- Processed Food

- Pickle Market

Pickle Market Size, Share, and Growth Forecast, 2025 - 2032

Pickle Market By Product Type (Cucumber Pickles, Mixed-Vegetable Pickles), Packaging (Glass Jars, PET Bottles), Distribution Channel, and Regional Analysis for 2025 - 2032

Pickle Market Size and Trends Analysis

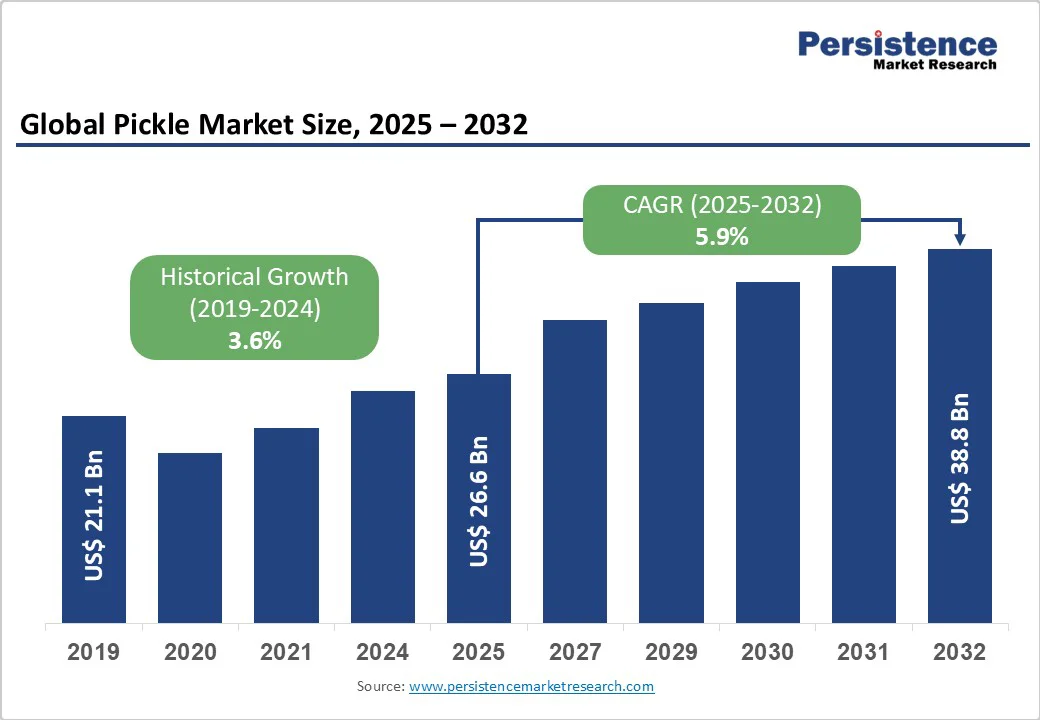

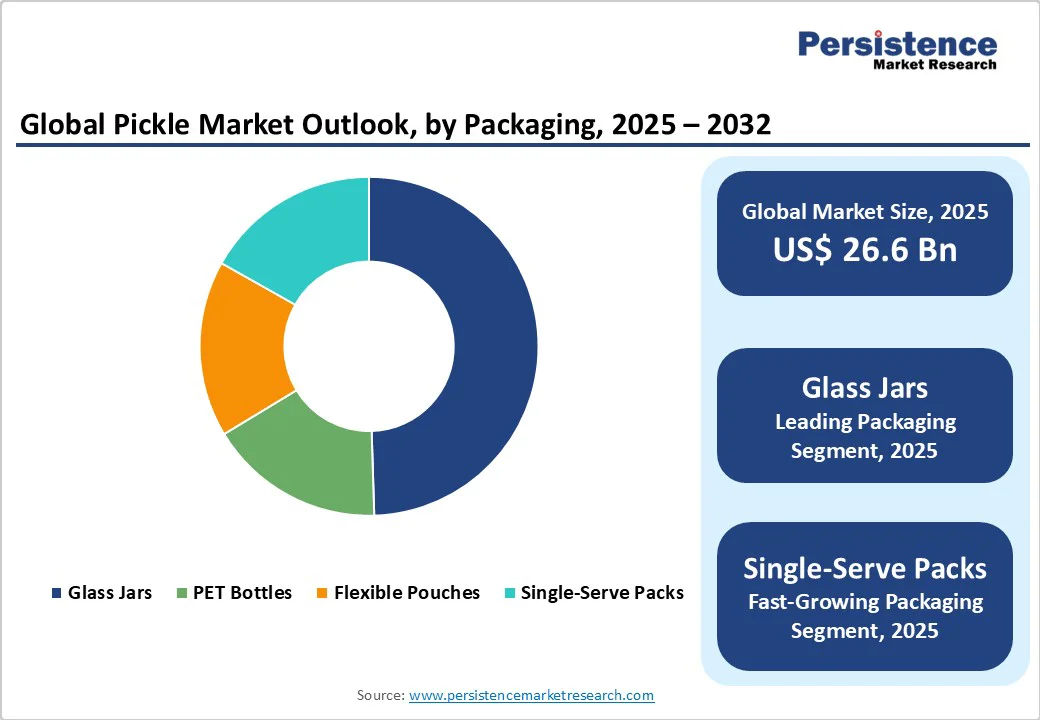

The global pickle market size was valued at US$26.6 Bn in 2025 and is projected to reach US$38.8 Bn by 2032, growing at a CAGR of 5.9% between 2025 and 2032, driven by the rising consumer interest