- Home Appliances

- Non-stick Cookware Market

Non-stick Cookware Market Size, Share, and Growth Forecast 2026 - 2033

Non-stick Cookware Market by Product Type (Pans & Woks, Pots, Griddle, Bakeware, Others), by Coating Type (Teflon/PTFE Coating, Ceramic Coating, Hard-anodized Coating, Other), by Sales Channel (Offline, Online), by End user (Residential, Commercial), by Regional Analysis, 2026 - 2033

Non-stick Cookware Market Size and Trend Analysis

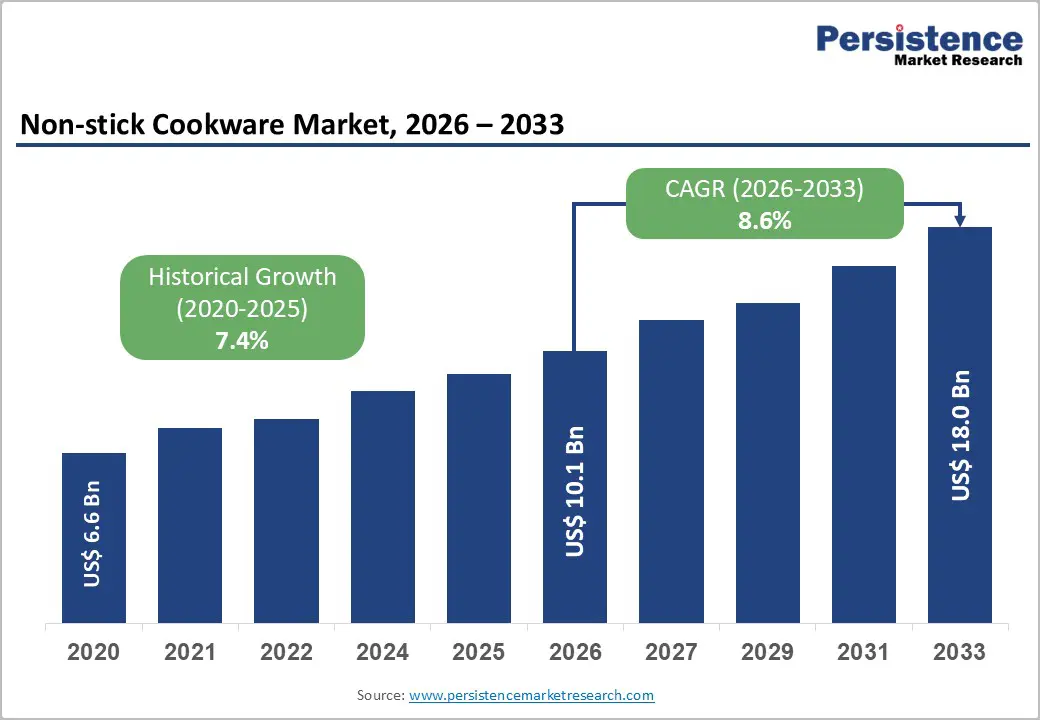

The global Non-stick Cookware Market size is likely to be valued at US$ 10.1 Billion in 2026 and is expected to reach US$ 18.0 Billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033. Rising consumer demand for convenient, low-oil cooking solutions drives this robust growth, fueled by health-conscious lifestyles and urbanization.

Key Industry Highlights:

