- Media & Entertainment

- Music Streaming Market

Music Streaming Market Size, Share, and Growth Forecast 2026 – 2033

Music Streaming Market by Type of Streaming (Live Streaming and On-Demand Streaming), by End-User (Residential and Commercial), and Content Type (Audio Streaming and Video Streaming) and Regional Analysis for 2026 – 2033

Music Streaming Market Overview

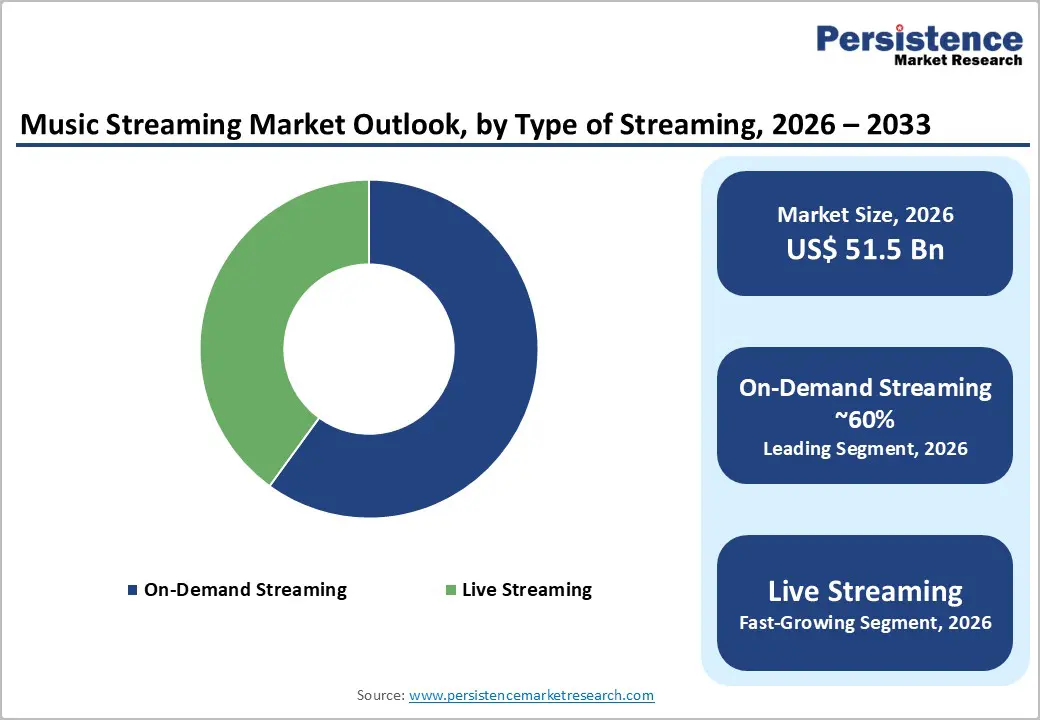

The global Music Streaming Market size was valued at US$ 51.5 Bn in 2026 and is projected to reach US$ 127.3 Bn by 2033, growing at a CAGR of 13.8% between 2026 and 2033. This robust expansion reflects the fundamental transformation in music consumption patterns, driven by ubiquitous smartphone adoption and high-speed internet penetration worldwide. The market's trajectory is further accelerated by shifting consumer preferences from music ownership to on-demand access models, creating sustained demand for streaming platforms.

