- Medical Devices

- Peripheral Drug Eluting Balloons Market

Peripheral Drug Eluting Balloons Market Size, Share, and Growth Forecast 2026 - 2033

Peripheral Drug Eluting Balloons Market by Drug Coating (Paclitaxel Drug Coating, Sirolimus Drug Coating, Others), by Indication (Peripheral Arterial Disease, Peripheral Aneurysms, In-Stent Restenosis, Others), by Artery Type, by End User, by Regional Analysis, 2026-2033

Peripheral Drug Eluting Balloons Market Size and Trend Analysis

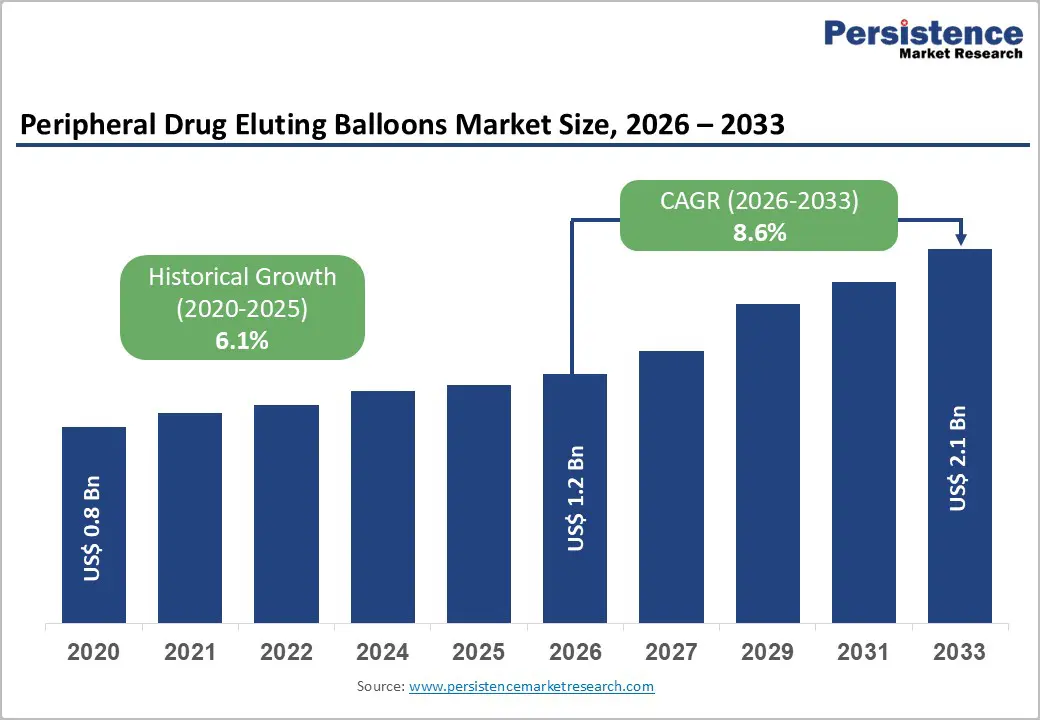

The global peripheral drug eluting balloons market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

Rising burden of peripheral arterial disease (PAD) in ageing and diabetic populations, combined with preference for minimally invasive endovascular procedures, is accelerating adoption of drug-coated balloons as an alternative or adjunct to stents in peripheral vessels. Growing clinical evidence supporting paclitaxel and emerging sirolimus coatings, coupled with favorable reimbursement and regulatory approvals in key markets such as the U.S., Europe, and China, further underpins steady volume expansion in femoropopliteal and infrapopliteal interventions. In addition, continuous innovation in coating technologies, vessel preparation techniques, and dedicated peripheral drug eluting balloon platforms is expected to sustain premium pricing and value-based procurement over the forecast horizon.

