- Travel and Tourism

- Music-Tourism Market

Music-Tourism Market Size, Share, Trends, Regional Analysis, 2026 to 2033

Music-Tourism Market by Event Type (Concerts, Festivals, Music Awards & Ceremonies, Nightlife & Club Music Events, Others), Age Group (Below 18 Years, 18–34 Years, 35–54 Years, 55 Years & Above), Booking Mode (Direct Booking, Online Travel Agencies (OTAs), Event Organizer Platforms, Travel Agents/Tour Operators), and Regional Analysis 2026–2033

Music Tourism Market Trends & Analysis

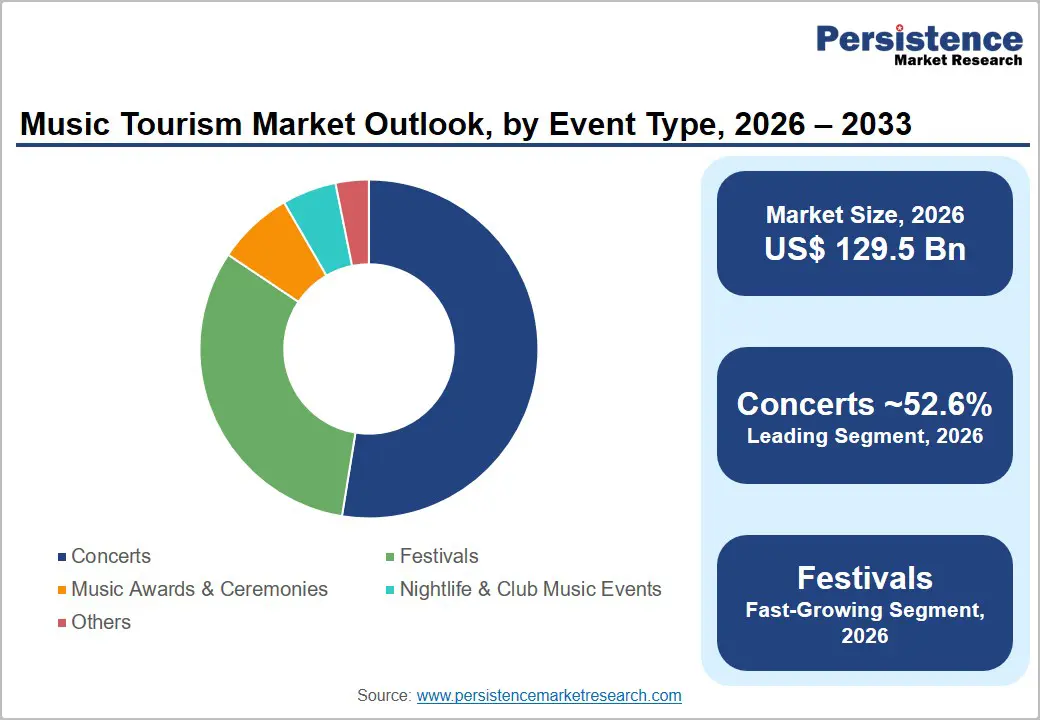

The global music tourism market size is projected at US$129.5 billion in 2026 and is projected to reach US$363.8 billion by 2033, growing at a CAGR of about 15.9% between 2026 and 2033. Demand is underpinned by the shift from goods to experience-led travel, with global travel and tourism already contributing nearly US$11.6 trillion to world GDP and expanding faster than the overall economy.

Cultural and creative tourism represents around 40% of international trips, with music festivals and events a core part of “intangible” cultural experiences. The rise in participation of 18–34-year-olds constitutes around 60% of festival audiences, and the fact that more than half of festivalgoers now travel over 100 miles for events positions music as a structured tourism driver rather than a secondary trip add?on. Digital booking, cashless payments, and integrated travel–event packages are accelerating ticket conversions and ancillary spend, while government cultural funding and destination-branding initiatives further support medium?term growth.

Key Industry Highlights:

- Experiential Shift: Around 40% of international tourists now travel for culture, and festivals already account for more than 30% of event?tourism value, structurally embedding music within the wider tourism economy.

- Segment Leaders: Concerts dominate event?type revenues with a 52.6% share, while festivals are the fastest?growing format supported by mega?events regularly attracting 400,000+ attendees.

