- Consumer Goods

- Needle Inserter Market

Needle Inserter Market Size, Share, and Growth Forecast, 2026 - 2033

Needle Inserter Market by Material (Aluminum, Stainless Steel, Others), Application (Medical, Textile, Others), and Regional Analysis for 2026 - 2033

Needle Inserter Market Share and Trends Analysis

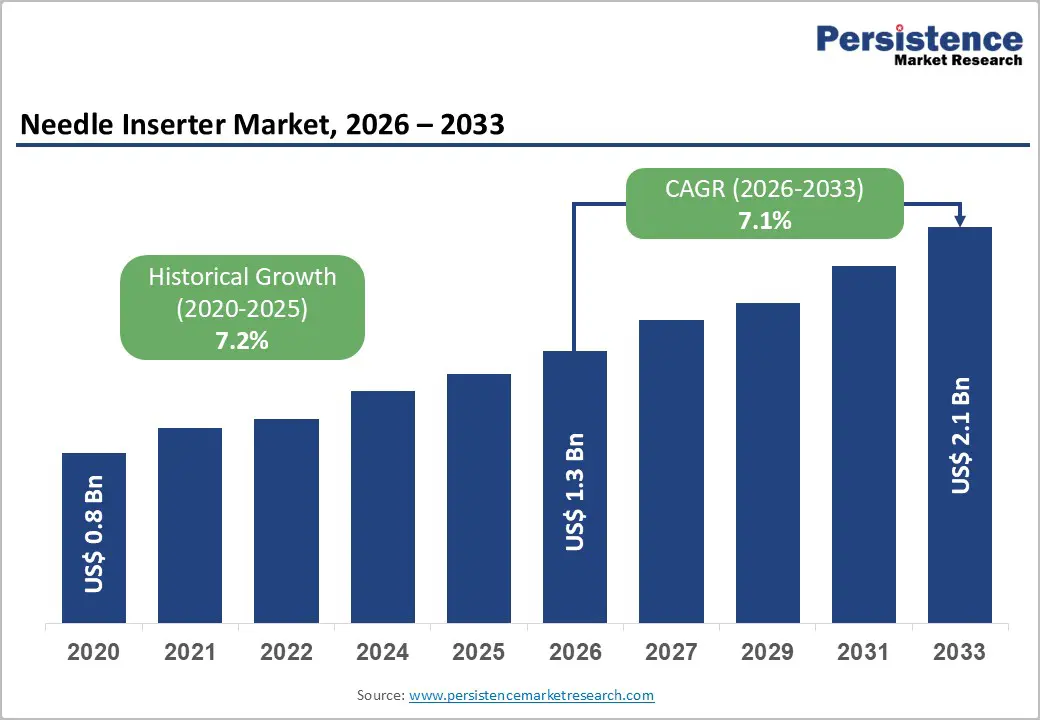

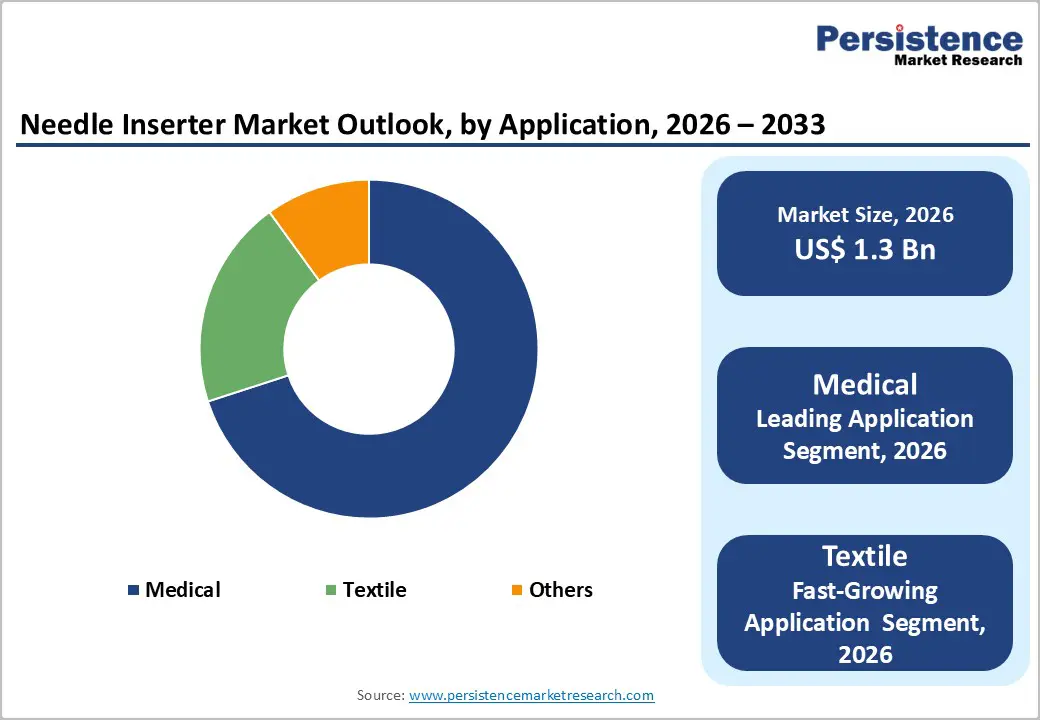

The global needle inserter market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 7.1% during the forecast period 2026 - 2033.

Market expansion is driven by rising clinical awareness and adoption of minimally invasive procedures, enhancing treatment precision and patient compliance. Increasing prevalence of chronic conditions and an aging population raises procedural volumes, supporting steady demand