- Electrical Equipment & Services

- Photovoltaic Mounting System Market

Photovoltaic Mounting System Market Size, Share, and Growth Forecast 2026 – 2033

Photovoltaic Mounting System Market by Product Type (Roof-Top and Ground Mounted), by End-use Industry (Residential, Commercial and Utility), by Type of Mounting (Fixed and Tracking) and Regional Analysis for 2026 - 2033

Photovoltaic Mounting System Market Overview 2026 to 2033

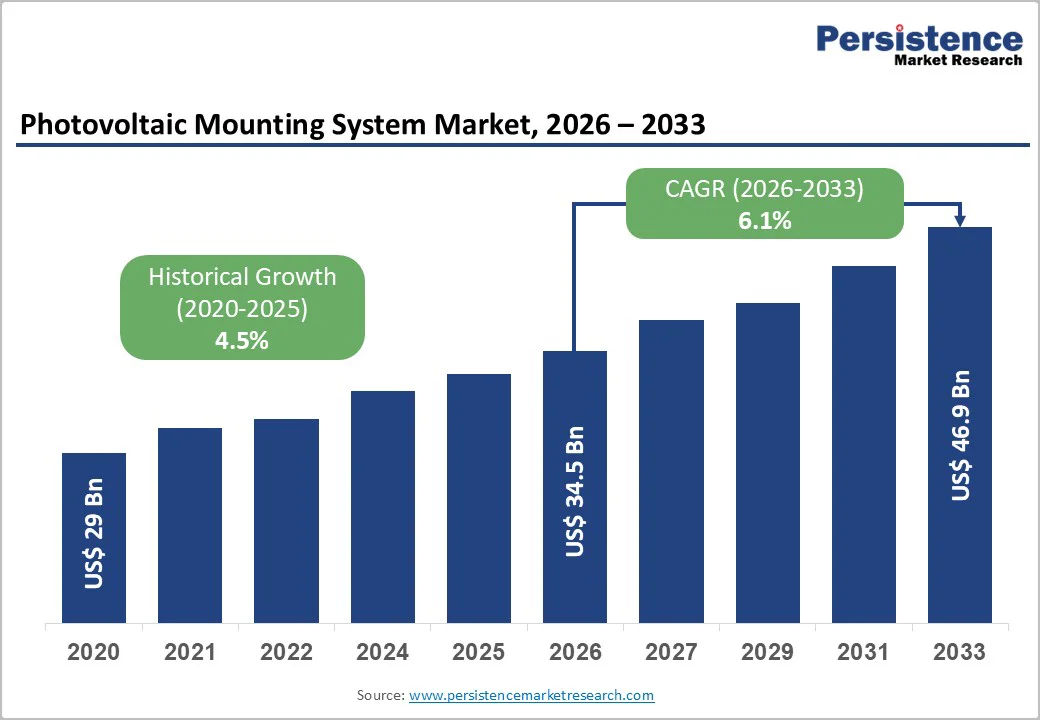

The global Photovoltaic Mounting System Market size was valued at US$ 34.5 Bn in 2026 and is projected to reach US$ 46.9 Bn by 2033, growing at a CAGR of 4.5% between 2026 and 2033. The photovoltaic mounting system market demonstrates sustained expansion driven by accelerating global renewable energy adoption, supported by regulatory mandates requiring solar deployment across residential, commercial, and utility-scale segments. The convergence of declining solar panel costs (approximately 70% reduction since 2010), expanded federal incentives including the U.S. Investment Tax Credit (ITC) of 30% through 2033, and ambitious European Union decarbonization targets via the Energy Performance of Buildings Directive (EPBD) mandate all new buildings achieve "solar-ready" status by 2026.

