- Advanced Materials

- Magnesium Oxide Market

Magnesium Oxide Market Size, Share, and Growth Forecast for 2025 - 2032

Magnesium Oxide Market By Product Type (Dead Burned Magnesia (DBM), Others), Application (Refractories, Others), End-user Industry (Iron & Steel, Cement & Glass, Non-ferrous Metallurgy, and Others), Regional Analysis for 2025 - 2032

Magnesium Oxide Market Size and Trends Analysis

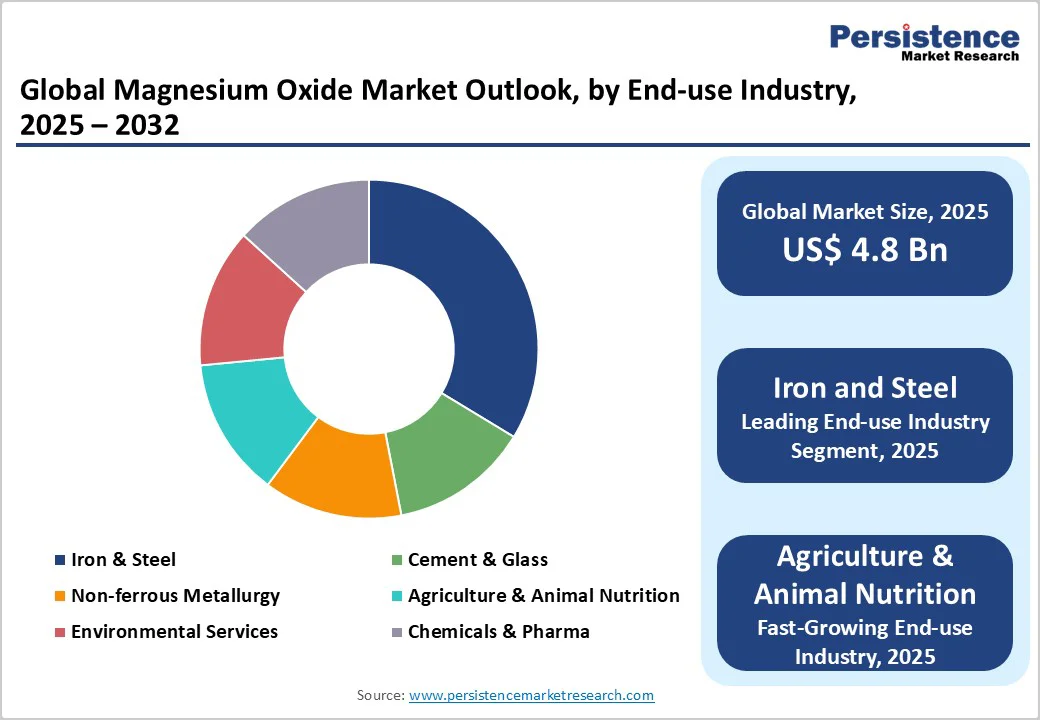

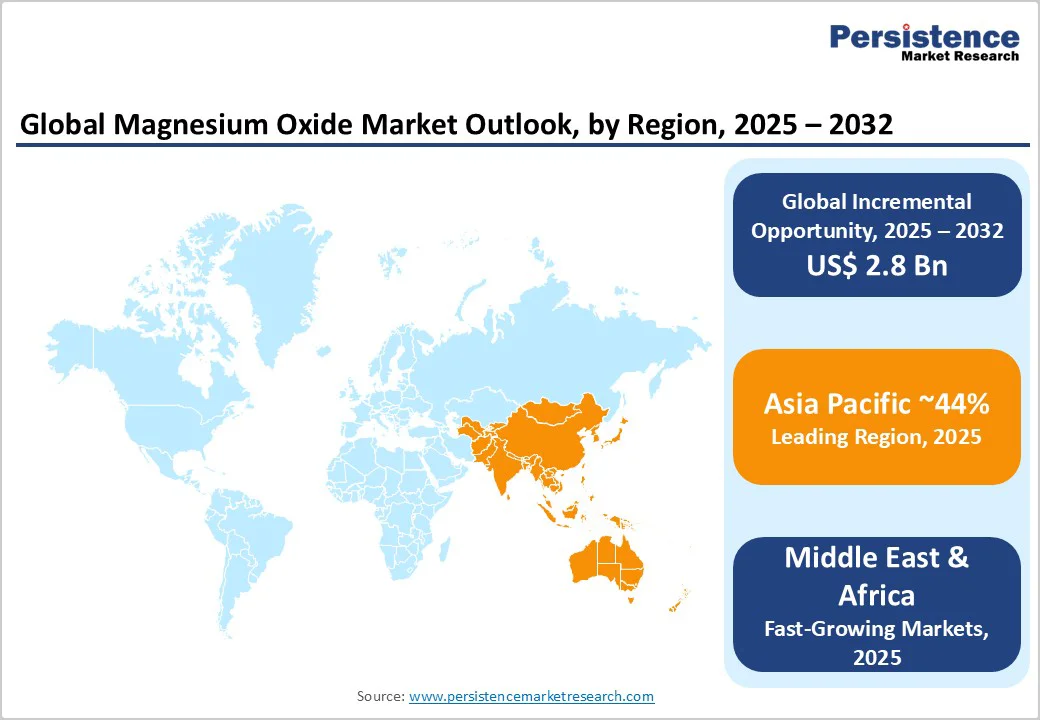

The global magnesium oxide market is expected to reach US$4.8 billion in 2025. It is expected to reach US$7.6 billion by 2032, growing at a CAGR of 6.8% during the forecast period from 2025 to 2032, driven by the growing demand from the construction and refractory sectors, expanding applications in flue gas desulfurization and wastewater treatment, and increasing use in agriculture and pharmaceuticals for soil conditioning and supplements.

Key Industry Highlights:

- Regional Leaders: Asia Pacific is the largest and fastest-growing region, capturing a 44% market share in 2025. Growth is fueled by China, India, and Japan, supported by extensive magnesite reserves, industrial expansion, and government initiatives promoting eco-friendly and fire-resistant building materials.

- Leading Segments: Dead Burned Magnesia (DBM) holds a dominant position with approximately 40% share, primarily due to its high melting point, chemical inertness, and critical use in refractory linings for iron, steel, and cement industries.

- Industry Applications: The refractories segment leads with around 35% share, underpinned by the expansion of global steel and cement production.

- Market Drivers: The construction sector continues to drive demand for MgO due to its fire-resistant and sustainable properties, enabling lightweight, durable, and eco-friendly building materials.

- Market Restraints: High production costs, caused by raw material price volatility (magnesite and dolomite) and the energy-intensive calcination and fusion processes, constrain market expansion.

- Market Opportunities: Magnesium Oxide Nanopowder is gaining traction across pharmaceuticals, cosmetics, and electronics, offering enhanced thermal stability, catalytic activity, and functional versatility.