for needle inserters. Advanced materials and automated delivery systems improve efficiency and reduce errors, attracting healthcare providers. Growth of healthcare infrastructure in emerging economies broadens access to interventions and accelerates technology uptake. Integration with digital monitoring and imaging devices standardizes procedures and optimizes workflows, while regulatory support for safety and clinical guidelines reinforces adoption, creating a stable investment environment.

Key Industry Highlights

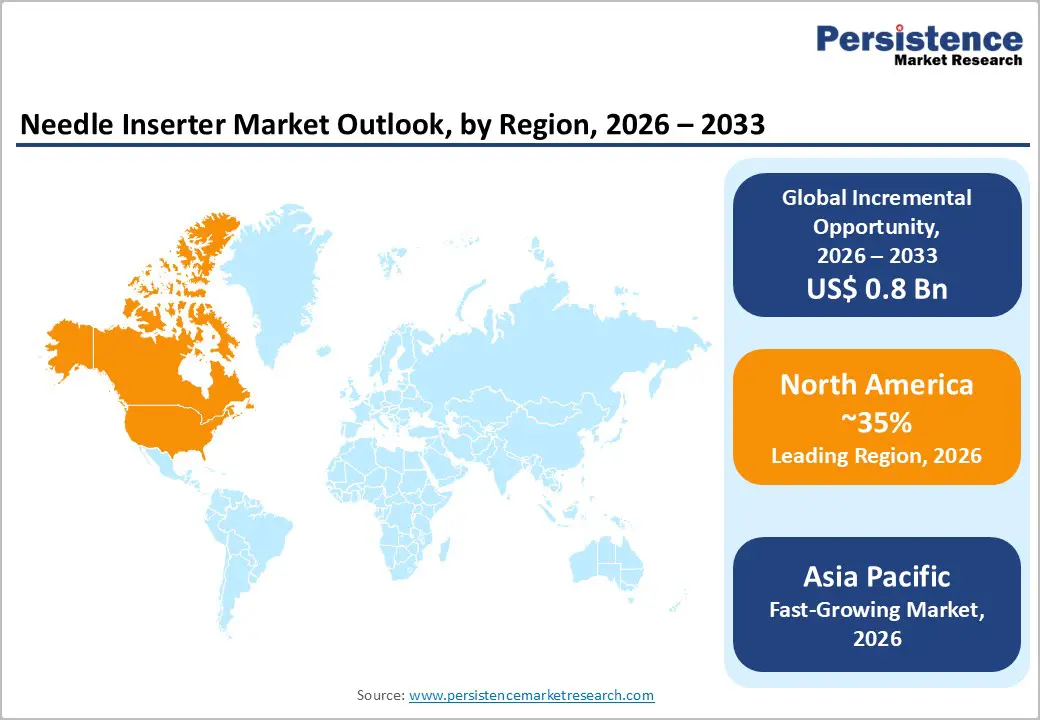

- Regional Leadership: North America is projected to lead in 2026 with roughly 35% share; Asia Pacific is expected to be the fastest-growing regional market due to infrastructure expansion, procedural growth, and favorable investment environment.