Key Market Highlights

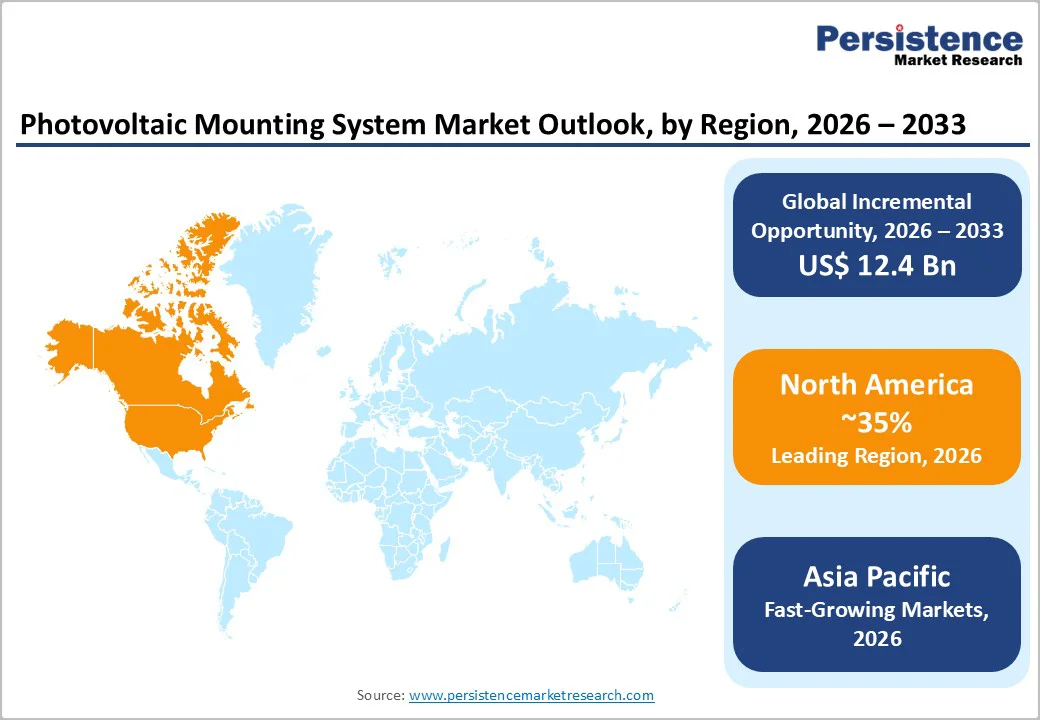

- North America Market Leadership: North America remains the dominant photovoltaic mounting system market, driven by U.S. commercial solar installations growing 108% in Q1 2026, a 30% federal investment tax credit through 2033, and the utility-scale sector's concentration comprising 92% of Q4 2024 installations.

- Asia-Pacific Fastest-Growth Region: Asia-Pacific is the fastest-growing region, with 39.6% of the solar module market share (2026), led by China's 60% global installation share and India's PM Surya Ghar program targeting 24 lakh residential installations by December 2026.

