- Advanced Materials

- Building Integrated Photovoltaics (BIPV) Glass Market

Building Integrated Photovoltaics (BIPV) Glass Market Size, Share, and Growth Forecast for 2026-2033

Building Integrated Photovoltaics (BIPV) Glass Market by Product Type (Crystalline Silicon, Thin-Film, Hybrid, Semi-Transparent, Opaque, Transparent, Others), Application (Building Facades, Roofing Systems, Canopies, Greenhouses, Others), End-Use Sector (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Building Integrated Photovoltaics (BIPV) Glass Market Share and Trends Analysis

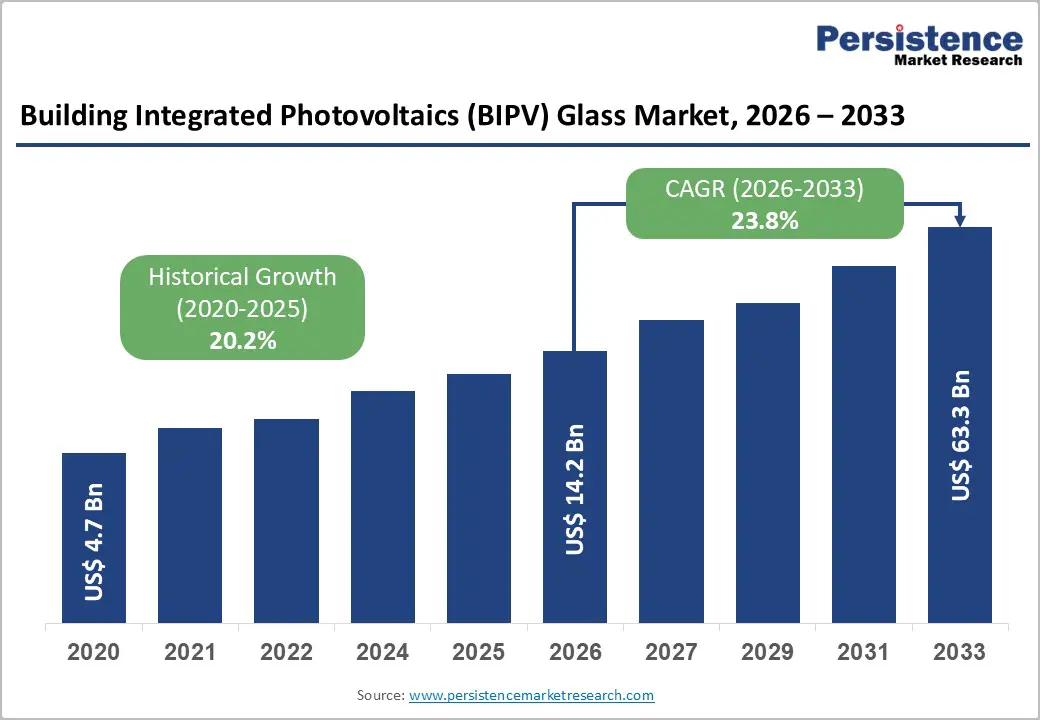

The global building-integrated photovoltaics (BIPV) glass market is likely to be valued at US$ 14.2 billion in 2026 and is projected to reach US$ 63.3 billion by 2033, growing at a CAGR of 23.8% during the forecast period 2026–2033. This strong expansion reflects the accelerating integration of renewable energy solutions into the built environment to meet net-zero targets.

The growth is driven by technological improvements in photovoltaic materials, increasing mandates for energy-efficient buildings, and expanding adoption of solar-integrated architectural elements. Urbanization and tightening building energy codes further underpin sustained investment in BIPV glass applications across residential, commercial, and infrastructure sectors.

Key Industry Highlights

- Dominant Product Type: Crystalline silicon BIPV glass is projected to hold about 42% revenue share in 2026, while thin film solutions are poised to register the highest 2026-2033 CAGR of nearly 28%, due to their high efficiency and architectural integration flexibility.

- Key Application: Building facades are anticipated to account for close to 38% revenue share in 2026, with greenhouses likely to grow the fastest through 2033, as they are known to maximize energy generation and multifunctional land use.