| Key Insights | Details |

|---|---|

| Magnesium Oxide Market Size (2025E) | US$4.8 Bn |

| Projected Market Value (2032F) | US$7.6 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 6.8% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Demand from the Construction Industry Due to Its Fire-Resistant and Sustainable Properties

The construction sector continues to be the largest consumer of magnesium oxide (MgO), primarily due to its versatile performance in cement and fire-resistant applications. MgO’s high melting point, excellent thermal insulation, and chemical stability make it a preferred additive for producing high-performance cements, including sustainable and eco-friendly alternatives to conventional Portland cement. Governments in China and India are actively promoting the use of green building materials to reduce carbon footprints and enhance energy efficiency in construction.

For instance, public infrastructure projects increasingly incorporate MgO-based cements, which provide better resistance to fire and corrosion while enabling lightweight structures. This adoption is driving an estimated 10-15% year-over-year growth in MgO cement usage, boosting the overall market. In addition, MgO’s ability to improve durability, dimensional stability, and resistance to cracking further solidifies its role in high-end construction, particularly in high-rise buildings, tunnels, and industrial facilities.

Increasing Use of Magnesium Oxide in Environmental Applications Due to Stricter Emission and Water Pollution Regulations

Stricter environmental regulations on emissions, water quality, and industrial effluents are significantly increasing the use of magnesium oxide in environmental applications. MgO’s strong alkaline and neutralizing properties make it an ideal material for flue gas desulfurization (FGD) in thermal power plants, where it reacts efficiently with sulfur dioxide (SO2) to form magnesium sulfite and sulfate, and reduces SO2 emissions by up to 95%. This capability enables industries to comply with stringent emission norms enforced by agencies such as the U.S. Environmental Protection Agency (EPA) and the European Union Industrial Emissions Directive (IED).