Key Market Highlights

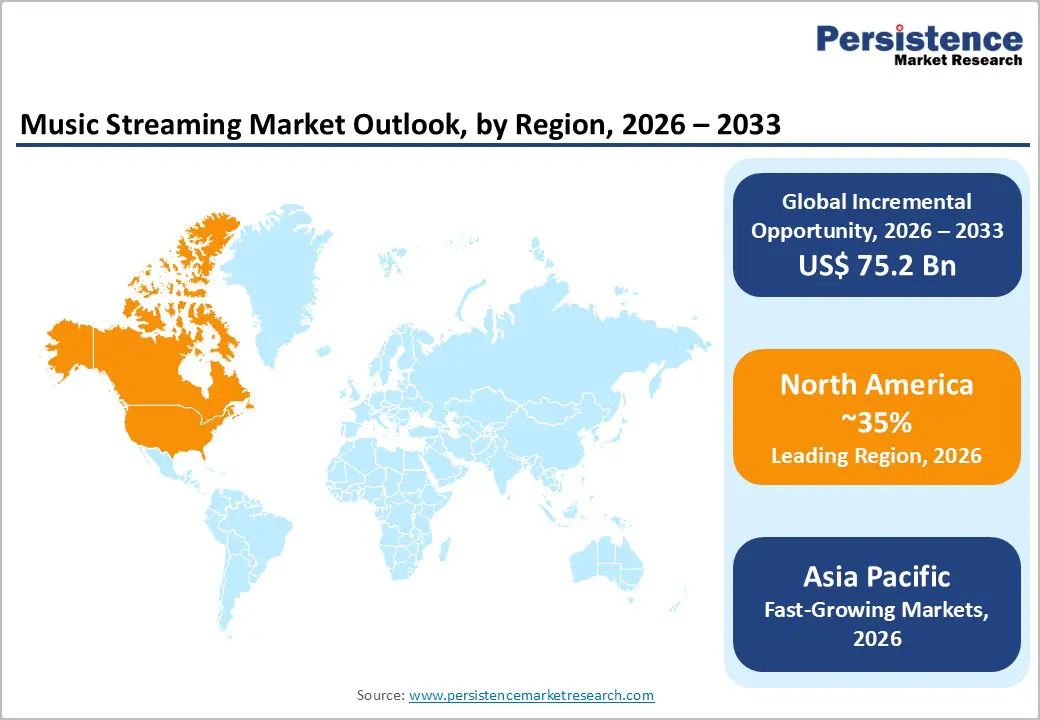

- Leading region: North America dominates the global music streaming market with approximately 35% revenue share, driven by high smartphone penetration, widespread adoption of paid subscriptions, strong presence of major streaming platforms, and advanced digital payment infrastructure.

- Fastest growing region: Asia Pacific is the fastest growing regional market, expanding at an estimated 18% CAGR, supported by rapid smartphone adoption, affordable mobile data, expanding middle-class populations, and growing youth demographics in countries such as India, China, Indonesia, and South Korea. Local language content expansion, freemium models, and partnerships with telecom operators are accelerating user acquisition across the region.

- Dominant segment: On-Demand Streaming services dominate the market with approximately 60% share, reflecting consumers’ preference for ad-free listening, offline downloads, and high-quality audio. The dominance is driven by competitive pricing, bundled offerings with telecom and device manufacturers, and increasing conversion from free to paid plans.

- Fastest growing segment: Podcast and audio content streaming is the fastest growing segment, registering over 20% CAGR, driven by rising demand for on-demand spoken content, exclusive creator deals, and increasing consumption during commuting and multitasking activities.

- Key market opportunity: AI-driven personalization, creator monetization tools, and immersive audio technologies (such as spatial audio and live interactive streaming) represent major growth opportunities, enabling improved user engagement, differentiated listening experiences, and new revenue streams for platforms and artists.

| Key Insights | Details |

|---|---|

|

Music Streaming Market Size (2026E) |

US$ 51.5 Bn |

|

Music Streaming Market Value (2033F) |

US$ 127.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

13.8% |

|

Historical Market Growth (CAGR 2020 to 2024) |

11.5% |

Market Dynamics

Market Growth Drivers

Proliferation of Smart Devices and Connectivity Infrastructure

The exponential growth in smartphone adoption globally is the primary catalyst for the expansion of the music streaming market. According to the International Federation of the Phonographic Industry (IFPI), paid subscription streaming revenues increased by 9.5% in 2024, reaching US$ 15.15 billion, while total streaming revenues exceeded US$ 20 billion for the first time. The Recording Industry Association of America (RIAA) reported that the United States surpassed 100 million paid music streaming subscriptions in 2024, representing a historic milestone. This growth is underpinned by the expansion of 4G and 5G networks, which enable seamless high-quality audio streaming. The Musical Instrument Market demonstrates complementary growth, as increased music consumption drives interest in music creation, further expanding the overall music ecosystem.

Shift from Ownership to Access-Based Consumption Models

Consumer behavior has fundamentally shifted from purchasing physical albums and digital downloads to accessing vast music libraries on-demand. This transition is evidenced by streaming's dominance, accounting for 69% of total global recorded music revenues in 2024. Spotify reported 276 million premium subscribers in Q2 2026, representing a 12% year-over-year increase, while monthly active users reached 696 million. The platform's growth reflects consumer demand for personalized playlists, offline listening capabilities, and cross-device synchronization. This trend is particularly pronounced among younger demographics who prioritize convenience and discovery over ownership, creating a sustainable revenue model for streaming platforms.

Market Restraints

Market Saturation and Intensifying Competition in Developed Regions

The music streaming market faces significant headwinds from saturation in mature markets like North America and Europe. The RIAA noted that US streaming revenue growth slowed to 3.6% in 2024, down from 8.1% in 2023, indicating diminishing returns in established territories. Spotify, Apple Music, and Amazon Music collectively command over 90% of the US market share, leaving limited room for new entrants. This concentration creates intense price competition and pressures profit margins. Additionally, the cost of content acquisition and licensing continues to rise, with major labels demanding higher royalty rates, squeezing platform profitability. The market's maturity in developed regions necessitates alternative growth strategies, such as bundling services or expanding into adjacent content categories.

