- Specialty & Fine Chemicals

- Paraffin Wax Market

Paraffin Wax Market Size, Share, and Growth Forecast, 2025 - 2032

Paraffin Wax Market By Application (Packaging, Candles, Others), Product Type (Fully Refined Paraffin, Hydrorefined/Specialty Paraffins, Others), Form, and Regional Analysis for 2025 - 2032

Paraffin Wax Market Size and Trends Analysis

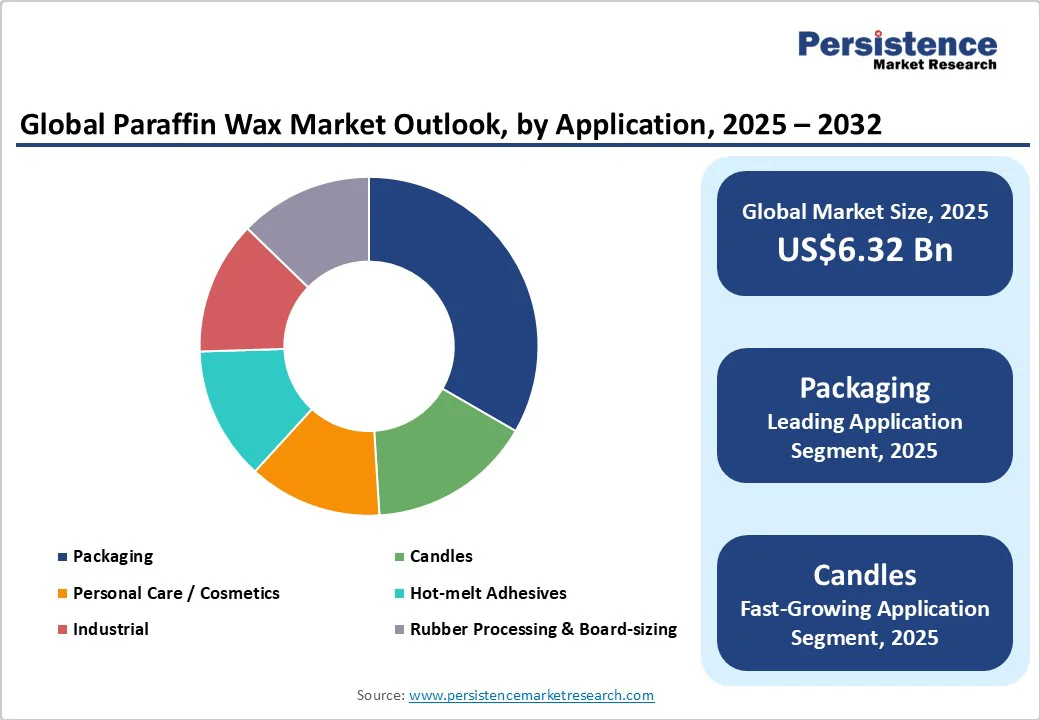

The global paraffin wax market size is likely to be valued at US$6.32 Billion in 2025 and is projected to reach US$9.73 Billion by 2032, growing at a CAGR of 6.5% between 2025 and 2032, driven by expanding demand across packaging, candle manufacturing, and personal-care applications.

Paraffin wax serves as a critical moisture and grease barrier in packaging, while also providing opacity, fragrance retention, and customizable melt points for candles and cosmetics.

Growth is driven by industrial uses such as hot-melt adhesives, board-sizing, and emerging phase-change materials. Asia Pacific leads the market with large refining capacity and cost advantages, while regulations in Europe and North America spur innovation. E-commerce and processed food exports further boost demand for high-quality paraffin wax in packaging.