- Youth Core: The 18–34 age group roughly holds 64.4% of music?tourism demand and is growing at an estimated 16.9% CAGR, driven by experiential preferences, social?media influence and higher propensity to travel for events.

- Digital Dominance: Online Travel Agencies and event platforms capture most bookings, as over 90% of festival tickets are bought digitally and cashless systems can lift per?attendee spend

- Strategic Moves: Post?2023, multi?year concert?travel alliances in Asia, acquisitions of Latin?American promoters, destination?experience partnerships in Las Vegas, and expanded public cultural funding (e.g., Canada Music Fund) are reshaping music?tourism supply and packaging.

Market Dynamics Analysis

Drivers - Experiential & Cultural Tourism Mainstreaming

UN Tourism and European market evidence indicate that about 40% of international tourists travel primarily for cultural experiences, with Europe alone holding roughly 39% of global cultural tourism flows. Within this, “intangible” culture- festivals, music events, and live performances- is gaining share over traditional sightseeing as travelers seek immersive and authentic experiences that connect them to local communities. This structural preference is aligned with broader trends: global tourism GDP has rebounded strongly, reaching US$11.6 trillion in 2025 and nearly 10% of global GDP, demonstrating the spending power available for high?value niches like music tourism.

For music tourism - concerts, destination festivals and music-themed city weekends are increasingly becoming the primary purpose for travel. Destinations are using music events to extend seasons, regenerate urban districts and differentiate culturally can capture a disproportionate share of long?haul and repeat visitors.

Digitalization of Booking, Payments and Trip Packaging

Across live events, over 90% of festival tickets are now purchased digitally, and mobile has become the default path to purchase. Digital adoption extends beyond ticketing: 65% of festivalgoers use mobile ticketing, cashless and RFID solutions can increase per?attendee spend by 15–30%, and more than half of consumers say they are more likely to attend if instalment or “buy?now?pay?later” options are available. These capabilities reduce friction in cross?border purchases, enable price tiering and upselling, and bring music?tourism products in line with mainstream online travel expectations.

Integrated travel–event packaging is now emerging as a dedicated growth lever. A multi?year partnership between Live?entertainment platforms and major online travel groups in Asia, for example, combines concert presales with flights, hotels and curated local experiences across markets such as Hong Kong, Singapore, Thailand, South Korea and Mainland China. Airline and hotel tie?ups that embed festival access into loyalty journeys further normalize music?driven trip planning. These developments expand average revenue per traveler and make the music?tourism offer more “trip?like” than ticket?like, materially supporting volume and yield.

Restraints - Capacity, Overtourism and Event Infrastructure Constraints

Music tourism concentrates visitors in specific locations and time windows, intensifying pressure on venues, transport networks and city infrastructure. Cultural?tourism analysis highlights overtourism and congestion at popular destinations as escalating risks, particularly where large?scale festivals overlap with heritage or high?density urban areas. Limited venue capacity, crowd?management regulations and neighbourhood opposition can cap ticket volumes and restrict new event approvals. For destinations, this structurally constrains peak?season growth and increases the importance of dispersal strategies, off?season programming and smaller “micro?events” to maintain expansion without triggering social and political backlash.

Affordability, Regulation and Youth Spending Power

Despite strong demand, affordability remains a critical barrier. Polling among younger audiences shows cost is the most commonly cited reason for not attending more events, with many indicating that subsidies or cultural vouchers would significantly increase their participation. At the same time, festival ticket prices have been rising by around 8% annually, reflecting production inflation and premiumization trends. Combined with visa, insurance and travel?cost volatility, this can slow international music?tourism growth, especially from emerging markets. Regulatory tightening on safety, environmental impact and secondary ticketing, though essential, can add compliance costs and complexity, discouraging marginal organisers and constraining supply elasticity.

Opportunities - Deepening Monetization through Premium, Hybrid and Themed Experiences

Experience?economy trends show strong willingness to pay for premium and transformative events, with over 65% of consumers seeking experiences that improve their lives or wellbeing and a growing share prioritizing mental?health and “reset” benefits from festivals. At the same time, VIP and premium ticket sales in major festivals have grown by around 20%, merchandise spend per attendee continues to rise, and travel and accommodation can account for nearly 40% of total festival outlay. This creates a multi?layered monetization canvas extending beyond base tickets into hospitality, wellness, creative workshops and local cultural add?ons.

