- Medical Devices

- Peripheral IV Catheter Market

Peripheral IV Catheter Market Size, Share, and Growth Forecast 2026 - 2033

Peripheral IV Catheter Market by Product Type (Short Peripheral IV Catheters, Integrated/Closed Peripheral IV Catheters, Safety Peripheral IV Catheters), by Technology (Conventional Peripheral IV Catheters, Safety Peripheral IV Catheters), End-user (Hospitals, Clinics, Ambulatory Surgical Centers, Homecare Settings), Regional Analysis, 2026–2033

Peripheral IV Catheter Market Share and Trends Analysis

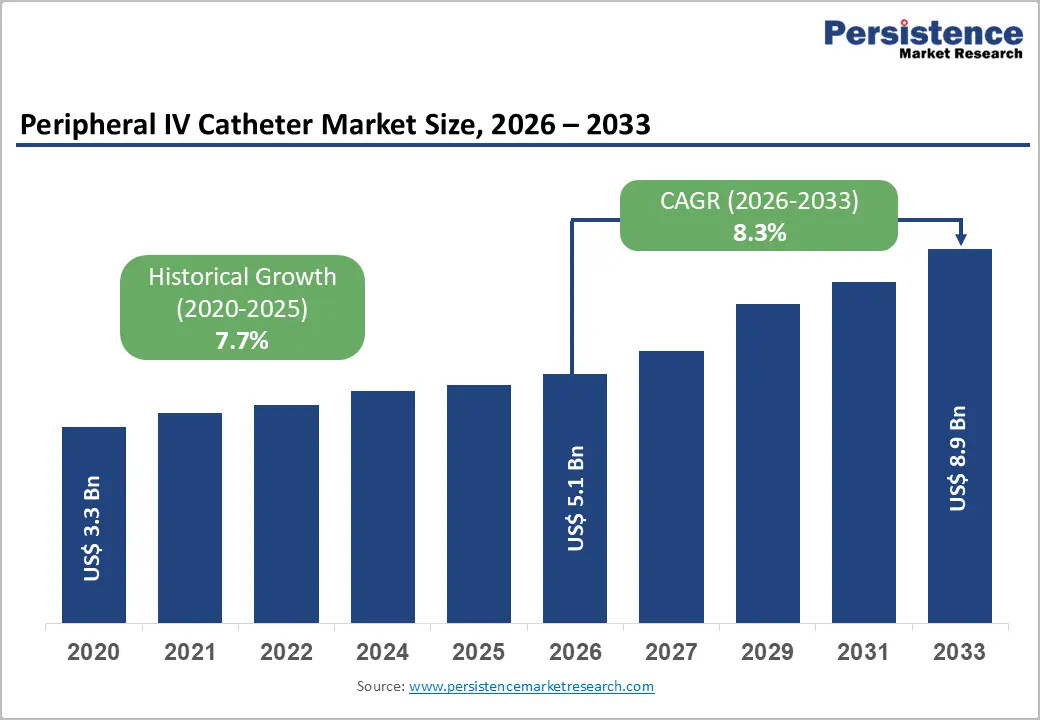

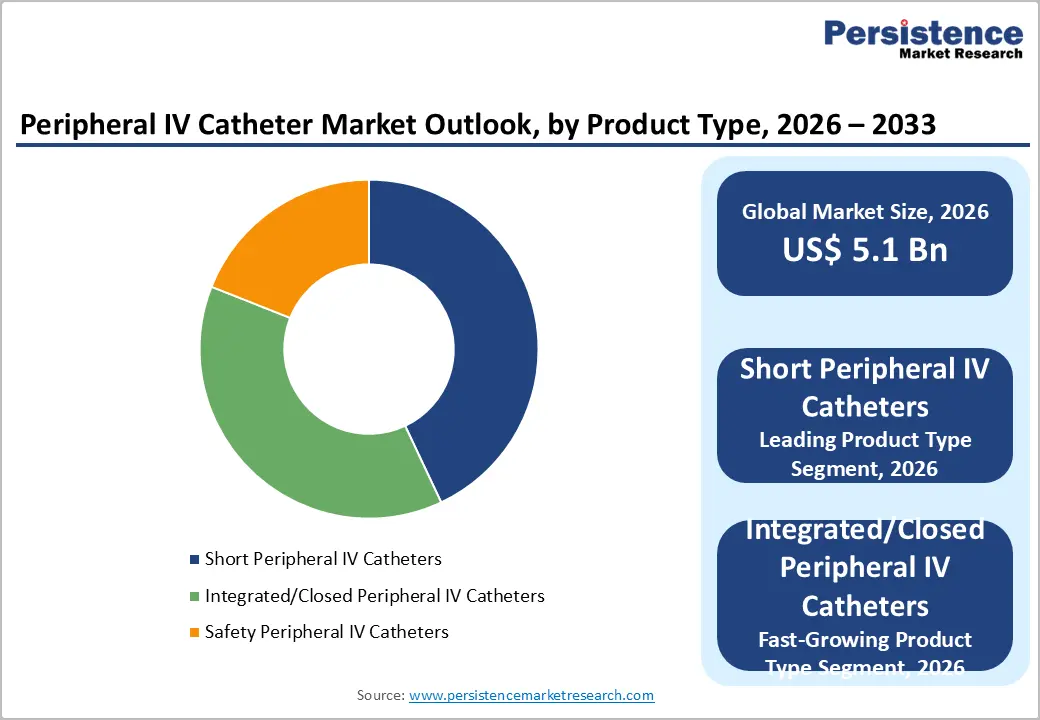

The global peripheral IV catheter market size is expected to be valued at US$ 5.1 billion in 2026 and projected to reach US$ 8.9 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. Rise in global surgical volumes, growing hospitalization rates, and intensifying regulatory focus on needlestick injury prevention mandate the adoption of safety-engineered IV access devices. The World Health Organization (WHO) estimates that over 313 million surgical procedures are performed annually worldwide, each requiring IV access. Simultaneously, mandates including the EU Directive 2010/32/EU on sharps injury prevention and equivalent U.S. regulations are structurally shifting procurement toward safety peripheral IV catheters. Expanding home care infusion therapy, growing ambulatory surgical center volumes, and rising healthcare infrastructure investment in Asia Pacific are further reinforcing consistent double-digit market demand growth.

Key Industry Highlights:

