- Automotive Components & Materials

- Nerf Bars and Running Boards Market

Nerf Bars and Running Boards Market Size, Share and Growth Forecast, 2026-2033

Nerf Bars and Running Boards Market by Product Type (Electric, Mechanical), Material (Steel, Stainless Steel, Composite Polymer, Aluminum, Others), Thickness (3 Inches, 4 Inches, 5 Inches, 6 Inches), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), and Regional Forecast for 2026-2033

Nerf Bars and Running Boards Market Share and Trends Analysis

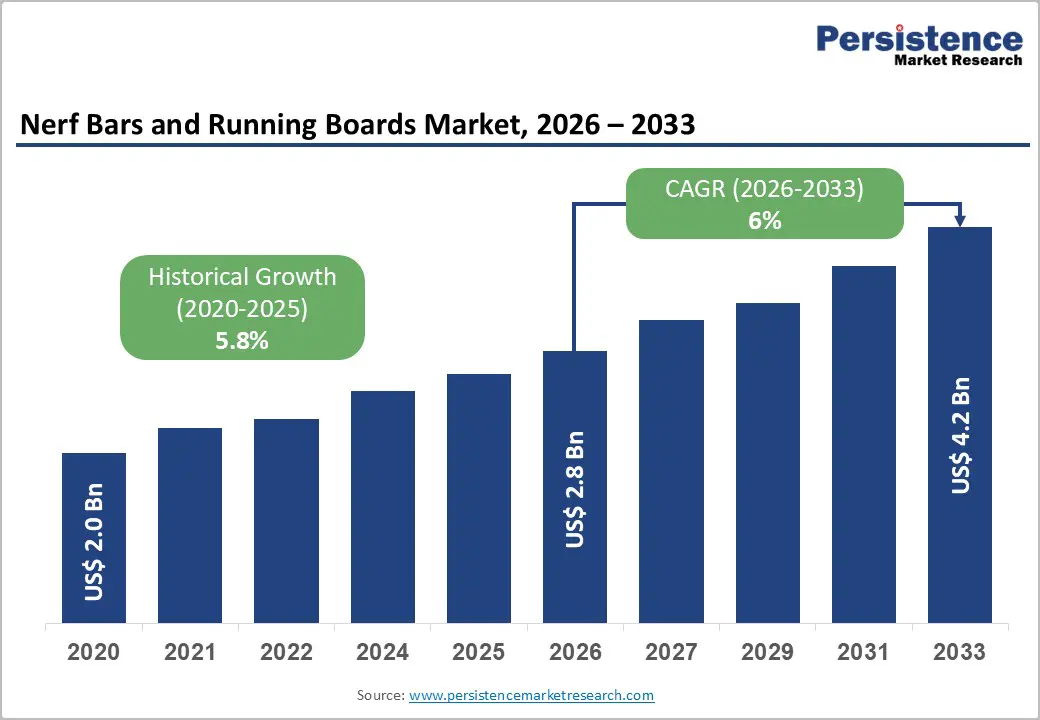

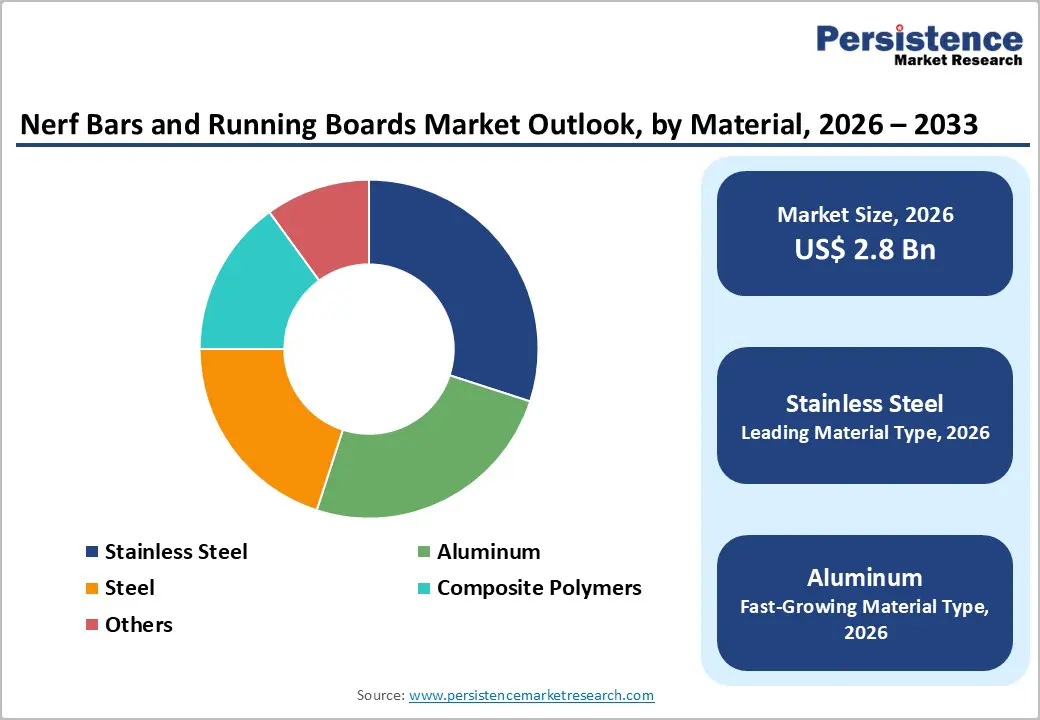

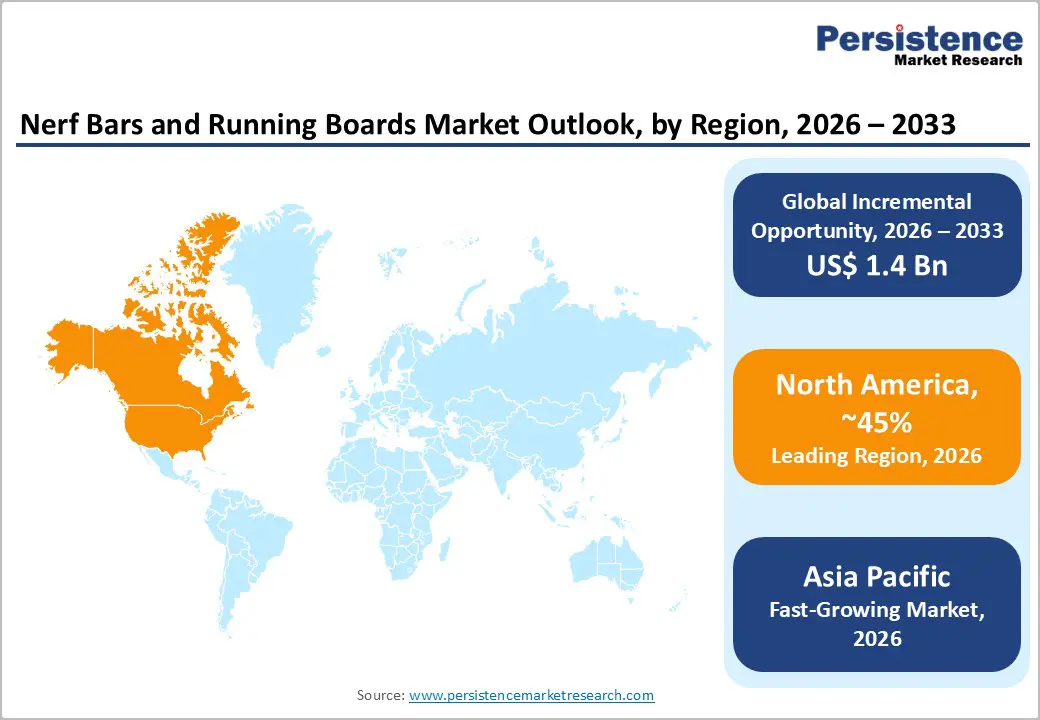

The global nerf bars and running boards market size is likely to be valued at US$ 2.8 billion in 2026, and is projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 6% during the forecast period 2026-2033.

