- Beverages

- Premium Alcoholic Beverage Market

Premium Alcoholic Beverage Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Premium Alcoholic Beverage Market Size, Share, Trends by Product Type (Spirits, Beer, Wine, and Others), by Distribution Channel (HoReCa, Hypermarkets/Supermarkets, Liquor Stores, Duty-Free Shops, Online Retail, and Others), and Regional Analysis, 2026 - 2033

Premium Alcoholic Beverage Market Share and Trends Analysis

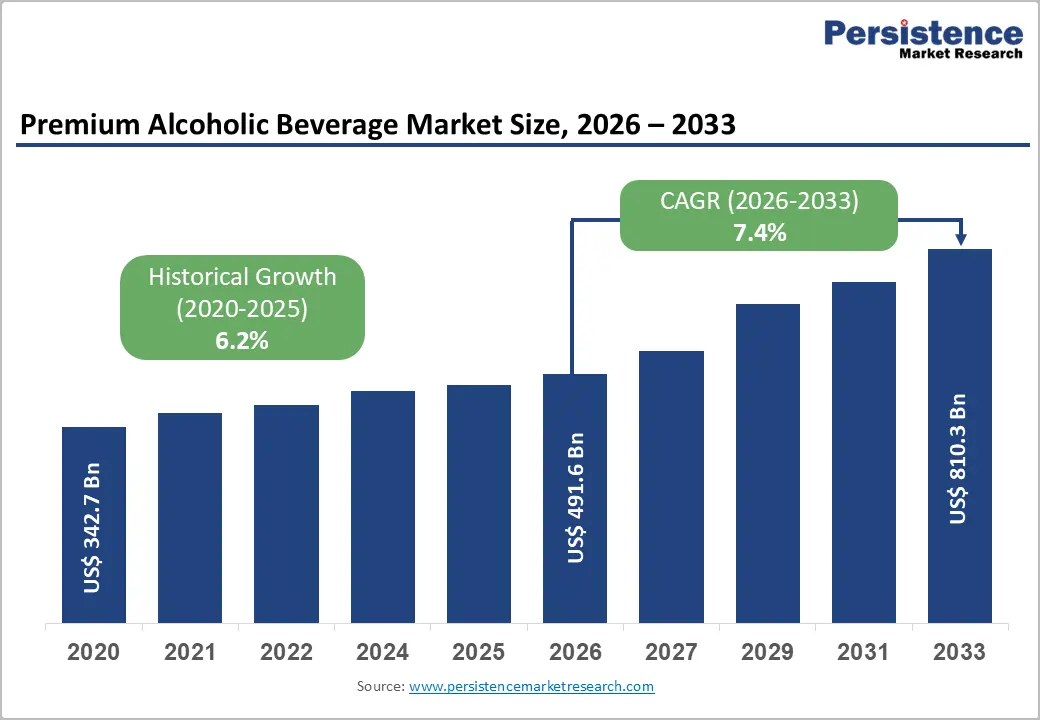

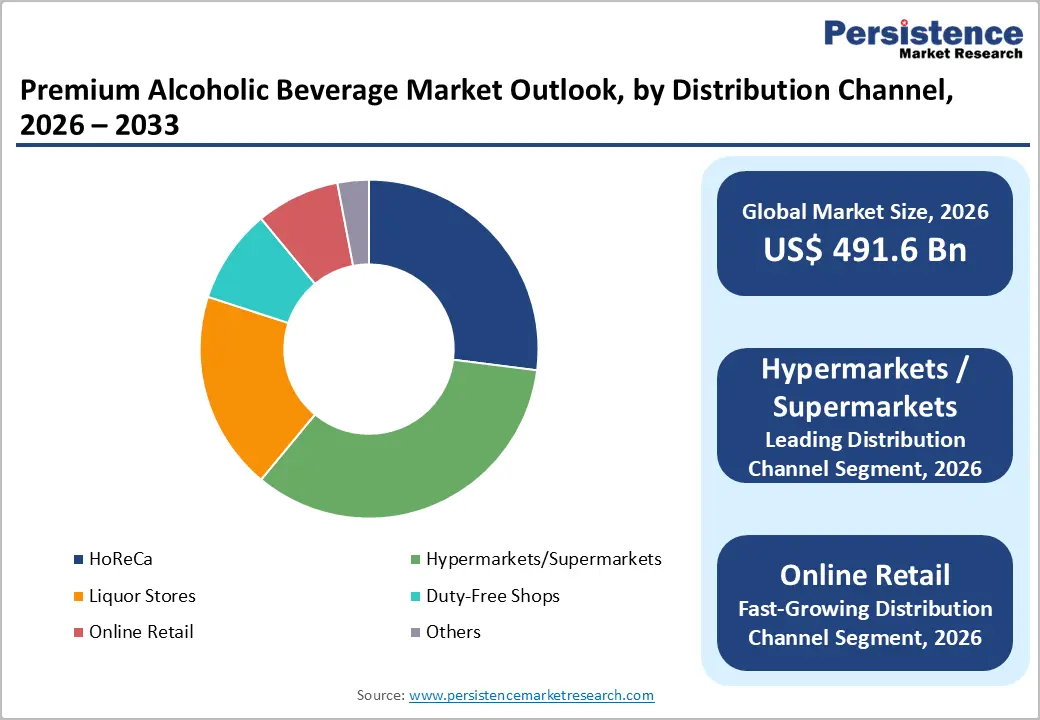

The global premium alcoholic beverage market size is expected to be valued at US$ 491.6 billion in 2026 and projected to reach US$ 810.3 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033.

The market is predominantly driven by the global premiumization trend, where consumers are shifting from volume-based consumption to value-based experiences, opting for less but better drinking habits. Rising disposable incomes in emerging economies, coupled with an increasing preference for artisanal and craft-based production methods, have solidified the market's