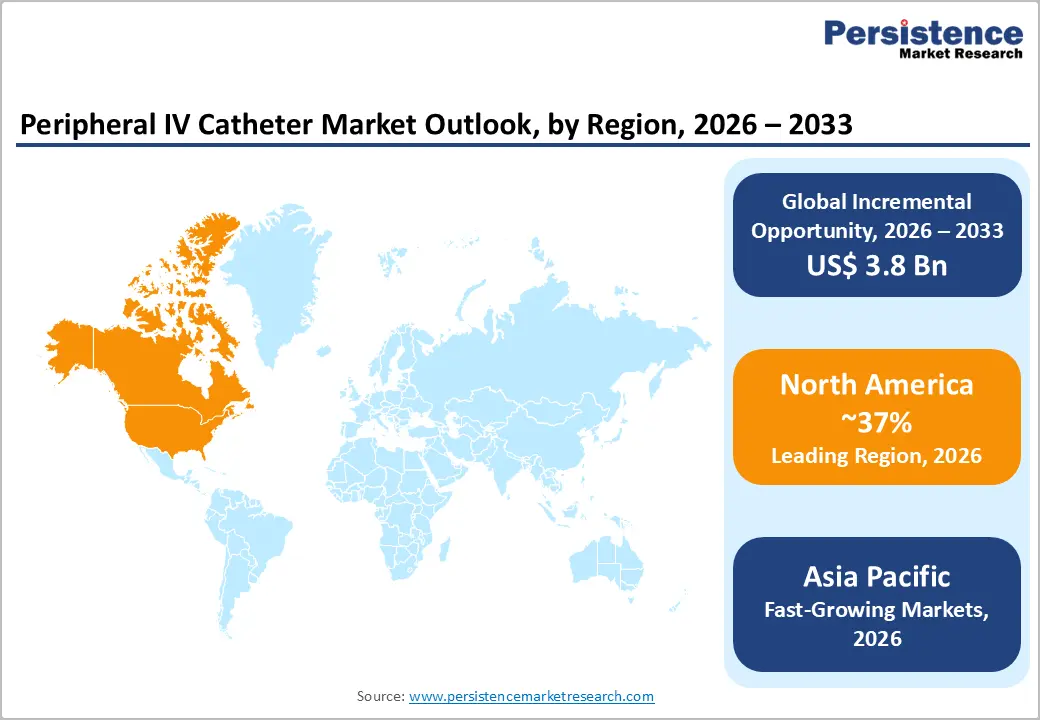

- Regional Leadership: North America leads the global peripheral IV catheter market with approximately 37% share in 2025, driven by over 50 million U.S. annual surgeries, OSHA sharps safety mandates, and premium safety catheter adoption by BD and Teleflex across major hospital GPO networks.

- Fast-growing Market: Asia Pacific is the fastest-growing peripheral IV catheter market, with China's 20 million+ hospital beds, India's Ayushman Bharat hospital expansion, and progressive sharps safety regulation adoption collectively driving above-average demand growth across the region.

- Leading Product: Short Peripheral IV Catheters lead the product type segment with approximately 43% share in 2025, standardized for universal acute care IV access use across emergency departments, surgical suites, and general wards globally, supported by BD's Nexiva and B. Braun's Introcan Safety product leadership.

- Fast-growing Product Type: Integrated/Closed Peripheral IV Catheters are the fast-growing product type, driven by CDC infection prevention priorities targeting catheter-associated bloodstream infections costing over US$ 46,000 per episode per AHRQ data, and Joint Commission standards mandating closed-system IV access adoption.

- Opportunity: The key opportunity lies in homecare infusion therapy expansion with NHIA reporting over 3 million U.S. homecare infusion patients annually, driving demand for extended dwell peripheral IV catheters enabling multi-day IV therapy in decentralized care settings beyond traditional hospital environments.

Market Dynamics

Drivers - Rising Surgical Volumes and Hospitalization Rates Globally

The growing global burden of surgical procedures encompassing elective, emergency, oncological, and cardiac interventions is the foundational structural driver of peripheral IV catheter demand, as IV access is required for virtually every inpatient and surgical care encounter. The WHO documents over 313 million surgical procedures annually globally, with over 50 million procedures performed in the United States alone per the American Hospital Association (AHA). Global hospitalization rates are rising in parallel with aging demographic trends. The UN DESA projects the population aged 65+ to reach 1.6 billion by 2050, increasing acute care admission volumes and per-patient IV catheter utilization. The non-substitutable nature of IV access in modern clinical care creates a direct, proportional demand relationship with healthcare service volumes.

Regulatory Mandates for Safety IV Catheter Adoption Driving Product Upgrades

Government and regulatory mandates requiring the adoption of safety-engineered sharps devices are creating a structural market transition from conventional to safety peripheral IV catheters across hospital procurement systems globally. The EU Council Directive 2010/32/EU implemented across all European Union member states, mandates the use of safety-engineered medical devices, including peripheral IV catheters to prevent needlestick injuries. In the United States, the Needlestick Safety and Prevention Act requires healthcare facilities to document annual reviews of safety device implementation. The U.S. Occupational Safety and Health Administration (OSHA) reports that approximately 385,000 needlestick injuries occur annually in U.S. healthcare settings. These regulatory frameworks create non-discretionary procurement mandates for safety IV catheter products, sustaining above-average growth for this sub-segment.

Restraints - Peripheral IV Catheter Failure Rates and Complications Limiting Utilization Efficiency

A significant clinical and economic restraint on peripheral IV catheter market growth is the high reported failure rate of conventional short peripheral IV catheters. Studies published in the Journal of Infusion Nursing indicate that over 50% of short peripheral IV catheters fail before completion of therapy, requiring reinsertion and generating additional product consumption while adding patient discomfort and clinician burden. High failure rates create pressure on hospitals to implement IV catheter stewardship programs, limiting unnecessary insertions, which may constrain per-patient utilization volumes in cost-sensitive healthcare environments.