This growth trajectory is supported by rising vehicle personalization trends, deeper penetration of sports utility vehicles (SUVs) and light trucks, and stronger demand for aftermarket accessories that improve step-in comfort and everyday usability. As global production of pickup models and SUVs has increased, fitment rates for side steps and running boards have been climbing, while the shift toward innovative, lightweight metals and composite structures has been reinforcing customer preference for higher-spec options. Growth has also been reinforced by regulatory safety expectations, as authorities in developed economies have increasingly required or encouraged assistive entry solutions on higher-clearance vehicles to protect occupants and improve accessibility for elderly or mobility-limited users. For manufacturers and channel partners, this environment has created a premium on designs that combine low weight, corrosion resistance, and integration with original equipment manufacturer (OEM) electronics, since these features have been helping automakers meet efficiency and safety objectives simultaneously.

Key Industry Highlights

- Regional Leadership: North America is projected to lead with about 45% share in 2026, driven by strong SUV and pickup truck adoption, while Asia Pacific is expected to register a 7.2% CAGR during 2026–2033, supported by rising vehicle ownership and aftermarket maturity.

- Product Type Dominance: Mechanical nerf bars and running boards are expected to dominate with 60% revenue share in 2026 due to their wide vehicle compatibility

- Fastest-growing Product Type: Electric-powered running boards are projected to grow at 8.1% CAGR through 2033, owing to the increasing adoption of premium SUVs and electric vehicles (EVs).

- Material Trends: Aluminum is forecast to exhibit the fastest growth at around 7.8% CAGR through 2033, driven by light-weighting and corrosion-resistance trends.

- Vehicle Type Outlook: Passenger cars are projected to lead in 2026, while the heavy commercial vehicles are expected to expand at a 2026-2033 CAGR of 7.5%, supported by regulatory focus on safer ingress and egress systems.

- Competitive Focus: Leading players that control the market revenue are prioritizing innovation-led strategies, with investments concentrated in electric running boards and lightweight materials, enabling growth for technology-focused portfolios.

| Key Insights | Details |

|---|---|

| Nerf Bars and Running Boards Market Size (2026E) | US$ 2.8 Bn |

| Market Value Forecast (2033F) | US$ 4.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Automotive Sales Boost Customization Demand and Accessory Adoption

The automotive aftermarket continues to be strongly influenced by the expanding light-truck vehicle base, which includes pickup trucks, SUVs, and crossover utility vehicles. More than half of all vehicles currently on the road in the United States fall into these categories, and their share continues to rise annually. This structural shift is particularly significant for the nerf bars and running boards market, as higher-ground-clearance vehicles inherently require entry-assist solutions to improve accessibility, safety, and daily usability. As light trucks transition from niche utility vehicles to mainstream personal transport, demand for functional exterior accessories increases in parallel.

Looking ahead, industry outlooks indicate that the light-truck segment is forecast to account for close to 80% of all new-vehicle sales by 2027, with pickup trucks dominating. This sustained dominance materially expands the long-term addressable market for running boards and nerf bars across both OEM installations and aftermarket upgrades. For example, the 2026 Cadillac Escalade has made power-retractable assist steps available on more trims, including Luxury, Premium Luxury, and Sport models, enhancing accessibility and luxury appeal across the lineup. As consumers increasingly customize trucks and SUVs for comfort, utility, and aesthetics, these products are evolving from discretionary upgrades into near-standard vehicle enhancements, reinforcing stable volume growth and recurring aftermarket demand.

Price Sensitivity and Rising Production Costs Limiting Market Growth

A key restraint affecting the nerf bars and running boards market growth is the gap between rising production costs and customer price tolerance. Premium materials such as aluminum and composite polymers cost 30–50% more to manufacture than conventional steel. Retail prices for advanced electric-powered or integrated step boards can reach US$ 1,000–US$ 1,500 per set, compared to US$ 400–US$ 600 for standard steel bars. This price difference limits adoption among cost-sensitive buyers in emerging markets and discourages fleet operators who prioritize lower upfront costs. Even in developed markets, higher pricing can slow premium product uptake. Balancing innovation with affordability is crucial to maintain market growth.