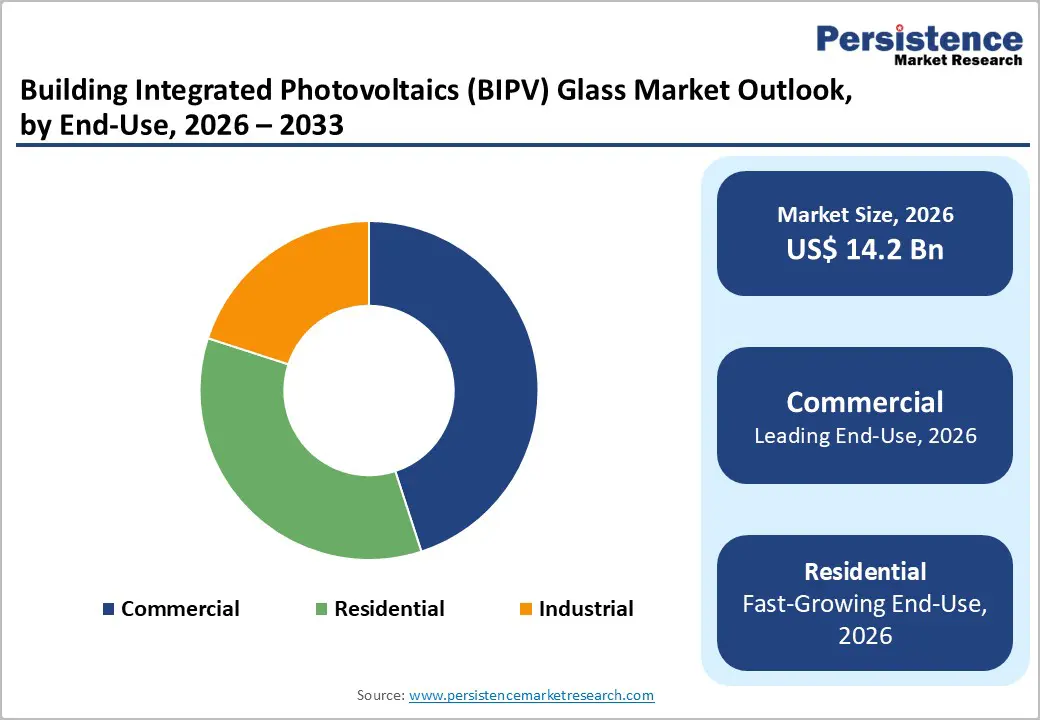

- Primary End-Use Sector: Commercial buildings are expected to capture approximately 45% of revenues in 2026, and residential applications are set to register a CAGR of about 26%, driven by rising net-zero home initiatives.

- Regional Leader: Europe is poised to hold 38% of global market share in 2026, whereas the Asia Pacific market is slated to grow the fastest at around 25.1% CAGR, supported by stringent energy codes, incentives, and rapid urbanization.

- Emerging Application: Agrivoltaics and greenhouse integrations are estimated to have a strong growth potential as they combine renewable energy generation with agriculture and infrastructure efficiency.

- April 2025: Trina Solar partnered with Lodestone Energy to launch New Zealand’s largest agrivoltaics farm, integrating solar generation with agricultural operations to boost renewable capacity and land use efficiency.

| Key Insights | Details |

|---|---|

| Building Integrated Photovoltaics (BIPV) Glass Market Size (2026E) | US$ 14.2 Bn |

| Market Value Forecast (2033F) | US$ 63.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 23.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 20.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Policy Led Acceleration of Sustainable and Net Zero Built Environments

The regulatory momentum toward sustainable buildings and net-zero energy standards is a foundational driver for BIPV glass adoption. In the European Union (EU), the revised Energy Performance of Buildings Directive (EPBD) mandates that all new buildings be designed to optimize solar energy generation beginning in 2026, with specific requirements for solar installations on residential and commercial buildings phased through 2030. Public buildings above defined size thresholds will also be required to integrate solar systems by 2028–2031 under this framework, fostering compliance with climate targets and renewable energy deployment. This directive supports the EU’s broader aim of expanding solar capacity toward 700 GW by 2030, creating regulatory certainty for solar-integrated building solutions.

Countries worldwide are also aggressively updating building energy codes and renewable energy policies to drive on-site solar deployment. As of 2024, more than 60 countries have policies promoting renewable energy integration and energy efficiency in the buildings sector, and at least 42 nations offer financial incentives for rooftop and building-integrated solar systems, strengthening market pull for BIPV technologies.