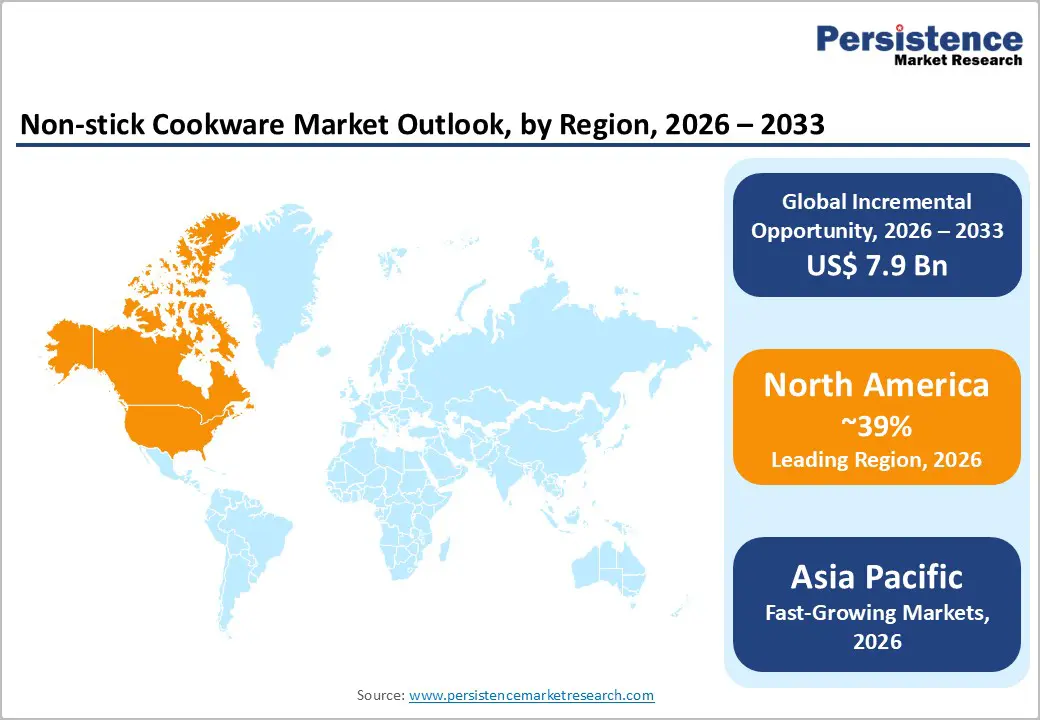

- Leading Region: North America leads as the dominant region having 39% share in the market, powered by U.S. innovation and strict FDA regulations ensuring consumer trust in safe, high-performance non-stick solutions.

- Fastest Growing Region: Asia Pacific emerges as fastest-growing region with rising CAGR of 9.8%, driven by China's manufacturing and India's urbanization fueling affordable residential demand.

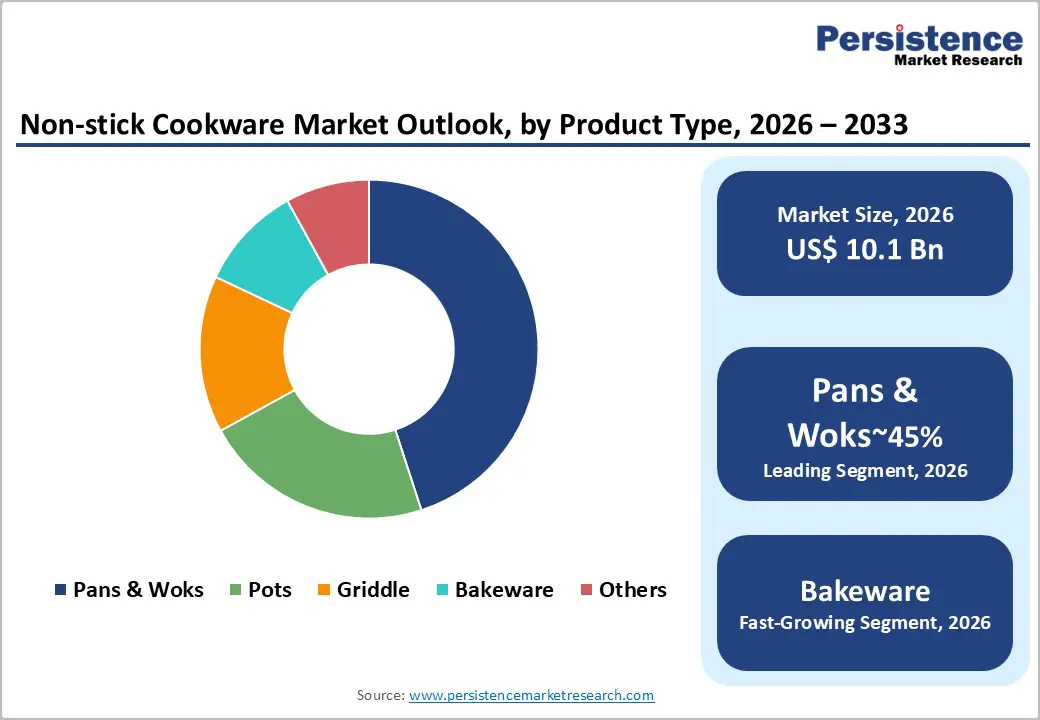

- Leading Segment: Pans & Woks dominate product type, holding 45% share due to versatile daily use in stir-frying across global households.

