- HVAC

- Mist Eliminators Market

Mist Eliminators Market Size, Share, and Growth Forecast 2025 - 2032

Mist Eliminators Market by Product Type (Wire Mesh, Vane, Fiber Bed, Cyclone, Baffle), Technology (Brownian Diffusion, Direct Interception, Inertial Impaction), Application (Distillation, Dehydrator, Evaporator, Others), End-user, and Regional Analysis for 2025 - 2032

Mist Eliminators Market Size and Trend Analysis

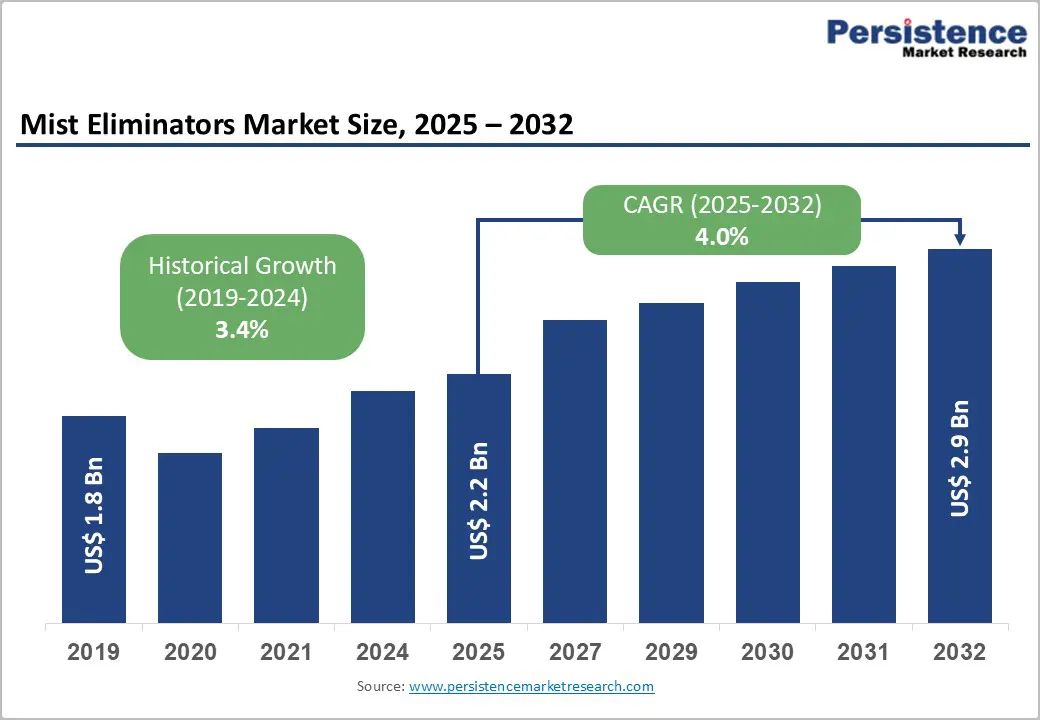

The global mist eliminators market size is likely to be valued at US$2.2 billion in 2025 and is expected to reach US$2.9 billion by 2032, growing at a CAGR of 4.0% during the forecast period from 2025 to 2032, driven by increasingly stringent air-emission regulations across major industrial economies, compelling operators to adopt advanced mist control solutions to meet compliance requirements.

Ongoing advancements in high-efficiency fiber-bed designs, low-pressure-drop vane systems, and corrosion-resistant materials are enhancing separation efficiency and reliability. Rising capacity expansion and plant modernization across energy, chemicals, refining, pharmaceuticals, and manufacturing sectors continue to drive demand, as mist eliminators are essential for process efficiency, product purity, and equipment protection.

