- Food Ingredients & Additives

- Olive Oil Market

Olive Oil Market Size, Share, and Growth Forecast 2026 - 2033

Olive Oil Market by Product (Extra Virgin Olive Oil, Virgin Olive Oil, Olive Pomace Oil, Refined Olive Oil), by End Use (Retail, Food Industry, Cosmetics), by Nature (Organic, Conventional), by Packaging, by Distribution Channel, by Regional Analysis, 2026 - 2033

Olive Oil Market Size and Trend Analysis

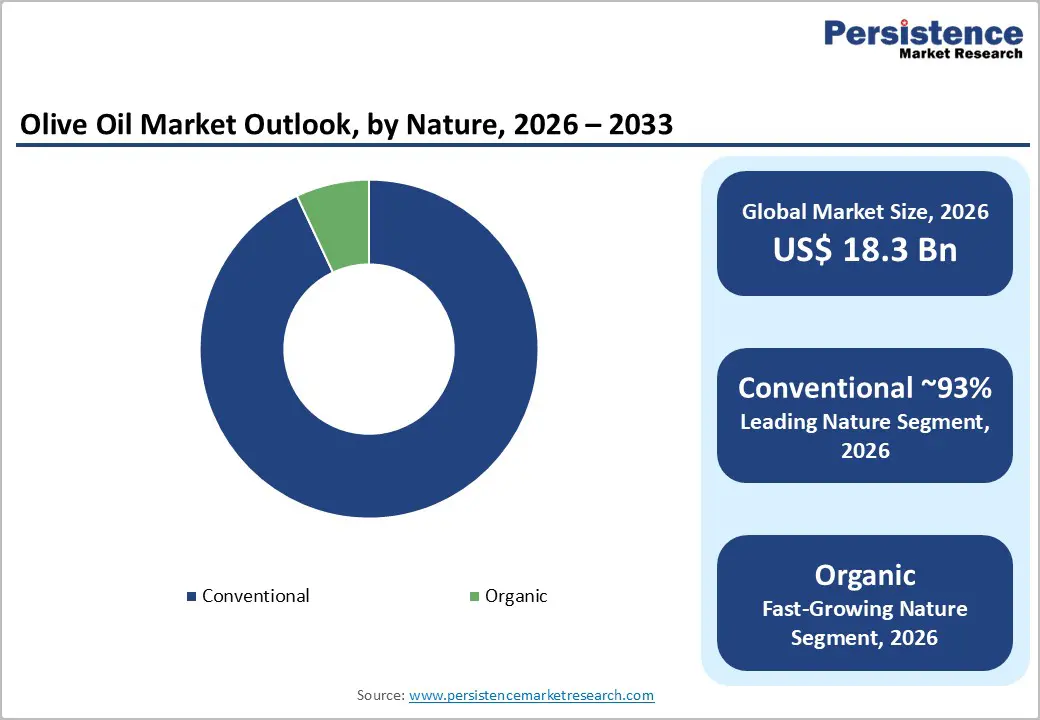

The global olive oil market size is expected to be valued at US$ 18.3 billion in 2026 and projected to reach US$ 24.5 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033. The market is expanding steadily, supported by increasing consumer inclination toward healthier and natural food ingredients.

Extra virgin olive oil, known for being minimally processed and free from chemicals, is gaining strong popularity due to its superior nutritional profile and rich antioxidant content. It preserves the natural flavor of olives and contains beneficial monounsaturated fats along with essential vitamins such as D and K. Growing awareness about its role in reducing cardiovascular risks, inflammation, and cholesterol levels is significantly driving its demand. The rising global focus on preventive healthcare and clean-label products is further accelerating adoption. As health-conscious eating habits continue to influence purchasing decisions, the demand for olive oil is expected to witness sustained growth in the coming years.

