- Specialty & Fine Chemicals

- Nanoceramic Powder Market

Nanoceramic Powder Market Size, Share, and Growth Forecast, 2025 - 2032

Nanoceramic Powder Market By Material Type (Alumina, Zirconia, Others), Application (Electronics & Electricals, Biomedical, Others), End-user Industry, and Regional Analysis for 2025 - 2032

Nanoceramic Powder Market Size and Trends Analysis

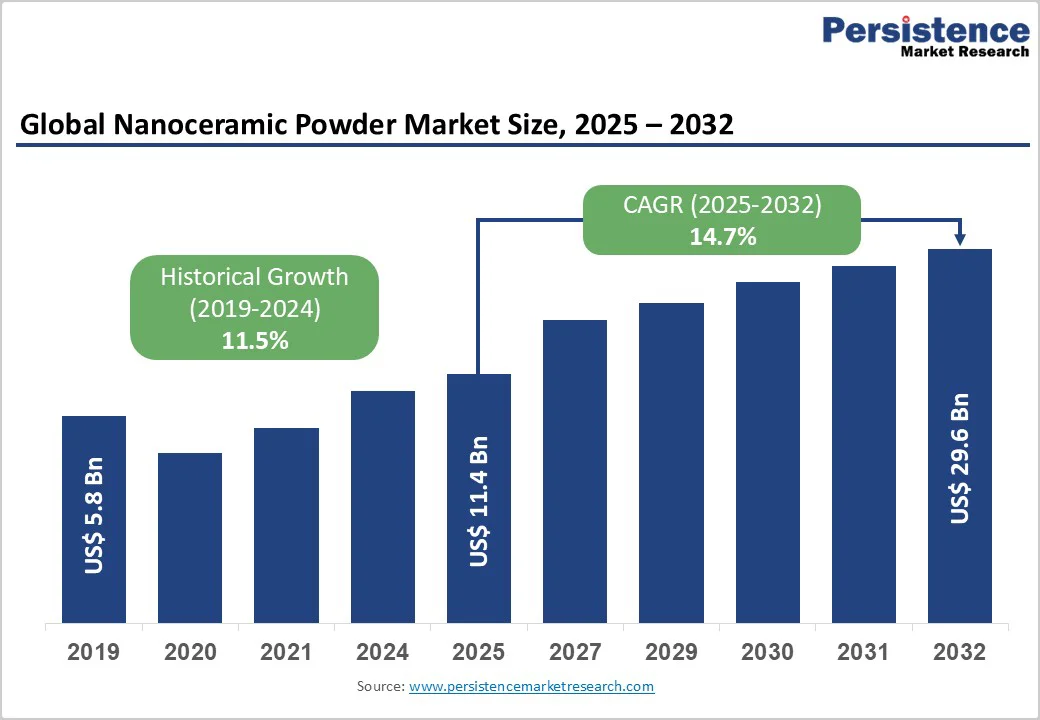

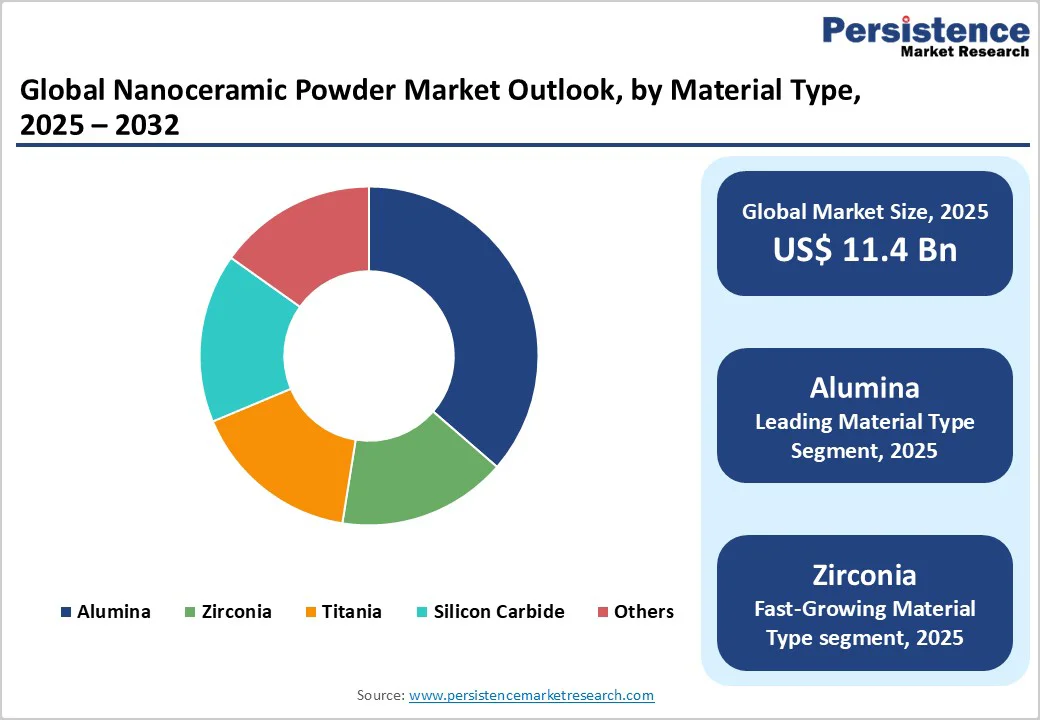

The global nanoceramic powder market size is likely to be valued at US$11.4 Billion in 2025 and is expected to reach US$29.6 Billion by 2032, growing at a CAGR of 14.7% during the forecast period from 2025 to 2032, driven by rising adoption of nanoceramic materials in electronics, automotive, aerospace, and energy sectors, coupled with advances in nanotechnology and additive manufacturing.