Key Industry Highlights

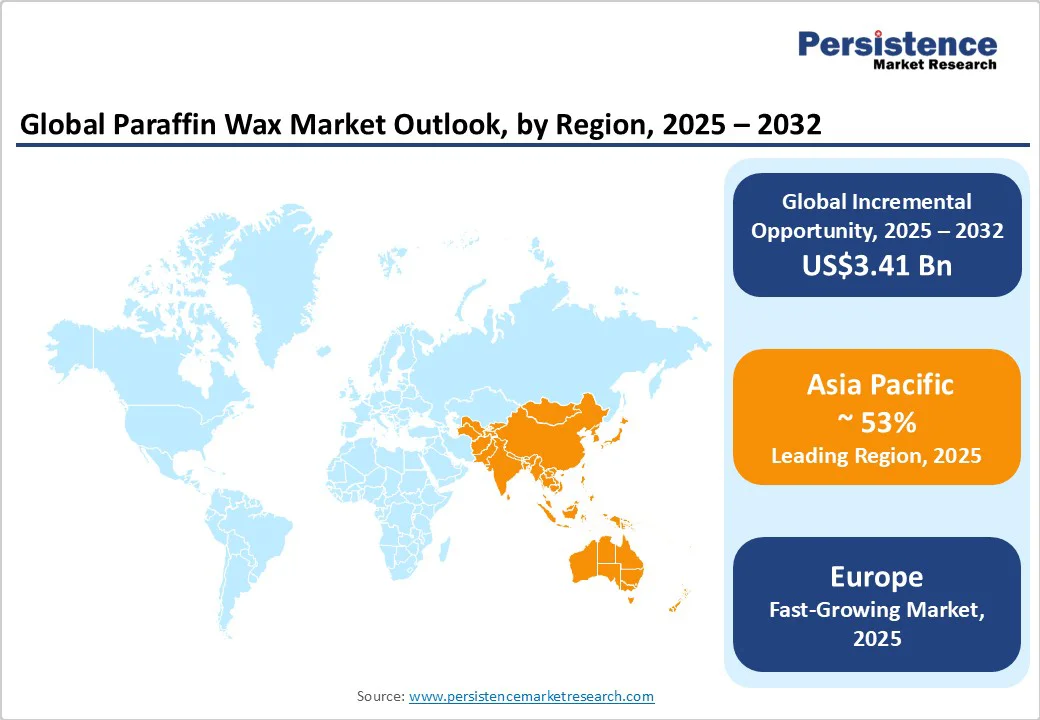

- Leading Region: Asia Pacific, accounting for approximately 53% of global revenue in 2025, driven by China’s large refining capacity, low-cost manufacturing, and growing domestic consumption across packaging, candles, and personal-care applications.

- Fastest-growing Region: Europe, with projected growth supported by premium candle demand, cosmetic applications, and regulation-driven adoption of low-VOC and hybrid paraffin waxes, contributing 28.7% of the global revenue share in 2025.

- Investment Plans: Capital investments are focused on establishing local blending and technical service hubs in Asia Pacific, upgrading production facilities for specialty and hydrorefined grades, and expanding R&D capabilities for low-VOC, high-performance paraffins to meet regulatory standards and customer demand.

- Dominant Application: Packaging dominates with 34% of total revenue in 2025, driven by paraffin’s use as a moisture and grease barrier in corrugated boards, food wraps, and multi-layer films, supported by e-commerce and processed food logistics growth.

- Leading Product Type: Fully refined paraffins lead the market, due to their purity and suitability for high-value applications such as cosmetics and premium candles, offering stable margins and regulatory compliance advantages.

| Key Insights | Details |

|---|---|

| Paraffin Wax Market Size (2025E) | US$6.32 Bn |

| Market Value Forecast (2032F) | US$9.73 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth in Packaging, E-commerce, and Personal Care

Paraffin wax is experiencing strong near-term growth, particularly in packaging, which accounted for about 33% of industry revenue in 2024. Its primary role is as a moisture barrier in corrugated boxes and food wraps. The rise of e-commerce and food exports in Asia Pacific and Latin America is driving demand for affordable, moisture-resistant packaging. This trend supports long-term supply contracts for refiners with strong logistics and ties to packaging manufacturers, enabling scale and price stability.

The candles segment is projected to grow, driven by rising demand for premium and scented candles in developed markets and growing aromatherapy use in emerging economies. Paraffin remains the preferred material due to its opacity, fragrance retention, and lower cost versus bio-based alternatives. In personal care, paraffin is used in ointments, wax blends, and skincare. Rising incomes in Asia are fueling demand, with higher margins for suppliers to beauty brands.

Industrial uses, such as adhesives, rubber processing, and board sizing, offer consistent demand and margin expansion through specialized waxes. Paraffin’s role in thermal energy storage and phase-change materials is also growing. Companies investing in custom formulations and R&D can command premiums and license technologies, turning specialty paraffin into a strategic growth asset.

Environmental Regulations and Price Volatility

As a petroleum-derived product, paraffin wax is under increasing environmental scrutiny, especially in Europe. Regulations like REACH and CLP, as well as national restrictions on the use of mineral oils in packaging, are raising compliance requirements.

To stay competitive in these regulated markets, producers may need to invest in purification systems, additional product testing, and new formulations that blend traditional paraffin with alternative feedstocks. These changes can raise production costs by several percentage points, particularly for companies aiming to maintain or grow their market share in the European Union.

Paraffin pricing is also highly sensitive to changes in crude oil and feedstock availability. Historically, prices have closely followed oil market trends. A sustained increase of 20% or more in crude oil prices can sharply reduce profit margins for wax producers and cause temporary supply shortages. Companies that do not own their own refining operations or lack a diversified raw material base are more exposed to this kind of earnings volatility.

Growth Opportunities in Asia Pacific and Specialty Low-Carbon Paraffins

Asia Pacific leads the global paraffin wax market, generating 55% of total revenue in 2025, with China at the forefront due to its vast refining infrastructure and manufacturing base. The region’s strongest growth opportunity lies in servicing rising export demand for packaging and cosmetic applications.