Key Industry Highlights:

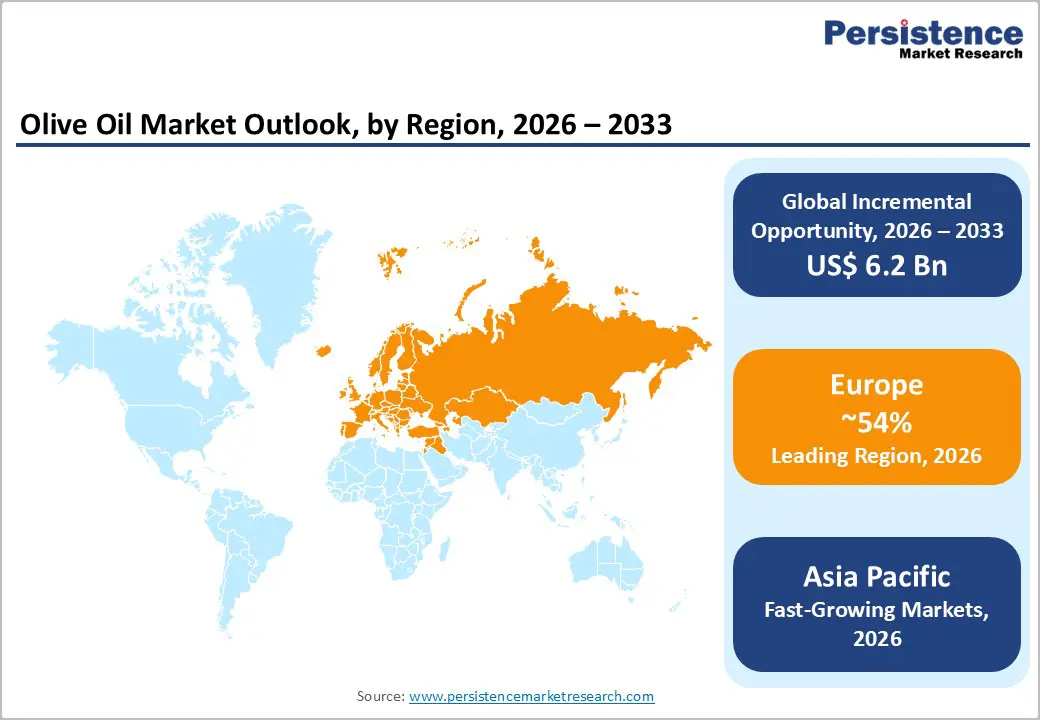

- Europe dominates the olive oil market with strong production capabilities and regulatory support, ensuring product quality and authenticity across Mediterranean countries.

- Asia Pacific is the fastest-growing region, driven by rising health awareness, higher incomes, and expanding retail and e-commerce infrastructure.

- Extra virgin olive oil is the dominant segment due to its superior nutritional profile and increasing consumer preference for premium products.

- Organic olive oil is the fastest-growing segment driven by demand for sustainable and chemical-free food products.

- Expansion in emerging markets and digital distribution channels offers significant growth opportunities for industry players.

| Key Insights | Details |

|---|---|

|

Olive Oil Market Size (2026E) |

US$ 18.3 billion |

|

Market Value Forecast (2033F) |

US$ 24.5 billion |

|

Projected Growth CAGR (2026–2033) |

4.2% |

|

Historical Market Growth (2020–2025) |

3.1% |

Market Dynamics

Drivers - Rising health consciousness and Mediterranean diet adoption

Growing awareness of the cardiovascular benefits of olive oil is a powerful driver of demand. Olive oil, especially extra virgin olive oil, is rich in monounsaturated fats and bioactive compounds such as polyphenols, which are associated with reduced risk of heart disease and inflammation. Reports from the World Health Organization (WHO) and the Harvard T.H. Chan School of Public Health highlight that replacing saturated fats with olive oil lowers total cholesterol and improves cardiovascular outcomes. The IOC notes that global olive oil consumption has increased at roughly 3% per year over the past few years, led by higher intake in developed economies and tourism-driven dining in Mediterranean countries. In the United States, the US Department of Agriculture (USDA) reports a consistent rise in olive oil imports, reflecting both at-home cooking and restaurant use, further supporting medium- to long-term growth in the olive oil market.

Restraints - Supply volatility due to climate and pest-related challenges

Olive oil supply is highly sensitive to weather patterns, droughts, and pest outbreaks, which can sharply reduce harvest volumes in key producing regions such as Spain, Italy, Greece, and Tunisia. The International Olive Council (IOC) and European Commission highlight that recent dry seasons have led to lower yields and increased production costs, pushing farm-gate prices higher. In several recent crop years, reported output fell by double digits compared with the previous year, affecting both domestic availability and export volumes. Higher prices incentivize substitution with cheaper vegetable oils (such as sunflower or soybean oil) in price-sensitive segments, potentially dampening olive oil demand growth in certain regions if supply constraints persist.