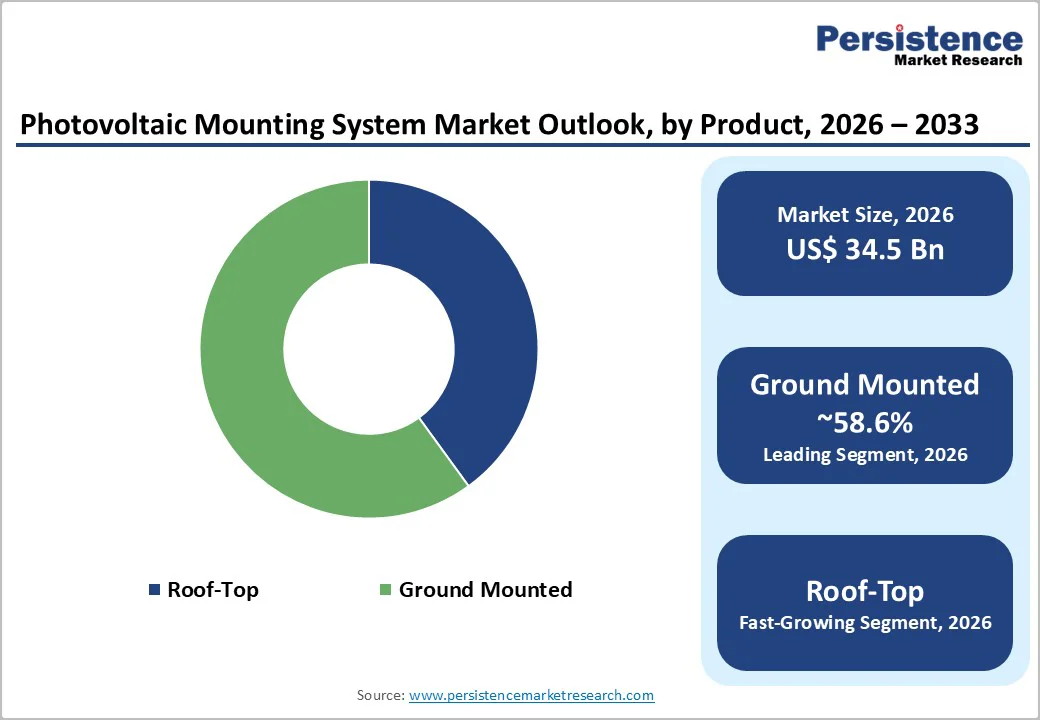

- Ground-Mounted Systems Dominant Segment: Ground-mounted photovoltaic mounting systems account for approximately 58% of the market, preferred for utility-scale farms and large commercial installations due to flexibility, ease of installation, and tracking system integration capabilities.

- Tracking Systems Fastest-Growing Technology: Single-axis solar trackers expanding at 20.3% CAGR through 2029, delivering 10-20% energy output improvement, with dual-axis systems achieving 30% efficiency gains over fixed installations, driving accelerating utility-scale adoption.

- Regulatory Mandate Market Opportunity: European Union Energy Performance of Buildings Directive mandating solar-ready buildings from 2026 creates structural demand expansion across residential, commercial, and utility segments, establishing multi-decade deployment requirements supporting sustained market growth.

| Key Insights | Details |

|---|---|

| Photovoltaic Mounting System Market Size (2026E) | US$ 34.5 Bn |

| Market Value Forecast (2033F) | US$ 46.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Market Growth Drivers

Accelerating Commercial and Utility-Scale Solar Installations with Supportive Policy Framework

Commercial and utility-scale solar installations are experiencing unprecedented acceleration, with U.S. commercial solar capacity expanding 108% year-over-year in Q1 2026 to reach 1.3 GWdc, positioning the sector for record-setting annual deployment exceeding 7.1 GWdc by year-end 2026. This expansion reflects multiple structural drivers: the Inflation Reduction Act (IRA) of 2022, establishing 30% federal investment tax credit (ITC) through 2033 for eligible installations, state-level incentives across California, Texas, and Florida, and corporate net-zero emissions commitments driving organizational solar investment. Utility-segment dominance intensified in 2024, with utility-scale photovoltaic installations representing 92% of Q4 2024 U.S. solar capacity additions—the highest percentage recorded.

This sector concentration creates substantial demand for ground-mounted tracking and fixed mounting systems engineered for large-scale applications. Asia-Pacific solar photovoltaic market added approximately 430 GW in 2024, led predominantly by China's manufacturing dominance and sustained infrastructure investment. The photovoltaic mounting system market benefits from increased replacement and upgrade cycles as existing installations transition to advanced mounting architectures that offer superior durability and performance optimization.

Regulatory Mandates and Decarbonization Targets Stimulating Residential and Commercial Rooftop Adoption

European Union's Energy Performance of Buildings Directive (EPBD) represents a transformative regulatory catalyst, mandating all new buildings achieve "solar-ready" status from 2026, with phased mandatory solar installations for public, commercial, and residential building categories through 2030. Germany's Solarpaket 1 legislative package further accelerates adoption by simplifying grid connection procedures, raising inverter limits for balcony-mounted systems to 800W, and streamlining permitting for distributed residential installations. India's government initiative, the PM Surya Ghar program, is projected to support solar panel installation for approximately 24 lakh (2.4 million) residential homes by December 2026, creating substantial demand for rooftop mounting systems engineered for residential applications. The U.S. residential solar market, despite a 32% decline in installations in 2024 due to policy uncertainty regarding interconnection limits, continues to advance through state-level incentives and renewable portfolio standards. These regulatory frameworks establish mandatory demand floors, supporting baseline growth trajectories and creating predictable investment signals for mounting system manufacturers planning capacity expansion.

Market Restraints

High Capital Expenditure Requirements and Financing Barriers Restricting Adoption Among Cost-Sensitive Market Segments

Despite compelling operational value propositions, mechanical and structural mounting system solutions present substantial upfront capital investment barriers constraining adoption among small-to-medium enterprises and price-sensitive emerging market segments. Commercial solar installations typically require multi-year financial commitment with complex financing structures including Power Purchase Agreements (PPAs) and solar leasing arrangements, with many small-to-medium businesses requiring expert guidance in navigating available options. Installation labor requirements demand specialized technical expertise, creating regional availability constraints in developing economies lacking established solar installation infrastructure. Urban spatial constraints in densely populated centers limit the availability of footprint for conventional ground-mounted and rooftop installations, thereby limiting addressable market expansion in metropolitan regions where land scarcity elevates per-kilowatt system costs.