Rising demand for lightweight, high-strength, and corrosion-resistant materials is driving commercial adoption across semiconductor manufacturing and advanced coatings. Growing investments in green production and defense-grade ceramics are further strengthening the global engineered powders market.

Key Industry Highlights

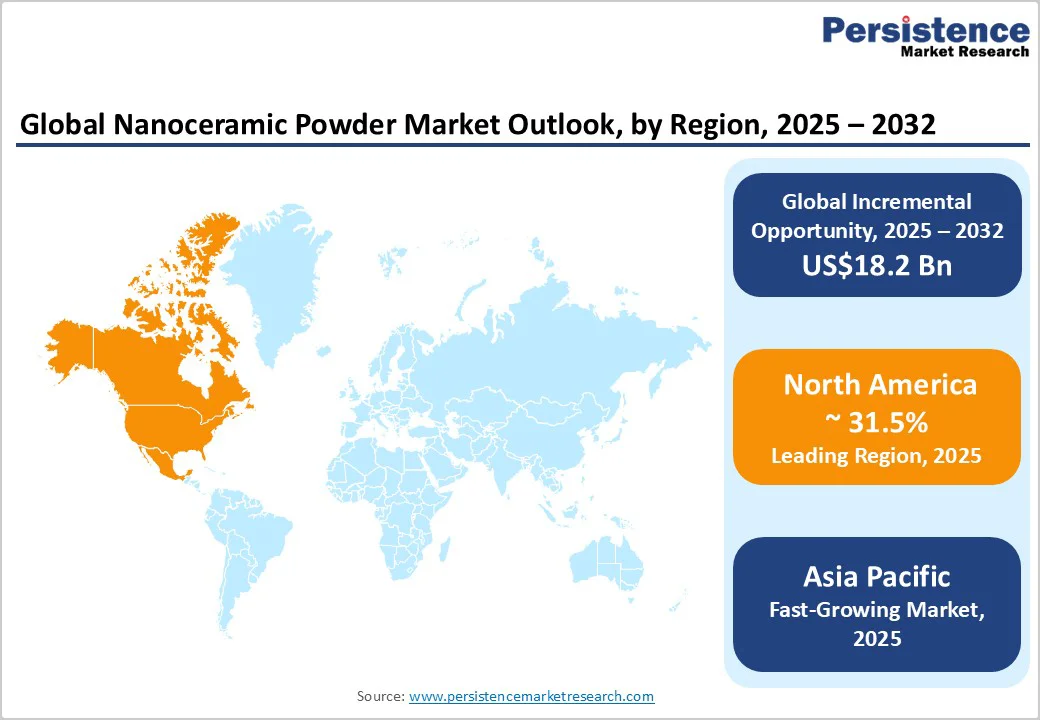

- Leading Region: North America holds the leading position with approximately 31.5% share of the global market in 2025, driven by strong aerospace, defense, and semiconductor manufacturing bases in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, fueled by large-scale industrialization in China, Japan, South Korea, and India.

- Investment Plans: Significant R&D and capacity expansion investments are underway across the U.S., Germany, and China, focusing on nanoceramic powders for solid oxide fuel cells, EV batteries, and aerospace composites, with multiple public-private partnerships advancing local production.