Artist Compensation and Royalty Distribution Challenges

Growing scrutiny over artist compensation models poses a significant restraint to market growth. Many artists and industry advocates argue that streaming royalties are insufficient, with MIDiA Research highlighting that emerging artists face financial challenges due to demonetization thresholds. The IFPI reported that while streaming revenues reached US$ 20.4 billion in 2024, concerns persist about equitable revenue distribution. This has led to calls for policy interventions and potential regulatory changes that could increase costs for streaming platforms. Furthermore, high-profile artists have temporarily withdrawn their catalogs from certain platforms to protest royalty rates, creating reputational risks and potential subscriber churn.

Market Opportunities

Expansion into High-Growth Emerging Markets

Asia Pacific and Latin America present substantial growth opportunities for music streaming platforms. The IFPI identified Latin America as the fastest-growing region with 22.5% revenue growth in 2024, while the Middle East and North Africa (MENA) grew by 22.8%. India and Southeast Asian markets offer particularly compelling prospects due to their large youth populations and increasing smartphone penetration. Spotify has demonstrated success in these regions, with significant subscriber growth in Latin America and Europe driving its Q2 2026 performance. Localizing content, offering regional pricing strategies, and partnering with telecom providers can unlock these markets. The Music Streaming Market opportunity extends beyond music to include podcasts, audiobooks, and live audio events, creating multiple revenue streams.

High-Fidelity Audio and Premium Tier Differentiation

The emergence of lossless and high-fidelity audio streaming represents a lucrative opportunity for market differentiation and revenue growth. Apple Music launched lossless audio at no additional cost, while Amazon Music HD and Tidal have positioned high-quality audio as premium offerings. This segment caters to audiophiles and music enthusiasts willing to pay premium prices for superior sound quality. Additionally, integrating AI-driven personalization, exclusive content, and virtual concert experiences can justify higher subscription tiers. Spotify's recent price increases reflect this strategy, with its Family tier now priced at $19.99 monthly in the US, demonstrating consumer willingness to pay for enhanced features. The convergence of music streaming with trends in the Musical Instrument Market, where consumers increasingly seek professional-grade audio experiences, further supports this opportunity.

Category-wise Insights

Type of Streaming Analysis

On-Demand Streaming dominates the music streaming landscape, commanding approximately 85% market share due to consumer preference for personalized, instant access to vast music libraries. This segment's leadership is reinforced by platforms like Spotify, Apple Music, and Amazon Music, which offer sophisticated recommendation algorithms, offline downloads, and cross-device synchronization. The IFPI reported that paid subscription streaming revenues grew 9.5% in 2024, reaching US$ 15.15 billion, while ad-supported formats grew modestly at 1.2%. The success of on-demand streaming is evidenced by Spotify's 276 million premium subscribers and 696 million monthly active users in Q2 2026. This segment's growth is further supported by integration with smart speakers, automotive systems, and wearable devices, creating seamless listening experiences across consumer touchpoints.

End-User Analysis

Residential users account for 90% of music streaming consumption. This dominance reflects the integration of streaming services into daily life, with consumers using platforms for personal entertainment, background music, and social sharing. The RIAA reported that paid subscriptions in the US reached 100 million in 2024, primarily driven by residential users seeking ad-free experiences. The segment's growth is fueled by family plans, student discounts, and bundling with other services, such as Amazon Prime. Spotify's Family tier, priced at $19.99 monthly, and Apple Music's family offerings demonstrate the importance of residential multi-user accounts. The Musical Instrument Market is showing parallel growth as residential users increasingly engage with music creation tools, indicating a broader cultural shift toward music creation.

Content Type Analysis

Audio Streaming maintains clear market leadership with 75% share, as music remains the core consumption format for streaming platforms. The IFPI confirmed that streaming revenues exceeded US$ 20 billion for the first time in 2024, representing 69% of total recorded music revenues. Spotify hosts over 100 million tracks, while Apple Music and Amazon Music offer similarly extensive catalogs. Audio streaming's portability and compatibility with diverse devices make it ideal for multitasking while commuting, at work, and during exercise. The segment continues evolving with podcast integration, with Spotify investing heavily in exclusive podcast content to differentiate its audio offering. The Music Streaming Market benefits from audio's lower bandwidth requirements compared to video, enabling broader accessibility in emerging markets with limited connectivity.