For music?tourism stakeholders, “festival plus” products, such as music cruises, resort?based destination events and city?wide music weeks, offer clear uplift opportunities. Live?entertainment companies are already piloting destination?experience brands and hotel partnerships in Las Vegas and other hubs to package lodging, pool parties and curated performances for international visitors. Combined with digital engagement (apps, AR/VR content, loyalty communities), this enables yield management across the entire journey and can significantly increase revenue per music tourist compared with stand?alone concert trips.

Policy Support, Cultural Funding and Sustainable Tourism Frameworks

Governments are increasingly recognizing festivals and live music as levers for cultural diplomacy, regional development and youth employment. For example, Canada’s 2024 federal budget allocates over US$1 billion equivalent for arts, culture and heritage over five years, including US$31 million for arts festivals and performing?arts presenters and US$32 million specifically for the Canada Music Fund to develop and promote artists. Similar initiatives in Europe and Asia integrate music and cultural events into heritage?tourism and city?branding strategies, often with infrastructure co?funding and skills programmes for local communities.

In parallel, frameworks from UNESCO’s World Heritage and Sustainable Tourism Programme and destination?level cultural?tourism guidelines formalize best practice around crowd management, community participation and climate resilience. Players that align music?tourism offerings with such policies, emphasizing sustainability, local inclusion and heritage conservation, can secure access to grants, favourable permitting and public?private investment platforms. Given the projected US$363.8 billion market size by 2033, even capturing a modest share of policy?linked projects constitutes a multi?billion?dollar addressable opportunity for promoters, DMCs, ticketing platforms and destinations.

Category-wise Analysis

Event Type Insights

The concerts segment leads with an estimated 52.6% share, significantly ahead of festivals, awards ceremonies, nightlife events and other formats. Concert tours by global headliners concentrate demand in major city venues and stadiums, attracting both domestic and international visitors who combine shows with short?break tourism. Festivals, however, are gaining strategic ground as governments and DMOs increasingly prioritize multi?day events for regional promotion and seasonal balancing, suggesting a gradual rebalancing of the mix over the long term.

Festivals are the fast?growing event type, expected to expand at around 16.7% CAGR, supported by destination festivals that regularly attract 400,000+ attendees and by the fact that festivals now account for roughly one?third of the global event?tourism economy. Growth is reinforced by strong digital engagement, rising sponsorship revenue and the ability to bundle camping, hospitality and cultural programming into multi?day packages.

Age Group Insights

The 18–34 Years segment is the clear age?group leader in music tourism with approximately 64.4% market share, reflecting its dominance in festival attendance, social?media influence and willingness to travel long distances for live events. Youth?travel research indicates that this cohort is more likely to seek immersive experiences, travel internationally and participate in multiple trips per year, amplifying its share of both ticket and ancillary tourism spending. Other age groups, particularly 35–54 years, contribute meaningfully to premium, higher?spend segments but remain structurally smaller in volume.

The 18–34 age group is also fast?growing, with an estimated 16.9% CAGR, underpinned by rising middle?class incomes in Asia, the normalization of event?led leisure travel, and strong alignment with digital discovery and booking channels. Gen Z is reported to be up to 3x more likely to attend live events than older cohorts and is particularly responsive to hybrid physical–digital experiences and values?driven festivals, supporting sustained growth in this age band.

Booking Mode Insights

Online Travel Agencies (OTAs) represent the leading booking mode, accounting for an estimated 55.8% share of music?tourism bookings as travellers increasingly expect to search, compare and purchase flights, accommodation and event tickets within unified digital environments. OTAs benefit from high traffic, multi?product packaging capabilities and strong mobile penetration, making them the default choice for many cross?border festival and concert trips. Direct booking, event?organiser platforms and travel agents remain relevant but structurally smaller, often focusing on niche or premium packages.

OTAs are also the fast?growing booking channel, with an anticipated 17.3% CAGR as concert?travel partnerships integrate presale access, flights and hotels on a single platform across multiple Asian and Western markets. As over 90% of tickets are now sold digitally and instalment payments become more common, the OTA and event?organiser platform ecosystem will capture most incremental growth, while offline channels shift toward customized or high?touch itineraries.