- Dominant Material Type: Alumina nanoceramic powders lead the material segment with over 35.8% market share in 2025, supported by their superior thermal stability and use in microelectronics and transparent ceramics.

- Leading Application: Electronics and electricals dominate the application segment, accounting for approximately 33.5% of total demand, owing to extensive use in multilayer ceramic capacitors (MLCCs), heat-resistant coatings, and semiconductor devices.

| Key Insights | Details |

|---|---|

| Nanoceramic Market Size (2025E) | US$11.4 Bn |

| Market Value Forecast (2032F) | US$29.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 14.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 11.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Advanced Electronics Manufacturing

The rapid proliferation of miniaturized electronic devices and semiconductors has significantly boosted demand for nanoceramic powders used in capacitors, sensors, and heat-resistant coatings. High-purity oxides such as alumina (Al2O3) and zirconia (ZrO2) are critical in insulating layers and thermal management systems.

With global semiconductor output expected to surpass US$1 Trillion by 2030, nanoceramic inputs are increasingly vital for achieving superior dielectric performance. This trend reinforces long-term consumption from leading chip fabrication hubs in East Asia and North America.

Rising Utilization in Aerospace and Defense Applications

Nanoceramic powders provide exceptional hardness, heat resistance, and low density, making them ideal for aerospace turbine coatings, lightweight armor, and missile nose cones.

Global defense spending exceeding US$2.4 Trillion has stimulated demand for structural ceramics and nano-engineered composites that enhance performance while reducing weight. These materials improve fatigue resistance and enable cost savings through extended service life, positioning nanoceramics as essential in next-generation aircraft and hypersonic vehicle development.

Growth in Sustainable Energy Technologies

The global shift toward renewable and sustainable energy sources has increased the adoption of nanoceramic coatings and electrolytes in fuel cells, batteries, and solar panels. Yttria-stabilized zirconia (YSZ) and ceria-based powders are key materials in solid oxide fuel cells (SOFCs) for efficient energy conversion.

As countries pursue decarbonization goals, investments in advanced energy systems are accelerating nanoceramic integration. The market’s alignment with the clean energy transition enhances its long-term resilience and investment appeal.

Barrier Analysis - High Manufacturing and Processing Costs

The synthesis of nanoceramic powders involves sophisticated chemical routes such as sol-gel, co-precipitation, and hydrothermal processing, demanding stringent quality control and costly equipment. These complexities increase the overall price, restricting small-scale adoption in cost-sensitive industries. Limited scalability further challenges mass production, creating dependency on specialized suppliers for high-purity grades.

Supply Chain Volatility and Raw Material Dependency

The production of high-performance nanoceramics relies on rare or refined oxides, whose supply is concentrated across limited geographic regions. Fluctuations in zirconium and aluminum oxide prices, coupled with export restrictions or environmental regulations, pose risks to material availability. These factors contribute to pricing volatility and can delay product delivery for downstream manufacturers.

Opportunity Analysis - Expansion of Additive Manufacturing and 3D Printing

Nanoceramic powders are emerging as key materials in additive manufacturing, particularly for high-temperature and wear-resistant components. The adoption of nano-reinforced ceramic inks and sintering technologies is opening opportunities across automotive tooling, biomedical implants, and energy components. The 3D printing ceramics segment is projected to surpass US$1 Billion by 2030, offering lucrative integration pathways for nanoceramic suppliers.

Growing Investments in Biomedical Applications

Nanoceramic powders such as hydroxyapatite and zirconia are gaining prominence in orthopedic and dental implants due to their superior biocompatibility and mechanical strength. Global healthcare modernization and rising implant surgeries, exceeding 4 million procedures annually, are creating a robust market for bio-nanoceramics. Research on nano-scale surface modification is expected to enhance osseointegration and reduce infection rates, supporting premium pricing and clinical adoption.

Emerging Applications in Environmental and Catalytic Systems

Nanoceramics offer catalytic and photocatalytic capabilities for water purification, pollutant degradation, and hydrogen generation. Governments prioritizing sustainable technologies are promoting investments in nanoceramic-based catalytic converters and environmental sensors.

Category-wise Analysis

Material Type Insights

Alumina (Al2O3) leads the market, accounting for over 35.8% of revenue in 2025. Its dominance is attributed to exceptional hardness, high melting point, electrical insulation, and corrosion resistance, making it indispensable in high-performance applications. In microelectronics, nano-alumina enhances thermal management and reliability in semiconductor substrates, chip carriers, and heat sinks.