Opportunities - Organic olive oil surge in wellness-oriented markets

Organic olive oil represents one of the most attractive growth areas in the olive oil market. Consumers are increasingly seeking certified organic, non-GMO, and sustainably sourced products, especially for staple items like cooking oils. The Organic Trade Association and European Union organic regulations have expanded the scope of certified organic olive oil production, enabling producers in Spain, Italy, Greece, and Turkey to meet export demand. In the Asia Pacific, domestic standards for organic food products (for example, in India and China) are driving import demand for European-sourced organic olive oil. The USDA notes that organic olive oil commands price premiums of roughly 20–30% over conventional counterparts, which improves margins for producers and encourages investments in certified orchards and sustainable farming practices.

Category-wise Analysis

Product Insights

Within the olive oil market, Extra Virgin Olive Oil is the leading product segment, accounting for approximately 45% of global market share in 2025. This segment is defined by stringent quality criteria: it must be produced solely by mechanical extraction, with low acidity and minimal sensory defects. The International Olive Council (IOC) standards and national grading systems in Spain, Italy, and Greece reinforce the premium positioning of extra virgin olive oil. Consumer surveys and taste-test reports from organizations such as Consumer Reports and national food-safety agencies consistently rank extra virgin olive oil higher in flavor, aroma, and health-benefit perceptions than refined or pomace oils. As a result, retailers and foodservice operators prefer extra virgin olive oil for premium-segment products, which sustains its dominance in both volume and value terms.

Nature Insights

From a natural perspective, Conventional olive oil remains the dominant category, accounting for about 93% of the market share in 2025. This dominance is driven by higher production volumes, lower certification costs, and broader availability across price tiers. The IOC and FAO data indicate that the vast majority of olive oil produced globally is conventional, with certified organic or biodynamic olive oil representing a still-smaller share of total output. Conventional olive oil is widely used in both retail and food industry channels, particularly in value-oriented segments where price sensitivity is high. In contrast, Organic olive oil, although smaller in volume, is growing at a faster rate due to health-conscious and environmentally aware consumers who are willing to pay a premium for certified products.

Distribution Channel Insights

By distribution channel, Business-to-Business (B2B) is the leading segment, accounting for about 65% of the olive oil market share in 2025. This channel includes sales to food manufacturers, restaurants, catering companies, and institutional buyers. The European Union and United States trade data show that a significant portion of imported olive oil is destined for industrial formulations and commercial kitchens rather than direct consumer retail. B2B buyers benefit from economies of scale, standardized quality specifications, and long-term contracts, which stabilize demand and reduce price volatility exposure. In contrast, the Business-to-Consumer (B2C) channel, while smaller in share, is growing faster due to e-commerce expansion, health-focused retail marketing, and direct-to-consumer branding by premium producers.

Regional Insights

Europe Olive Oil Market Trends and Insights

Europe remains the world’s largest producer and consumer of olive oil, with countries such as Spain, Italy, Greece, Portugal, and Turkey forming the core of the regional market. The International Olive Council (IOC) estimates that Europe accounts for over 70% of global olive oil production, with Spain alone responsible for roughly 45% of world output in a typical year. The European Union's Common Agricultural Policy and rural development programs support olive farming and modernization, helping maintain production capacity despite climatic challenges. The EU PDO (Protected Designation of Origin) and PGI (Protected Geographical Indication) schemes also differentiate regional olive oils, reinforce quality perceptions, and justify premium pricing in both domestic and export markets.

Within Europe, mature markets such as Germany, France, the United Kingdom, and Scandinavia continue to grow due to rising demand for Mediterranean-style cuisines and health-oriented cooking. The European Food Safety Authority (EFSA) recognizes specific health claims for olive oil and heart health, which companies may reference in marketing communications. Cross-border trade within the Single Market ensures that olive oil flows efficiently from producing countries to high-value consuming markets, with Germany and France acting as major distribution hubs. At the same time, European regulations on sustainability, labeling, and traceability are pushing producers to adopt more transparent supply-chain practices, which reinforces consumer trust and supports long-term growth in the European olive oil market.