- Fastest Growing Segment: Ceramic Coating grows fastest in coatings, riding eco-trends and PFOA-free appeal for health-conscious buyers.

- Key Opportunity lies in commercial kitchens, where durable anodized options meet rising HORECA needs amid 4% outlet expansion.

| Key Insights | Details |

|---|---|

|

Non-stick Cookware Market Size (2026E) |

US$ 10.1 Billion |

|

Market Value Forecast (2033F) |

US$ 18.0 Billion |

|

Projected Growth CAGR(2026-2033) |

8.6% |

|

Historical Market Growth (2020-2025) |

7.4% |

Market Dynamics

Drivers - Growing health awareness and reduced oil consumption trends are accelerating global demand for non-stick cookware solutions

Growing health awareness among consumers worldwide is significantly increasing demand for non-stick cookware, as it supports oil-free or minimal-oil cooking aligned with global wellness trends. According to the World Health Organization, more than 1.9 billion adults were overweight in 2024, encouraging a shift toward healthier cooking habits. Research from the Harvard T.H. Chan School of Public Health indicates that methods such as air-frying and stir-frying can reduce fat intake by up to 80%.

In India, the National Institute of Nutrition reports that urban households have reduced oil consumption by nearly 20% since 2020, directly supporting higher sales of non-stick pans and woks. Millennials aged 25 to 40 represent around 40% of total buyers, as highlighted by Statista consumer panels. This strong alignment between health priorities and cooking convenience is ensuring steady and long-term volume growth in everyday kitchen categories.

Rapid urbanization and dual-income lifestyles are increasing preference for convenient, easy-to-clean non-stick cookware products

Rapid urbanization is driving demand for efficient and easy-to-use cookware, as busy city consumers increasingly prioritize convenience and faster meal preparation. Data from the UN-Habitat shows that 56% of the global population was living in urban areas by 2025, compared to 50% in 2020. At the same time, reports from the OECD indicate a 25% rise in dual-income households, where time-saving kitchen solutions are highly valued.

Non-stick cookware reduces post-cooking cleaning time by nearly 50%, according to tests conducted by Consumer Reports. Products using DuPont’s Teflon coating have experienced strong sales growth, particularly in densely populated Asia Pacific markets. The addition of features such as oven-safe compatibility and durable handles further supports premiumization, attracting modern, tech-savvy consumers seeking reliable and multifunctional kitchen tools.

Restraints - Ongoing safety concerns regarding PTFE coatings and overheating risks continue to influence consumer buying decisions

Concerns about chemical safety continue to restrict market growth, particularly around PTFE coatings previously associated with PFOA usage. Although the U.S. Environmental Protection Agency mandated the elimination of PFOA in 2015, consumer perception challenges remain. The Consumer Product Safety Commission reported that coating wear accounted for 12% of cookware-related complaints in 2024.

The European Food Safety Authority also notes that overheating PTFE above 260°C may release fumes, raising safety concerns among users. A survey in the UK revealed that 35% of consumers worry about scratches leading to chemical migration into food. While regulatory approvals confirm product safety within recommended limits, these perceptions slow adoption, particularly in price-sensitive markets, and are encouraging a gradual shift toward premium ceramic-coated alternatives.

Rising environmental awareness and recycling regulations are pressuring manufacturers to adopt more sustainable cookware solutions

Environmental concerns are increasingly influencing purchasing decisions in the non-stick cookware market. The Ellen MacArthur Foundation estimates that kitchenware contributes around 5% of household plastic waste, with PTFE coatings being non-biodegradable and difficult to recycle. Under the European Commission’s Circular Economy Action Plan introduced in 2020, stricter recycling targets have been set, yet nearly 60% of cookware products fail to meet these standards, according to Eurostat data.

In India, the Central Pollution Control Board reports approximately 1.2 million tons of kitchen waste generated annually. Consumer preference is also shifting, with 42% favoring eco-certified products such as those approved by Green Seal, according to Nielsen surveys. These pressures are increasing raw material and compliance costs while compelling manufacturers to innovate toward sustainable solutions.

Opportunity-Increasing demand for non-toxic ceramic coatings presents strong innovation and growth opportunities for manufacturers

Manufacturers have a strong opportunity to expand into ceramic-coated cookware, which is emerging as the fastest-growing segment due to its non-toxic and environmentally friendly positioning. The U.S. Food and Drug Administration has confirmed that ceramic coatings are safe at temperatures up to 450°C, higher than traditional PTFE limits. According to Mintel consumer trends, nearly 28% of U.S. consumers shifted toward ceramic-coated cookware after 2023.