It is also extensively used in aerospace turbine components, ballistic armor, and wear-resistant industrial coatings. Emerging developments in transparent alumina ceramics, used for optical windows and laser systems, further reinforce its market leadership. Manufacturers are refining sub-100 nm particle size distributions to improve sintering, surface area, and dispersion in composite matrices.

Zirconia (ZrO2) represents the fastest-growing nanoceramic segment, driven by its superior fracture toughness, ionic conductivity, and chemical inertness. It is increasingly utilized in dental restorations, biomedical implants, oxygen sensors, and solid oxide fuel cells (SOFCs). In dentistry, nano-zirconia replaces metal and polymer alternatives for crowns, bridges, and prosthetics due to its biocompatibility and aesthetic translucency.

In energy applications, yttria-stabilized zirconia (YSZ) enhances SOFC performance and temperature resilience. Advances in dopant modification, using yttria, magnesia, or Scandia, have improved structural stability, enabling use in thermal barrier coatings and hydrogen sensors. With rising electrification and medical innovation, zirconia nanoceramics are set for robust global adoption.

Application Insights

The electronics and electrical segment dominates the market, accounting for about 33.5% of total consumption in 2025. Materials such as alumina, titania, and barium titanate are widely used in multilayer ceramic capacitors (MLCCs), chip substrates, sensors, and thermal barrier coatings. These nanoceramics provide superior dielectric stability, heat resistance, and miniaturization, enabling high-performance compact circuits and integrated devices.

The rapid expansion of 5G networks, Internet of Things (IoT) infrastructure, and automotive electronics is driving demand for nano-engineered insulating materials. For example, barium titanate nanoceramics are increasingly utilized in high-energy-density capacitors that power electric vehicles and smart devices.

Rising consumer electronics production in China, Japan, and South Korea further accelerates market growth, while European manufacturers employ nanoceramics in advanced PCB insulation and high-frequency radar sensors for connected mobility.

The biomedical and healthcare segment is the fastest-growing, propelled by innovations in tissue engineering, orthopedic implants, and dental prosthetics. Nanoceramic powders such as hydroxyapatite, zirconia, and bioactive glass are valued for their biocompatibility, strength, and osteoconductive properties.

Applications include nano-hydroxyapatite coatings for titanium implants, zirconia-based dental crowns, and titania ceramics for antibacterial surfaces. The convergence of nanotechnology and regenerative medicine positions biomedical nanoceramics as a critical growth frontier worldwide.

Regional Insights

North America Nanoceramic Powder Market Trends - Defense, Aerospace, and Clean-Energy Innovation Drive Market Leadership

North America accounts for around 31.5% of the nanoceramic powder market in 2025, with the U.S. as the principal contributor. The market benefits from strong investments in aerospace, defense, and semiconductor manufacturing, where nanoceramic materials are utilized in turbine coatings, thermal barriers, and chip substrates.

The U.S. Department of Defense continues to prioritize advanced ceramic composites for armor and propulsion systems, while major aerospace OEMs are integrating nano-engineered thermal coatings to extend engine life and improve fuel efficiency.

R&D initiatives across institutions such as the National Nanotechnology Initiative (NNI) and industry-led projects in Silicon Valley and Texas are boosting domestic innovation and patent activity in oxide and non-oxide nanoceramics. In 2024, several U.S.-based materials producers expanded production lines for yttria-stabilized zirconia (YSZ) powders used in solid oxide fuel cells (SOFCs) and battery separators, aligning with the nation’s clean-energy objectives.

Canada is also emerging as a secondary hub, focusing on nanoceramic coatings for mining equipment and industrial heat exchangers. Favorable regulatory frameworks emphasizing environmental compliance and materials safety further strengthen the region’s global leadership position.

Europe Nanoceramic Powder Market Trends - Sustainable Manufacturing and Hydrogen Economy Propel Advanced Ceramic R&D

Europe is supported by an extensive industrial ecosystem spanning aerospace, automotive, and renewable energy applications. Leading economies such as Germany, France, the U.K., and Spain contribute significantly through high-value engineering and materials research. The region’s commitment to sustainability and eco-efficient manufacturing is driving the adoption of low-emission ceramic synthesis and closed-loop recycling processes.