Pricing Pressure from Group Purchasing Organizations and Competitive Tendering

The peripheral IV catheter market faces significant pricing pressure from consolidated hospital group purchasing organizations (GPOs) and government healthcare procurement authorities that leverage high-volume contracts to drive per-unit price reductions. In the U.S., major GPOs, including Premier Inc. and Vizient, negotiate standardized supply contracts covering tens of thousands of hospital beds, constraining individual manufacturer pricing power. In Europe and Asia Pacific, public hospital tender mechanisms similarly create winner-take-all procurement dynamics that compress margins for IV catheter manufacturers, limiting revenue growth relative to volume growth.

Opportunities - Integrated/Closed Peripheral IV Catheter Systems Reducing Infection Risk

Integrated and closed peripheral IV catheter systems incorporating passive safety mechanisms, closed-system blood control, and needleless connector integration represent the fastest-growing product type and a compelling commercial opportunity. The Centers for Disease Control and Prevention (CDC) estimates that catheter-associated bloodstream infections (CABSIs) affect hundreds of thousands of hospitalized patients annually, generating enormous preventable costs exceeding US$ 46,000 per infection episode per AHRQ data. Integrated IV catheter systems with closed blood management reduce accidental blood exposure and infection risk, making them increasingly preferred under hospital infection control protocols. Becton, Dickinson and Company (BD) and B. Braun Melsungen AG are leading commercial development of advanced closed-system IV catheter platforms, with hospitals and ASCs adopting these products to meet Joint Commission infection prevention standards.

Expanding Homecare Infusion Therapy and Ambulatory IV Access Markets

The rapid expansion of home care infusion therapy, encompassing IV antibiotic therapy, chemotherapy infusion, total parenteral nutrition, and hydration therapy administered in home settings, represents a high-growth market segment driving demand for extended dwell peripheral IV catheter products. According to the National Home Infusion Association (NHIA), the U.S. home infusion market serves over 3 million patients annually and is among the fastest-growing segments of home healthcare. Midline catheters and extended dwell peripheral IV catheters from manufacturers including Teleflex Incorporated and ICU Medical, Inc. are enabling multi-day IV therapy in home care settings previously requiring hospitalization. Post-pandemic expansion of decentralized care models, supported by payer incentives favoring site-of-care shift, is creating a durable new demand channel for advanced peripheral IV catheter products beyond traditional hospital settings.

Category-wise Analysis

Product Type Insights

Short peripheral IV catheters lead the product type segment with approximately 43% of total market share in 2025. Short PIVCs, typically 18–24 gauge, ranging from 1.75 to 2.5 inches in length, are the most widely used IV access device in acute care settings globally, standardized for emergency department access, surgical preparation, medication administration, and fluid/blood product infusion. Their universal clinical applicability across patient acuity levels, established nurse insertion proficiency, and cost-competitive pricing relative to more complex IV access alternatives entrench their dominant position.

Technology Insights

Safety peripheral IV catheters constitute the leading technology segment, capturing approximately 62% of total technology-based market share in 2025. Safety PIVCs' market leadership is directly attributable to regulatory mandates enacted across North America, Europe, and increasingly Asia Pacific requiring safety-engineered sharps devices in clinical settings. The OSHA Bloodborne Pathogens Standard (29 CFR 1910.1030) and EU Directive 2010/32/EU have created non-discretionary hospital procurement requirements for passive or active safety mechanism IV catheters. The reported reduction in needlestick injuries with safety IV catheter adoption, demonstrating 90%+ injury risk reduction in clinical evaluations published in Infection Control & Hospital Epidemiology, has accelerated institutional standardization and continues to drive progressive displacement of conventional catheters globally.