In 2024, Groupe SEB launched new ceramic product lines, capturing approximately 15% market share in Europe based on company filings. Regulatory frameworks such as the European Chemicals Agency REACH standards are further encouraging PFOA-free innovation. In China, government-backed green manufacturing subsidies planned for 2025 are expected to boost production capacity. This segment is projected to grow at a CAGR of 12% through 2033, presenting strong revenue potential for innovation-driven brands.

The expanding foodservice industry demand for durable, high-performance cookware creates significant commercial growth opportunities

The commercial kitchen segment presents a significant growth opportunity, as restaurants and hotels increasingly require durable, high-performance non-stick cookware for heavy usage. The National Restaurant Association projects 4% annual growth in foodservice outlets through 2030, creating steady demand for long-lasting products. Hard-anodized cookware variants last up to 50% longer than standard options, according to testing by the Association of Home Appliance Manufacturers.

In India, hygiene regulations introduced by the Food Safety and Standards Authority of India are encouraging upgrades, with 22% of hotels adopting advanced cookware solutions by 2025, as per HVS reports. The World Travel & Tourism Council estimates global HORECA spending at nearly $50 billion, creating margin opportunities of 15% for suppliers offering scratch-resistant and antimicrobial innovations tailored to commercial kitchens.

Category-wise Insights

Product Type Analysis

Pans and woks account for approximately 45% of the product type segment, driven by their versatility in daily cooking activities such as stir-frying and sautéing. Data from the United States Department of Agriculture National Home Food Consumption Survey shows that pans are used weekly in nearly 60% of U.S. households due to even heat distribution and the ability to reduce cooking time by up to 30%.

In Asia, woks remain culturally essential, with Japan’s Ministry of Agriculture, Forestry and Fisheries reporting penetration rates close to 70%. Product durability improvements, including reinforced rims and scratch-resistant bases, have further strengthened consumer loyalty, according to ratings from Consumer Reports. The continued rise in home cooking after the pandemic has reinforced this dominance, ensuring stable revenue contribution from everyday-use cookware categories.

Coating Type Insights

Teflon or PTFE coatings hold around 52% share within the coating type segment due to their strong non-stick performance and cost-effectiveness. Developed and patented by DuPont, Teflon coatings are recognized for durability and smooth release properties that last nearly twice as long as many alternatives. Tests conducted under ASTM International standards indicate up to 90% oil reduction during cooking. The European Food Safety Authority confirms that PTFE remains safe when used below 260°C, supporting consumer confidence.

Sales Channel Insights

Offline retail channels account for nearly 60% of total sales, supported by consumer preference for physical product inspection before purchase. The National Retail Federation reports that around 70% of cookware purchases occur in-store, where customers can assess weight, coating finish, and handle comfort. Major retailers such as Walmart and Tesco drive high volumes through promotional campaigns and in-store demonstrations.

In India, the Federation of Indian Chambers of Commerce & Industry notes that nearly 55% of buyers prefer offline channels due to greater trust in quality verification. While e-commerce continues to expand, especially among younger consumers, physical retail remains dominant because it provides immediate product availability and strengthens brand confidence at the point of sale.

End-user Insights

Residential users represent approximately 75% of total demand, reflecting the continued importance of home cooking across global markets. Data from the OECD indicates that nearly 85% of meals worldwide are prepared at home daily. The International Labour Organization reports a 40% increase in remote and hybrid work arrangements since 2020, which has further encouraged home meal preparation.

Insights from Euromonitor International highlight affordability and convenience as key drivers for families choosing non-stick cookware. With more than 2.4 billion urban residents globally, as reported by the United Nations data, demand for easy-to-clean and time-saving kitchen products continues to rise. This strong residential base ensures stable recurring purchases and reinforces long-term market leadership over commercial segments.

Regional Insights

North America Non-stick Cookware Market Trends

North America leads the global market, supported by strong U.S. demand and strict regulatory standards. The U.S. Food and Drug Administration has enforced PFOA-free compliance since 2016, strengthening consumer trust and encouraging innovation. The United States Department of Agriculture reports that nearly 80% of U.S. households owned non-stick cookware by 2025, driven by health-focused cooking habits.