In the wastewater treatment sector, magnesium oxide is increasingly replacing lime and caustic soda due to its higher neutralization efficiency, lower sludge generation, and reduced handling hazards. It effectively removes heavy metals, ammonia, and phosphates, ensuring compliance with stricter water discharge standards in regions such as North America, Europe, Japan, and South Korea. Furthermore, as industries transition toward sustainable production, the use of MgO aligns with circular economy principles; its by-products can often be repurposed or safely disposed of without environmental harm.

The global shift toward low-carbon and eco-friendly materials has further reinforced the importance of magnesium oxide, especially in applications where lightweight, non-toxic, and recyclable materials are prioritized, such as in the magnesium alloy market and industrial filtration systems. Together, these factors are propelling the expansion of MgO demand in environmental technologies, transforming it from a niche neutralizing agent into a critical enabler of industrial sustainability and environmental compliance.

Barrier Analysis - Raw Material Price Volatility and Energy-Intensive Manufacturing

The market is significantly constrained by high production costs, primarily stemming from fluctuating raw material prices and the energy-intensive nature of MgO manufacturing. The key raw materials, magnesite and dolomite, are prone to price volatility due to factors such as mining challenges, environmental restrictions, and geopolitical disruptions in major producing countries such as China and Turkey. These price fluctuations directly affect the overall production economics, making it difficult for manufacturers, especially small and mid-sized producers, to plan long-term investments or expand production capacity.

The calcination and fusion processes required to produce high-purity magnesium oxide demand substantial energy inputs, with electricity and fuel costs accounting for a large portion of operational expenses. In regions with high energy tariffs, particularly Europe, producers face reduced profitability and slower market penetration compared to cost-competitive regions such as Asia-Pacific. The combined effect of raw material cost instability and rising energy consumption increases manufacturing expenses, thereby restricting the overall growth potential of the magnesium oxide market.

Opportunity Analysis - Emerging Applications of Magnesium Oxide Nanopowder across Several Industries

Technological advancements in magnesium oxide nanopowder are unlocking new applications across the pharmaceutical, cosmetic, and electronic sectors. These nanoparticles offer superior surface area, enhanced thermal stability, and excellent catalytic activity, enabling their use in advanced formulations and functional materials.

In pharmaceuticals, MgO nanopowders serve as antibacterial agents, drug carriers, and excipients, improving drug delivery efficiency and bioavailability. Their biocompatibility and non-toxic nature make them ideal for use in wound dressings, dental care, and controlled-release drug systems. In the cosmetics industry, magnesium oxide nanopowders are increasingly used in UV-protection creams, deodorants, and skin-soothing formulations, leveraging their high absorbency and antimicrobial characteristics.

The electronics sector is witnessing growing adoption of MgO nanopowder in semiconductor devices, sensors, and dielectric coatings due to its excellent insulating and heat-resistant properties. This technological evolution positions MgO nanopowder as a key driver of innovation and premiumization within the broader magnesium oxide market.

Integration of Magnesium Oxide in High-Performance Magnesium Alloys

The robust expansion of the magnesium alloy market presents a significant opportunity for magnesium oxide (MgO) producers. MgO is increasingly being utilized as a reinforcing and coating agent to enhance the strength, corrosion resistance, and thermal stability of magnesium alloys.

These alloys are gaining traction in the automotive and aerospace industries, where the push for lightweight materials is central to achieving fuel efficiency and lower carbon emissions. For instance, substituting aluminum or steel components with magnesium alloys can reduce overall vehicle weight by up to 30%, directly contributing to improved mileage and reduced emissions.

In the aerospace sector, MgO-reinforced alloys are being explored for use in engine casings, gear housings, and structural components, where high temperature resistance and dimensional stability are critical. Additionally, the integration of MgO coatings improves oxidation resistance, extending the service life of magnesium alloy parts. This integration not only expands MgO’s application base but also strengthens its position as a strategic material supporting the global transition toward lightweight and sustainable engineering solutions.

Category-wise Analysis

Product Type Insights

Among product types, Dead Burned Magnesia (DBM) holds a commanding position in the market, accounting for approximately 40% of the total demand. DBM is produced by high-temperature calcination (above 1,800°C) of magnesite or dolomite, resulting in a dense, chemically inert, and heat-resistant material.

Its exceptionally high melting point, exceeding 2,800°C, and superior resistance to slag and corrosion make it indispensable for use in refractory linings within iron, steel, and cement industries. These characteristics enable DBM to withstand extreme thermal shocks and aggressive chemical environments, ensuring longer service life and reduced maintenance in furnaces and kilns.