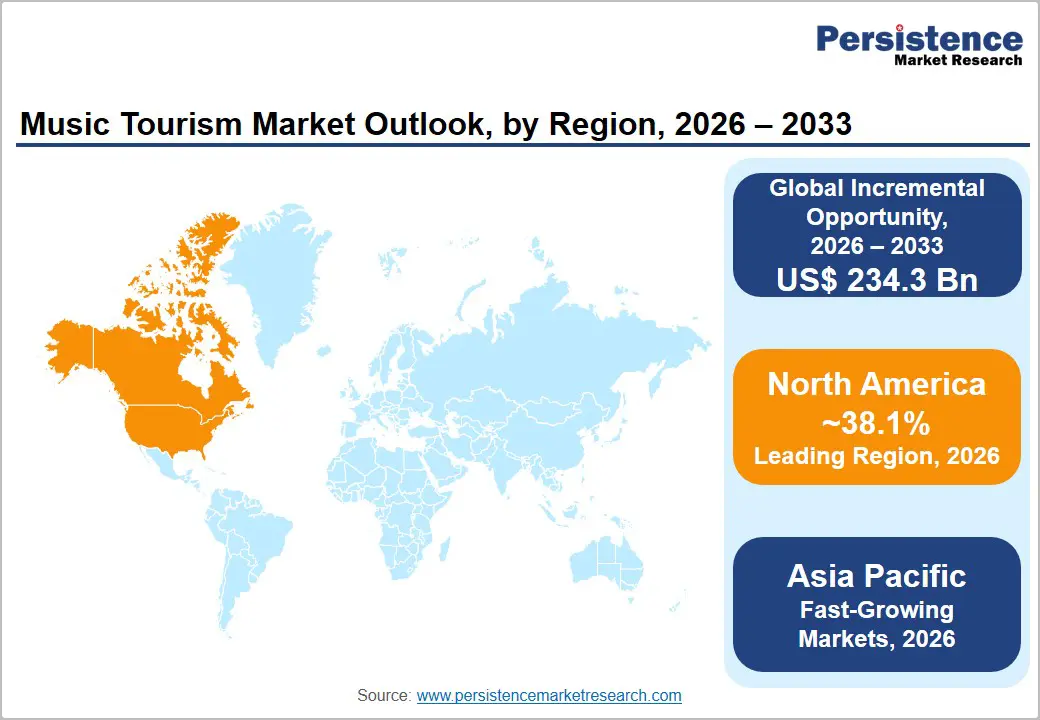

Regional Market Insights

North America Music Tourism Market Insights

North America’s vastness is supported by high per-capita incomes, a dense network of venues, and globally recognized festivals. This region accounts for approximately 38.1% of global music-tourism revenues, with the United States making up the vast majority of demand.

U.S. Music?Tourism Market

The U.S. Music?Tourism Market is estimated at roughly US$40.7 billion, supported by a rich live?music legacy, destination festivals such as Coachella and large?scale touring circuits across major metros. Projections indicate continued growth to well above US$100 billion by the early 2030s, supported by festivalization, premium offerings and strong domestic and inbound demand.

Beyond the U.S., Canada contributes meaningfully through city?based festivals and robust federal cultural funding, including increased budgets for festivals, performing arts and the Canada Music Fund, which together support content creation and the event ecosystem. Emerging hubs such as Toronto, Montreal and Vancouver are leveraging music events for urban regeneration and international branding, while regulatory frameworks emphasize sustainability, accessibility and community participation.

Europe Music Tourism Market Insights

Europe commands an estimated 28.4% share of the global music?tourism market and is the world’s largest cultural?tourism region, with nearly 40% of global culture?oriented international tourists. Pan?European rail connectivity, dense festival calendars and heritage cities underpin strong intra?regional visitor flows for concerts and festivals

Germany Music?Tourism Market

The Germany Music?Tourism Market is estimated around US$9.2 billion, driven by a mix of large urban events, open?air festivals and strong outbound travel to music destinations worldwide. Germany’s role as both source and host market, coupled with high disposable incomes and cultural?exchange programmes, supports continued mid?teens growth in music?tourism?related spend.

Other key European contributors include the U.K., France and Spain with strong domestic festival brands and high cultural?tourism participation rates, often exceeding 40% of outbound travellers engaging in culture?related activities. European Union sustainability frameworks and UNESCO heritage policies increasingly shape event licensing, capacity limits and destination?management strategies, pushing organisers toward greener and more community?integrated music?tourism models.