Key Industry Highlights

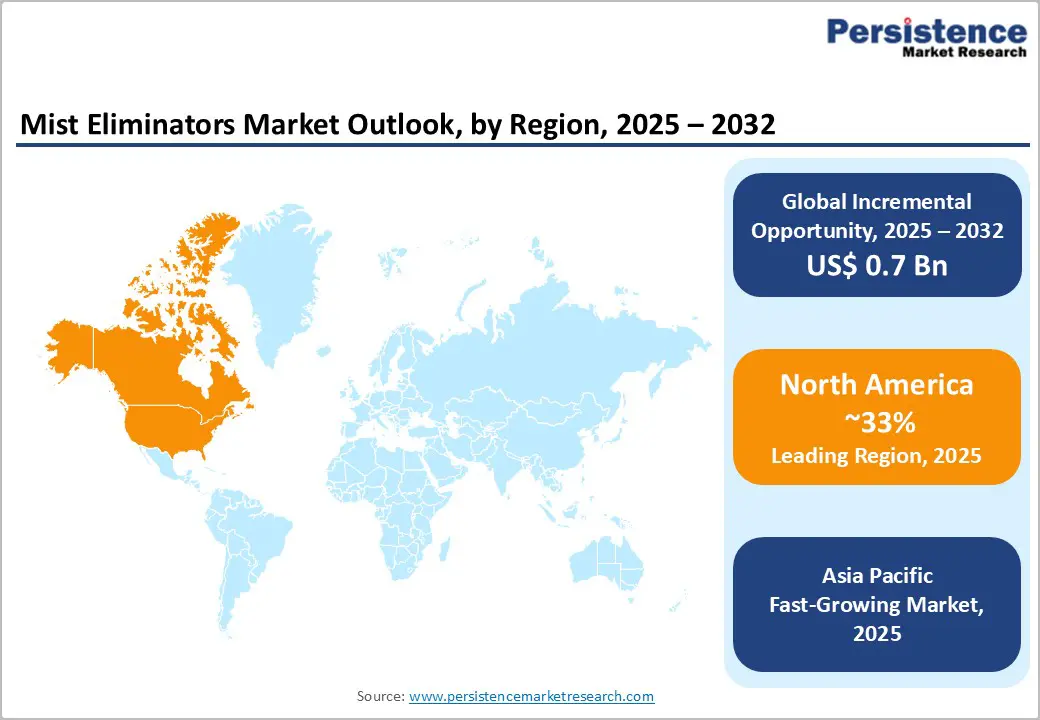

- Leading Region: North America leads the market with around 33% share, driven by stringent EPA emission norms, strong innovation incentives, and rising investments in advanced pollution-control technologies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by large-scale industrial expansion in China, Japan, and India, stricter pollution regulations, and rising investments in next-generation separation technologies across major ASEAN economies.