- Leading Material: Stainless steel is forecasted to hold a revenue share of about 60% in 2026, due to durability and regulatory alignment.

- Fastest-growing Material: Aluminum is expected to be the fastest-growing segment between 2026 and 2033, driven by lightweight design, ergonomic advantage, and portability.

- Leading Application: Medical is set to hold 70% of the needle inserter market in 2026, supported by high procedural volumes and regulatory facilitation.

- Fastest-Growing Application: Textile segment is forecasted to record the fastest growth between 2026 and 2033, fueled by industrial automation and emerging market expansion.

- Innovation Trends: Integration of automated systems, imaging and digital monitoring, ergonomic materials, and hybrid device applications drives adoption, operational efficiency, and clinical standardization.

| Key Insights | Details |

|---|---|

| Needle Inserter Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

DRO Analysis

Rising Demand for Automated Medical Devices

High adoption of automation technology by U.S. hospitals illustrates a structural shift toward systems that reduce labor intensity and streamline care delivery. In 2024, 71% of non-federal acute-care hospitals reported using predictive technologies integrated into electronic health records, reflecting readiness to deploy advanced tools that augment clinical and operational tasks. Administrators allocate capital to devices that improve throughput and accuracy, prompting suppliers to invest in platforms meeting safety and compliance standards. Automated needle inserters deliver repeatability, integration, and precise dosing, aligning with institutional priorities for efficiency, accuracy, and scalable deployment across diverse procedural workflows.

Operational cost pressure and staffing shortages elevate the value of automated systems in healthcare settings. Devices that lower hands-on time per procedure and standardize therapeutic workflows reduce incidence of variability and errors. Inserter systems provide consistent performance, reduce labor requirements, and enable higher throughput, addressing both operational constraints and clinical precision demands. Integration with robotics, sensors, and digital platforms supports predictive analytics and workflow optimization. Hospitals leverage these systems to maintain quality standards while managing limited resources. This alignment of efficiency, safety, and scalability strengthens adoption across acute-care, outpatient, and home-based settings, reinforcing structural demand for automation.

Growth in Chronic Disease Prevalence

Rising chronic disease prevalence drives significant procedural demand for needle inserters. In the United States, approximately three in four adults report at least one chronic disease. Conditions such as diabetes, cardiovascular disease, cancer, and autoimmune disorders require frequent injectable treatments. Expanding patient populations increase demand for devices that deliver consistent dosing, reduce clinical time, and ensure procedural safety. Adoption in outpatient, home care, and long-term care facilities grows as providers seek standardized delivery. Higher treatment volumes create operational efficiencies and reduce variability, reinforcing economic incentives for healthcare providers to integrate precision injection systems.

Patients with multiple chronic conditions face complex therapeutic regimens requiring coordinated dosing schedules. Manual injection administration introduces risks of dosage errors, timing inconsistencies, and workflow inefficiencies. Automated needle insertion systems provide repeatable, accurate delivery, reducing cognitive load for clinicians and caregivers. Enhanced procedural efficiency improves throughput, lowers labor costs, and supports adherence to prescribed therapy. Aging demographics further amplify this demand, expanding the base of patients requiring long-term injectable care. Operational reliability and safety benefits position these systems as critical solutions for managing high-volume, multi-drug treatment scenarios, and strengthening adoption across healthcare segments.

Competition from Traditional Methods

The prevalence of conventional manual syringes and injection techniques continues to restrict adoption of automated needle inserters. Low procurement cost of traditional methods allows healthcare facilities to maintain operational budgets while covering large patient volumes. Familiarity with manual techniques among medical personnel reduces the need for training investments, supporting faster patient throughput. Clinics and home care providers often prioritize simplicity and reliability over technological sophistication, especially in regions with limited resources. Established supply chains for syringes and needles create economies of scale, lowering unit costs and sustaining widespread use. Operational continuity favors proven methods with minimal maintenance requirements.