trajectory. Furthermore, the expansion of the Online Retail sector and the integration of Direct-to-Consumer (DTC) models have significantly lowered barriers for high-end spirits and limited-edition wines to reach a global audience, fueling a robust CAGR of 7.4% over the forecast period.

Key Highlights:

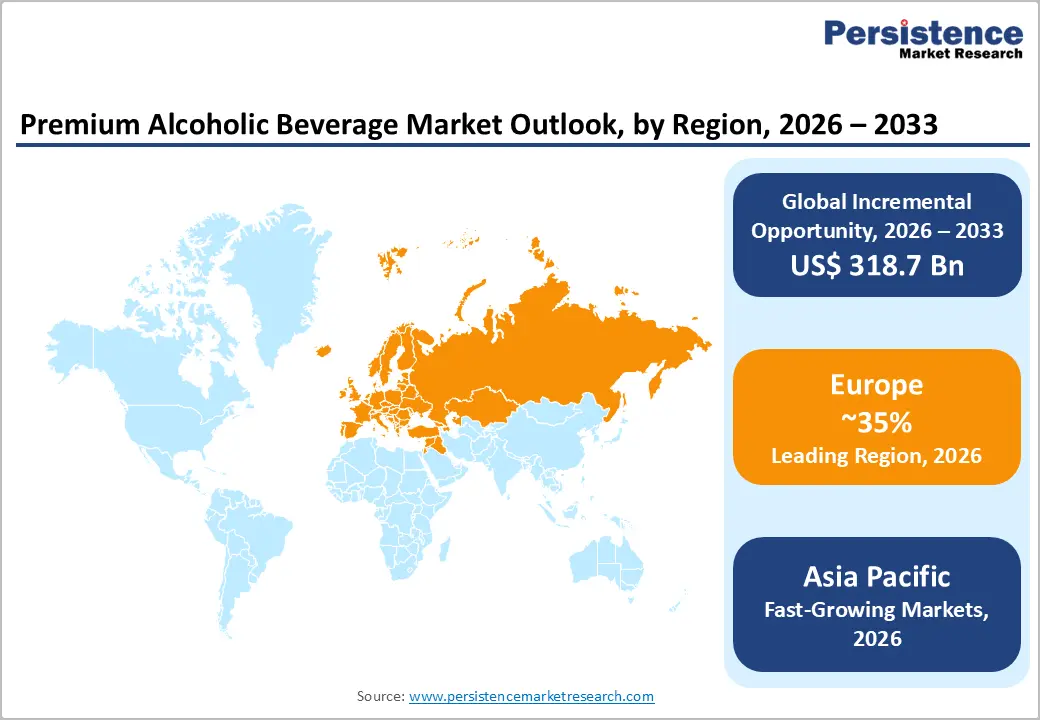

- Leading Region: Europe accounted for a 35% market share in 2025, supported by a rich heritage of wine and spirits production and a robust HoReCa sector in countries such as France and Italy.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, driven by the expanding middle class in China and India and the adoption of premium Western-style drinking cultures

- Dominant Segment: Hypermarkets/Supermarkets held the largest distribution share at 34% in 2025, providing the scale and physical infrastructure required for mass premium brand visibility.

- Fastest Growing Segment: Online Retail is the fastest-growing distribution channel, as digital platforms and DTC models offer consumers unprecedented access to rare and niche premium beverages.