Key Market highlights

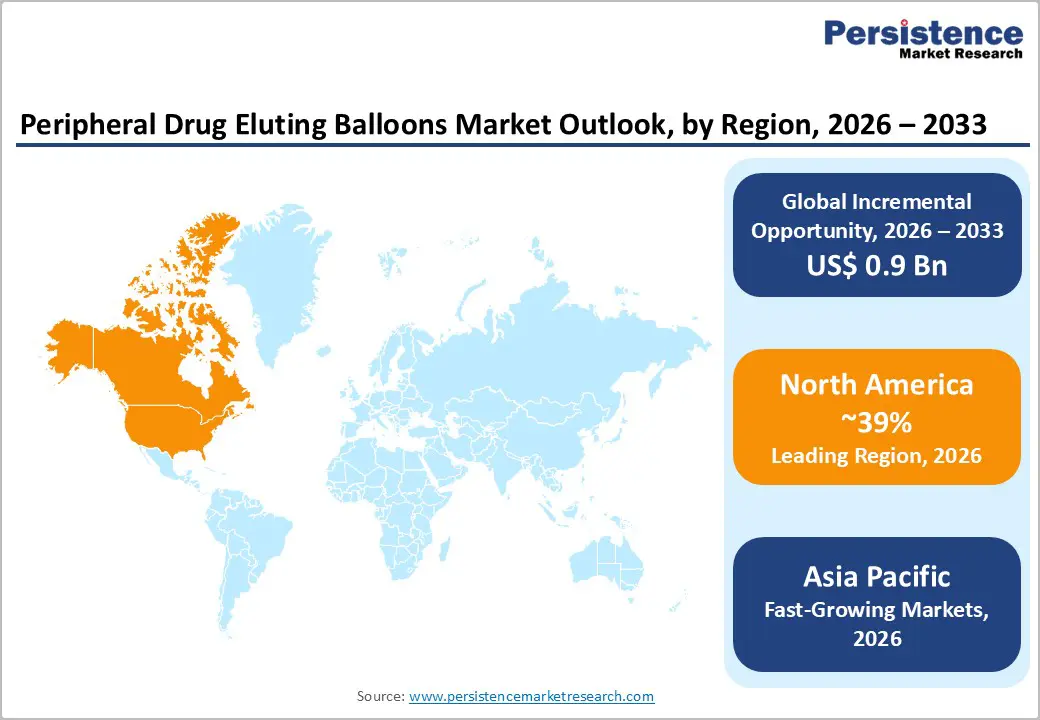

- North America remains the leading region, driven by high PAD burden, strong U.S. innovation and regulatory approvals, and robust reimbursement frameworks that support adoption of premium peripheral drug eluting balloon technologies across major vascular centers.

- Asia Pacific is the fastest growing region, propelled by rising cardiovascular risk factors in China, India, and ASEAN, expanding cath lab infrastructure, and supportive local manufacturing and policy initiatives that progressively improve access to advanced endovascular therapies.