in fermented and probiotic foods, increasing demand for ready-to-eat convenience products, and product innovation, including premium and ethnic flavors.

The expansion of retail and e-commerce distribution channels, combined with investments in automation and quality assurance technologies, is enhancing operational efficiency and margin potential.

Key Industry Highlights

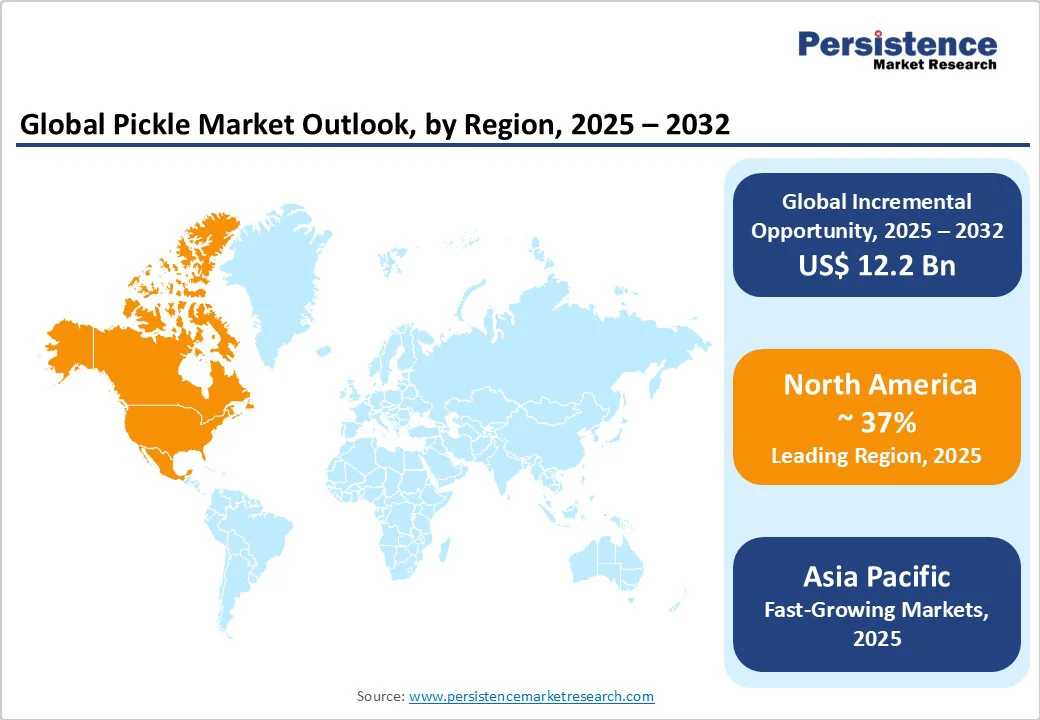

- Leading Region: North America leads the market, accounting for 37% of global packaged pickle revenues, driven by U.S. consumption, private-label growth, and QSR demand.