Grid Connection Complexity and Supply Chain Vulnerabilities Creating Project Development Delays and Cost Uncertainty

Grid interconnection procedures remain highly variable across jurisdictions, resulting in permit processing delays of 4-12 weeks in many regions and uncertainty regarding project development timelines and capital deployment schedules. Germany's regulatory environment, while progressive, features increasingly complex approval processes for large-scale installations, with some federal states requiring stricter architectural coordination and visual-impact assessments. Supply chain constraints affecting specialized mounting system materials, including corrosion-resistant alloys and composite frameworks, create intermittent procurement delays and cost volatility. Logistics network disruptions and port congestion continue elevating delivered costs for manufacturing equipment and component shipments, particularly impacting emerging market manufacturers lacking established supply chain relationships with material suppliers.

Market Opportunities

Advanced Solar Tracking Technology Integration: Delivering Substantial Energy Yield Enhancement with Accelerating Market Penetration

Solar tracking systems represent the most dynamic growth segment, with single-axis tracker market expanding at 20.3% CAGR from 2026-2029, substantially outpacing fixed system growth trajectories. Single-axis solar trackers deliver 10-20% energy output improvement over fixed installations, while dual-axis systems achieve 30-40% efficiency gains. Total payback periods are reduced by approximately 0.39 years for single-axis and 18 months for dual-axis configurations compared to fixed-mount alternatives. Utility-scale solar projects increasingly integrate tracking systems to maximize energy yield across their designated project footprints, creating incremental demand for advanced east-west tracking mechanisms, backtracking algorithms that reduce row-to-row shading losses, and weather-resilience features that enable protective positioning during extreme wind or precipitation events. Emerging tracking system innovations incorporating fuzzy logic control (FLC) algorithms and artificial intelligence (AI) prediction capabilities achieve energy output increases up to 96% in variable cloud conditions, supported by hybrid tracking systems combining GPS data with light-dependent resistor (LDR) sensor integration delivering measured performance improvements of 33.2% versus fixed-tilt installations. Technological convergence, including Internet of Things (IoT) enablement, predictive maintenance algorithms, and autonomous condition-monitoring systems, creates opportunities for manufacturers to position advanced tracking solutions that address utility-scale deployment requirements.

Emerging Energy Transition Applications and Corporate Sustainability Commitments Driving Specialized Mounting Solution Development

Hydrogen infrastructure development, carbon capture utilization and storage (CCUS) facility deployment, and renewable energy integration initiatives create incremental demand for specialized photovoltaic mounting systems engineered for novel operating parameters and environmental conditions. Electric vehicle charging infrastructure expansion, particularly for commercial and fleet charging stations, increasingly integrates solar power generation and battery storage systems, requiring mounting architectures that support simultaneous renewable energy capture and vehicle charging. Corporate net-zero emissions targets, adopted by an estimated 10,000+ enterprises globally, establish organizational commitments driving solar investment across real estate portfolios, manufacturing facilities, and distribution centers. Community solar project expansion, particularly in New York, Maine, and Illinois, creates decentralized deployment opportunities for rooftop and ground-mounted systems serving multiple stakeholder organizations. Agrivoltaic system development, combining agricultural production with photovoltaic generation on shared land areas, requires specialized mounting configurations that maintain crop access and meet cultivation requirements, creating niche market opportunities for manufacturers offering agriculture-compatible mounting solutions.

Category-wise Insights

Product Type Analysis

Ground-Mounted Systems: The ground-mounted photovoltaic mounting system segment maintains dominant positioning within the broader category framework, commanding approximately 58% of market share, driven by extensive deployment across utility-scale solar farms, large commercial installations, and fixed-tilt agricultural applications. Ground-mounted configurations offer compelling advantages for large-scale projects, including superior flexibility in optimizing array orientation, ease of installation across diverse terrain, the capacity to integrate tracking technology enabling solar panel repositioning throughout daylight hours, and simplified maintenance procedures that require minimal roof-related safety considerations. The segment's dominance reflects these operational advantages, with utility operators increasingly preferring ground-mounted architectures for expansion-phase installations where land availability exists. Single-axis tracking integration in ground-mounted systems enables incremental efficiency gains of 10-20%, while dual-axis configurations achieve 30-40% improvement over fixed installations. Ground-mounted systems' fastest-growing application domain is utility-scale solar farms targeting large-scale electricity generation for grid supply, with the Asia-Pacific region, particularly China, demonstrating accelerating capacity additions, reflected in 430 GW net additions in 2024. The segment sustains consistent demand through replacement and optimization cycles as aging fixed systems transition to modern tracking architectures.