North America Olive Oil Market Trends and Insights

North America is a key import-dependent region for olive oil, with the United States driving most of the regional demand. The USDA reports that U.S. imports of olive oil have increased consistently over the past several years, reflecting both rising consumer awareness of health benefits and the expansion of Mediterranean-style restaurants and packaged foods. Domestic production, led by California Olive Ranch and other growers in California, has expanded through high-density orchards and modern irrigation techniques, but it still accounts for only a fraction of total U.S. demand. Federal and state-level food-safety and labeling standards, such as those from the FDA, help ensure product authenticity and quality, which supports consumer confidence in both imported and domestically produced olive oils. Supermarkets, club stores, and online retailers increasingly emphasize premium and organic olive oil lines, which aligns with broader wellness trends in North America.

Asia Pacific Olive Oil Market Trends and Insights

Asia Pacific is the fastest-growing regional segment for olive oil, with China, Japan, India, and several ASEAN countries driving demand. The International Olive Council (IOC) and trade data indicate that per-capita consumption in this region is still low compared with Europe, but it has been rising rapidly due to urbanization, rising disposable incomes, and exposure to Mediterranean cuisine. E-commerce platforms and modern retail chains have introduced olive oil to consumers who previously used cheaper vegetable oils, positioning it as a premium, health-oriented cooking fat. In India, the Agricultural and Processed Food Products Export Development Authority (APEDA) reports that imports of olive oil have increased at double-digit rates in recent years, mainly entering the retail and foodservice segments.

Manufacturing advantages in Southeast Asia and East Asia, such as established food-processing clusters and logistics infrastructure, also support the expansion of olive oil-based products. In China, government initiatives such as the “Healthy China 2030” strategy emphasize balanced diets and reduced saturated fat intake, thereby indirectly promoting olive oil consumption. Local food manufacturers are reformulating products to meet these guidelines, often using olive oil as a cleaner-label ingredient. In Japan, olive oil-based dressings, sauces, and bakery products are gaining share in supermarkets, supported by strong quality standards and consumer trust in imported brands. The combination of population growth, rising incomes in middle-class groups, and policy-driven health awareness positions Asia Pacific as the fastest-growing region for the olive oil market over the forecast horizon.

Competitive Landscape

The global olive oil market exhibits a moderately consolidated structure, dominated by a mix of large multinational companies and regional cooperatives. Key players such as Deoleo, S.A., California Olive Ranch, Cargill, Incorporated, Gallo Worldwide, LDA, and Colavita USA, LLC maintain strong market positions through vertical integration and extensive distribution networks. However, fragmentation persists due to numerous small-scale producers across Mediterranean regions. Companies are increasingly focusing on mergers, sustainability initiatives, premium product lines, and innovations in packaging and traceability, alongside expanding digital and direct-to-consumer sales channels to enhance competitiveness.

Key Developments:

- In January 2025, Borges India introduced Zero Pesticide Residue (ZPR) almonds along with two single-variety extra virgin olive oils, reinforcing its commitment to delivering high-quality, health-focused, and sustainable Mediterranean food products to Indian consumers.

- In July 2024, Spanish firm Genosa launched an innovative olive oil enriched with hydroxytyrosol, a phenol-rich compound known for its strong antioxidant properties and diverse health and application benefits.

Companies Covered in Olive Oil Market

- Gallo Worldwide, LDA

- Cargill, Incorporated

- Broges SA

- Deoleo, S.A.

- California Olive Ranch

- Fieldfresh Foods Private Limited

- Almazaras de la Subbetica

- Paolo Bonomelli Boutique Olive Farm

- Conagra Brands

- Oro del desierto

- Sucesores de Hermanos López SA

- Hacienda El Palo SL

- Frantoio Romano

- Colavita USA, LLC

- Others

Frequently Asked Questions

The market is expected to reach US$ 18.3 billion in 2026.

Rising health awareness and demand for functional and healthy edible oils are key drivers.

Europe leads with around 54% market share.

Key players include Deoleo, S.A., Cargill, Incorporated, California Olive Ranch, Colavita USA, LLC, and Gallo Worldwide, LDA.