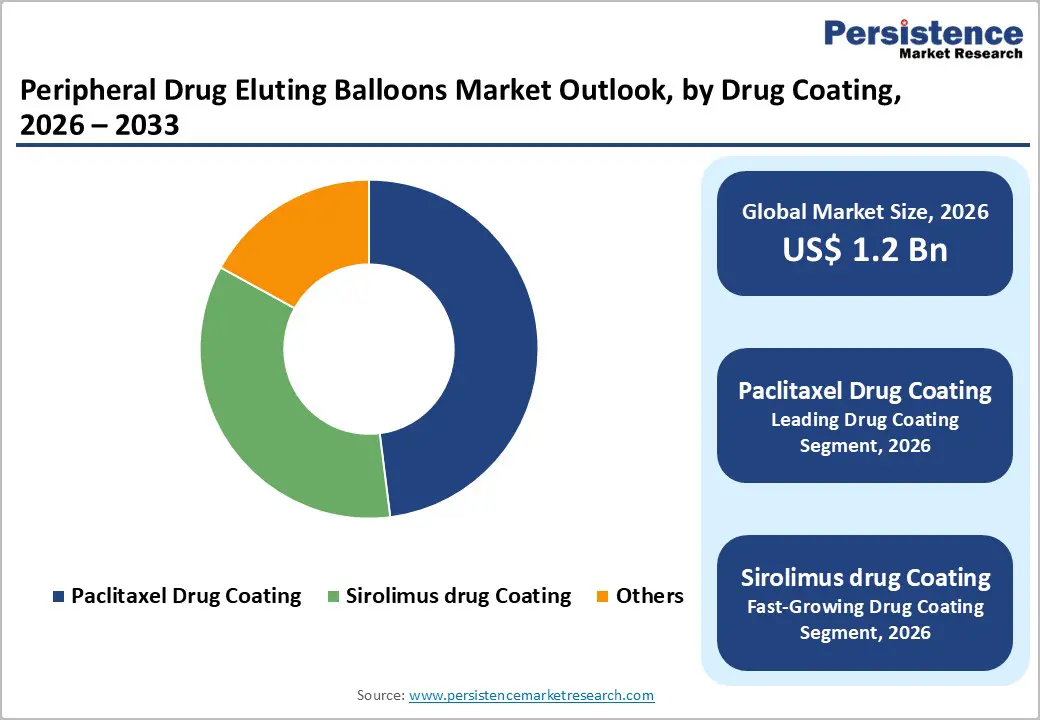

- Paclitaxel drug coating is the dominant segment by drug type, holding close to 48% share due to extensive clinical evidence, established safety communications, and broad adoption in femoropopliteal PAD interventions across North America and Europe.

- Sirolimus drug coating is the fastest growing segment, benefiting from emerging clinical data suggesting favorable vascular healing, strong interest in limus-based platforms, and new approvals such as rapamycin-coated balloons in high-growth Asian markets.

- A key market opportunity lies in expanding use of peripheral drug eluting balloons for complex femoropopliteal, BTK, and in-stent restenosis lesions, supported by vessel-preparation technologies, limb-preservation strategies, and evolving guidelines in PAD management.

| Global Market Attributes | Key Insights |

|---|---|

| Peripheral Drug Eluting Balloons Market Size (2026E) | US$ 1.2 billion |

| Market Value Forecast (2033F) | US$ 2.1 billion |

| Projected Growth CAGR (2026-2033) | 8.6% |

| Historical Market Growth (2020-2025) | 6.1% |

Market Dynamics

Driver- Rising prevalence of peripheral arterial disease and high-risk comorbidities

The primary growth driver for the peripheral drug eluting balloons market is the expanding pool of patients with peripheral arterial disease, largely driven by ageing demographics, diabetes, obesity, and smoking. Global epidemiology estimates suggest that more than 200 million people live with PAD, with prevalence increasing sharply after 60 years of age and among patients with type 2 diabetes and chronic kidney disease. These patients often present with complex, diffuse, and calcified lesions in femoropopliteal and infrapopliteal arteries, where restenosis after plain balloon angioplasty remains a major challenge and repeated revascularization is common. Drug-eluting balloons, by delivering antiproliferative drugs without leaving a permanent implant, help reduce target lesion revascularization (TLR) and maintain vessel patency, thereby improving limb salvage and quality of life, which significantly boosts clinical preference and procedural volumes.

Clinical and regulatory validation of paclitaxel and sirolimus-coated balloons

A second key driver is the strengthening of clinical and regulatory evidence demonstrating the safety and efficacy of paclitaxel-coated balloons and the emergence of sirolimus-coated balloons in peripheral applications. Earlier concerns about late mortality with paclitaxel devices have been addressed by updated analyses and communications from the U.S. FDA, which in 2023 stated that paclitaxel-coated devices used to treat PAD are unlikely to increase risk of mortality based on new long-term data. This has supported renewed clinician confidence and continued approvals of devices such as the SurVeil Drug-Coated Balloon in 2023 and AGENT Paclitaxel-Coated Balloon Catheter in 2024, reflecting robust regulatory support for this technology class. In parallel, randomized trials comparing sirolimus versus paclitaxel-coated balloons for peripheral interventions are expanding the evidence base and enabling differentiation of newer-generation products in terms of safety and vascular healing outcomes.

