- Industrial Machinery

- Mechanical Seals Market

Mechanical Seals Market Size, Share, and Growth Forecast 2026 - 2033

Mechanical Seals Market by Product Type (Pusher Seals, Bellows Seals, Cartridge Seals, Split Seals), Design (Single Mechanical Seals, Double Mechanical Seals, Tandem Mechanical Seals), Application (Pumps, Compressors, Mixers & Agitators, Reactors, Marine Seals, Others), Industry (Oil & Gas, Chemical & Petrochemical, Power Generation, Water & Wastewater, Food & Beverage, Pharmaceuticals, Pulp & Paper, Mining & Metals), Distribution Channel, Regional Analysis, 2026 - 2033

Mechanical Seals Market Size and Trend Analysis

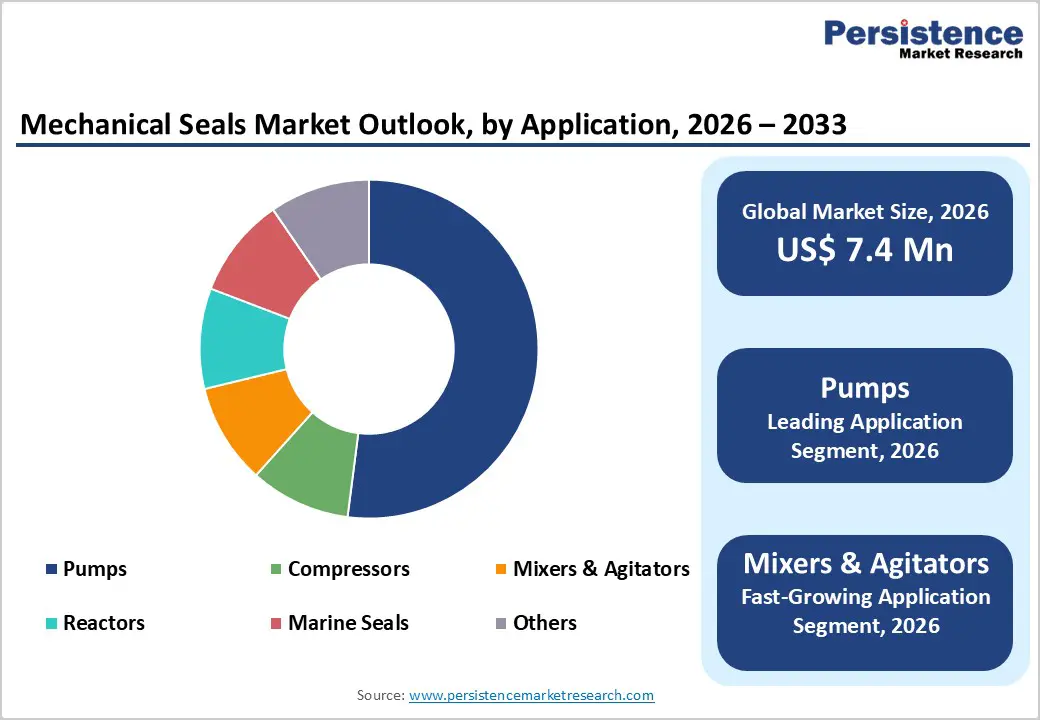

The global Mechanical Seals market size is expected to be valued at US$ 7.4 billion in 2026 and projected to reach US$ 10.4 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033.

The market is poised for steady and sustained expansion, underpinned by rising investment in process industries, most notably oil & gas, chemical & petrochemical, power generation, and water & wastewater treatment, where mechanical seals are mission-critical components for rotating equipment reliability and environmental compliance.

Stringent global regulations governing fugitive emissions from industrial rotating equipment, including the U.S. Environmental Protection Agency (EPA) 40 CFR Part 63 LDAR (Leak Detection and Repair) standards and the European Industrial Emissions Directive (IED 2010/75/EU), are compelling industrial operators to retrofit and upgrade sealing systems to double or tandem mechanical seal configurations. Accelerating infrastructure investment in water treatment, LNG liquefaction, and pharmaceutical manufacturing across both mature and emerging economies is further broadening the mechanical seals demand base through the forecast horizon.