Raw material price volatility and supply chain uncertainty further constrain the market. Steel and aluminum costs fluctuate due to tariffs, trade restrictions, and geopolitical tensions, impacting production expenses. Smaller aftermarket manufacturers without long-term supplier agreements face heightened risk. Cost swings of 15–20% can erode profitability in low-margin segments. These factors can cause production delays, inventory challenges, and restrict competitive pricing strategies. Stabilizing input costs is therefore essential to enable broader adoption of premium running boards and nerf bars.

Electrification, Emerging Markets, and Digital Customization Driving Growth

The accelerating electrification of the automotive industry, particularly the expansion of electric pickup trucks and SUVs, is creating strong demand for advanced running boards with integrated mechanisms, sensors, and deployable features. These products not only improve accessibility but also enhance the overall user experience, aligning with the evolving design of EV platforms. Reflecting this trend, in March 2025, Westin Automotive Products partnered with AMP Research to co-develop electric-ready running boards for light trucks and SUVs, signaling how manufacturers are adapting accessory solutions to meet the functional and aesthetic needs of electrified vehicles. Such initiatives highlight the growing synergy between vehicle electrification and premium accessory adoption.

The emerging economies of Asia Pacific and Latin America are driving aftermarket growth, fueled by rising vehicle ownership and a growing middle class seeking personalization and comfort features. The rise of digital sales channels and online configurators further strengthens this opportunity by enabling buyers to customize material, thickness, and style while improving engagement and conversion rates. Thus, integrating EV-compatible products, expanding into high-growth regions, and adopting digital customization platforms create a compelling growth pathway for the nerf bars and running boards market through 2033.

Category-wise Analysis

Product Type Insights

Mechanical running boards and nerf bars are likely to remain the leading product type, accounting for approximately 65% of the revenue share in 2026. Their dominance is driven by broad compatibility with traditional pickup trucks and SUVs, simple installation processes, and established OEM and aftermarket pipelines. Mechanical boards are widely used for fleet vehicles and personal trucks where cost-efficiency and reliability are priorities. For example, standard steel fixed running boards are commonly integrated in full-size pickups such as the Ford F-150 and Chevrolet Silverado, serving both utility and commercial needs. These products are often favored in regions with high road salt usage or winter conditions, where durability is critical. The established manufacturing base and widespread adoption ensure continued revenue stability for mechanical solutions.

Electric powered running boards are the fastest-growing segment, projected to expand at roughly 8.1% CAGR from 2026 to 2033, driven by luxury and convenience features. They are increasingly integrated with high-end SUVs and emerging EV pickup platforms, such as electric versions of the Rivian R1T and Tesla Cybertruck. Automated deployment, sensor-based safety mechanisms, and remote operation enhance user experience and align with smart vehicle ecosystems. Adoption is particularly strong in premium markets where consumer’s value advanced technology and seamless integration. Rising EV adoption globally provides a growing addressable base, supporting sustained expansion for these innovative products.

Material Insights

Stainless steel is expected to remain the dominant material, holding approximately 30% of the nerf bars and running boards market revenue share in 2026. Steel provides structural strength, durability, and cost-effectiveness, while stainless steel adds corrosion resistance, especially in harsh climates. North American markets, where winter road salts and extreme weather are common, rely heavily on stainless steel for long-term performance. Standard steel running boards in mainstream pickups and light commercial vehicles illustrate the continued preference for tried-and-tested materials. These materials also allow for easier manufacturing and mass production, enabling suppliers to meet both OEM and aftermarket demand efficiently. Their reliability and established supply chains make them the preferred choice across global markets.

Aluminum is anticipated to be the fastest-growing material, forecast to achieve a 7.8% CAGR through 2033. Lightweight properties reduce overall vehicle weight, improving fuel efficiency and aligning with stricter emission standards. Composite polymers also offer high corrosion resistance and design flexibility, making them suitable for premium SUVs and EV pickups. For example, aluminum running boards are increasingly used in vehicles such as the GMC Hummer EV to combine strength with reduced weight. Growing consumer interest in sustainability and vehicle efficiency further supports this segment, creating a strong growth trajectory for innovative materials.