Patient trust and comfort also favor established injection techniques, shaping demand patterns across healthcare settings. Manual methods permit direct control over injection speed, depth, and angle, supporting procedural flexibility in diverse clinical scenarios. Cost-sensitive institutions may delay equipment upgrades, while high turnover of consumables maintains recurring revenue streams for suppliers. Adoption of automated systems requires procurement approvals, staff training, and integration with existing workflows, creating administrative and logistical friction. Perceived complexity and risk of technical failures further limit willingness to transition from manual approaches, constraining uptake despite technological advantages.

Complexity of Device Operation

The intricate design and operational requirements of advanced needle inserters create barriers to adoption across healthcare facilities. Medical staff require specialized training to ensure proper handling, calibration, and maintenance, increasing labor costs and administrative burden. Training cycles consume time and resources, particularly in clinics with high personnel turnover or limited technical expertise. Operational errors during initial deployment can disrupt workflow efficiency and reduce throughput in injection procedures. Procurement decisions favor devices with straightforward usability, limiting demand for systems perceived as technically demanding. Smaller healthcare providers with constrained budgets face difficulty allocating funds for skill development alongside equipment investment.

Technical complexity influences patient throughput and procedural scheduling. Systems that demand frequent adjustments or error monitoring slow service delivery in high-volume environments. Hospitals prioritize devices that integrate seamlessly with existing workflows, minimizing disruptions and reducing staff stress. Complexity can lead to increased downtime for troubleshooting and maintenance, impacting operational efficiency. The learning curve for safe, effective use constrains adoption among less-experienced practitioners, particularly in emerging markets with limited technical infrastructure. Perceived operational difficulty creates reluctance in purchasing committees, affecting capital allocation and long-term demand expansion.

Miniaturization and Portability

Compact design and transportability drive structural demand growth by enabling deployment across diverse clinical and non-clinical settings with minimal operational friction. Miniaturized devices reduce physical footprint and power requirements, allowing use in home care, mobile clinics, and point-of-care facilities. Smaller instruments lower inventory, handling, and maintenance costs, enhancing workflow efficiency in high-volume ambulatory centers. In 2025, the U.S. Centers for Disease Control and Prevention (CDC) reported that 76.4% of adults live with at least one chronic condition, intensifying demand for frequent monitoring tools manageable outside hospitals. This trend broadens the adoption base for portable, self-administered solutions.

Advances in microelectronics, sensors, and materials improve functionality and reduce production cost without compromising safety or precision. Miniaturized designs facilitate continuous monitoring, remote therapy, and integration with digital health platforms, unlocking recurring revenue through consumables and software services. Operational flexibility allows rapid deployment in rural outreach, telemedicine, and emergency response scenarios, expanding addressable markets. As adoption scales, unit economics improve, enabling penetration in cost-sensitive segments. Lightweight, compact instruments increase provider efficiency and patient convenience, supporting broader acceptance of automated needle insertion across emerging and established healthcare systems.

Integration with Telemedicine and Remote Monitoring

Wider adoption of telemedicine and remote monitoring unlocks structural demand expansion by linking digital care networks with peripheral clinical interventions such as needle insertion. Health systems in the United States integrate virtual diagnosis with follow-up device-assisted procedures, reducing logistical friction for patients and providers operating on constrained capacity. Remote monitoring delivers real-time patient data from home settings to physician dashboards, enabling more frequent touch points and proactive intervention triggers. This increases procedure throughput for clinical networks and lowers cost per episode by capturing early signs of need prior to acute exacerbation, creating operational leverage for devices tied to injection or infusion services.

Expansion of telemedicine infrastructure reduces geographic and capacity barriers that previously segmented demand toward in-person visits. Virtual triage and remote patient monitoring platforms extend clinician reach across rural and underserved urban populations, enlarging potential patient pools for ancillary procedures. Ongoing digital investment in interoperable health records and connected monitoring tools strengthens physician reliance on remote care pathways and encourages bundling of virtual consultation with adjacent intervention services. Commercial and public payer reimbursement of telehealth encounters aligns payment incentives with efficient, distributed care delivery.