- Key Market Opportunity: The premium Ready-to-Drink (RTD) category represents a significant opportunity, combining the high-quality status of premium spirits with the convenience required by modern lifestyles.

| Key Insights | Details |

|---|---|

| Premium Alcoholic Beverage Market Size (2026E) | US$ 491.6 Bn |

| Market Value Forecast (2033F) | US$ 810.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Dynamics

Driver - Rising Disposable Income and the Drink Less, Drink Better Movement

Premium alcohol growth is reshaped by fuller wallets and leaner habits. As disposable incomes rise across urban and affluent consumer segments, alcohol purchasing decisions increasingly favor quality, provenance, and craftsmanship over volume. The "drink less, drink better" mindset reflects a deliberate shift toward fewer occasions, paired with higher-priced spirits, wines, and craft beers that signal taste and discernment. Consumers are allocating discretionary spend toward aged whiskies, small-batch gins, and limited-release wines, viewing alcohol as an experiential indulgence rather than a routine staple.

In the U.S., premium tequila and American whiskey exemplify this driver. Brands such as Clase Azul and high-end Kentucky bourbons have expanded despite slowing overall alcohol volumes, supported by higher-income consumers trading up within familiar categories. This behavior rewards brands that emphasize authenticity, aging credentials, and scarcity, reinforcing premium alcohol as a lifestyle choice aligned with financial confidence and mindful consumption patterns worldwide today.

Restraints - Stringent Regulatory Frameworks and Excise Duties

The global alcoholic beverage industry operates under a highly complex regulatory landscape that can significantly hinder market growth. Many governments employ high excise taxes and strict licensing requirements to curb consumption and boost public health. For instance, in countries such as India, import tariffs on luxury spirits can range from 100% to 150%, making premium products prohibitively expensive for a large share of the population. Additionally, tightening restrictions on alcohol advertising and marketing in the European Union and parts of Southeast Asia limit brands' ability to engage new consumers. These legal barriers often increase operational costs and complicate the distribution strategies of multinational corporations like LVMH Moët Hennessy.

Opportunity - E-commerce Expansion and Digital-First Consumer Engagement

The digital transformation of the alcohol retail landscape presents a massive growth opportunity for premium brands. The Online Retail channel is projected to be the fastest-growing distribution segment, as consumers seek the convenience of home delivery and access to a wider variety of niche products that are not available in local stores. Platforms like Drizly and brand-owned DTC websites allow companies to collect first-party data, personalize marketing efforts, and offer exclusive online-only releases. By leveraging social media influencers and virtual tasting events, brands can build deep loyalty with younger consumers, driving high-value transactions that bypass the traditional retail margins. This digital ecosystem is essential for scaling in vast, geographically diverse markets like North America and China.

Category-wise Analysis

Product Type Insights

Spirits hold approx. 47% market share as of 2025, reflecting their unrivalled position within premium alcohol consumption. Premium spirits benefit from aging potential, higher price elasticity, and strong gifting appeal, thereby allowing brands to command significant per-unit margins. Categories such as single malt whisky, premium vodka, tequila, and dark rum align closely with the "drink less, drink better" mindset, in which consumers prioritise flavour complexity, heritage, and brand storytelling. Spirits also perform well across on-trade and off-trade channels, supported by cocktail culture, mixology trends, and limited-edition releases that encourage trading up rather than trading down.

Wine retains relevance through premium appellations and sustainability cues, while high-end beer relies on craft credentials and seasonal experimentation. However, both face volume constraints relative to spirits, which scale globally with consistent formats, longer shelf life, and stronger luxury positioning across mature and emerging markets, as producers seek to maintain market share.

Distribution Channel Insights

The hypermarkets/supermarkets segment remained the leading distribution channel in 2025, accounting for approximately 34% of the market share. These retailers provide high visibility and one-stop convenience, often featuring dedicated premium aisles for luxury wines and spirits. However, Online Retail is the fastest-growing segment through 2032. This growth is driven by the rapid adoption of smartphone apps and the liberalization of home-delivery regulations across jurisdictions. The ability to browse detailed product descriptions, reviews, and limited-drop exclusives makes the digital channel highly attractive to the premium segment, enabling artisanal brands to compete on a global scale without a substantial physical retail presence.

Regional Insights

North America Premium Alcoholic Beverage Market Trends and Insights

Premium alcohol in North America is increasingly shaped by moderation, premiumization, and experiential value. In the United States, consumers are gravitating toward aged spirits, additive-free tequila, and small-batch bourbon, with storytelling and provenance influencing purchasing decisions. Cocktail culture continues to drive demand for premium vodka and gin, while limited releases and collaborations create urgency and higher price acceptance in urban markets.

Canada mirrors this shift with strong demand for premium whisky, craft gin, and low-sugar ready-to-serve formats, reflecting health awareness and regulatory discipline. Across both countries, premium brands benefit from omnichannel retail, travel retail recovery, and consumers willing to pay more for quality, authenticity, and responsibly produced alcohol during fewer, more intentional occasions. This dynamic supports steady value growth despite flat overall consumption volumes regionwide, particularly among affluent urban professionals and older millennials seeking consistently elevated everyday indulgence from trusted brands.