Asia Pacific Music Tourism Market Insights

Asia Pacific is the fast?growing region, estimated to rise at a positive CAGR and regional revenues projected to more than triple in the years ahead. Demographic depth, rapid urbanization and rising disposable incomes underpin both domestic and cross?border concert travel, particularly around K?Pop, J?Pop and regional festival brands.

China & India Music?Tourism Market Trends

China’s music?tourism market is estimated at roughly US$12.9 billion, with large?scale arena tours, city festivals and cross?border K?Pop events driving outbound and inbound flows. India’s market is smaller in absolute terms, around US$8.2 billion, but benefits from an exceptionally young population and rise in international festival footprint.

Beyond China and India, Japan and ASEAN destinations (such as Thailand, Singapore and Indonesia) are increasingly positioned as regional music hubs, leveraging integrated travel packages and multi?year partnerships between live?entertainment companies and major online travel agencies. Governments in several Asia Pacific markets are tying festivals to broader tourism strategies, using them to promote cultural heritage, attract high?spending visitors and stimulate creative?economy employment.

Competitive Landscape

The global music tourism Market is moderately consolidated at the global platform level but fragmented at destination and event?organiser level, as a few large live?entertainment and ticketing groups control global touring and ticket distribution while thousands of independent festivals and regional promoters operate locally. Key differentiators include global artist relationships, integrated ticketing and sponsorship platforms, data?driven marketing, destination partnerships and the ability to bundle travel, hospitality and experiences into seamless packages.

Strategic themes centre on innovation in experience design, expansion into high?growth geographies (especially Asia Pacific and Latin America), and digital monetization, alongside cost discipline in production and logistics. Leaders increasingly pursue ecosystem strategies, combining ticketing, promotion, sponsorship and travel partnerships, to capture a larger share of the music?tourism value chain.

Strategic Developments:

- In March 2024, AEG Presents partnered with Cárdenas Marketing Network (CMN) to establish a global Latin music touring powerhouse. This partnership enables expanded cross-border touring, enhances festival offerings, and leverages AEG's global resources with CMN's expertise to boost Latin music's international presence.

- In May 2025, Live Nation Entertainment acquired SD Concerts, the leading Dominican Republic concert promoter, strengthening its Latin American footprint through expanded event operations, venue access, and Ticketmaster integration to enhance regional music tourism and ticketing capabilities.

- In October 2025, Trip.com Group and Live Nation Asia launched a multi-year partnership to formalize concert-travel packages across key Asian markets, including Hong Kong, Macau, Singapore, Thailand, South Korea, and Mainland China. This collaboration allows fans to secure exclusive presale concert tickets bundled with flights, accommodation, and curated local attractions to boost entertainment-led tourism.

Global Music Tourism Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 58.1 Bn |

| Current Market Value (2026) | US$129.5 Bn |

| Projected Market Value (2033) | US$363.8 Bn |

| CAGR (2026–2033) | 15.9% |

| Leading Region | North America – 38.1% |

| Dominant Event Type | Concerts – 52.6% |

| Top?ranking Product | Online Travel Agencies (OTAs) – 55.8% |

| Incremental Opportunity | ~US$ 234.3 Bn |

Companies Covered in Music-Tourism Market

- Live Nation Entertainment

- AEG Presents

- Ticketmaster Entertainment

- Eventbrite

- StubHub

- Vivid Seats

- Songkick

- Bandsintown

- Festicket

- VenuWorks

- Percept Limited

- Trip.com Group

Frequently Asked Questions

The global music tourism market is estimated at around US$129.5 billion in 2026, projected to reach about US$363.8 billion by 2033.

Growth is driven by experiential and cultural‑tourism demand, youth‑centric festival attendance, digital ticketing and travel packaging, and supportive cultural‑funding and destination‑branding policies worldwide.

Between 2026 and 2033, the market is expected to grow at an estimated CAGR of about 15.9%, outpacing general tourism and leisure sectors.

The most attractive opportunities lie in Asia Pacific’s high‑growth markets, premium and themed destination experiences, digital cashless ecosystems, and public–private initiatives that link music events with cultural, heritage and sustainable‑tourism agendas.

Key players include Live Nation Entertainment, AEG Presents, Ticketmaster, Eventbrite, StubHub, Vivid Seats, Songkick, Bandsintown, Festicket, VenuWorks, Percept Limited and Trip.com Group’s concert‑travel partnerships, spanning promotion, ticketing and travel integration.