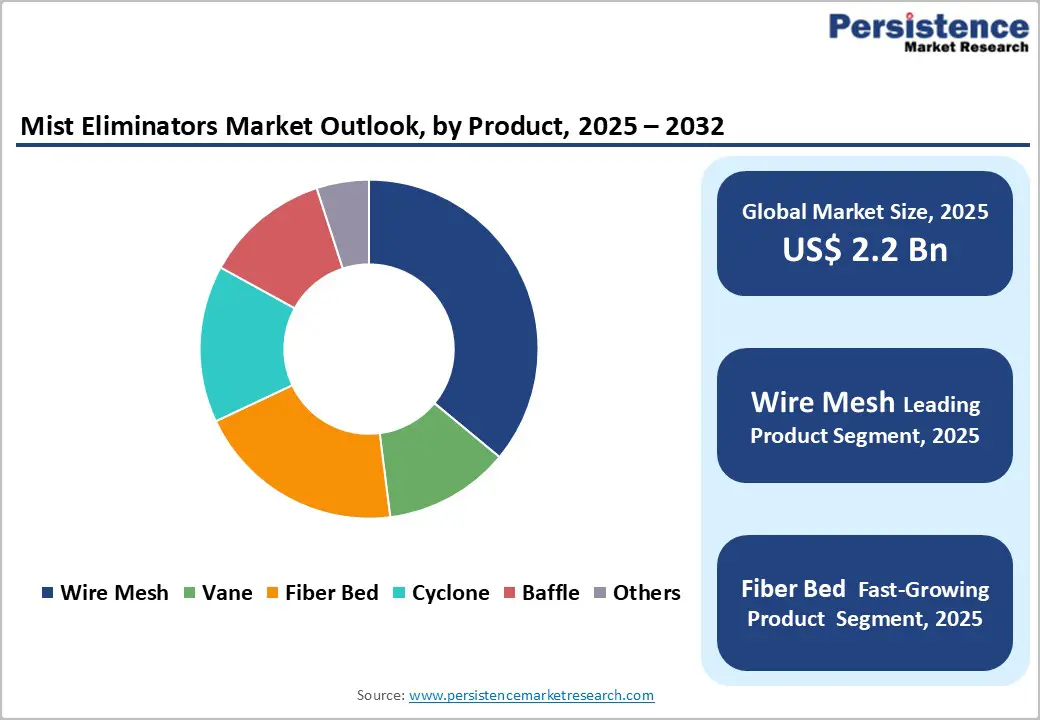

- Leading Product Type: Wire mesh mist eliminators lead the product type segment with 42% revenue share in 2025, driven by their cost-effectiveness, reliability, and wide industrial applicability.

- Leading Technology: Direct interception leads the market with over 37% revenue share in 2025, driven by its precision droplet removal and broad suitability for scrubbers and knockout drum applications.

- Leading Application: Distillation columns account for the largest share of revenue at 30%, driven by their critical role in ensuring product purity and operational efficiency in refining and bulk chemical processing.

- Leading End-user Type: Mist removal represents the leading segment in the market with about 41% revenue share, driven by its essential role in ensuring process clarity, reducing material loss, and enhancing operational safety across manufacturing industries.

| Key Insights | Details |

|---|---|

| Mist Eliminators Market Size (2025E) | US$2.2 Bn |

| Market Value Forecast (2032F) | US$2.9 Bn |

| Projected Growth CAGR (2025 - 2032) | 4.0% |

| Historical Market Growth (2019 - 2024) | 3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Intensification

Regulatory intensification is significantly accelerating the demand for mist eliminators. Regulatory bodies such as the U.S. EPA, the European Environment Agency, and China’s Ministry of Ecology and Environment are tightening limits on vapor-phase pollutants and aerosols across major industrial sectors. According to the WHO, outdoor air pollution contributes to roughly 4.2 million premature deaths every year, highlighting the urgent need for stronger emission-control measures. As compliance thresholds become stricter, industries are increasingly required to implement reliable separation technologies to control fine droplets and hazardous mists. This trend is especially pronounced in refining, chemicals, power generation, and metals processing, where emissions scrutiny is the highest.

Mist eliminators are emerging as vital tools to help industry balance performance and compliance. Companies in energy generation and process manufacturing are increasingly investing in high-efficiency mist eliminators, such as wire-mesh, vane, and fiber-bed designs, to meet regulatory mandates, reduce chemical losses, and prevent equipment corrosion. Regulatory pressure is driving new installations and the retrofitting of legacy systems with advanced mist-control solutions. Long-term compliance planning is boosting demand for modular designs and aftermarket upgrades, positioning mist eliminators as critical components of modern environmental control strategies.

Capital and Operating Cost Pressures

Mist eliminators deliver essential environmental and process benefits; their adoption is often constrained by high capital and operating costs. High-performance systems, particularly fiber-bed and vane designs, require significant upfront investments due to complex engineering, precision manufacturing, and specialized materials. These cost pressures are more pronounced in applications that require corrosion-resistant materials, such as PTFE-coated mesh, stainless steel, or high-grade alloys, to withstand aggressive process conditions. For small and mid-sized operators, such investments can delay upgrades or limit adoption, especially in price-sensitive or emerging markets.

Operating expenses affect the total cost of ownership. Mist eliminators require regular inspection, cleaning, and replacement to maintain separation efficiency, particularly in high-load or contaminated gas streams. Fouling, plugging, and corrosion gradually reduce performance and increase pressure drop, thereby increasing energy consumption. In highly corrosive environments such as sulfuric acid, chlor-alkali, or specialty chemical processes, component degradation can occur rapidly, shortening service life. Operators may also face higher spare parts costs and increased shutdown frequency to maintain compliance.