Thickness Insights

The 4-inch thickness segment is likely to lead the market, capturing an estimated 50% of the market revenues in 2026, due to its balance of structural support and usability for a wide range of passenger and utility vehicles. This thickness is well-suited for mainstream SUVs, pickups, and light commercial vehicles, allowing easy ingress while maintaining stability. Popular mid-size pickups like the Toyota Tacoma and Ford Ranger often use 4-inch boards for optimal ergonomics. The segment’s broad applicability across both OEM and aftermarket channels ensures steady adoption. Manufacturers continue to offer this thickness as the default for most standard vehicles, reinforcing its market share.

5- and 6-inch thickness variants are expected to be the fastest-growing, projected to display a 2026-2033 CAGR of 7%, as they accommodate larger vehicles with higher ground clearance in a more holistic manner. Full-size SUVs, premium pickups, and heavy commercial trucks benefit from deeper treads that provide safer access. Vehicles like the Chevrolet Silverado HD and RAM 3500 frequently adopt these thicker boards for heavy-duty use. Growth is also driven by consumer preference for enhanced stability and load-bearing capacity in luxury and utility models. These thicknesses are increasingly requested in aftermarket upgrades for lifted or modified trucks, thereby accelerating their adoption.

Vehicle Type Insights

Passenger cars and light commercial vehicles collectively hold the largest market share of around 70% in 2026, driven by high production volumes and widespread aftermarket adoption. These vehicles represent the bulk of SUV and pickup sales in urban and suburban areas, where accessibility and convenience features are key. Running boards for these vehicles enhance safety for families and commercial operators, providing step support for daily ingress and egress. Vehicles such as mid-size SUVs, vans, and light trucks commonly use standard mechanical boards, which are cost-effective and easy to install. The broad installed base ensures stable demand across OEM and aftermarket channels.

Heavy commercial vehicles are expected to be the fastest-growing segment, with a 7.5% CAGR through 2033, as safety regulations increasingly require assistive entry systems for tall vehicles. High-clearance trucks, construction vehicles, and long-haul commercial fleets benefit from reinforced boards and electric-powered options to meet regulatory and operational needs. For example, utility trucks in North America and Europe are often equipped with deeper, electrically deployable running boards for compliance and convenience. The combination of regulatory mandates, safety focus, and fleet modernization drives strong growth in this segment, creating new opportunities for specialized manufacturers.

Regional Insight

North America Nerf Bars and Running Boards Market Trends

North America is anticipated to command approximately 45% of the nerf bars and running boards market share in 2026, supported by a strong pickup truck and SUV culture and high aftermarket spending. The United States dominates regional demand, with light truck sales exceeding 12 million units annually, and compliance requirements for commercial fleets reinforcing accessory adoption. Safety mandates from the Federal Motor Carrier Safety Administration (FMCSA) have increased the need for reliable entry-assist solutions. Consumer preference for personalization, combined with mature distribution networks, ensures wide availability and adoption of aftermarket running boards. Investment trends show increased focus on lightweight materials and electrically integrated designs to appeal to premium segments. Popular mid-size vans and SUVs in North America also illustrate the consistent need for durable, easy-to-install solutions.

Regional growth is further propelled by technology-driven accessory innovation and fleet modernization initiatives. Programs incentivizing upgrades to commercial and government vehicles have boosted the adoption of modular and multifunctional running boards. Integration of LED step lighting, anti-slip coatings, and sensor-based mechanisms is becoming more common in fleet and private vehicles alike. These innovations, combined with strong consumer interest in customization, ensure North America will maintain a dominant market offering manufacturers and aftermarket suppliers a stable yet evolving landscape.

Europe Nerf Bars and Running Boards Market Trends

Europe is a key regional market for nerf bars and running boards, driven by rising SUV ownership and growing consumer interest in functional and aesthetic vehicle accessories. Germany, the U.K., France, and Spain lead demand, supported by well-developed aftermarket networks and high urban vehicle density. Safety-focused European Union (EU) vehicular standards encourage running board adoption for higher-clearance family SUVs, while emission and environmental regulations have increased the preference for lightweight aluminum boards. Collaborations between local specialists and global suppliers emphasize compliance, durability, and optimized material use. Urban fleets, including passenger vans and crossovers, are adopting running boards to improve safety and accessibility. High-profile launches of family-oriented SUVs in Germany and France with optional step and accessory packages further illustrate adoption trends.

