segment is anticipated to lead, accounting for approximately 53.2% of the market share, due to strong recyclability credentials, superior print quality, and widespread use in cartons, rigid boxes, and gift packaging.

- Leading Packaging Type: Rigid packaging is estimated to hold about 56% market share, with boxes contributing roughly 30%, reflecting strong demand for luxury presentation, unboxing experiences, and premium gifting formats across retail and e-commerce channels.

| Key Insights | Details |

|---|---|

| Premium Packaging Market Size (2026E) | US$6.9 Bn |

| Market Value Forecast (2033F) | US$9.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Premiumization and Consumer Experience Economics

Demand for premium, gift-grade, and limited-edition packaging continues to rise across cosmetics, spirits, confectionery, and luxury goods. Brands increasingly invest in tactile substrates, foil stamping, embossing, specialty coatings, and custom closures, as higher perceived product value enables retail price premiums of 8-25%. This pricing power allows brands to allocate higher budgets toward packaging without compromising margins. The shift reflects a broader strategic reallocation of brand spend from traditional advertising toward physical brand experience. For converters, this trend translates into higher margins from design-intensive packaging and finishing services, while brand owners benefit from stronger shelf differentiation and customer engagement.

Regulatory and Retail Sustainability Requirements

Policy initiatives across North America and Europe, including single-use material restrictions, extended producer responsibility programs, and recyclability targets, are reshaping premium packaging material choices. These measures have accelerated demand for high-quality recyclable paperboard and mono-material flexible solutions, driving retrofit investments across premium packaging production lines. Paper and paperboard now dominate the premium material mix due to recyclability, print quality, and compatibility with luxury finishes. Over time, regulatory pressure is reducing reliance on complex multi-material laminates, supporting long-term material substitution toward sustainable premium substrates.

Technology Convergence: Smart Packaging and Personalization

Advances in digital printing, small-batch finishing, and serialization technologies are enabling commercially viable customized premium packaging. Smart authentication features such as NFC tags, holograms, and serialized identifiers help combat counterfeiting in luxury categories while enhancing consumer engagement. Brands increasingly allocate design and innovation budgets to variable printing and smart-packaging features, particularly for limited releases and regional customization. For suppliers, this trend unlocks new revenue streams through design services, data-enabled packaging, and recurring finishing work rather than one-time commodity production.

Barrier Analysis - Input Cost Volatility and Specialty Material Availability

Premium packaging relies on high-grade paperboard, specialty glass finishes, metal embellishments, and advanced coatings, all of which are subject to raw-material price volatility. Sudden increases in pulp, resin, glass cullet, or metal prices compress margins because brand owners often resist full cost pass-through. Small and mid-sized converters face disproportionate risk, increasing consolidation pressure within the industry. In parallel, the limited availability of specialty varnishes and decorative foils creates lead-time risks, forcing manufacturers to adopt hedging strategies or localized sourcing to protect revenue stability.

Regulatory Fragmentation and Compliance Complexity

While sustainability regulations stimulate demand, inconsistent regional standards regarding recyclability definitions, labeling, and additive restrictions raise compliance costs. Global brand owners frequently require multiple packaging variants to meet regional requirements, increasing design, tooling, and certification expenses. In some cases, brands must adopt harmonized solutions that exceed minimum regulatory thresholds, elevating per-unit packaging costs. The effect is slower product launches, reduced flexibility for limited editions, and higher capital expenditure for premium packaging programs.

Opportunity Analysis - Repackaging Services and Nearshoring for Luxury Brands

Luxury brands increasingly favor regionally localized premium packaging to shorten lead times, reduce logistics costs, and mitigate tariff exposure. This shift creates strong demand for converters offering integrated design-to-shelf services, small-lot production, and rapid finishing. Even a modest conversion of global luxury goods spending into nearshore premium packaging represents a substantial incremental revenue opportunity by 2030. Providers that combine creative studios, flexible production lines, and logistics integration are best positioned to capture this growing demand.

Circular Premium Packaging Platforms

Refillable and reusable premium packaging formats are gaining traction, particularly in cosmetics and fragrances. Brands leverage durable outer packaging paired with refill systems to command higher upfront pricing while lowering repeat-purchase costs for consumers. If refillable formats capture a meaningful share of the premium cosmetics segment by 2030, packaging suppliers could generate recurring revenue from refill components, closures, and licensing arrangements. This model enhances customer lifetime value while aligning with sustainability objectives.

Smart Authentication and Anti-Counterfeit Solutions

Counterfeiting remains a material revenue risk for luxury brands. Premium packaging integrated with authentication technologies offers a high-value solution. Adoption across even a fraction of premium spirits and cosmetics SKUs can significantly increase average packaging spend per unit. For packaging suppliers, this creates opportunities in hardware integration, data services, and recurring authentication programs, strengthening long-term client relationships.