These policy frameworks reduce capital risk, increase project bankability, and align real estate development with energy performance reporting requirements, accelerating adoption among commercial, institutional, and residential developers. Such government engagement signals a long-term commitment to net-zero infrastructure transformation, making BIPV glass a strategic compliance and investment priority for forward-looking stakeholders.

High Upfront Costs and Technical Barriers Hamper BIPV Deployment

The prohibitive upfront cost of BIPV glass systems continues to limit broad adoption despite long term energy savings. BIPV systems typically carry a premium of around 20% or more versus conventional building materials, driven by specialized photovoltaic components, glass tempering, and integration requirements. In retrofit scenarios, these costs can escalate further due to structural reinforcement needs and bespoke design work.

For example, during the retrofit of Chicago’s 110-year-old Merchandise Mart, architects were forced to abandon glass BIPV laminates and opt for lighter, more expensive organic PV alternatives, significantly increasing project costs and undermining projected energy yields. This underscores how financial and technical hurdles can deter developers focused on short-term return horizons, especially in markets lacking robust incentives.

Compounding cost pressures is a shortage of technical expertise and awareness among builders and designers, particularly in developing regions. Many construction professionals lack the training to effectively design, install, and maintain integrated photovoltaic systems, leading to delays, higher risk perception, and increased project budgets.

Since BIPV requires collaboration across architecture, structural engineering, and electrical disciplines, projects without skilled interdisciplinary teams often extend timelines and incur additional costs. Until industry education, certification programs, and standardized installation protocols become more widespread, these knowledge and skill gaps will continue to constrain BIPV adoption, slowing growth outside leading markets with established technical capacity.

Smart Integration and Emerging Applications Unlock BIPV Potential

The integration of building-integrated photovoltaics glass with smart building systems and IoT platforms offers significant growth potential. Embedding real-time energy generation and performance data into building management systems (BMS) enables predictive maintenance, optimized energy flows, and participation in demand response programs. This reduces energy costs, improves occupant comfort, and enhances asset value. A notable example is the transparent organic photovoltaic facade installed on a commercial building in Santa Barbara, California, which offsets 20% of energy use while preserving architectural transparency, highlighting the commercial viability of smart BIPV solutions.

Emerging markets and cross-sector applications further expand opportunities. Rapid urbanization across Latin America, Africa, and Southeast Asia, combined with infrastructure investments in airports, hospitals, and civic centers, is driving scalable BIPV demand. Financing tools such as green bonds and power purchase agreements (PPAs) reduce adoption barriers. Non-building applications, such as agrivoltaics, generate energy while supporting agriculture, demonstrating how multifunctional BIPV solutions can unlock sustainability and new revenue streams across sectors. This expansion positions BIPV as a key enabler of climate-resilient and energy-efficient infrastructure worldwide.

Category-wise Analysis

Product Type Insights

The crystalline silicon segment is set to be the leading product type in 2026, accounting for approximately 42% of the BIPV glass market revenue share in 2026. Its energy conversion efficiency, durability, and well-established manufacturing ecosystem make it likely to remain the preferred choice for commercial facades and roofing systems. Global supply chains and production scale are projected to continue reducing unit costs, reinforcing its leadership. Based on industry deployments, Gain Solar integrated crystalline silicon BIPV glass across multiple commercial and residential projects, which suggests sustained adoption in both new construction and retrofits. These integrations provide a basis to estimate stable growth in market share and reinforce investor confidence in this segment’s dominance.

The thin-film technologies are projected to be the fastest-growing product segment, with an estimated CAGR of 28% through 2033, driven by demand for architectural flexibility and daylighting preservation. These advanced thin-film solutions are likely to gain traction in high-end residential and mixed-use developments. 2025 demonstrations of semi-translucent solar window modules in Spain indicate growing feasibility for aesthetic integration without compromising energy generation, supporting projected accelerated adoption. The market estimates suggest that as design-driven requirements increase, these advanced thin-film products will continue to capture a larger share of new BIPV installations.

Application Insights

Building facades are estimated to account for approximately 38% of the building-integrated photovoltaics glass market revenue share in 2026, likely maintaining the largest share among applications. Facades provide extensive surface area for energy generation while supporting architectural appeal in commercial and institutional buildings.