Restraint- Safety perceptions and legacy concerns around paclitaxel devices

Despite improved regulatory clarity, lingering safety perceptions around paclitaxel-coated balloons continue to act as a restraint in some markets and institutions. Meta-analyses of earlier randomized trials had suggested a potential signal for increased late mortality at 5-year follow-up in patients treated with paclitaxel-coated devices, with relative risk estimates around 1.57 compared with uncoated devices, prompting warnings and label changes. Although subsequent analyses and extensive post-market data have mitigated these concerns, some physicians and payers remain cautious, leading to slower adoption in specific patient subgroups and favoring alternative technologies such as bare metal stents or atherectomy in selected cases. This conservative stance can delay procedure growth and limit penetration in risk-averse healthcare systems.

Cost pressures and reimbursement variability across regions

Another restraint is the high per-procedure cost of drug eluting balloons relative to plain balloon angioplasty, combined with inconsistent reimbursement mechanisms across regions. In advanced markets, bundled payments and diagnosis-related group (DRG) systems may not fully recognize the incremental cost of premium devices, compelling hospitals to carefully select cases or negotiate discounts with manufacturers. In emerging economies, limited public funding, constrained private insurance coverage, and out-of-pocket payment structures restrict access to advanced endovascular technologies, especially in lower-tier hospitals. These cost and reimbursement challenges can slow broader diffusion outside high-volume tertiary centers and delay adoption in early-stage markets despite growing clinical need.

Opportunity- Rapid growth of sirolimus-based peripheral drug eluting balloons

One of the most attractive opportunities lies in the expansion of sirolimus-based peripheral drug eluting balloons, which are increasingly viewed as the next generation of antiproliferative technology for both coronary and peripheral applications. Sirolimus and related limus-family drugs offer a distinct mechanism of action with strong anti-proliferative effects and more favorable vascular healing profiles compared with paclitaxel, which is driving interest among interventionalists and trial sponsors. Emerging clinical data from studies such as NCT04475783, which compares Magic Touch PTA sirolimus drug-coated balloon to paclitaxel-coated balloons, along with national experiences in countries like India and China, suggest low rates of major adverse cardiac events (MACE) and TLR, supporting broader adoption. As more peripheral-specific sirolimus balloons gain regulatory approvals and reimbursement backing, this segment is expected to exhibit above-market CAGR and create differentiation opportunities for innovators.

Expanding use in complex lesions and below-the-knee interventions

A second opportunity arises from expanding indications and procedural use of peripheral drug eluting balloons in complex lesions such as long-segment femoropopliteal disease, in-stent restenosis, and below-the-knee (BTK) critical limb ischemia. As endovascular specialists seek to avoid multiple stents and maintain future treatment options, drug-eluting balloons are increasingly considered for de novo lesions, restenotic stents, and multilevel disease, especially when combined with vessel-preparation tools like atherectomy and specialty balloons. Ongoing clinical trials in regions such as Europe and Asia-Pacific are assessing peripheral drug eluting balloons in BTK applications, where improving limb salvage and wound healing is a key unmet need. Positive data from these studies, coupled with guideline updates by vascular societies and improved reimbursement for limb-preservation strategies, could significantly expand procedure volumes and drive long-term market growth.

Category-wise Insights

Drug Coating Analysis

Within Drug Coating, paclitaxel drug coating is the leading segment, accounting for about 48% of the global peripheral drug eluting balloons market in 2025. Paclitaxel’s strong lipophilicity and rapid tissue uptake enable short inflation times and durable suppression of neointimal hyperplasia, making it the reference standard for many femoropopliteal and infrapopliteal indications. Extensive clinical experience and product portfolios from major players such as Medtronic, Boston Scientific, and others, combined with multiple regulatory approvals and updated safety communications from the U.S. FDA, have reinforced confidence in paclitaxel-coated balloons for peripheral arterial disease treatment. Although sirolimus drug coating is projected to be the fastest growing segment, paclitaxel’s entrenched installed base, broad reimbursement coverage, and strong real-world outcomes keep it in a dominant position throughout the forecast period.