Application Insights

The refractories segment remains the largest application area for magnesium oxide, contributing roughly 35% of global market share. MgO’s unique thermal and chemical stability make it an essential raw material for furnace linings, kilns, and reactors used in steelmaking, glass, and cement manufacturing.

Its incorporation enhances the thermal endurance and durability of refractory bricks, reducing wear and tear from molten metal and slag. The growth in global steel production, particularly in China, India, and Southeast Asia, continues to drive MgO consumption in refractories. The expansion of cement manufacturing capacities in emerging economies supports steady market demand.

End-user Industry Insights

The iron and steel industry represents the largest end-use segment for magnesium oxide, accounting for nearly 38% of global demand. Refractory-grade MgO is critical for lining basic oxygen furnaces, electric arc furnaces, and ladles, where it helps maintain structural integrity under extreme temperatures and prevents slag corrosion.

The close correlation between global steel output and MgO consumption ensures steady market growth, with major steel-producing nations, such as China, India, Japan, and South Korea, serving as key demand centers.

Regional Insights

North America Magnesium Oxide Market Trends

North America, led by the U.S., is witnessing growth driven by stringent environmental laws and innovations in refractory technologies. The Environmental Protection Agency’s (EPA) emphasis on emission reductions has increased the implementation of MgO-based materials in wastewater and air pollution control systems. The region’s advanced manufacturing and construction sectors continue to adopt sustainable solutions where MgO plays a vital role.

Europe Magnesium Oxide Market Trends

Europe’s market growth is supported by Germany’s continued dominance in production and application, particularly in the refractory and agriculture sectors. Regulatory harmonization under EU standards promotes consistent quality and environmental compliance, encouraging the adoption of MgO in green construction and industrial processes. The U.K., France, and Spain are notable contributors to the development of advanced MgO materials aligned with sustainability goals.

Asia Pacific Magnesium Oxide Market Trends

Asia Pacific holds the largest share globally, especially driven by China’s extensive magnesite reserves and industrial base. Growing demand from steel, cement, and environmental sectors in China, India, and Japan underpins regional market leadership. Investments in infrastructure and urbanization projects elevate MgO requirements, while manufacturing cost advantages in the region intensify its competitive edge.

Competitive Landscape

The global magnesium oxide market is moderately consolidated, with major companies focusing on capacity expansion, backward integration, and R&D to develop specialty grades. Leading players differentiate through product purity, energy-efficient manufacturing, and tailored solutions for specialized applications, including nanopowder innovations. Emerging trends include collaborations for sustainable production and licensing of proprietary technologies to expand global reach.

Recent Industry Developments

- In March 2025, Premier Magnesia announced a 15% increase in its Dead Burned Magnesia (DBM) production capacity at its U.S. facilities to address the growing demand from the refractories sector. This expansion involved upgrading calcination and grinding units, enabling higher throughput while maintaining consistent product purity and particle size distribution.

- In September 2024, ICL Group introduced a new line of environmentally friendly magnesium oxide products specifically designed for water and wastewater treatment applications. These MgO grades are engineered for high neutralization efficiency and low solubility, enabling improved removal of acidic pollutants, heavy metals, and phosphates from industrial effluents.

- In January 2024, Martin Marietta Materials announced a major research and development initiative targeting magnesium oxide nanopowder for advanced industrial applications. The focus is on producing ultra-fine MgO particles with controlled surface properties, suitable for catalysis, high-performance ceramics, and electronics.

Companies Covered in Magnesium Oxide Market

- RHI Magnesita

- Martin Marietta Materials

- Magnezit Group

- Grecian Magnesite

- Ube Corporation

- Nedmag

- ICL Group

- Premier Magnesia

- Kumas Magnesite

- Xinyang Mineral Group

- Imerys

- Haicheng Magnesite Group

- Russian Mining Chemical Company

- SMZ Jelsava

- Dandong Jinyuan Group

Frequently Asked Questions

The magnesium oxide market is projected to reach US$7.6 Billion by 2032 with a CAGR of 6.8% from 2025.

The construction sector, due to MgO’s fire-resistance and insulation properties, remains the primary growth driver.

Dead Burned Magnesia (DBM) dominates owing to its critical role in refractory applications.

Asia Pacific leads the market, particularly driven by high industrial consumption in China and India.

Expanding applications of magnesium oxide nanopowder in pharmaceuticals and technology sectors offer significant growth potential.

Leading companies include RHI Magnesita (Luxembourg), Martin Marietta Materials (U.S.), and Magnezit Group (Russia).