European energy transition programs, including the EU Hydrogen Strategy, are fostering large-scale deployment of nanoceramic electrolytes in hydrogen fuel cells and electrolyzers. In 2024, several collaborative projects between universities and advanced materials firms in Germany and the Netherlands introduced nano-zirconia-based coatings for high-temperature turbine applications, aiming to reduce carbon footprints in power generation.

The U.K. has invested in nanoceramic additive manufacturing powders to strengthen local aerospace supply chains. France’s research centers are also exploring nanostructured alumina for electric vehicle components to improve heat dissipation and mechanical strength. With strong public-private R&D partnerships and adherence to the European Green Deal, Europe continues to evolve as a hub for next-generation ceramic innovation and sustainable production.

Asia Pacific Nanoceramic Powder Market Trends - Industrial Expansion and Government Support Power Global Nanoceramic Production Hub

Asia Pacific remains the fastest-growing regional market, supported by rapid industrialization, infrastructure expansion, and technological advancements in China, Japan, South Korea, and India. The region benefits from cost-effective manufacturing, abundant raw materials, and government-backed innovation programs, which together underpin its competitive advantage in the nanoceramics domain.

China leads global nanoceramic production, fueled by increasing demand in electronics, automotive, and renewable energy sectors. In 2025, major Chinese firms announced capacity expansions for nano-alumina and nano-silica to meet growing domestic requirements in EV battery separators and chip substrates. Japan continues to lead in precision and biomedical ceramics, where companies are developing ultra-fine zirconia powders for dental implants and solid oxide fuel cells.

In India, government initiatives such as the ‘Make in India’ and ‘Defence Production & Export Promotion Policy’ are encouraging localized manufacturing of nanoceramic composites for defense armor and aerospace applications. The country’s emerging semiconductor ecosystem is also driving demand for nano-alumina substrates in high-performance microelectronics.

Regional expansion of renewable energy projects and the establishment of dedicated nanomaterials research parks in South Korea and Taiwan further position Asia Pacific as the epicenter of nanoceramic powder innovation, production, and application diversification.

Competitive Landscape

The global nanoceramic powder market is moderately consolidated, with the top ten players accounting for approximately 55% of the global share. Competition centers on product purity, particle size control, and sintering performance. Global producers focus on high-value applications in defense, healthcare, and energy. Strategic vertical integration of raw materials and powder fabrication improves supply stability and pricing control.

Industry leaders are focusing on innovation-driven expansion, advanced material engineering, and precision processing. Strategic alliances between manufacturers and research institutions are key to accelerating product customization and enhancing global competitiveness.

Key Industry Developments

- In April 2025, a global advanced materials firm announced release of a new yttria-stabilized zirconia nanopowder designed for solid oxide fuel cells and next-gen thermal barrier coatings, aiming to strengthen its foothold in clean-energy and aerospace materials segments.

- In June 2024, a European ceramics manufacturer acquired a regional nanopowder specialist to bolster its additive-manufacturing powder portfolio and accelerate entry into thermal-spray and nano-coating markets for electronics and automotive.

Companies Covered in Nanoceramic Powder Market

- Saint-Gobain S.A.

- 3M Company

- CeramTec GmbH

- Kyocera Corporation

- Nanophase Technologies Corporation

- Showa Denko K.K. (Resonac Holdings Corporation)

- Tosoh Corporation

- Advanced Nano Products Co., Ltd.

- Materion Corporation

- Merck KGaA

- NANOFRONTIER TECH Co., Ltd.

- Baikowski SAS

- Sigma-Aldrich (MilliporeSigma)

- American Elements

- Innovnano - Nanostructured Materials S.A.

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd.

- Fineway Inc.

- Inframat Advanced Materials LLC

- PlasmaChem GmbH

Frequently Asked Questions

The global nanoceramic powder market size in 2025 is estimated at US$11.4 Billion.

By 2032, the nanoceramic powder market is projected to reach US$29.6 Billion.

Key trends include growing use of nanoceramics in fuel cells and energy storage systems, rising deployment in semiconductor fabrication, and expanding applications in medical implants, armor systems, and EV batteries.

The alumina nanoceramic powder segment leads the market, accounting for over 35.8% of the global revenue in 2025, due to its high thermal stability and electrical insulation properties.

The nanoceramic powder market is expected to grow at a CAGR of 14.7% from 2025 to 2032.

Major players include Saint-Gobain S.A., 3M Company, CeramTec GmbH, Kyocera Corporation, and Nanophase Technologies Corporation.