Category-wise Analysis

Material Insights

Stainless steel is poised to lead with a forecasted 60% of the needle inserter market revenue share in 2026, due to its strength, corrosion resistance, and widespread clinical acceptance. Clinicians favor stainless steel inserters for reliability, precision, and compatibility with sterilization protocols. Hospitals and clinics prioritize consistent performance under rigorous use, while regulatory compliance is simplified due to established biocompatibility standards. Mature manufacturing infrastructure ensures availability and cost efficiency, and proven durability reduces maintenance and replacement needs, supporting adoption in high-volume clinical environments.

Aluminum is expected to witness the fastest growth between 2026 and 2033, driven by its lightweight characteristics, ergonomic advantages, and cost-efficiency in production. Lighter inserters reduce clinician fatigue, enhancing workflow efficiency in high-volume settings. Anodized or coated aluminum improves durability and biocompatibility, supporting minimally invasive procedures. Emerging healthcare providers and mobile clinics favor aluminum for portability, lower capital requirements, and operational flexibility. Design innovations and hybrid material integration enhance performance, while weight reduction supports adoption of automated and portable devices in clinical environments.

Application Insights

Medical applications are poised to lead with a forecasted over 70% market share in 2026, owing to increasing procedural volumes, clinician preference for precision devices, and regulatory support for minimally invasive treatments. Needle inserters are essential in hospitals, clinics, and specialty centers for drug delivery, biopsy, and diagnostics. Clinical trust in performance, standardized insertion techniques, and integration with sterilization, monitoring, and imaging systems drive adoption. Preventive healthcare initiatives, chronic disease management, and supportive reimbursement policies further stimulate utilization in established care settings.

Textile applications are anticipated to be the fastest-growing segment between 2026 and 2033, driven by rising industrial automation and specialized fabric manufacturing needs. Needle inserters enable precision stitching, embroidery, and complex fabric handling, improving efficiency and reducing manual labor. Lightweight, durable, and ergonomic designs support extended operations. Expansion in emerging economies, combined with automated and smart manufacturing, broadens the addressable market. Investment in training and digital quality monitoring further accelerates adoption, positioning textile applications as a high-growth segment with significant revenue potential.

Regional Insights

North America Needle Inserter Market Trends

North America is expected to lead with an estimated 35% of the needle inserter market share, supported by advanced healthcare infrastructure and widespread integration of precision medical devices. High procedural volumes in hospitals, outpatient clinics, and specialty centers drive consistent device utilization. Strong regulatory frameworks promote adoption of automated and minimally invasive systems, ensuring patient safety and procedural efficiency. Established procurement networks and access to capital allow healthcare providers to invest in high-performance devices. Skilled clinical personnel favor systems that offer accuracy, reliability, and compatibility with sterilization protocols, reinforcing market penetration and operational consistency across high-volume facilities.

Robust medical technology manufacturing and research ecosystems contribute to sustained dominance. Device availability, quality control, and after-sales support reduce operational downtime and maintain clinical throughput. Rising preventive healthcare programs and chronic disease management initiatives further support device demand. Integration with digital monitoring, imaging systems, and electronic health records ensures workflow efficiency and standardized procedures. Cost efficiency from mature supply chains encourages procurement at scale. Investment in clinician training and procedural standardization enhances adoption rates, enabling facilities to maintain consistent service levels and patient outcomes while leveraging advanced device capabilities.

Europe Needle Inserter Market Trends

Europe maintains a significant position in the needle inserter market, driven by established healthcare systems and high adoption of precision medical devices. Regulatory frameworks ensure device safety, performance, and compliance with sterilization standards, encouraging hospitals and clinics to integrate advanced inserters into routine procedures. High procedural volumes in specialized centers and outpatient facilities support demand. Skilled personnel prioritize devices delivering consistent accuracy, reducing patient discomfort and streamlining workflow. Mature procurement networks and access to capital enable deployment of automated systems with integration into digital monitoring and imaging platforms.

Industrial and textile sectors further support market growth through automated, high-precision operations. Needle inserters are used for embroidery, stitching, and complex fabric manipulation, enhancing efficiency and quality. Durable, ergonomic devices reduce labor intensity and support extended operational hours. Investment in workforce training, process standardization, and digital integration ensures consistent output and error reduction. Expansion of specialized manufacturing clusters and mature supply chains enables cost-effective production and timely delivery, reinforcing adoption across medical and industrial facilities.