Europe Premium Alcoholic Beverage Market Trends and Insights

Europe holds approximately. 35% market share in the European premium alcoholic beverage market, underpinned by deep cultural ties to spirits, wine, and craft production. The region benefits from strong domestic consumption alongside export-driven prestige, with premium categories anchored in heritage, protected origins, and artisanal credibility. Consumers increasingly favour fewer drinking occasions paired with higher quality, supporting premium pricing across established alcohol traditions.

In the UK, premium gin and single malt whisky continue to evolve through innovation and limited editions. France reinforces its luxury image with cognac and high-end champagne, while Germany shows rising interest in premium schnapps and craft spirits. Spain and Italy combine premium aperitifs, vermouth, and heritage wines with modern branding, attracting younger consumers seeking authenticity with contemporary flair. This balance of tradition and reinvention sustains premium value growth across Europe, despite regulatory complexity and mature consumption patterns in core markets today.

Asia Pacific Premium Alcoholic Beverage Market Trends and Insights

Asia Pacific region is expected to achieve a CAGR of 9.7%, driven by rapid premiumization and expanding middle-class wealth. Consumers across the region increasingly associate premium alcohol with status, social occasions, and gifting, encouraging trade-up from mass brands. Urbanization, Western-style cocktail culture, and digital discovery channels further accelerate premium adoption across spirits and selected wine categories.

India is seeing strong momentum in premium whisky and gin, while China’s premium spirits growth is driven by gifting culture and localised luxury branding. Japan continues to value craftsmanship through premium whisky and sake innovation, and South Korea shows rising demand for premium imports aligned with lifestyle trends. Collectively, Asia Pacific rewards brands that balance heritage cues with modern design, flavour experimentation, and aspirational positioning. This creates long-term headroom for premium category expansion across urban and emerging consumption hubs through 2030.

Competitive Landscape

The global premium alcoholic beverage market is moderately consolidated, led by multinational spirits, beer, and wine groups alongside influential niche players. Leading companies focus on portfolio premiumization through aged expressions, limited editions, and strong brand narratives. Designer bottle packaging has become a strategic tool, using distinctive shapes, sustainable glass, and tactile finishes to signal luxury at the shelf and bar level. Celebrity-backed brands add cultural relevance, accelerate awareness, and attract younger, style-driven consumers across key markets.

Flavor innovation supports differentiation, with botanicals, barrel finishes, and regional profiles refreshing mature categories. International expansion targets the Asia Pacific and travel retail, supported by distribution networks and local partnerships. Collaborations with chefs, artists, and fashion houses elevate brand storytelling. Regulatory complexity shapes pricing and marketing discipline, while select players cautiously test D2C platforms where permitted, leveraging digital engagement to strengthen global loyalty.

Key Developments:

- In January 2026, ABSOLUT and TABASCO® Brand expanded the flavored spirits landscape with the global launch of ABSOLUT® TABASCO™, a spicy vodka blending premium vodka with TABASCO’s iconic heat.

- In January 2026, Radico Khaitan Limited announced that Rampur Indian Single Malt Whisky secured the No. 4 position in the World’s Top Trending Whiskies for 2026, reinforcing India’s growing credibility in the premium and super-premium whisky segment.

- In November 2025, Barrell Craft Spirits released its latest New Year bourbon, a multi-state, multi-mashbill blend assembled specifically for its annual celebration bottling.

- In October 2025, Samuel Adams released Utopias 2025, its iconic ultra-premium beer, once again hitting a historic 30% ABV.

Companies Covered in Premium Alcoholic Beverage Market

- Diageo plc

- Pernod Ricard S.A.

- LVMH Moët Hennessy

- Anheuser-Busch InBev

- Heineken N.V.

- Constellation Brands

- Brown-Forman Corporation

- Asahi Group Holdings

- Campari Group

- Rémy Cointreau

- Beam Suntory

- The Edrington Group

- Others

Frequently Asked Questions

The global Premium Alcoholic Beverage market is projected to be valued at US$ 491.6 Bn in 2026.

Rising Disposable Income and the Drink Less, Drink Better Movement is driving demand for Premium Alcoholic Beverage market.

The Global Premium Alcoholic Beverage market is poised to witness a CAGR of 7.4% between 2026 and 2033.

E-commerce Expansion and Digital-First Consumer Engagement is key opportunity for key players in the market.

Leading companies include Diageo plc, Pernod Ricard S.A., LVMH Moët Hennessy, Anheuser-Busch InBev, Heineken N.V., Constellation Brands, and Others.