Key Industry Highlights:

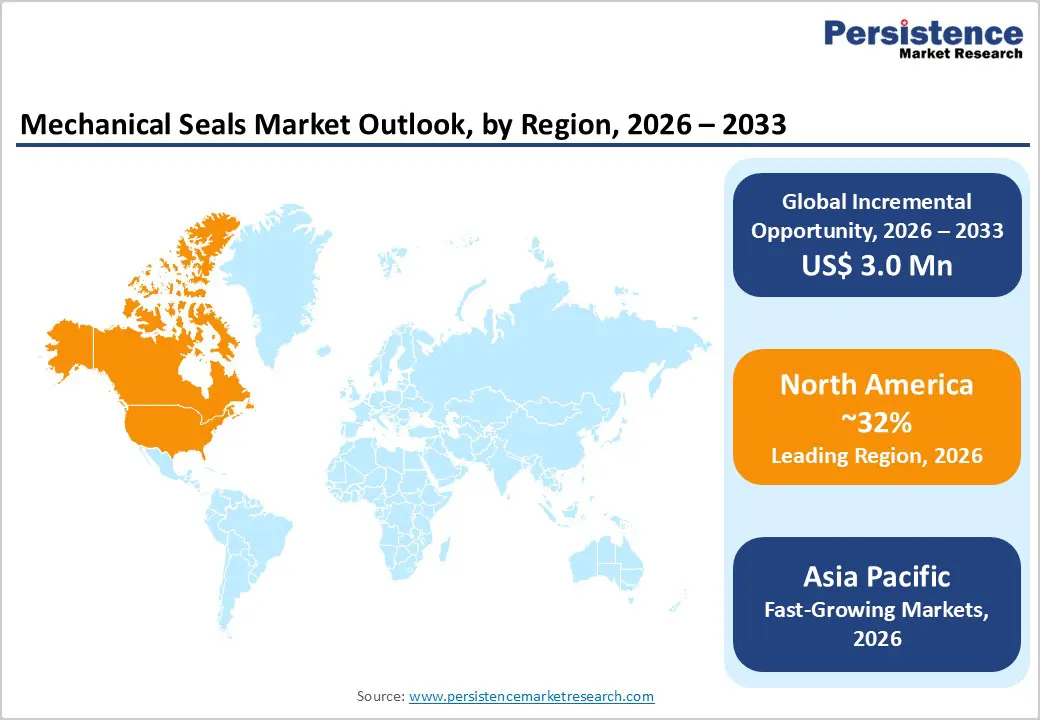

- Leading Region: North America leads the global Mechanical Seals market with approximately 32% revenue share in 2025, driven by the U.S. EPA’s stringent LDAR fugitive emission mandates, robust oil & gas sector capital spending, active water infrastructure modernization, and the world’s most concentrated industrial aftermarket service ecosystem.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market, projected to expand at approximately 6.5% CAGR through 2033, fueled by China’s massive chemical complex expansion, India’s Jal Jeevan Mission pump infrastructure investment, and surging LNG and pharmaceutical sector development across South Korea, ASEAN, and emerging Asian economies.

- Dominant Segment: Cartridge seals dominate the product type segment with approximately 38% market share in 2025, preferred across oil & gas, chemical, and power generation applications for their factory pre-set assembly, superior installation reliability, lower lifecycle cost, and explicit recommendation under API 682’s 5th Edition sealing standard.

- Fastest Growing Segment: Double and tandem mechanical seal configurations represent the fastest growing design sub-segment, as expanding EPA LDAR and EU Industrial Emissions Directive requirements systematically mandate zero-leakage sealing arrangements for hazardous and volatile process fluid services across refinery, chemical, and LNG applications globally.

- Key Opportunity: The pharmaceutical and food & beverage sectors’ rapid capacity expansion, driven by biologics manufacturing growth and FAO-tracked food processing investment across emerging markets, presents a high-value opportunity for manufacturers of FDA 21 CFR-, EHEDG-, and 3-A Sanitary Standards-certified hygienic mechanical seals commanding significant pricing premiums.

| Key Insights | Details |

|---|---|

|

Mechanical Seals Market Size (2026E) |

US$ 7.4 Billion |

|

Market Value Forecast (2033F) |

US$ 10.4 Billion |

|

Projected Growth CAGR (2026–2033) |

5.0% |

|

Historical Market Growth (2020–2025) |

4.5% |

DRO Analysis

Driver - Stringent Fugitive Emission Regulations Driving Seal Upgrades in Process Industries