Innovation in Brownian Diffusion and Direct Interception Technologies

Innovation in Brownian diffusion and direct interception technologies offers a compelling growth opportunity in the mist-eliminator market by combining ultra-high efficiency with lower operational costs. Brownian diffusion systems, supported by advances in materials science, are becoming a preferred choice for industries handling corrosive, toxic, or submicron particulate streams. These systems enable superior capture efficiency while maintaining low pressure drop, helping operators meet tightening emission standards without major energy penalties. Growing adoption in pharmaceuticals, semiconductors, specialty chemicals, and clean-process industries is accelerating development.

Direct interception designs are also undergoing significant performance enhancements through geometry optimization and flow-path engineering. Recent experimental studies indicate that redesigned wave-plate angles and spacing improve droplet capture under high re-entrainment and fluctuating flow conditions, enhancing reliability in scrubbers and knockout drums. Manufacturers are increasingly adopting hybrid configurations that combine fiber-bed, mesh, and vane mechanisms to address a wider range of particle sizes and process conditions. These integrated designs improve operational flexibility, simplify retrofitting, and support multi-stage separation. As digital modeling and CFD tools mature, gains in efficiency and scalability are expected, reinforcing innovation as a key market driver.

Category-wise Analysis

Product Type Insights

Wire mesh leads the market, capturing around 42% of the total revenue share in 2025. This commanding share reflects their strong value proposition: mesh eliminators combine low cost, simplicity, and high reliability. Their versatile design excels in a range of industrial settings from oil & gas refineries and chemical plants to food and beverage processing, making them a go-to choice for both coarse and fine droplet separation.

Fiber bed represents the fastest-growing product type, driven by demand from industries requiring ultrafine aerosol control, such as pharmaceuticals, semiconductor manufacturing, and specialty chemical processing. In these sectors, removing very fine mists down to submicron sizes is critical to ensuring product purity, minimizing emissions, and meeting increasingly strict environmental regulations. Fiber bed designs deliver superior submicron capture, driving adoption as performance and emission standards tighten.

Technology Type Insights

Direct interception mist eliminators lead the market, accounting for over 37% revenue share in 2025, driven by their low cost, simplicity, and proven reliability. They are widely used in crude and vacuum distillation units in oil refineries, amine and glycol dehydration units in natural gas processing, and evaporators in food and beverage plants. In chemical manufacturing, wire-mesh mist eliminators, such as those supplied by DuPont de Nemours, are widely used in flash drums and absorption columns to capture entrained liquids and safeguard downstream compressors. Their ability to efficiently handle moderate droplet sizes, along with low pressure drop and easy maintenance, makes them a preferred solution for high-throughput, cost-sensitive industrial processes.

Brownian diffusion represents the fastest-growing technology segment, driven by rising demand for ultrafine aerosol control in sulfuric acid plants, phosphoric acid production, semiconductor fabs, and pharmaceutical reactors. These systems are critical in applications such as tail-gas treatment units and acid concentration towers, where effective removal of submicron acid mist is essential for emissions compliance and equipment protection. Leading manufacturers such as Koch-Glitsch provide FLEXIFIBER® mist eliminators, designed for specialty chemical applications that require high submicron particle capture with minimal pressure drop. Fiber-bed designs are also seeing increased adoption in battery materials and specialty chemical processing, where strict purity standards are critical.

Application Type Insights

Distillation columns lead the market, capturing around 30% of total revenue share, reflecting their critical role in maintaining product purity, preventing liquid carryover, and ensuring stable separation efficiency. Mist eliminators are extensively used in crude and vacuum distillation units in oil refineries and fractionation columns in petrochemical complexes, such as Reliance Industries, where even minor entrainment can reduce yield and damage downstream equipment. They are also essential in alcohol distillation for ethanol production and solvent recovery units in bulk chemical manufacturing, ensuring consistent product specifications.