- Fastest-growing Region: Asia Pacific is the fastest-growing market, projected to grow at 5% CAGR, driven by urbanization, convenience-led demand, and export opportunities.

- Investment Plans: Key investments focus on automation, cold-chain logistics, and sustainable packaging, with notable moves including the launch of low-sodium products in the U.S., organic lines in Europe, and export-driven expansions in India.

- Dominant Product Type: Vegetable pickles hold the largest share, accounting for 48% of global revenues, supported by their versatility in both household meals and foodservice.

- Leading Packaging Type: Glass jars remain the most widely adopted packaging type, accounting for nearly 50% of the market share.

| Key Insights | Details |

|---|---|

| Market Size (2025E) | US$26.6 Bn |

| Market Value Forecast (2032F) | US$38.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Health and Functional Positioning

Consumers increasingly view pickles as functional foods, particularly fermented varieties that promote gut health. The rising popularity of probiotic and clean-label pickles has led to higher consumer engagement and willingness to pay a premium. Industry data indicate that fermented and probiotic pickle launches are expanding at a CAGR of 5-6%, contributing to overall category growth. Retailers have expanded shelf space for health-focused products, reflecting increased demand for functional food options.

Innovation in Formats and Flavors

Brands are extending pickles into snacks, including pickle-flavored chips, popcorn seasonings, and frozen fried pickles, capturing new consumption occasions. Flavor innovation, including ethnic and fusion offerings, has enhanced category relevance for younger consumers. These product extensions contribute to increasing per-unit revenue and higher-margin, private-label opportunities. The market has seen measurable incremental sales from such innovations in both retail and e-commerce channels.

Supply-Chain Automation and Scale Economies

Automation and AI technologies are being applied in cucumber sorting, quality assessment, and supply-chain optimization. These measures reduce waste, enhance throughput, and improve product consistency. Companies report double-digit efficiency gains in pilot facilities, shortening time-to-shelf and lowering unit costs. Extended shelf life and enhanced packaging technologies also facilitate broader distribution to retail and e-commerce outlets.

Barrier Analysis - Raw-Material Volatility

Pickle production is highly dependent on seasonal vegetable harvests, particularly cucumbers. Adverse weather or supply shortages can lead to price spikes and constrain volume availability. A 5-10% shortfall in key production regions can significantly increase procurement costs, compress margins, and force temporary SKU rationalization.

Regulatory Pressure on Sodium and Preservatives

The high sodium content in pickles has attracted regulatory scrutiny, with initiatives from the FDA, WHO, and the EU focusing on reducing sodium consumption. Compliance requires reformulation, which can increase costs and impact product taste and texture. Reformulation programs may raise production costs by 3% while necessitating sensory testing to maintain consumer acceptance.

Opportunity Analysis - Premium and Artisanal Fermented Lines

Premium and artisanal pickles, including small-batch and cold-brine fermented varieties, are commanding 40% higher price points than mainstream products. Growth in premium segments could increase global revenues by several hundred million dollars if market penetration expands from 10% to 17% by 2032. Scaling artisanal quality at industrial cost offers a path to higher margins.

Emerging-Market Commercialization

Traditional pickling markets in India, China, Southeast Asia, and Latin America are transitioning to packaged commercial formats. An 8% point increase in packaged penetration could significantly expand global unit volumes. Region-specific flavor launches and localized supply chains are key enablers for capturing this growth opportunity.

Category-wise Analysis

Product Type Insights

Vegetable pickles, led by cucumber and mixed-vegetable varieties, hold the largest market share, accounting for 48% of the total global revenues. Their dominance is driven by universal consumer familiarity, easy availability of raw materials, and year-round consumption.

Cucumber pickles, for example, are widely integrated into fast-food and quick-service restaurant (QSR) menus, particularly in the U.S. and European nations, where burger and sandwich chains such as McDonald’s and Subway heavily rely on them.

In the Asia Pacific, mixed-vegetable pickles are an integral part of traditional diets, with India and China leading both production and consumption volumes. The combination of affordability, long shelf life, and culinary adaptability ensures vegetable pickles remain the backbone of the pickle market.