Tightening global environmental regulations governing fugitive emissions from industrial rotating equipment represent the most consequential structural driver of mechanical seals market growth. The U.S. EPA’s National Emission Standards for Hazardous Air Pollutants (NESHAP) and 40 CFR Part 60 (New Source Performance Standards) mandate Leak Detection and Repair (LDAR) programs at refineries, chemical plants, and compressor stations, effectively compelling operators to transition from traditional packing-based sealing to double or tandem mechanical seal arrangements that deliver superior fugitive emission containment. Similarly, the European Industrial Emissions Directive (IED 2010/75/EU) and Best Available Techniques Reference Documents (BREFs) specify mechanical seals as the preferred sealing technology for volatile organic compound (VOC)-handling pumps in chemical and petrochemical facilities.

The American Petroleum Institute (API) Standard 682, the globally recognized reference standard for shaft sealing systems in centrifugal and rotary pumps, now in its 5th edition, continues to set increasingly stringent sealing performance requirements, driving systematic specification upgrades across refinery and petrochemical plant maintenance programs worldwide.

Expanding Oil & Gas Infrastructure Investment and LNG Sector Growth

Global oil & gas capital expenditure recovery and the accelerating buildout of liquefied natural gas (LNG) infrastructure are generating structural, multi-year demand for high-performance mechanical seals in pumps, compressors, and rotating equipment across upstream, midstream, and downstream sectors. According to the International Energy Agency (IEA) World Energy Investment 2023 report, global upstream oil & gas investment reached approximately US$ 528 billion in 2023, with LNG liquefaction and regasification capacity additions representing one of the fastest-growing capital expenditure sub-categories.

Each LNG liquefaction train requires hundreds of cryogenic pump and compressor mechanical seals engineered to stringent low-temperature and high-pressure performance specifications. EagleBurgmann, John Crane Group, and Flowserve Corporation, key mechanical seal OEM suppliers to the LNG sector, have reported growing order backlogs from new LNG project awards in Qatar, Australia, the United States, and Mozambique, confirming the sector’s robust near-to-medium-term demand pipeline for specialized mechanical sealing solutions.

Restraints - High Initial Cost and Technical Complexity of Advanced Mechanical Seal Systems

Advanced double and tandem mechanical seal systems with support systems (API Plan 52, 53, 54) require substantially higher upfront capital investment compared to traditional packing or lip seal alternatives, creating adoption barriers particularly for small and medium-sized industrial operators in price-sensitive emerging markets. According to the Hydraulic Institute, total lifecycle cost of seal-related pump failures, including maintenance labor, replacement parts, and production downtime, remains a key decision parameter, yet the higher installed cost of premium mechanical seal systems continues to defer their adoption in cost-constrained industrial maintenance budgets across developing economies, limiting market penetration velocity in segments where payback period analysis is less systematically applied.

Availability of Alternative Sealing Technologies Creating Substitution Pressure

Magnetic drive pumps, which eliminate shaft penetration and the associated need for mechanical seals entirely, represent a growing substitution threat in chemical processing and pharmaceutical applications where zero-leakage requirements are paramount. The European Association of Pump Manufacturers (Europump) has noted increasing specification of magnetic drive pump configurations in new chemical plant designs, particularly for highly hazardous fluid handling. Additionally, lip seals and PTFE-based compression packing retain entrenched positions in low-pressure, low-hazard utility pump applications, constraining mechanical seals’ ability to fully displace legacy sealing technologies across the full spectrum of rotating equipment applications.

Opportunities - Water and Wastewater Infrastructure Expansion as a Sustained Demand Catalyst

Global investment in water and wastewater treatment infrastructure represents one of the most predictable and policy-supported long-term growth opportunities for the mechanical seals market. The United Nations projects that global water demand will exceed supply by 40% by 2030, driving massive public and private investment in water treatment, desalination, and wastewater reuse infrastructure. The U.S. Infrastructure Investment and Jobs Act (IIJA 2021) allocated US$ 55 billion specifically for water infrastructure modernization over a five-year period, encompassing pump station upgrades and new treatment plant construction, each representing direct mechanical seal demand. The European Commission’s Urban Wastewater Treatment Directive (UWWTD) revision, adopted in 2024, mandates secondary and tertiary treatment upgrades for over 2,000 European wastewater treatment plants by 2030, creating a decade-long pipeline of pump and mechanical seal upgrade activity. Water sector mechanical seals benefit from recurring aftermarket replacement demand, providing mechanical seal manufacturers with highly predictable, annuity-such as revenue streams alongside the initial equipment supply opportunity.