Scrubber applications represent the fastest-growing segment, driven by tightening emissions regulations and the rapid expansion of industrial gas-cleaning infrastructure, particularly across the Asia Pacific. Mist eliminators are increasingly deployed in flue gas desulfurization (FGD) systems at coal-fired power plants and wet scrubbers used in non-ferrous metal smelting and fertilizer production. These applications require efficient removal of acid mists and fine aerosols to meet regulatory limits. Growing investments in chemical parks, waste-to-energy plants, and industrial pollution-control retrofits are further boosting demand for high-efficiency mist eliminators, positioning scrubbers as a key growth engine in the market.

End-user Insights

Mist removal is the leading end-user segment, accounting for about 41% of revenue share, underscoring the critical role of mist eliminators in maintaining process efficiency, reducing product losses, and improving operational safety. These systems are extensively used in oil & gas refineries, chemical plants, pharmaceutical manufacturing, and food processing facilities to separate liquid droplets from vapor streams. Common applications include amine and glycol dehydration units in natural gas processing, pharmaceutical evaporation systems to prevent solvent carryover, and spray dryers and fermentation exhausts in food and beverage plants where moisture entrainment can affect hygiene and performance.

Pollution control represents the fastest-growing end-user segment, propelled by increasingly stringent environmental regulations. Industries are adopting mist eliminators in flue gas desulfurization (FGD) units at power plants and in wet scrubbers used across fertilizer, metal smelting, and chemical manufacturing to control acid mist, aerosols, and particulate emissions. Tightening regulations from authorities such as the EPA, EEA, and China’s Ministry of Ecology and Environment are driving upgrades of legacy emission-control systems, reinforcing mist eliminators as essential components of modern compliance strategies.

Regional Insights

North America Mist Eliminators Market Trends

North America is the leading region, driven by mature industrialization, strict air-emission regulations, and continuous investments in pollution-control technologies. The U.S., in particular, dominates demand due to strong enforcement of EPA standards across oil & gas, power generation, chemicals, pharmaceuticals, and wastewater treatment industries. Growing focus on reducing hazardous air pollutants, acid mist, and fine aerosols is accelerating both new installations and upgrades of existing systems. Infrastructure modernization and refinery capacity optimization programs are reinforcing long-term demand for high-efficiency mist elimination solutions.

The region is also witnessing accelerated adoption of advanced corrosion-resistant materials, enabling longer equipment life in harsh environments such as refineries and petrochemical plants. Leading suppliers, including Koch-Glitsch, CECO Environmental, and Munters, are expanding their portfolios with low-pressure-drop, high-capacity designs that increase operational efficiency and reduce energy consumption. Digital monitoring, predictive maintenance, and aftermarket service contracts are gaining traction as operators seek to maximize uptime and lifecycle performance.

Europe Mist Eliminators Market Trends

Europe remains a significant market for mist eliminators for control computers, supported by its advanced chemical, refining, and energy process industries and strong environmental commitments under the European Green Deal. The region benefits from a harmonized regulatory framework, including the EU Emissions Trading Scheme (ETS) and the Industrial Emissions Directive (IED), which standardize emissions-control requirements and encourage widespread adoption of high-efficiency mist elimination technologies across member states. These regulations are pushing industries to reduce acid mist, aerosols, and particulate emissions, driving both new installations and system upgrades.

Market expansion is driven by growing emphasis on environmental compliance, tighter emission thresholds, and increasing demand for ultrafine mist and aerosol control in critical industrial operations. Innovation in low-pressure-drop, modular, and corrosion-resistant designs is improving performance while reducing operating costs. The integration of digital monitoring and predictive maintenance is also helping operators enhance reliability and extend equipment life. Collaborative sustainable R&D initiatives, joint ventures, and active competition between large OEMs and specialized SMEs continue to strengthen Europe’s position as a technology-driven, compliance-focused mist eliminators.