Asia Pacific Needle Inserter Market Trends

Asia Pacific is forecasted to be the fastest-growing market for the needle inserter market between 2026 and 2033, stimulated by rapid expansion of healthcare infrastructure and rising procedural volumes. In China, investment in modern hospitals and outpatient facilities drives adoption of precision injection systems. India shows strong growth from increasing chronic disease management programs and preventive healthcare initiatives. Japan demonstrates rising integration of automation and digital monitoring in medical procedures. South Korea exhibits growth through advanced clinical technology adoption and high demand for minimally invasive treatments. Expanding skilled workforce and training programs support consistent device utilization across these countries.

Industrial and textile applications further contribute to market acceleration. Growth in automated manufacturing and smart factory implementations in China and India increases demand for needle inserters in precision stitching and embroidery operations. Japan and South Korea emphasize operational efficiency and quality control through integration of ergonomically designed, digital-enabled devices. Availability of affordable devices through local manufacturing and supply chain development reduces procurement constraints. Rising industrial output, coupled with supportive government policies for technology adoption, strengthens market scalability. Facility-level investment in workflow standardization, training, and digital integration ensures high adoption rates and sustained operational efficiency.

Competitive Landscape

The global needle inserter market is moderately consolidated, with a mix of multinational manufacturers and specialized regional players. Leading companies such as Becton Dickinson, Terumo Corporation, Smiths Medical, B. Braun Melsungen AG, and Medtronic hold an estimated 50-60% of market share, reflecting strong brand recognition, technological expertise, and established distribution networks. Competition is driven by innovation, focusing on device automation, material quality, and integration with digital monitoring or imaging systems.

Emerging players target niche applications, cost-efficient models, or regional partnerships to capture incremental segments. Operational reliability, regulatory compliance, and technological advancement remain key differentiators for procurement by hospitals, outpatient clinics, and specialty centers. Companies invest in automation, precision, and device durability to maintain market presence. Strategic focus on training, workflow integration, and digital compatibility reinforces adoption, ensuring sustained competitive positioning and incremental growth across established and emerging markets.

Key Industry Developments

- In December 2025, a novel biopsy needle integrating optical coherence tomography (OCT) that enables real-time blood vessel detection with ~97.7% accuracy, significantly reducing the risk of hemorrhage during brain procedures, was studied by researchers at the University of Adelaide. This advancement highlights a shift toward smart, sensor-integrated needle systems, directly informing the needle inserter market’s evolution toward precision-guided, safety-enhanced, and minimally invasive insertion technologies.

- In November 2025, Elevaris Medical Devices’ introduced contract development and manufacturing organization (CDMO) services and a diversified procedural needle portfolio in Europe, the Middle East, and Africa (EMEA), underscoring the growing emphasis on precision-engineered, customizable needle components for advanced medical devices. Its capabilities in micro-machining, laser processing, and cleanroom assembly support the integration of high-accuracy, automated delivery systems, reinforcing innovation in the needle inserter market focused on precision, scalability, and minimally invasive performance.

Companies Covered in Needle Inserter Market

- Becton Dickinson

- Terumo Corporation

- Smiths Medical

- B. Braun Melsungen AG

- Medtronic

- Fresenius Kabi

- Nipro Corporation

- Integra LifeSciences

- Roche Diagnostics

- Hamilton Company

- Covidien

- AccuMed Technologies

- Jiangsu Yuyue Medical Equipment & Supply

- Shanghai Microport Medical

- Braunform GmbH

Frequently Asked Questions

The global needle inserter market is projected to reach US$ 1.3 billion in 2026.

Rising demand for precision, automated injection systems in medical and industrial applications is driving the market.

The market is poised to witness a CAGR of 7.1% from 2026 to 2033.

Expansion in home healthcare, automated procedures, and emerging industrial applications offers significant growth opportunities for the market.

Some of the key market players include Becton Dickinson, Terumo Corporation, Smiths Medical, B. Braun Melsungen AG, and Medtronic.