Pharmaceutical and Food & Beverage Sector Growth Spurring Demand for Hygienic Mechanical Seals

The global pharmaceutical and food & beverage manufacturing sectors represent high-value, rapidly growing end-markets for specialized hygienic mechanical seals designed to meet stringent sanitary design standards. The global pharmaceutical market is projected to exceed US$ 1.5 trillion by 2023 per the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), with continuous expansion of biologics, sterile injectables, and vaccine manufacturing capacity creating sustained demand for FDA 21 CFR-compliant and European Pharmacopoeia (Ph. Eur.)-compliant hygienic sealing solutions. Similarly, the Food and Agriculture Organization (FAO) reports food processing capacity expansions across Asia, Africa, and Latin America are generating new demand for EHEDG (European Hygienic Engineering & Design Group)- and 3-A Sanitary Standards-certified mechanical seals for pumps handling dairy, beverage, and processed food products. Freudenberg Sealing Technologies GmbH and Co. KG. and Garlock Sealing Technology have specifically expanded their hygienic seal product portfolios to capitalize on this growing demand, underscoring the commercial opportunity’s attractiveness for specialized mechanical seal manufacturers.

Category-wise Analysis

Product Type Insights

Cartridge seals represent the leading product type segment in the mechanical seals market, commanding approximately 38% of total market revenue in 2025. Cartridge mechanical seals, pre-assembled, self-contained sealing units that integrate the seal faces, springs, and gland in a single factory-set assembly, offer significant installation, maintenance, and reliability advantages over traditional component seals requiring field assembly. Their pre-set construction eliminates field measurement errors during installation, a primary cause of premature seal failure, resulting in meaningfully lower total lifecycle costs.

The American Petroleum Institute (API) Standard 682’s strong recommendation of cartridge seal configurations for general refinery service has systematically driven their specification as the default seal type in oil & gas, chemical, and power generation plant procurement standards. Major OEMs including John Crane Group and Flowserve Corporation report cartridge seals as their highest-volume product line by both unit count and revenue across all end-use industry segments they serve globally.

Design Insights

Single mechanical seals lead the design category with approximately 52% market share in 2025, reflecting their widespread specification in the broadest range of industrial pump and rotating equipment applications where the process fluid is non-hazardous, non-toxic, and leakage to atmosphere is permissible within regulatory thresholds. Single mechanical seals offer the simplest installation, lowest purchase cost, and most straightforward maintenance profile of all design configurations, making them the default specification choice for water & wastewater, pulp & paper, and general-purpose utility pump applications. However, double and tandem seal configurations are the fastest growing design sub-segment, as expanding fugitive emission regulations under EPA LDAR and EU IED frameworks increasingly mandate zero-leakage sealing arrangements for volatile or hazardous fluid services in chemical, petrochemical, and oil & gas applications, systematically shifting specification patterns toward more complex multi-seal configurations in high-risk process streams.

Application Insights

Pumps represent the dominant application segment for mechanical seals, accounting for approximately 58% of total market revenue in 2025. Centrifugal pumps, the most widely deployed pump type in global process industries, represent the single largest application category for mechanical seals, with virtually every centrifugal pump handling liquid process fluids requiring a shaft sealing solution. The Hydraulic Institute estimates that there are over 700 million pumps operating globally across all sectors, with the majority utilizing mechanical seals as the primary shaft sealing solution in process and utility service applications. The API 610 standard for centrifugal pumps in petroleum, petrochemical, and natural gas industries explicitly references API 682 mechanical seal configurations, ensuring pumps represent a sustainably dominant application segment for mechanical seal manufacturers across the broadest range of end-use industries and geographies served by the global pump installed base.

Industry Insights

The oil & gas industry leads the mechanical seals market end use industry segment with approximately 28% of total market revenue in 2025, reflecting the sector’s extraordinarily high installed base of pumps, compressors, and rotating equipment requiring regular mechanical seal maintenance, replacement, and specification upgrades. Upstream oil & gas operations, encompassing onshore and offshore production platforms, alongside midstream pipelines and downstream refining facilities collectively represent the largest single source of mechanical seal demand globally, driven by both new equipment supply through OEM channels and an active and recurring aftermarket replacement cycle. The IEA’s projection of continued oil & gas production investment through 2030 to meet global energy transition requirements, combined with the sector’s adoption of increasingly stringent emission performance requirements under API 682 5th Edition, ensures oil & gas maintains its leading end-use position through the forecast period.