Artery Type Analysis

By Artery Type, Fem-Pop arteries (femoropopliteal segment) represent the leading segment and are estimated to account for around 45–50% of peripheral drug eluting balloon utilization in 2025. The superficial femoral and popliteal arteries are common sites of atherosclerotic disease, often with long, diffuse, and calcified lesions that are prone to elastic recoil and restenosis after plain angioplasty or bare metal stenting. Drug-eluting balloons have become an important treatment option in this vascular bed by delivering antiproliferative drugs to reduce neointimal hyperplasia while avoiding the challenges of multiple or long stent placements, especially across knee joints where mechanical stress is high. Strong clinical evidence for paclitaxel-coated devices in femoropopliteal disease, combined with ongoing studies of sirolimus-based systems, supports continued dominance of the Fem-Pop arteries segment compared with carotid, iliac, or purely infrapopliteal targets.

End User Analysis

Among End User segments, Hospitals constitute the leading setting for peripheral drug eluting balloon procedures, representing an estimated 60–65% share in 2025 due to concentration of vascular surgery and interventional radiology services in tertiary and large secondary care centers. Complex PAD and critical limb ischemia cases, as well as high-risk patients with multiple comorbidities, are typically managed in hospital-based catheterization labs and hybrid operating rooms that have advanced imaging, multidisciplinary teams, and access to a full range of devices. Moreover, reimbursement frameworks in regions such as North America and Europe often channel PAD interventions through inpatient or hospital outpatient departments, reinforcing hospitals’ dominant role compared with ambulatory surgical centers/outpatients and standalone cardiac catheterization labs. As case complexity and use of adjunctive technologies increase, hospitals are likely to maintain leadership, even as high-volume ambulatory centers grow faster in selected markets.

Regional Insights

North America Peripheral Drug Eluting Balloons Market Trends and Insights

North America is the leading regional market, accounting for about 39% share of the global peripheral drug eluting balloons market in 2025, driven primarily by the United States. High prevalence of PAD linked to obesity, diabetes, and smoking, together with well-established vascular centers and widespread availability of advanced endovascular technologies, supports strong procedure volumes. The U.S. FDA has approved multiple paclitaxel-coated balloon platforms, including the SurVeil Drug-Coated Balloon in 2023 and AGENT Paclitaxel-Coated Balloon Catheter in 2024, highlighting a robust regulatory and innovation ecosystem.

Reimbursement policies under Medicare and commercial insurers for peripheral interventions, along with ongoing registry and real-world evidence programs, further sustain device utilization and encourage adoption of newer drug-coating technologies. Academic vascular centers and integrated health systems in the U.S. and Canada actively participate in clinical trials and technology assessments, shaping evidence-based guidelines and accelerating uptake of both paclitaxel and sirolimus-coated balloons in complex PAD management.

Europe Peripheral Drug Eluting Balloons Market Trends and Insights

In Europe, the peripheral drug eluting balloons market benefits from a mature regulatory and clinical environment, with countries such as Germany, U.K., France, and Spain serving as key adoption hubs. High burden of cardiovascular and peripheral arterial disease in ageing populations, combined with strong public healthcare systems, drives steady demand for minimally invasive endovascular procedures. Harmonized regulatory pathways under the EU Medical Device Regulation (MDR) and long-standing experience with paclitaxel-coated balloons in femoropopliteal interventions support broad clinical acceptance and reimbursement in major markets.

Germany and other Western European countries have been early adopters of drug-coated balloons, incorporating them into routine PAD care and guideline recommendations, while the U.K. and France contribute significantly through national registries and health technology assessments. Southern European markets such as Spain show increasing utilization, supported by improvements in cath lab infrastructure and training. As newer sirolimus-based platforms complete clinical evaluations and secure CE marks, Europe is expected to remain a key region for early commercial roll-out and comparative effectiveness research in peripheral drug eluting balloon technologies.