Fruit pickles, such as mango and lemon, along with ethnic fermented varieties like Korean kimchi and Japanese tsukemono, are registering CAGRs of 5% between 2025 and 2032. Demand is particularly strong among health-conscious consumers due to their probiotic benefits, natural fermentation, and association with digestive wellness.

For instance, the popularity of kimchi in Western markets has grown significantly, with exports from South Korea surpassing US$150 Mn in 2024, according to government trade data. Similarly, mango pickle exports from India have captured strong demand in diaspora communities across North America, the U.K., and the Middle East.

This segment is expected to expand further as consumers seek premium, authentic, and globally inspired food options, offering significant opportunities for brands to market traditional recipes in modern packaging formats.

Packaging Insights

Glass jars remain the most widely adopted packaging type, accounting for nearly 50% of global pickle revenue. Their appeal lies in product visibility, consumer trust in quality, and recyclability, aligning with sustainability goals in mature markets such as Europe and North America. Brands like Vlasic (U.S.) and Kühne (Germany) heavily rely on glass jars to reinforce their premium positioning.

Moreover, consumer perception links glass packaging with authenticity and freshness, driving repeat purchases in retail chains and specialty stores. Despite being heavier and more costly to transport, glass jars retain their dominance due to a strong brand association and regulatory preferences for recyclable materials in the EU and other developed regions.

Single-serve formats are projected to grow between 2025 and 2032. These formats are particularly favored in on-the-go consumption settings, QSRs, and online retail channels, where lower shipping costs and lighter weight offer logistical advantages.

For example, single-serve pickle packs have been adopted in the U.S. school and office snack markets. At the same time, Indian brands like Priya and Mother’s Recipe increasingly use single-serve packs to reach rural markets at competitive price points.

Convenience-driven demand in the Asia Pacific and rising e-commerce penetration worldwide are key accelerators, with packaging innovations such as resealable pouches and biodegradable materials expected to further boost this category.

Regional Insights

North America Pickle Market Trends -U.S. Market Dominance and Low-Sodium Innovation

North America is projected to account for 37% of global packaged pickle revenues, making it the largest regional market. The U.S. dominates, supported by high per-capita consumption, retail consolidation, and integration of pickles into QSR menus and everyday household meals.

Major brands such as Vlasic, Claussen (Kraft Heinz), and Mt. Olive lead in product availability and innovation. The region has seen an increase in the launch of low-sodium and organic pickles, aligning with the FDA's sodium-reduction targets. For example, in 2024, Mt. Olive introduced a line of reduced-sodium dill pickles to cater to health-conscious consumers.

From a structural perspective, North America’s market is a blend of large consumer packaged goods (CPG) companies and regional co-packers, the latter of which supply private-label brands to major retailers such as Walmart and Costco. Investments are channeling into automation, extended-shelf-life processing, and frozen pickle innovations. A notable 2023 development was Claussen’s launch of refrigerated pickle chips, designed for snacking and cross-category usage with charcuterie and dips.

The U.S. remains the regional leader, accounting for more than 85% of North American revenues. The growing consumer preference for functional foods has led to an expansion of fermented pickle varieties with a focus on probiotic positioning. Demand in the food service industry is also rising, with QSR chains offering pickles as premium add-ons or snack sides, creating incremental revenue opportunities.

Asia Pacific Pickle Market Trends - Urbanization-Driven Packaged Pickle Growth and Diaspora Exports

Asia Pacific is the fastest-growing region. Countries such as India, China, Japan, and ASEAN nations are transitioning from home-pickling traditions to packaged, branded formats, driven by urbanization, rising disposable incomes, and convenience-led lifestyles. Competitive manufacturing costs, combined with export opportunities, further strengthen the region’s outlook.

In 2024, Mother’s Recipe (India) expanded its distribution to the U.S. and the Middle East, signaling the role of diaspora markets in fueling exports. Similarly, Japanese pickle companies are capitalizing on the rising global demand for fermented varieties, such as tsukemono, which is supported by government-backed promotional campaigns. Investment trends highlight the importance of modern co-packing infrastructure, cold-chain logistics, and standardized certifications in improving quality and boosting exports.