Companies such as Conair Corporation expanded production capacity in 2024 to meet rising demand. In addition, brands such as Calphalon introduced advanced anodized product lines, contributing to approximately 15% growth in premium cookware sales, according to the Association of Home Appliance Manufacturers. Continuous R&D investment and strong retail infrastructure further strengthen regional leadership.

Europe Non-stick Cookware Market Trends

Europe’s market growth is shaped by regulatory alignment and sustainability standards across member states. Guidelines from the European Food Safety Authority encourage safer coating technologies, accelerating the shift toward ceramic alternatives. Germany and the United Kingdom together account for nearly 40% of regional demand. Groupe SEB, through its Tefal brand, reported a 20% sales increase in France in 2024.

Spain’s European Food Information Council promotes low-fat cooking awareness, indirectly supporting product demand. In the UK, British Retail Consortium standards reinforce compliance and commercial adoption. Companies such as Denby Pottery Company continue to innovate with REACH-compliant sustainable coatings, strengthening Europe’s position as a regulated and quality-focused cookware market.

Asia Pacific Non-stick Cookware Market Trends

Asia Pacific is the fastest-growing region, supported by strong manufacturing capacity and rising domestic consumption. China accounts for nearly 80% of global cookware production capacity, according to industry estimates from the China Association of Automobile Manufacturers. Exports remain strong, while domestic demand in India is expanding rapidly, with Hawkins Cookers Limited reporting 18% growth in 2025 filings.

In Japan, premium precision cookware technologies enhance product quality and durability. Urbanization across ASEAN countries is expected to reach 60% by 2030, based on United Nations projections, further increasing residential demand. Indian brands such as TTK Prestige are strengthening online distribution channels, supporting higher household penetration and sustained regional expansion.

Competitive Landscape

The non-stick cookware market is moderately consolidated, with leading players holding a combined share of approximately 35%. Companies such as Groupe SEB and Newell Brands maintain strong positions through acquisitions, innovation, and global distribution networks. Strategic focus areas include sustainable coating technologies, premium product launches, and expansion of direct-to-consumer channels. Brands differentiate themselves through advanced durability features, including Teflon-branded coatings that reinforce performance credibility.

At the same time, regional manufacturers continue to compete on price and localized offerings, resulting in a fragmented competitive environment in emerging markets. Increasing investment in digital marketing, omnichannel retail strategies, and R&D is shaping long-term competition. Overall, established leaders are leveraging brand reputation and product innovation to strengthen margins while expanding their global footprint.

Key Developments:

- In March, 2024: Groupe SEB unveiled a new eco-designed ceramic non-stick cookware range in Europe featuring advanced ceramic coatings and substantial use of recycled materials, including up to 25% recycled content to reduce environmental footprint while meeting rising consumer demand for sustainable kitchen products.

- In July, 2025: TTK Prestige Limited announced the commissioning of expanded triply cookware production capacity at its Gujarat facility, boosting annual output by 12 lakh units to serve commercial and FSSAI-compliant durable cookware segments amid rising demand for high-quality cookware in hotels and foodservice sectors.

- In November, 2024: Newell Brands’s Calphalon brand rolled out advanced scratch-resistant PTFE non-stick cookware in the U.S., marketed for enhanced durability and performance, helping strengthen retail partnerships with major national retailers and attract quality-focused consumers.

Companies Covered in Non-stick Cookware Market

- Bernde

- Bradshaw International

- Conair Corporation

- Groupe SEB

- Calphalon (Newell Brands LLC)

- Cook N Home

- Cuisinart

- Denby Group Limited

- Nordic Ware

- Regal Ware, Inc.

- The Vollrath Company, LLC

- Tefal

- Hawkins Cookers

- Scanpan USA, Inc.

- TTK Prestige Limited

- Meyer Corporation

- GreenPan

- Lodge Cast Iron

Frequently Asked Questions

Valued at US$ 10.1 Billion in 2026, it will reach US$ 18.0 Billion by 2033, growing at 8.6% CAGR amid health-driven demand.

Health consciousness for low-oil cooking and urbanization promoting time-saving tools lead growth, supported by WHO obesity stats and UN urban trends.

Pans & Woks hold 45% share, favored for versatility in daily cooking per USDA usage data.

North America dominates via U.S. innovation and FDA safety standards, driving premium adoption.

Ceramic coatings offer high potential with eco-appeal and regulatory support like EU REACH, targeting 12% CAGR.