To capitalize, companies can establish regional supply hubs, toll-blending units, and technical service centers. Strategic moves such as joint ventures with local refiners, supply chain localization, and development of value-added blends could help unlock US$1.5-2.5 Billion in additional revenue by 2032.

Simultaneously, investing in low-carbon paraffin waxes presents long-term value. Products derived from gas-to-liquid (GTL) or hydrotreated processes, and hybrid blends incorporating bio-based inputs, align with tightening global regulations and appeal to sustainability-focused buyers. Certification of reduced carbon footprints can secure premium pricing and improve market access, particularly in Europe.

Specialty paraffins also offer margin expansion, yielding 10-30% higher returns per ton than standard grades. Shifting even a small share of output,5-10%, to these products can boost profitability and reduce exposure to commodity price swings. Together, regional expansion in Asia Pacific and innovation in low-carbon specialty waxes provide a dual-path strategy for sustainable growth and resilience.

Category-wise Analysis

Application Insights

Packaging remains the largest revenue contributor in the paraffin wax market, accounting for approximately 34% of total revenue in 2025. Its primary application is as a moisture and grease barrier in corrugated board, food wraps, and multi-layer packaging films.

High-volume, low-margin contracts dominate this segment, favoring large refiners with extensive logistics networks and the ability to maintain a consistent supply. Growth in e-commerce, cold-chain logistics, and processed food exports has further reinforced the importance of paraffin wax in packaging. Innovations in paper-based coatings and barrier films have increased demand for high-quality refined grades, ensuring that producers with scalable operations retain market dominance.

Candles are projected to register the fastest CAGR, driven by rising consumer preference for premium and scented products, particularly in North America, Europe, and Asia Pacific. The growth is fueled by lifestyle trends emphasizing home decor, wellness, and aromatherapy.

Paraffin wax is preferred for candle manufacturing due to its opacity, scent retention, and ease of molding. High demand for boutique candles and private-label products allows suppliers to sell higher-refined grades and customized melt-point waxes, enhancing per-ton revenue and margins. Expansion in emerging markets, especially India, ASEAN nations, and China, offers additional growth potential as disposable income rises.

Product Type Insights

Fully refined paraffins dominate, particularly in high-value applications such as cosmetics and premium candles, where purity, low oil content, and odor-free characteristics are critical. These grades are extensively used in applications involving food-contact and personal-care formulations.

The high standards required for fully refined paraffins create barriers to entry, benefiting established players with advanced refining and hydroprocessing capabilities. Producers of fully refined grades can command premium pricing, particularly in regions with strict regulatory frameworks such as Europe and North America.

Hydrorefined and specialty paraffins are seeing strong growth driven by stricter regulatory standards, sustainability goals, and performance-based applications. These high-purity grades are used in food-grade coatings, cosmetics, adhesives, and phase-change materials (PCMs) for thermal energy storage.

Their appeal lies in customizable properties such as melting point, oil content, and odor control to meet OEM requirements. Producers with hydroprocessing, GTL, or specialty blending capabilities can command price premiums and stand apart from commodity-grade waxes. This shift supports margin expansion and revenue stability through long-term OEM contracts, reducing reliance on cyclical segments, including candles and packaging, while strengthening competitive positioning.

Form Insights

Solid paraffin blocks and flakes remain the most common commercial form, used across candles, packaging, and industrial blending. Their advantages include simplified transportation, ease of storage, and predictable melting properties for processing.

This segment benefits from bulk contract agreements and long-standing supply chains that favor large-scale integrated refiners. Solid forms dominate export trade, particularly from China and the Middle East, to Europe and Asia, due to stability and handling efficiency.

Paraffin emulsions and liquid formulations are experiencing rapid growth, especially in textile, paper-sizing, and coating applications. Water-based emulsions are increasingly preferred over solvent-based alternatives to comply with VOC regulations and environmental mandates.

Industrial modernization in Asia and regulatory pressure for cleaner production processes have accelerated adoption. Emulsions offer process efficiencies, improved coating uniformity, and reduced energy costs for converters, creating opportunities for paraffin producers to expand into value-added, service-oriented markets.

Regional Insights

Asia Pacific Paraffin Wax Market Trends - Global Leader Fueled by Scale, Cost Efficiency, and Export Growth

Asia Pacific continues to dominate the global market, contributing approximately 53% of paraffin wax revenue in 2025. China remains the largest producer and consumer, benefiting from extensive refining capacity and a growing domestic demand for packaging, personal care, and industrial products. India and ASEAN countries are emerging as high-growth markets, supported by industrial expansion, population growth, and rising consumer spending.