End-use Industry Analysis

Utility Sector: The utility-scale power generation sector holds a dominant market share in the end-use segment, reflecting universal sealing requirements across pumps, compressors, turbines, and other rotating equipment, which require reliable leak-prevention solutions. Utility-scale photovoltaic installations represent the fastest-growing sector in renewable energy, with 92% of Q4 2024 U.S. solar capacity additions from utility-scale deployments, reflecting a structural preference for large-scale centralized generation over distributed residential alternatives. Utility installations are increasingly focused on tracking systems and advanced mounting architectures to optimize energy yield, with manufacturers including K2 Systems, Schletter, and UNIRAC developing specialized utility-scale solutions. India's power generation sector expansion, including grid-connected solar farms supporting the government's renewable portfolio standards, creates substantial demand for mounting systems engineered for large-capacity installations exceeding 100 MW. Power industry operators require mounting systems certified to UL 2703 standards, IEC specifications, and regional building codes, thereby establishing baseline technical requirements that constrain competition among manufacturers with robust engineering and certification capabilities. The segment's dominance reflects fundamental operational necessity paired with capital intensity, creating substantial dollar-denominated opportunities for mounting system suppliers.

Type of Mounting Analysis

Fixed-Mount Systems: Fixed photovoltaic mounting systems maintain a 60% market share in the mounting architecture segment, commanding dominant positioning through cost-effective implementation, simplified installation, minimal maintenance requirements, and proven long-term durability across diverse climate conditions. Fixed-mount photovoltaic systems use optimized tilt angles tailored to specific geographic locations, capturing solar radiation efficiently while eliminating rotating mechanical components that require regular maintenance and condition monitoring. The segment benefits from 25-year product warranties offered by manufacturers, including UNIRAC and K2 Systems, institutional customer confidence in system reliability, and standardized design procedures simplifying engineering documentation and permitting processes. Residential installations predominantly use fixed-roof-mounted systems for cost-effectiveness and compatibility with standard residential roof architectures, including asphalt shingles, tile, and standing-seam metal. Commercial rooftop installations similarly favor fixed-mount systems when building structural characteristics support mounting load requirements. The fastest-growing mounting segment comprises tracking systems, including single-axis and dual-axis configurations, which achieve energy output improvements of 10-40% compared with fixed installations. Tracking system expansion reflects declining equipment costs, improved control algorithms, and increasing emphasis on energy-yield optimization among utility-scale and commercial project developers.

Regional Insights

North America Photovoltaic Mounting System Trends

North America maintains dominant market positioning within photovoltaic mounting systems, driven by U.S. market leadership reflecting largest global solar capacity additions concentrated in Texas, California, and Florida, representing **43% of 2024 total U.S. solar installations. The U.S. commercial solar market achieved a remarkable 108% year-over-year growth in Q1 2026, with 7.1 GWdc of additional capacity projected by year-end 2026, establishing unprecedented deployment rates requiring substantial mounting system volumes. Federal investment tax credit (ITC) of 30% through 2033 established by the Inflation Reduction Act (2022) creates sustained financial incentive supporting commercial and utility-scale project development. Utility-scale installations, comprising 92% of Q4 2024 U.S. solar additions, drive specialized demand for ground-mounted fixed and tracking systems, with manufacturers including Quick Mount PV, UNIRAC, and RBI Solar developing utility-optimized solutions.

North America's regulatory framework emphasizes UL 2703 certification, IEC standard compliance, and regional building code adherence, establishing a technical baseline that constrains competition among manufacturers with robust engineering and testing capabilities. Single-axis tracking system adoption continues to accelerate, with a 20.3% CAGR projected through 2029, reflecting utility operators' recognition of cost-effective efficiency gains. State-level renewable portfolio standards and utility commission regulations increasingly mandate solar deployment, creating a supportive regulatory environment for sustained sector growth. Declining solar panel costs (approximately 70% reduction since 2010), combined with system integration advances enabling solar plus storage deployment, strengthen residential and commercial segment prospects despite the 2024 residential sector decline.