End-user Insights

Hospitals represent the dominant end-user segment in the peripheral IV catheter market, accounting for approximately 65% of total end-user share in 2025. Hospitals' market leadership reflects their role as the primary site of IV catheter utilization across emergency departments, ICUs, surgical suites, oncology infusion centers, and general medical/surgical wards. The American Hospital Association (AHA) reports over 6,000 registered hospitals in the United States alone, collectively administering tens of millions of IV catheter insertions annually. Large academic medical centers and integrated health systems represent the most significant institutional procurement accounts, standardizing IV catheter portfolios through GPO contracts. Ambulatory surgical centers represent the fastest-growing end-user segment, as the shift toward outpatient care models drives IV catheter demand beyond traditional hospital inpatient settings.

Regional Insights

North America Peripheral IV Catheter Market Trends and Insights

North America leads the global peripheral IV catheter market with approximately 37% of total market share in 2025, driven by the United States' high per-capita surgical and hospitalization volumes, robust hospital safety device mandates under OSHA regulations, and the significant installed base of leading manufacturers. Expanding home care infusion therapy and ambulatory surgical center growth are sustaining premium product adoption.

U.S. Peripheral IV Catheter Market Size

The United States accounts for approximately 85% of North American market share in 2025. With over 50 million annual surgical procedures and 385,000 healthcare needlestick injuries per year per OSHA data, U.S. hospitals are mandated to adopt safety IV catheters, sustaining strong premium segment revenue for BD, Smiths Medical, and Teleflex.

Europe Peripheral IV Catheter Market Trends and Insights

Europe is a mature and regulatory-driven peripheral IV catheter market, governed by EU MDR 2017/745 and the EU Sharps Directive 2010/32/EU mandating safety device adoption across healthcare facilities. Germany, the U.K., and France maintain well-established procurement programs for safety PIVCs, with public hospital tender frameworks favoring volume pricing for safety-engineered catheter portfolios from established manufacturers.

Germany Peripheral IV Catheter Market Size

Germany holds approximately 21% of the European peripheral IV catheter market in 2025. Germany's robust hospital infrastructure of over 1,900 acute care hospitals and stringent sharps safety regulations under the Technische Regel für Biologische Arbeitsstoffe (TRBA 250) drive consistent safety PIVC procurement. B. Braun Melsungen AG's German headquarters strengthens domestic market presence.

U.K. Peripheral IV Catheter Market Size

The United Kingdom represents approximately 17% of the European market in 2025. NHS procurement frameworks and NHS England's infection prevention directives mandate safety IV catheter adoption across all NHS trusts. Health and Safety Executive (HSE) enforcement of the UK Sharps Regulations (2013) creates a consistently regulated procurement environment supporting safety PIVC demand.

France Peripheral IV Catheter Market Size

France accounts for approximately 14% of the European peripheral IV catheter market in 2025. The Agence nationale de sécurité du médicament (ANSM) regulates IV catheter approvals, while French public hospital procurement through UGAP (the national procurement body) standardizes safety catheter sourcing. France's High Authority for Health (HAS) guidelines on healthcare-associated infection prevention reinforce safety PIVC procurement priorities.

Asia Pacific Peripheral IV Catheter Market Trends and Insights

Asia Pacific is the fastest-growing regional market for peripheral IV catheters, driven by rapidly expanding hospital infrastructure, rising surgical volumes, and growing regulatory harmonization toward safety device adoption. China is the largest and fastest-growing national market, with the National Health Commission of China reporting over 20 million hospital beds and implementing sharps safety regulations that are progressively increasing safety IV catheter uptake.

India Peripheral IV Catheter Market Size

India holds approximately 16% of Asia Pacific market share in 2025, driven by a hospital network exceeding 70,000 facilities per Ministry of Health and Family Welfare data and rising surgical procedure volumes under Ayushman Bharat. Domestic IV catheter manufacturers supplement supply from BD and B. Braun in the growing safety catheter segment.

Japan Peripheral IV Catheter Market Size

Japan holds approximately 20% of Asia Pacific market share in 2025. Japan's advanced healthcare infrastructure, high surgical procedure volumes, and active Ministry of Health, Labour and Welfare (MHLW) sharps safety guidelines drive consistent safety PIVC demand. Premium integrated and closed IV catheter systems are gaining adoption in Japanese academic medical centers and specialized surgical facilities.