Growth opportunities in Europe are particularly notable in premium SUV and light commercial vehicle segments, where consumer demand for eco-friendly, durable, and visually appealing running boards is rising. OEMs and aftermarket suppliers are increasingly investing in localized accessory manufacturing to match region-specific vehicle dimensions and design preferences. Online configurators and e-commerce platforms allow buyers to select material, finish, and feature options, improving engagement and conversion. Modular and electronically-assisted designs are gaining popularity in urban areas, reflecting a shift toward both functional and premium aesthetics. As a result, Europe is poised to remain a stable and technologically evolving market with increasing adoption of innovative, lightweight running boards.

Asia Pacific Nerf Bars and Running Boards Market Trends

Asia Pacific is slated to be the fastest-growing regional market for nerf bars and running boards, forecasted to showcase a CAGR of nearly 7.2% between 2026 and 2033, due to rapid urbanization and expanding automotive production hubs in China, India, and ASEAN countries. Growth is supported by a rising fleet of light vehicles and a developing aftermarket culture, where pickup trucks and SUVs are gaining popularity for both private and commercial use. The region benefits from lower manufacturing costs and proximity to raw materials, positioning it as a production and export hub. Emerging consumer segments in urban centers are increasingly investing in comfort and convenience features for higher-clearance vehicles. Local fleet operators and delivery companies are gradually adopting functional accessories for operational efficiency.

Further market expansion is set to be fueled by flexible regulatory environments and technology adoption, which allow innovative accessory solutions to enter the market more rapidly than in North America or Europe. Regional suppliers are developing EV-compatible running boards and products tailored to city-specific vehicle sizes, with modular and digitally configurable options for consumers. Investments in locally produced, lightweight boards also reduce costs while meeting regional demand. These factors position Asia Pacific as the market with the most lucrative opportunities, offering both high-volume adoption and innovation-driven growth potential through 2033.

Competitive Landscape

The global nerf bars and running boards market structure has achieved moderate consolidation. Leading manufacturers such as Westin Automotive, AMP Research, Dee Zee, ARIES Automotive, and Lund International have captured over 50% of global revenue. These companies have leveraged strong partnerships with OEMs, extensive aftermarket networks, and continuous product innovation to maintain their competitive edge. Their product portfolios have included electric-powered boards, deployable steps, and lightweight aluminum or composite designs that address diverse customer needs.

Regional and niche players have targeted specialized segments in emerging markets, offering cost-effective or premium solutions. Barriers such as regulatory compliance and material costs have limited new entrants, while digital customization and modular designs have enabled startups to participate. Market consolidation will have accelerated as leading brands have expanded geographically and collaborated with OEMs for next-generation products.

Key Industry Developments

- In September 2025, LEER.com added Westin’s full line of running boards and nerf bars, including the R5 Series Wheel-to-Wheel Nerf Bars, HDX Running Boards, and Signature 3 Nerf Bars, to increase market reach for premium accessories.

- In July 2025, Rugged Ridge offered platform-specific nerf bars and running boards for the 2025 Jeep Wrangler JL, highlighting its focus on tailored products for popular off-road models.

- In March 2025, Putco’s Excalibur LED Tailgate Light Bar received the award for its OEM-style fitment, multi-functional lighting, rugged durability, and DIY-friendly installation, reflecting key aftermarket trends.

Frequently Asked Questions

The global nerf bars and running boards market is projected to reach US$ 2.8 billion in 2026.

The market is driven by rising SUV and pickup truck adoption, growing aftermarket customization demand, and increasing integration with electric vehicle platforms.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Key opportunities exist in electrification, burgeoning automotive markets in Asia Pacific and Latin America, and digital customization platforms.

Leading companies include Westin Automotive Products, AMP Research, Dee Zee, ARIES Automotive, Lund International, N-FAB, Go Rhino, Putco, Husky Liners, and Access Technologies.