Distribution Channel Insights

The aftermarket distribution channel leads the mechanical seals market with approximately 62% of total revenue share in 2025, reflecting the highly recurring, non-discretionary nature of mechanical seal replacement demand in operating industrial plants. Mechanical seals are wear components with defined operational lifespans, typically ranging from 6 to 36 months depending on service severity, fluid characteristics, and operating conditions, necessitating regular replacement cycles that generate predictable aftermarket revenue streams independent of new equipment capital expenditure cycles.

Industrial MRO (Maintenance, Repair & Operations) distributors, including Grainger, MSC Industrial, and regional specialist distributors, represent major aftermarket channel partners for mechanical seal brands. Leading manufacturers including AW Chesterton Company and AESSEAL plc have invested heavily in digital aftermarket platforms offering rapid cross-referencing, predictive maintenance advisory services, and expedited delivery capabilities to capture and retain aftermarket share in an increasingly competitive distribution landscape.

Regional Insights

North America Mechanical Seals Market Trends and Insights

North America is the leading regional market for mechanical seals, holding approximately 32% of global revenue share in 2025, anchored by the United States’ world-class oil & gas, chemical, pharmaceutical, and water infrastructure sectors. The U.S. EPA’s stringent LDAR requirements under 40 CFR Part 60 and Part 63 are among the most comprehensive fugitive emission regulatory frameworks globally, systematically compelling refinery and chemical plant operators to upgrade sealing systems and maintain rigorous seal performance monitoring programs. The U.S. Inflation Reduction Act (IRA)’s methane emissions reduction provisions, imposing escalating fees on methane emissions from oil & gas operations starting at US$ 900 per metric ton in 2024 and rising to US$ 1,500 per metric ton by 2026, are creating direct financial incentives for oil & gas operators to invest in advanced double and tandem seal systems that minimize fugitive methane emissions at pump and compressor shafts.

Canada’s oil sands and LNG export project pipeline, including the LNG Canada Phase 1 project in British Columbia, which commenced commercial operations in 2025, represents a significant source of cryogenic and high-pressure mechanical seal demand. The U.S. water infrastructure modernization program funded through the Infrastructure Investment and Jobs Act is generating sustained mechanical seal demand across municipal water and wastewater pump station upgrades. North America’s mature industrial aftermarket, serviced by established regional distributors and direct manufacturer service networks, provides a high-margin recurring revenue base for mechanical seal manufacturers, with John Crane Group, Flowserve Corporation, and Parker Hannifin Corp maintaining the region’s strongest installed base and aftermarket service capabilities.

Europe Mechanical Seals Market Trends and Insights

Europe represents a mature but technically sophisticated mechanical seals market, holding approximately 26% of global revenue share in 2025. Germany, as Europe’s largest chemical and industrial manufacturing hub, home to BASF, Covestro, and numerous Mittelstand industrial equipment manufacturers, represents the region’s single largest national demand center. The European Industrial Emissions Directive (IED) and its sector-specific Best Available Techniques Reference Documents (BREFs) for refining, chemicals, and large combustion plants effectively mandate mechanical seals as the BAT (Best Available Technology) for fugitive emission control in rotating equipment, creating a comprehensive regulatory floor for mechanical seal specification across European process industries. EagleBurgmann (a subsidiary of the Freudenberg Group and KSB SE) and Trelleborg Industries maintain dominant market positions in European industrial and power generation applications respectively.

The United Kingdom’s offshore oil & gas sector, regulated by the North Sea Transition Authority (NSTA), continues to generate specialized mechanical seal demand for subsea and topside rotating equipment, despite mature field production profiles. France’s significant nuclear power generation fleet, operated by EDF across 56 operational reactors, represents a highly specialized, high-criticality application for nuclear-grade mechanical seals with stringent qualification requirements under ASME Section III and RCC-M codes. Spain, Italy, and Eastern Europe represent emerging growth sub-markets within the region, driven by expanding pharmaceutical manufacturing capacity and EU-funded water infrastructure upgrades under the EU Cohesion Fund and Recovery and Resilience Facility (RRF) programs, which allocate significant capital toward water sector modernization.