They are projected to remain critical for environmental, social & governance (ESG)-aligned construction and operational energy savings. Industry observations of facade integrations in dense urban projects suggest that BIPV glass can be effectively retrofitted, which supports continued estimated growth in this application. These trends indicate that building facades will remain the primary avenue for BIPV deployment during the forecast period.

Greenhouses and agrivoltaics are projected to be the fastest-growing application areas for building-integrated photovoltaic glass, expected to showcase a CAGR of around 29% through 2033, due to their dual-use energy and agricultural functionality. Photovoltaic glass in agrivoltaics can optimize land use and lower operational energy costs for farms. According to a research study conducted at IIT Bhilai, India, vertical module orientation configurations are likely to increase energy yield while maintaining crop productivity, supporting projected adoption. These developments suggest that BIPV solutions in agriculture could become a substantial emerging segment, particularly in regions with tropical and subtropical climates.

End-Use Sector Insights

The commercial sector is estimated to lead in terms of deployment, holding approximately 45% of the BIPV glass market share in 2026, driven by large facade and roof surfaces and sustainability mandates. Commercial adoption is likely to remain strong due to high visibility, ESG compliance, and potential ROI from energy savings. Pilot installations demonstrate measurable reductions in electricity consumption and validate expected efficiency gains, supporting projected continued market dominance. These trends reinforce the estimation that commercial buildings will remain the primary end-use sector for BIPV solutions over the forecast period.

The residential segment is projected to be the fastest-growing end-use sector, with an estimated CAGR of 26% between 2026 and 2033, supported by urban solar adoption and net-zero home initiatives. Modular and aesthetically integrated BIPV products are expected to drive uptake in high-end residential and multi-family buildings. Early 2026 implementations in Europe show enhanced natural lighting and energy performance, reinforcing adoption projections. Thus, the residential sector is likely to represent an increasingly significant share of BIPV installations, contributing to overall market growth estimates.

Regional Insights

North America Building Integrated Photovoltaic (BIPV) Glass Market Trends

North America is estimated to be a key regional market for BIPV glass in 2026, driven by the increasing adoption of integrated photovoltaic solutions in commercial, residential retrofit, and institutional buildings. A standout 2025 development is the SunRise Residential project in Edmonton, Alberta, where Mitrex’s eFacade PRO Plus building-integrated photovoltaic panels were installed over more than 30,000sq. ft. of facade area, earning a Guinness World Record for the largest solar panel mural and generating an estimated 265 kW of clean energy while reducing carbon emissions by around 150 tons per year. This visually striking and functional integration illustrates how BIPV systems can transform aging urban structures into energy-producing assets that align with sustainability goals.

The estimated growth trajectory of this regional market is further supported by federal and state-level sustainability policies, building energy codes, and evolving renewable incentives that enhance the business case for integrated solutions. Local building standards, such as California’s Title 24 and other green construction requirements, are fostering demand for advanced facade systems that contribute to emissions reductions and net-zero building aspirations. Supplier innovation in customizable BIPV panels that blend performance with architectural aesthetics is also broadening consideration among design professionals. With increasing emphasis on energy-efficient envelopes, North America is positioned to remain an important regional growth market for BIPV glass, particularly in mixed-use urban developments and major retrofit initiatives where integrated solar solutions can deliver both environmental and economic value.

Europe Building Integrated Photovoltaics (BIPV) Glass Market Trends

Europe is anticipated to lead the building-integrated photovoltaics glass market share in 2026, with an anticipated 38% share of global revenue, underpinned by strong climate policies and financial incentives. Schott AG launched semi-transparent BIPV glass modules for architectural applications across European building projects, reinforcing the region’s capacity to commercialize photovoltaic glass that meets both design and energy performance criteria. Europe’s regulatory environment, including EU-level mandates for near-zero energy buildings, supports this trend, making integrated PV an attractive option for new builds and major renovations.

Europe’s market is projected to have a stable growth with ongoing policy support and funding mechanisms that encourage broader uptake. Saint-Gobain’s August 2025 announcement of BIPV-integrated curtain wall solutions also signals continued supplier commitment to advanced integrated PV products tailored for European sustainable building markets. These developments, combined with feed-in tariffs and renovation incentives in countries such as Germany and France, are expected to underpin strong demand across commercial, institutional, and high-end residential segments. The region’s mature construction industry and stringent energy efficiency standards reinforce Europe’s long-term leadership in BIPV adoption.