Regional Insights

North America Music Streaming Trends

North America maintains its position as the largest music streaming market, with the United States reaching 100 million paid subscriptions in 2024 according to the RIAA. The region generated US$ 14.9 billion in streaming revenues, accounting for 84% of total recorded music revenues. Spotify leads with 36% market share, followed by Apple Music at 30.7% and Amazon Music at 23.8%, collectively commanding 90.5% of the US market. The region's maturity is evidenced by slowing growth, with streaming revenues increasing only 3.6% in 2024 compared to 8.1% in 2023. However, innovation remains strong, with platforms introducing hi-fi audio, exclusive content, and bundled services. The Canadian market shows similar patterns, with strong smartphone penetration and established platform presence driving steady adoption.

Europe Music Streaming Trends

Europe represents the second-largest region, contributing 29.5% of global recorded music revenues with 8.3% growth in 2024. The United Kingdom grew by 4.9%, Germany by 4.1%, and France by 7.5%, demonstrating robust performance across major markets. Spotify, headquartered in Sweden, maintains strong regional presence, with Europe accounting for 28% of its monthly active users. The region's regulatory framework, including the Digital Services Act and copyright directives, creates a structured environment for streaming operations. Europe's diverse linguistic landscape necessitates localized content strategies, with platforms investing in regional playlists and artist partnerships. The Musical Instrument Market in Europe shows complementary growth, indicating deep cultural engagement with music. Streaming accounts for most revenues in all major European markets, with physical formats declining but vinyl maintaining niche appeal.

Asia Pacific Music Streaming Trends

Asia Pacific emerges as the fastest-growing region, with China, Japan, India, and ASEAN countries driving dynamic expansion. The region's growth is fueled by massive youth populations, increasing disposable incomes, and improving internet infrastructure. Spotify reported strong performance in Latin America and Europe in Q2 2026, but Asia Pacific represents the next frontier, with platforms tailoring offerings to local preferences. Tencent Music dominates China with over 800 million users, while India shows explosive growth potential. The IFPI highlighted Latin America's 22.5% growth and MENA's 22.8% growth, indicating similar potential in Asia Pacific's emerging markets. Local partnerships with telecom providers and regional pricing strategies are essential for market penetration. The Music Streaming Market benefits from Asia's manufacturing advantages for devices and infrastructure, supporting affordable access.

Competitive Landscape

Market Structure Analysis

The music streaming market exhibits a consolidated structure dominated by Spotify, Apple Music, and Amazon Music, which collectively control over 90% of the US market. This concentration reflects high barriers to entry, including substantial content licensing costs, technological infrastructure requirements, and network effects. Companies pursue differentiation through AI-driven personalization, exclusive content acquisitions, and ecosystem integration. Spotify invests heavily in podcast content and algorithmic recommendations, while Apple Music leverages its hardware ecosystem and lossless audio offerings. Amazon Music benefits from Prime bundling, creating sticky user relationships. Emerging trends include hi-fi audio tiers, live audio events, and social features that enable collaborative playlists and sharing. The market's consolidation pressures smaller players like Deezer and Tidal to target niche segments with specialized offerings.

Key Market Developments

- In February 2026, Spotify launched "Mi Primer Escenario" (My First Stage) in Argentina, a music contest designed to support emerging artists. The contest offers up-and-coming Argentine musicians the chance to showcase their talent and connect with listeners, with the grand prize being a performance slot at Quilmes Rock, a major music festival, alongside established acts.

- In December 2024, Apple, Inc. (Apple Music) expanded its live global radio offering with the launch of three new stations: Apple Música Uno, Apple Music Club, and Apple Music Chill. These stations join Apple Music 1, Hits, and Country to provide listeners with more exclusive shows hosted by a diverse range of artists.

Companies Covered in Music Streaming Market

- Apple

- Amazon Music

- Spotify

- Pandora

- SoundCloud

- JOOX

- Tidal

- iHeartRadio

- Deezer

- KKBox

- Other Key Players

Frequently Asked Questions

The global Music Streaming Market is projected to reach approximately US$ 126.4 billion by 2033, expanding from US$ 51.1 billion in 2026, at a forecast CAGR of 13.8% between 2026 and 2033.

The primary demand drivers for the Music Streaming Market are outlined below, reflecting consumer behaviour, technology adoption, and industry dynamics.

On-Demand Streaming services dominate the market with approximately 60% share, reflecting consumers’ preference for ad-free listening, offline downloads, and high-quality audio.

North America, particularly the United States, dominates the global Music Streaming Market with approximately 35%, with the United States reaching 100 million paid subscriptions in 2024 according to the RIAA.

Major players include Apple, Google, Amazon Music, Spotify and Pandora.