Europe Photovoltaic Mounting System Trends

European Union Energy Performance of Buildings Directive (EPBD) represents a transformative regulatory mandate requiring all new buildings achieve "solar-ready" status from 2026, with phased mandatory solar installation requirements for public, commercial, and residential building categories through 2030. This regulatory transformation creates structural demand expansion across residential rooftop systems, commercial installations, and utility-scale ground-mounted applications, establishing multi-decade deployment requirements. Germany, as Europe's largest commercial/industrial photovoltaic market, implements Solarpaket 1, a legislative package that simplifies grid connection procedures, raises balcony-mounted inverter limits to 800W, and streamlines distributed residential installation permitting. Germany's manufacturing sector leadership in mounting system production, represented by manufacturers including Schletter and Mounting Systems GmbH, supports competitive cost structures and regional supply chain resilience. However, Germany's declining feed-in tariff scheme and quarterly subsidy reduction mechanisms necessitate operator focus on energy yield optimization through tracking system integration, supporting single-axis tracker market expansion.

The UK's decarbonization target, achieving net-zero emissions by 2050, drives substantial rooftop and ground-mounted installation expansion, with 7.5% CAGR projected through 2035, supported by grid modernization initiatives and renewable energy infrastructure investment. France's consistent policy framework and moderate incentive structures support predictable market development, while Spain's renewable energy expansion, supported by European Green Deal financing, accelerates solar deployment. The European Sealing Association (ESA) and harmonized technical standards facilitate standardized mounting system design across member states, thereby supporting manufacturers' economies of scale.

Asia Pacific Photovoltaic Mounting System Trends

Asia-Pacific emerges as the fastest-growing photovoltaic mounting system region, accounting for approximately 39.6% of the solar photovoltaic module market share by 2026, driven by China's dominant position, capturing approximately 60% of global solar installations, supported by PowerChina's December 2026 announcement of 31 GW solar module purchase, signaling sustained capacity investment. Chinese manufacturing leadership in mounting system production supports competitive cost positioning and export market dominance, with domestically-focused manufacturers LEAPTON ENERGY and regional producers capturing substantial market share. India's government initiative, the PM Surya Ghar program, is projected to support 24 lakh (2.4 million) residential rooftop installations by December 2026, creating substantial demand for residential-scale mounting systems. India's energy infrastructure expansion, including Tata Power's December 2024 announcement of 4.3 GW manufacturing facility in Tamil Nadu, demonstrates commitment to domestic solar capacity development supporting regional supply chain integration.

Japan's photovoltaic market recovery following Feed-in Tariff (FIT) system adjustments demonstrates a renewed emphasis on efficiency innovation and advanced technologies, with Panasonic's December 2026 launch of HIT heterojunction solar panels that incorporate improved architectural aesthetics, supporting urban rooftop adoption.

ASEAN region expansion, including Vietnam, Thailand, Indonesia, and Singapore, accelerates through manufacturing relocation from developed economies and rising electricity demand, supporting utility-scale and commercial-scale deployment. India's renewable portfolio standards and government tax incentives establish a supportive regulatory framework, driving mounting system adoption across residential, commercial, and utility segments.

Competitive Landscape

The photovoltaic mounting system market demonstrates moderate-to-high competitive fragmentation with specialized regional manufacturers complementing global players, including UNIRAC, K2 Systems, Schletter, and Quick Mount PV, commanding established market positions through product differentiation, geographic specialization, and technical service integration. UNIRAC maintains North American market leadership, leveraging 25-year limited product warranties, ISO certifications (9001:2008, 14001:2004, OHSAS 18001:2007), and advanced product lines, including NXT UMOUNT rail-based systems and SFM INFINITY rail-less pitched roof configurations. K2 Systems, established in 2004, operates as a global player, emphasizing modular photovoltaic racking systems featuring shared-rail configurations that reduce material usage and installation complexity, with products supporting 12-20-year warranty coverage and customizable solutions for unique roof conditions.

Schletter Group demonstrates competitive positioning through durability engineering, multi-application mounting architectures (pitched roof, flat roof, façade, fixed-tilt, tracking, agrivoltaic), and a global manufacturing footprint supporting regional supply chain optimization. Competitive differentiation increasingly emphasizes tracking system integration, advanced materials that reduce structural load, and digital design tools that streamline engineering workflows. Asia-Pacific market fragmentation persists, with regional manufacturers including Pennar Industries Limited and Nuevosol Energy competing through cost advantages and localized customer relationships supporting market access.