The region’s cost-competitive production environment is further strengthened by integrated refining and petrochemical infrastructure. Investment trends are centered on expanding downstream blending capacities, establishing local service and formulation centers, and upgrading production lines for export-oriented applications. The rise in e-commerce, contract manufacturing, and private-label beauty brands is also boosting the demand for high-quality, customizable wax blends.

Recent developments include the commissioning of new wax production units in Southeast Asia, investments in fermentation-based and botanical-derived wax alternatives, and the introduction of digital quality tracking tools to meet international export standards. Governments in the region are increasingly supporting innovation in sustainable packaging and personal care, encouraging the adoption of paraffin wax alternatives and blends with improved biodegradability.

Europe Paraffin Wax Market Trends - Regulatory Compliance Driving Low-VOC and Sustainable Wax Solutions

Europe is the fastest-growing region as demand for paraffin wax is concentrated in countries, including Germany, the U.K., France, and Spain, where consumers favor premium candles and high-quality personal care products. The region is known for its strict regulatory environment, with rules such as REACH and CLP requiring extensive product testing and traceability of ingredients.

The shift toward low-VOC and hybrid waxes is gaining momentum, driven by both consumer preference and environmental mandates. Research and development activity is focused on formulating blends that meet performance requirements while reducing environmental impact. Investment efforts are targeting modernization of existing production sites, sustainable raw material integration, and development of multifunctional wax systems for cosmetic and household applications.

Recent developments include the rollout of low-emission waxes for indoor use, trials of bio-based additives in wax blends, and pilot projects exploring the circular use of wax in packaging applications. There is also increasing engagement with EU-funded sustainability programs aimed at reducing fossil-derived inputs across personal-care and home care product formulations.

North America Paraffin Wax Market Trends - Steady Demand and Focus on Clean Labels and Specialty Blends

Paraffin wax demand in North America remains strong, led by the U.S. Key drivers include consistent growth in candles, packaging, and personal-care applications. In particular, scented and wellness candles are gaining popularity as more consumers seek to enhance home ambiance and relaxation. Industrial uses, such as hot-melt adhesives and board-sizing for packaging and construction, also contribute meaningfully to regional consumption.

Regulatory pressure is shaping the market toward cleaner formulations, with increased adoption of fully refined paraffin and hydrotreated waxes. These developments are closely tied to safety and environmental standards, especially for products used in close contact with consumers. Capital investments are being directed toward quality improvements, modernization of production units, and the development of specialty blending operations near OEM and retail clusters to enhance service and logistics performance.

Recent developments in North America include the expansion of blending plants focused on clean-label candle formulations, upgrades to emission control systems at wax processing facilities, and collaborative R&D initiatives to develop waxes compatible with natural and plant-derived additives. Several producers are also exploring partnerships with sustainability certification bodies to align their products with consumer and retailer expectations.

Competitive Landscape

The global paraffin wax market is moderately fragmented, with several large integrated oil & refinery players achieving economies of scale, while numerous regional producers target niche applications. Leading global names include PetroChina, Sinopec, Sasol, ExxonMobil, Calumet, Nippon Seiro, Repsol, H&R Group, Honeywell, and Ergon.

Market concentration is higher in commodity packaging volumes and lower in specialty paraffins. Dominant strategies are product differentiation, vertical integration (refining + wax production), and regional footprint expansion. Leaders emphasize R&D for low-carbon products and strategic partnerships with OEMs.

Key Industry Developments

- In February 2025, Sasol expanded micronized wax portfolio with 32% lower product carbon footprint claims: captures low-carbon specialty market.

- In April 2024, ExxonMobil launched “Prowaxx,” reinforcing technology leadership and customer-facing branding for wax lines.

Companies Covered in Paraffin Wax Market

- Sinopec

- PetroChina

- ExxonMobil

- Sasol

- Calumet Specialty Products

- Nippon Seiro

- Repsol

- H&R Group

- Honeywell International

- Ergon, Inc.

- Cepsa

- Eni S.p.A.

- Linde Group

- Indian Oil Corporation

- TotalEnergies

- Shell Chemicals

- Gujarat State Fertilizers & Chemicals (GSFC)

- Sasol Wax

- Fuchs Petrolub

- Clariant

Frequently Asked Questions

The paraffin wax market size is estimated at US$6.32 Billion in 2025.

By 2032, the paraffin wax market is projected to reach US$9.73 Billion, growing at a CAGR of 6.5% between 2025 and 2032.

Key trends are the rising demand in packaging as a moisture and grease barrier and the growth of premium and scented candles globally, particularly in Asia Pacific.

By application, packaging is the leading segment, accounting for approximately 34% of total revenue in 2025, driven by its role in moisture and grease barrier applications for corrugated boards and food wraps.

The paraffin wax market is projected to grow at a CAGR of 6.5% from 2025 to 2032.

Key players include Sinopec, ExxonMobil, Sasol, Calumet Specialty Products, and PetroChina.