Southeast Asia Peripheral IV Catheter Market Size

Southeast Asia contributes approximately 13% of Asia Pacific market share in 2025, with Thailand, Indonesia, and Vietnam as the most active markets. Rapid expansion of private hospital chains, growing medical tourism in Thailand, and improving public hospital procurement of safety-engineered IV devices are driving above-average peripheral IV catheter demand growth across the subregion.

Competitive Landscape

The global peripheral IV catheter market is moderately consolidated, with Becton, Dickinson and Company (BD), B. Braun Melsungen AG, Terumo Corporation, Teleflex Incorporated, and ICU Medical, Inc. collectively dominating global revenue through broad product portfolios, established GPO contracts, and global distribution networks. Competitive differentiation centers on passive safety mechanism innovation, closed blood management system integration, ultrasound-guided catheter placement accessories, and digital catheter tracking platforms. Emerging business model trends include outcome-based procurement agreements, vascular access team support services, and IV insertion training program bundling. Smiths Medical and Vygon SA compete through specialty catheter customization and hospital-direct sales models.

Key Developments:

- In September 2025, Johnson & Johnson launched the Shockwave Javelin Peripheral Intravascular Lithotripsy (IVL) Catheter in Europe to improve treatment for patients with peripheral artery disease (PAD) suffering from severely calcified and difficult-to-cross lesions.

- In November 2025, Fujifilm Sonosite launched PIV Assist, an AI-powered ultrasound feature designed to support peripheral intravenous (PIV) access planning. The solution was made available on Sonosite LX, PX, and ST ultrasound systems and helped clinicians identify candidate veins, assess vein size, and determine the maximum cannula size using catheter-to-vein ratio (CVR) analysis.

Global Peripheral IV Catheter Market - Key Insights

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 3.3 Billion |

|

Current Market Value (2026) |

US$ 5.1 Billion |

|

Projected Market Value (2033) |

US$ 8.9 Billion |

|

CAGR (2026–2033) |

8.3% |

|

Leading Region |

North America, ~37% market share (2025) |

|

Dominant Category (Product Type) |

Short Peripheral IV Catheters, ~43% share (2025) |

|

Top-ranking Category (Technology) |

Safety Peripheral IV Catheters, ~62% share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 3.8 Billion |

Companies Covered in Peripheral IV Catheter Market

- Becton, Dickinson and Company (BD)

- B. Braun Melsungen AG

- Terumo Corporation

- Teleflex Incorporated

- Smiths Medical

- Nipro Medical Corporation

- Vygon SA

- Argon Medical Devices, Inc.

- ICU Medical, Inc.

- C. R. Bard, Inc.

- Medical Components, Inc.

- AngioDynamics, Inc.

- Medtronic plc

Frequently Asked Questions

The global peripheral IV catheter market is estimated to be valued at US$ 5.1 billion in 2026.

The primary demand drivers are the global surgical volume exceeding 313 million annual procedures per WHO, regulatory mandates under OSHA's Bloodborne Pathogens Standard and EU Directive 2010/32/EU requiring safety IV catheter adoption, and rapid expansion of homecare infusion therapy serving over 3 million U.S. patients annually per NHIA data.

North America leads the global peripheral IV catheter market with approximately 37% of total market share in 2025.

The most significant opportunity lies in integrated/closed peripheral IV catheter adoption to address catheter-associated bloodstream infections which AHRQ estimates cost over US$ 46,000 per episode and the rapid expansion of homecare and ambulatory infusion therapy markets where Teleflex and ICU Medical are developing extended dwell IV catheter solutions enabling safe multi-day IV access.

The key market players include Becton, Dickinson and Company (BD), B. Braun Melsungen AG, Terumo Corporation, Teleflex Incorporated, ICU Medical, Inc., Smiths Medical, Vygon SA, Nipro Medical Corporation, AngioDynamics, Inc., Argon Medical Devices, Inc., and Medtronic plc, among others competing across short PIVC, safety, and integrated IV catheter system segments globally.