Asia Pacific Peripheral Drug Eluting Balloons Market Trends and Insights

Asia Pacific is poised to be the fastest growing region for the peripheral drug eluting balloons market between 2025 and 2032, supported by rapid growth in China, Japan, India, and ASEAN countries. Rising prevalence of diabetes and vascular disease, expanding middle-class populations, and investments in cardiovascular and endovascular infrastructure are increasing the volume of PAD diagnoses and interventions. In China, healthcare reforms and favorable reimbursement policies for advanced devices have supported adoption of drug-coated balloons, with local approvals such as Firelimus® Rapamycin Drug-Eluting Balloon Catheter highlighting the region’s growing innovation capacity.

In India, clinical experience and post-marketing surveillance with both paclitaxel and sirolimus-coated balloons demonstrate favorable safety and efficacy profiles, fostering physician confidence and incremental uptake. Japan and developed ASEAN markets such as Singapore and Malaysia offer sophisticated cath lab networks and high procedure volumes, enabling premium device penetration. At the same time, regional manufacturing advantages and domestic device companies in China and India are contributing to cost-competitive offerings and local clinical evidence, reinforcing Asia Pacific’s position as the fastest growing market for peripheral drug eluting balloons in the coming decade.

Competitive Landscape

Market Structure Analysis

The global peripheral drug eluting balloons market is moderately consolidated, with leading shares held by large multinational device manufacturers alongside a growing cohort of specialized vascular companies. Major players such as Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, BIOTRONIK SE & Co. KG, and B. Braun Melsungen AG compete based on drug-coating technologies, deliverability, clinical evidence, and integrated procedural solutions. Key strategic themes include investments in sirolimus-based platforms, expansion of clinical programs in complex PAD and BTK indications, portfolio synergies with stents and atherectomy devices, and geographic expansion into high-growth markets in Asia Pacific and Latin America. Emerging business models feature value-based contracting, outcome-linked pricing, and partnerships with hospital systems to support limb-preservation programs and comprehensive PAD management pathways.

Key Market Developments

- In June 2023, Surmodics, Inc., a prominent provider of medical device and in vitro diagnostic technologies for the healthcare sector, announced that the U.S. Food and Drug Administration (FDA) had approved its SurVeil™ drug-coated balloon (DCB).

- In Aug 2022, BD initiated the first-in-human trial, non-randomized study designed to evaluate the safety of a drug-coated balloon (DCB). The study will determine the viability of sirolimus for treating peripheral arterial disease in the femoropopliteal arteries.

Companies Covered in Peripheral Drug Eluting Balloons Market

- Abbott Laboratories

- Boston Scientific Corporation

- Cook Medical Inc.

- MicroPort Scientific Corporation (Endovastec™)

- Medtronic Plc.

- Cardinal Health, Inc.

- B. Braun Melsungen AG

- BIOTRONIK SE & Co. KG

- Becton, Dickinson and Company

- W. L. Gore & Associates Inc.

- Getinge AB

- Terumo Corp

- Kyoto Medical Planning Co Ltd

- iVascular S.L.U

- Others

Frequently Asked Questions

The global peripheral drug eluting balloons market size is estimated at US$ 1.2 billion in 2026, with the market projected to grow to US$ 2.1 billion by 2033 at a CAGR of 8.6%.

Key demand drivers include rising peripheral arterial disease prevalence, ageing and diabetic populations, expanding minimally invasive endovascular procedures, and strong clinical evidence supporting paclitaxel and sirolimus-coated balloons for reducing restenosis and repeat interventions.

North America leads with 39% share in 2025.

A major opportunity lies in developing and commercializing sirolimus-based peripheral drug eluting balloons and expanding indications to complex femoropopliteal, below-the-knee, and in-stent restenosis lesions, supported by robust clinical trials and emerging reimbursement.

Key players include Abbott Laboratories, Boston Scientific Corporation, Medtronic plc, Cook Medical Inc., MicroPort Scientific Corporation, B. Braun Melsungen AG, BIOTRONIK SE & Co. KG, Becton, and others.