Key Market Developments

January 2026: U.S. Commercial Solar Market Surge — U.S. commercial solar installations reached 1.3 GWdc in Q1 2026, representing 108% year-over-year growth, establishing momentum toward 7.1 GWdc annual deployment, driving mounting system demand across commercial rooftop and utility-scale projects.

December 2026: PowerChina 31 GW Solar Procurement Announcement — PowerChina's announcement of a massive 31 GW solar photovoltaic module purchase demonstrates sustained Chinese infrastructure investment supporting Asia-Pacific manufacturing capacity expansion and mounting system demand acceleration.

December 2026: Panasonic HIT Solar Panel Launch in Japan — Panasonic's introduction of heterojunction technology solar panels with improved aesthetics and high-temperature performance signals continuing product innovation supporting residential rooftop adoption in space-constrained urban environments.

Top Companies in Photovoltaic Mounting System Market

UNIRAC Inc. (USA) — UNIRAC maintains leading market position through 25-year product warranty coverage, ISO certifications demonstrating quality excellence, and advanced product portfolios including NXT UMOUNT systems for residential and commercial applications and SFM INFINITY rail-less pitched roof architecture for flush-mount installations. The company leverages comprehensive technical support infrastructure, engineering documentation resources, and established distributor relationships supporting North American market dominance and international expansion initiatives.

K2 Systems (Germany) — K2 Systems operates as global leader established 2004, specializing in modular photovoltaic racking systems featuring standardized hardware reducing installation complexity and supporting multi-roof repeat commercial projects. The company offers 12-20 year warranty coverage, online design tools facilitating customer engineering workflows, and customization capabilities for unique roof configurations, positioning K2 as preferred partner for large-scale commercial and utility deployments.

Schletter Group (Germany) — Schletter demonstrates competitive market positioning through uncompromising quality control processes, 25+ year durability standards for harsh environmental conditions, and diverse mounting architectures including pitched roof, flat roof, façade, fixed-tilt, tracking, and agrivoltaic systems. The company's global manufacturing footprint and regional supply chain optimization support competitive cost positioning, while advanced material engineering (composite frames, corrosion-resistant alloys) enables system performance in challenging climates.

Companies Covered in Photovoltaic Mounting System Market

- Quick Mount PV

- UNIRAC Inc.

- Nuevosol Energy Pvt. Ltd.

- K2 Systems

- Pennar Industries Limited

- Schletter Canada Inc.

- Wind & Sun Ltd

- Mounting Systems GmbH

- RBI Solar Inc.

- Belmont Solar

- Others Key Players

Frequently Asked Questions

The global photovoltaic mounting system market is valued at approximately US$ 34.5 billion in 2026 and is projected to reach US$ 46.9 billion by 2033, expanding at a CAGR of 4.5% during the forecast period.

Demand drivers include U.S. federal investment tax credit (ITC) of 30% through 2033, European Union Energy Performance of Buildings Directive mandating solar-ready buildings from 2026, India's PM Surya Ghar program targeting 24 lakh residential installations, accelerating commercial solar installations with 108% growth in Q1 2026, and corporate net-zero emissions commitments driving organizational renewable energy investments.

Ground-mounted photovoltaic systems command approximately 58% market share, driven by extensive deployment across utility-scale solar farms and large commercial installations due to installation flexibility, integration capabilities with tracking technology, and superior energy optimization potential for large-scale applications.

North America maintains dominant market leadership position driven by U.S. commercial solar market expansion, utility-scale installation concentration representing 92% of Q4 2024 additions, federal tax incentives through 2033, and established manufacturer presence including UNIRAC, Quick Mount PV, and RBI Solar.

Tracking systems represent the most significant opportunity, with single-axis solar trackers expanding at 20.3% CAGR through 2029, delivering 10-20% energy output improvement, and dual-axis systems achieving 30-40% efficiency gains, driving accelerating utility-scale and commercial adoption supported by declining equipment costs and improved control algorithms.

Leading manufacturers include UNIRAC Inc., K2 Systems (Germany) specializing in modular systems, Schletter Group (Germany) and Quick Mount PV (USA).