Challenges persist, including fragmented rural distribution networks and the need for uniform food safety certifications to enter regulated markets, such as those in the U.S. and European countries. Nevertheless, increasing e-commerce penetration and the growing appeal of authentic, ethnic flavors provide strong upside potential. India represents the largest APAC market by volume, driven by the mass consumption of mango, lemon, and mixed-vegetable pickles.

Packaged brands such as Priya Foods and Mother’s Recipe are gaining ground, while SMEs and local producers dominate regional markets. Recent government initiatives, such as the PLI (Production Linked Incentive) scheme for food processing, are encouraging modern manufacturing and export competitiveness, particularly to North America, the U.K., and GCC countries.

Europe Pickle Market Trends - Gherkin Tradition, Organic Growth, and Sustainable Packaging

Europe demonstrates steady and mature demand, with Germany, the U.K., France, and Spain leading consumption volumes. Pickles, especially gherkin-based products and fermented varieties, are deeply embedded in traditional diets.

Germany has the highest per-capita consumption, with local producers such as Kühne driving innovation in both premium and mainstream categories. EU regulatory harmonization emphasizes clean-label standards, sodium reduction, and sustainable packaging, which have become critical for market competitiveness.

Growth is moderate at around 2-3% annually, but premium and artisanal products are gaining traction. For example, in 2024, Kühne expanded its organic pickle line across Germany and Austria, reflecting consumer interest in natural, additive-free foods. Online marketplaces, such as Ocado (U.K.), are also boosting the visibility of niche artisanal pickle producers, enabling cross-border scaling of specialty offerings.

Germany is the largest single European market for pickles, accounting for over 25% of regional revenues. Traditional gherkin consumption, coupled with rising demand for organic and locally sourced products, drives growth. Recent investments include regional cooperatives introducing recyclable glass jars to meet EU green-packaging directives, signaling the market’s focus on sustainability and authenticity.

Competitive Landscape

The global pickle market is moderately fragmented. Multinational CPG players hold significant branded shares in developed markets, while regional and artisanal producers dominate local niches. Market concentration is lower in Asia Pacific and Latin America, where SMEs account for a large portion of production. Competitive dynamics involve brand heritage, product innovation, and private-label collaborations.

Market leaders focus on product innovation, cost leadership through automation, and geographic expansion. Differentiation is achieved through brand heritage, supply chain control, and partnerships with retail and private-label channels. Emerging players emphasize artisanal, low-sodium, and functional pickles.

Key Industry Developments

- In March 2025, Grillo’s Pickles partnered with Hippeas to launch "Dill Pickle Puffs," a gluten-free, vegan snack combining chickpea flour and dill pickle seasoning.

- In April 2025, Popeyes introduced a limited-time pickle-themed menu, featuring pickle-glazed wings, sandwiches, fried pickles, and pickle lemonade.

- In June 2025, Hormel Foods launched "Dill Pickle Flavored Pepperoni," catering to consumer demand for pickle-infused snack products.

Companies Covered in Pickle Market

- Vlasic

- Claussen

- Mt. Olive Pickle Company

- Best Maid Products

- Heinz (The Kraft Heinz Company)

- B&G Foods (Mrs. Klein’s, Nalley)

- Pinnacle Foods

- Gedney Foods Company

- Van Holten’s Pickles

- Kruegermann Pickles

- Maille (Unilever)

- Kühne

- Gundelsheim Pickles

- Patak’s (Associated British Foods)

- Desai Brothers (Mother’s Recipe)

- Nilon’s Enterprises

- Priya Foods

- Gujarat Pickles

- Hengstenberg

- ADF Foods

Frequently Asked Questions

The pickle market size in 2025 is estimated at US$26.6 Bn.

By 2032, the pickle market is projected to reach US$38.8 Bn, driven by rising snack innovations and growing demand for low-sodium and clean-label variants.

Key trends include the adoption of low-sodium formulations, premium and artisanal pickle launches, sustainable packaging innovations, and the expansion of online retail distribution across emerging markets.

Cucumber pickles lead the market, accounting for the largest share, driven by demand in sandwiches, burgers, and quick-service restaurant offerings.

The pickle market is projected to expand at a CAGR of 5.9% between 2025 and 2032.

Major players include Vlasic, Mt. Olive Pickle Company, Claussen, Best Maid Products, and Gujarat Pickles.