Asia Pacific Building Integrated Photovoltaics (BIPV) Glass Market Trends

Asia Pacific is projected to be the fastest-growing regional market for BIPV glass, with an estimated CAGR of 25.1% during the 2026-2033 forecast period, driven by high-scale urbanization, renewable mandates, and large-scale infrastructure spending. Climacy announced transparent BIPV panels with 400 W capacity for roofs and facades, indicating advanced product availability tailored to mixed commercial, industrial, and residential applications. This launch highlights the region’s ability to commercialize high-capacity photovoltaic glass adapted to diverse building forms and climates.

Regional market expansion is further bolstered by rapid solar capacity additions such as China’s significant solar growth which provide a strong market pull for integrated solutions in new high-rise and urban developments. Collaborative initiatives such as the partnership between Netherlands-based Kameleon Solar and India’s Nithin SAI Renewables aim to accelerate local BIPV solution adoption in India, reinforcing broader Asia Pacific deployment prospects. Local government incentives, smart city frameworks, and infrastructure programs in countries such as Japan, South Korea, and Singapore also underpin projected BIPV penetration, especially in commercial and public buildings seeking sustainability credentials. These dynamics position Asia Pacific as a core engine of BIPV market growth globally.

-glass-market-outlook-by-region-2026–2033.webp)

Competitive Landscape

The global building integrated photovoltaics glass market structure appears to be moderately consolidated, led by players such as AGC Inc., Saint-Gobain, NSG Group, Onyx Solar, and Mitrex, which collectively control the lion’s share of revenues. These companies leverage strong ties with architects and developers, along with proprietary glass-coating and photovoltaic integration technologies.

Continuous R&D investment focuses on improving efficiency, transparency, durability, and architectural aesthetics. Vertical integration across glass manufacturing and PV technology provides scale and cost advantages. Strategic collaborations with engineering, procurement, & construction (EPC) firms and real-estate developers support wider adoption.

Alongside global leaders, regional and niche manufacturers compete through customized designs, localized compliance, and application-specific solutions such as façades and skylights. High entry barriers from certification requirements, long project timelines, and envelope integration limit rapid new entry. However, modular BIPV systems and prefabricated construction are gradually broadening participation. The competitive landscape is expected to evolve through selective consolidation, licensing, and technology partnerships. These strategies aim to expand geographic presence and address cost and performance constraints in net-zero buildings.

Key Industry Developments

- In December 2025, Panasonic began testing glass-based perovskite solar panels integrated into office windows to combine energy generation with transparent building envelope elements. This initiative is demonstrating commercial viability of perovskite photovoltaics for architectural applications and expanding opportunities for building-integrated solar solutions.

- In October 2025, Aelius Turbina announced that it will inaugurate a BIPV manufacturing facility in early 2026 to support the domestic production of façade panels, solar roof tiles, other BIPV products, and reduce import dependence in India. The new plant is expected to strengthen local supply chains and accelerate BIPV adoption in commercial and residential construction.

- In August 2025, Onyx Solar expanded its footprint across major U.S. cities by deploying customized photovoltaic glass in skyscrapers and urban infrastructure projects. The company continues to replace conventional facade and skylight materials with energy-generating glass across commercial buildings. With over 500 projects globally and partnerships with firms such as Coca-Cola, HP, and Novartis, Onyx Solar reinforces BIPV’s viability at scale.

Companies Covered in Building Integrated Photovoltaics (BIPV) Glass Market

- AGC Inc.

- Onyx Solar Group LLC

- Wuxi Suntech Power Co., Ltd.

- Borosil Renewables Ltd.

- First Solar

- TAIYO KOGYO CORPORATION

- SHARP CORPORATION

- GOODWE

- Belectric

- Carmanah Technologies Corp.

- Ertex Solar

- Tesla

- Nippon Sheet Glass Co., Ltd.

- Canadian Solar

Frequently Asked Questions

The global Building Integrated Photovoltaic (BIPV) glass market is estimated to reach approximately US$ 14.2 billion in 2026.

Stringent building energy regulations, net-zero targets, and the growing preference for multifunctional building envelopes are key demand drivers.

The market is estimated to grow at CAGR of 23.8% through 2033.

Opportunities are emerging from smart building integration, urban infrastructure investments, and expanding applications beyond traditional buildings.

AGC Inc., Saint-Gobain, NSG Group, Onyx Solar, and Mitrex are among the prominent participants shaping the competitive landscape.