Asia Pacific Mist Eliminators Market Trends

Asia Pacific is the fastest-growing region in the mist eliminators market, driven by rapid industrialization, urban expansion, and tightening emissions regulations in major economies such as China and India. Governments are increasing investments in pollution-control infrastructure, prompting industries to adopt high-efficiency mist eliminators to curb acid mist, SOx, and fine aerosol emissions. Large industrial groups such as Sinopec, PetroChina, Reliance Industries, and Tata Chemicals are installing advanced mist elimination systems across refineries, chemical plants, and power facilities to meet evolving environmental standards and improve operational efficiency.

Technological preferences in the region are shifting toward polypropylene-based mist eliminators due to their cost-effectiveness and resistance to corrosion in scrubber and acid-gas environments. Companies such as AMACS and local Asian manufacturers supply PP mesh and vane systems tailored to regional process conditions. Cyclonic mist eliminators are also gaining traction in high-throughput petrochemical and refining operations for their robustness and low maintenance needs. Suppliers are also promoting modular, skid-mounted designs that allow faster project execution, easier retrofits, and reduced downtime.

Competitive Landscape

The global mist eliminators market is moderately fragmented, driven by regulatory demand for emissions control, industrial capacity expansions in energy and chemicals, and ongoing product innovations that enhance performance while reducing lifecycle costs. Increasing retrofit projects and stronger aftermarket services are prompting suppliers to offer low-pressure-drop solutions and corrosion-resistant materials. Key market players include Koch-Glitsch, Sulzer, Munters, and others, with the market comprising both large multinational engineering firms and specialized manufacturers catering to niche process needs.

Companies compete through differentiated technology portfolios, strong OEM and EPC partnerships, and expanded aftermarket offerings such as performance upgrades, predictive maintenance, and performance guarantees. Innovations such as hybrid fiber-vane modules, low-pressure-drop designs, polypropylene options for scrubbers, and digital monitoring are becoming critical competitive levers. Strategic initiatives include joint R&D efforts, regional manufacturing to reduce lead times, and targeted acquisitions to strengthen market positioning.

Key Industry Developments:

- In September 2025, Absolent launched the AW-range, a new generation of compact and modular oil mist filter units designed for high-precision and micro-machining environments. The AW-range features a plug-and-play design, flexible mounting options, and a balanced fan system that minimizes vibration, enabling easy integration and reliable operation in sensitive machining applications.

- In June 2024, Elessent Clean Technologies launched the Brink® ezSEP™ high-efficiency separation system for green hydrogen producers. Designed specifically for electrolyzer applications, the solution delivers advanced mist elimination and liquid recovery, capturing submicron mist particles and achieving very high separation efficiency in saturated gas streams. Brink® ezSEP™ helps reduce makeup water and electrolyte losses, lowers maintenance requirements, and improves downstream equipment protection, including compressors and desiccant dryers.

Companies Covered in Mist Eliminators Market

- Filtermist International Limited

- Amacs Process Towers Internals

- Munters AB

- Hilliard Corporation

- Koch Engineered Solutions

- Sulzer Ltd

- DuPont

- Boegger Industrial Limited

- REA Plastik Tech GmbH

- Agilis Technologies

- Sullair, LLC

- Kimre, Inc.

- Air Quality Engineering

- KCH Services, Inc.

- Coastal Technologies, Inc.

- Okutani Ltd.

- MMAQUA!

- VARUN ENGINEERING

Frequently Asked Questions

The global mist eliminators market is valued at US$2.2 billion in 2025 and expected to reach US$2.9 billion by 2032, reflecting robust growth.

The primary demand drivers for the mist eliminators market are stringent regulatory requirements for emissions control, advancements in high-efficiency separation technologies, and the ongoing expansion of industrial infrastructure.

In the mist eliminators market, the wire mesh segment leads in the product type category, holding approximately 42% market share, while direct interception is the leading technology.

North America dominates, capturing over 33% market share, driven by stringent EPA emission norms, strong innovation incentives, and rising investments in advanced pollution-control technologies.

The key opportunities include innovation in Brownian diffusion separation, expansion in emerging markets, and the rise of green manufacturing and circular economy adoption.