Segmentation Analysis

Material Insights

Paper and paperboard are anticipated to dominate with a revenue share of 53.2%, due to their strong recyclability profile, superior print fidelity, and structural versatility across cartons, rigid boxes, and gift packaging. Premium coated and solid bleached sulfate (SBS) boards enable advanced finishing techniques such as embossing, foil stamping, spot UV coatings, and textured varnishes, which are widely used in luxury cosmetics, premium chocolates, and high-end beverage secondary packaging. For example, fragrance cartons and artisanal confectionery gift boxes frequently rely on high-GSM coated paperboard to convey craftsmanship while complying with sustainability requirements.

From a supply-side perspective, paperboard offers cost predictability and scalability compared with glass or metal, supporting both mass-premium and ultra-premium applications. Brand owners benefit from easier regulatory compliance and consumer acceptance, while converters with integrated design studios and in-house finishing lines capture higher margins through value-added services. As regulatory pressure intensifies, paper-based premium solutions continue to replace complex multi-material structures in secondary packaging formats.

Plastic is likely to be the fastest-growing material segment within premium packaging, driven by advancements in recyclable mono-material designs, bio-based polymers, and post-consumer recycled (PCR) resin integration. High-clarity rigid plastics are increasingly used in luxury beauty refills, skincare jars, and fragrance accessories, where transparency and precision molding enhance perceived product quality.

Premium flexible films are also gaining traction in refill pouches for personal care and premium food products, supporting sustainability narratives while reducing material usage. Weight reduction and durability make plastic particularly attractive for e-commerce-oriented premium brands, where shipping efficiency and product protection are critical. Brands increasingly pair sustainable plastic substrates with premium finishes such as soft-touch coatings, metallic inks, and custom closures to maintain luxury appeal. This balance between sustainability, functionality, and aesthetics is accelerating plastic adoption across premium packaging applications, especially in cosmetics and direct-to-consumer channels.

Packaging Type Insights

Rigid packaging is estimated to lead the market, accounting for approximately 56% of the total revenue share in 2026. Rigid boxes, magnetic-closure cases, and multi-layer gift packs are widely used in luxury fashion, premium spirits, watches, and cosmetics to create a differentiated unboxing experience. These formats allow for complex internal structures, protective inserts, and mixed-material combinations that reinforce brand positioning and exclusivity. In luxury retail environments, rigid packaging serves not only as a protective solution but also as a long-term brand artifact, often reused or displayed by consumers.

Premium spirits gift boxes and limited-edition cosmetic sets are prime examples where rigid packaging directly influences purchase decisions. Despite higher unit costs, brands continue to favor rigid formats because they deliver strong perceived value, higher shelf presence, and superior durability across both in-store and premium e-commerce channels.

Premium flexible packaging is likely to expand rapidly as brands seek cost-efficient, lightweight, and sustainability-aligned alternatives to rigid formats. High-barrier pouches, laminated soft boxes, and specialty flexible wraps are increasingly used for premium food, beverage refills, and personal care products. These formats offer excellent shelf impact through advanced printing and finishing, while significantly reducing material consumption and transportation emissions. Growth in direct-to-consumer and subscription-based business models is accelerating adoption, as flexible packaging performs well in shipping and reduces damage rates.

For example, premium coffee, wellness supplements, and beauty refill packs increasingly rely on flexible formats to combine convenience with premium branding. As mono-material and recyclable flexible structures become more widely available, this segment is expected to capture a larger share of premium packaging demand over the forecast period.

Regional Insights

North America Premium Packaging Market Trends - Brand-Led Premiumization and Nearshore Sustainable Innovation

North America is projected to account for approximately 37.4% of global premium packaging demand in 2026, underpinned by a mature luxury retail ecosystem, strong brand-led innovation, and high per-capita spending on cosmetics, premium beverages, and specialty foods. The U.S. leads regional consumption, driven by premium beauty brands, craft spirits, and luxury gifting segments that place a strong emphasis on differentiated packaging design and unboxing experiences. Major U.S.-based cosmetics and fragrance brands increasingly use rigid boxes with specialty paperboard, magnetic closures, and soft-touch finishes to reinforce brand positioning in both physical retail and direct-to-consumer channels.

Sustainability initiatives play a decisive role in shaping material choices across the region. State-level regulations related to packaging waste reduction and recyclability are accelerating the transition toward recyclable paperboard, post-consumer recycled plastics, and simplified material structures. In response, large packaging converters in the U.S. have expanded investments in digital printing, short-run production, and water-based coatings to support premium customization without compromising sustainability goals.

Canada mirrors these trends, with luxury food, beverage, and personal care brands rapidly adopting recyclable premium formats to align with national sustainability objectives. Mexico is increasingly positioned as a nearshore production hub for premium packaging, particularly for rigid boxes, folding cartons, and gift packaging used by North American luxury and beauty brands. Lower manufacturing costs, skilled labor availability, and proximity to U.S. consumer markets have encouraged brands to regionalize supply chains. This shift supports faster turnaround times, reduced logistics risk, and improved responsiveness to seasonal and limited-edition premium packaging demand across the region.

Europe Premium Packaging Market Trends - Luxury Heritage Driven by Regulatory-Led Sustainability

Europe represents the second-largest premium packaging market globally, anchored by long-established luxury brand clusters in France, the U.K., Germany, Italy, and Spain. The region’s dominance is closely linked to its leadership in luxury fashion, cosmetics, fragrances, wines, and spirits, where packaging serves as a critical extension of brand identity and heritage. European luxury brands consistently invest in high-quality secondary packaging, including rigid boxes, premium glass bottles, and decorative paperboard solutions, to support storytelling and perceived exclusivity.