Asia Pacific Mechanical Seals Market Trends and Insights

Asia Pacific is the fastest growing mechanical seals market, projected to expand at a CAGR of approximately 6.5% through 2033, driven by accelerating industrialization, oil & gas infrastructure development, power generation capacity additions, and water treatment investment across China, India, South Korea, Japan, and ASEAN economies. China, as the world’s largest chemical manufacturing nation by output, represents the single largest mechanical seal demand market in Asia Pacific, with its expansive petrochemical complex developments along the Yangtze River Delta and Pearl River Delta corridors generating consistent OEM and aftermarket seal demand. China’s 14th Five-Year Plan explicitly targets chemical industry upgrades for safety and environmental compliance, driving systematic replacement of legacy sealing systems with modern mechanical seal configurations meeting international standards.

India’s mechanical seals market is growing rapidly, propelled by the government’s Jal Jeevan Mission, targeting universal household tap water connections by 2024 with pump infrastructure investment across 600,000+ villages, and the expanding refinery and petrochemical sector including Indian Oil Corporation’s (IOCL) refinery expansion programs and Reliance Industries’ Jamnagar complex. Japan’s precision engineering heritage sustains a high-quality domestic mechanical seal manufacturing sector, with companies including Eagle Industry Co., Ltd., a major affiliate of the NOK Corporation group, serving both domestic and export automotive and industrial markets. ASEAN’s growing refining, LNG, and pharmaceutical manufacturing sectors are creating new demand pools for international mechanical seal brands establishing regional manufacturing and distribution footprints.

Competitive Landscape

The global mechanical seals market exhibits a moderately consolidated structure, with a limited number of technologically advanced multinational players dominating the high-value industrial and oil & gas segments. These companies leverage proprietary sealing technologies, compliance with stringent industry standards, and extensive global service networks to maintain strong market positions. Their focus remains on delivering high-performance, reliability-driven solutions tailored for critical applications.

In contrast, the standard-grade and aftermarket segments are highly fragmented, characterized by strong competition from regional manufacturers, particularly across Asia, competing primarily on cost efficiency and localized supply capabilities. Competitive differentiation increasingly centers on advanced seal face materials, integration of digital monitoring and predictive maintenance solutions, and strong OEM partnerships with equipment manufacturers. Additionally, companies are expanding lifecycle-based offerings, including maintenance contracts and seal management services, to secure recurring revenue streams and enhance long-term customer retention.

Key Developments:

- September 2025: John Crane unveiled its Type 8628VL next-generation mechanical seal for ethane pipelines, featuring spiral groove non-contacting technology to enhance reliability, reduce leakage, and improve operational efficiency under fluctuating pressure and temperature conditions.

- June 2025: John Crane launched its next-generation Type 93AX coaxial separation seal, designed to reduce emissions, improve equipment reliability, and cut nitrogen consumption by up to 80%, enhancing efficiency and sustainability across energy and process industries.

- January 2025: Sealmatic India secured a major order to supply supercritical mechanical seals for critical industrial applications, marking a significant milestone in strengthening its position in high-performance sealing solutions for energy and process industries.

Companies Covered in Mechanical Seals Market

- AW Chesterton Company

- Dana Corporation

- EagleBurgmann (Freudenberg-KSB Joint Venture)

- Flowserve Corporation

- John Crane Group

- Freudenberg Sealing Technologies GmbH and Co. KG.

- Cooper-Standard

- Gallagher Seals

- Garlock Sealing Technology

- Bal Seal Engineering

- Trelleborg Industries

- Flexitallic Group

- Dover Corporation

- Flex-a-seal

- Parker Hannifin Corp

- SKF Group

- AESSEAL plc

- Sulzer Ltd.

Frequently Asked Questions

The mechanical seals market is projected to reach US$ 7.4 billion in 2026.

Demand is driven by emission regulations and growth in oil & gas and industrial infrastructure.

North America leads the market with the highest revenue share.

Opportunities lie in water infrastructure upgrades and hygienic applications in pharma and food industries.

Key companies in the global Mechanical Seals market include John Crane Group, EagleBurgmann, Flowserve Corporation, Freudenberg Sealing Technologies GmbH and Co. KG., Parker Hannifin Corp, AW Chesterton Company, etc.