The European market is strongly shaped by regulatory harmonization and stringent sustainability frameworks, which have accelerated the adoption of recyclable and mono-material premium packaging. These policies have driven widespread use of premium paperboard, lightweight glass, and fiber-based alternatives to plastic laminates. As a result, European converters are investing heavily in fiber innovation, metal-free decorative finishes, biodegradable coatings, and closed-loop glass recycling systems. Many luxury fragrance and spirits brands now specify packaging designs that prioritize recyclability without sacrificing visual impact, setting global benchmarks for sustainable premium packaging.

Europe’s role as an innovation hub is reinforced by collaboration between brand owners, packaging suppliers, and material science specialists. Investments in circular packaging systems and refillable luxury formats, particularly in cosmetics and personal care, are reshaping demand patterns across the region. These developments not only strengthen Europe’s leadership in sustainable premium packaging but also influence global design standards adopted by multinational luxury brands operating in other regions.

Asia Pacific Premium Packaging Market Trends - Fast-Growth Premiumization Fueled by Beauty, E-Commerce, and Emerging Luxury

Asia Pacific is likely to be the fastest-growing regional market for premium packaging, driven by rising disposable incomes, rapid expansion of the beauty and personal care sector, and the emergence of strong domestic luxury brands. China accounts for the largest share of regional growth, supported by premiumization across cosmetics, fragrances, specialty beverages, and gifting categories. Chinese beauty and lifestyle brands increasingly invest in high-quality rigid boxes, premium cartons, and decorative finishes to compete with established global luxury brands, particularly in online and social commerce environments.

Japan remains a key market for premium packaging innovation, characterized by meticulous attention to material quality, minimalistic design, and functional elegance. Japanese brands favor high-grade paperboard, precision-molded plastics, and refined finishing techniques that emphasize craftsmanship. India is emerging as a high-growth market, with premium packaging demand rising in cosmetics, wellness products, artisanal foods, and luxury gifting. Domestic brands increasingly adopt premium cartons and rigid boxes to appeal to urban consumers seeking aspirational products.

E-commerce and social commerce platforms across Asia Pacific significantly influence premium packaging design, driving demand for visually distinctive, lightweight, and shipping-optimized formats. While regulatory pressure related to sustainability is less stringent than in Europe, voluntary commitments by brands and growing consumer awareness are accelerating the adoption of recyclable paperboard and PCR-based plastic solutions. Combined with the region’s manufacturing scale and cost advantages, these trends position Asia Pacific as a critical growth engine for premium packaging over the forecast period.

Competitive Landscape

The global premium packaging market exhibits a hybrid structure. Large global packaging companies dominate material-intensive segments such as paperboard, glass, and metal, while specialized luxury packaging firms control high-margin bespoke and gifting applications. Industrial-scale capacity is relatively consolidated, whereas design-driven premium packaging remains fragmented among niche players. Investments in glass manufacturing capacity have alleviated supply constraints for premium beverage packaging. Market leaders emphasize vertical integration, sustainable material innovation, digital printing, and regional manufacturing expansion. Speed-to-market, design differentiation, and verified sustainability credentials remain key competitive differentiators.

Key Industry Developments

- In November 2025, UPM launched UPM Circular Renewable Black™, the world’s first bio-based, near-infrared (NIR) detectable, carbon-negative black pigment designed for premium packaging applications, enabling brands to achieve high-impact black aesthetics while improving recyclability and lowering carbon footprint.

- In January 2025, Mondi launched its Mondi Luxe premium folding carton range, engineered for high-end cosmetics and fragrance packaging with enhanced barrier properties, premium printability, and full recyclability, targeting brands seeking elevated aesthetics with sustainable credentials.

Companies Covered in Premium Packaging Market

- Amcor plc

- Crown Holdings, Inc.

- Smurfit WestRock

- Ardagh Group

- International Paper

- Owens-Illinois

- GPA Global

- Tetra Pak

- Mondi Group

- Ball Corporation

- Prestige Packaging Group

- Pendragon Presentation Packaging

Frequently Asked Questions

The global premium packaging market is estimated to be valued at US$6.9 billion in 2026.

By 2033, the premium packaging market is projected to reach US$9.6 billion, driven by continued premiumization and higher value-per-unit packaging.

Key trends include premiumization in cosmetics, beverages, and luxury goods, rising demand for distinctive unboxing experiences, growing adoption of recyclable and sustainable premium materials, increased use of digital printing and short-run customization, and the integration of smart and anti-counterfeit packaging features.

By material, paper and paperboard lead the market, accounting for approximately 53.2% of total demand, supported by strong sustainability credentials and superior print and finishing capabilities.

The premium packaging market is expected to grow at a CAGR of 4.8% between 2026 and 2033.

Major players include Amcor plc, Smurfit Kappa Group, Crown Holdings, Inc., Ardagh Group S.A., and Owens-Illinois (O-I Glass).