- Metals & Minerals

- Magnesium Alloy Market

Magnesium Alloy Market Size, Share, and Growth Forecast for 2025 - 2032

Magnesium Alloy Market By Alloy Type (Wrought Alloys, Cast Alloys), Application (Automotive & Transportation, Aerospace & Defense, Construction, Electrical & Electronics, Packaging, Marine, Consumer Goods, Others), and Regional Analysis for 2025 - 2032

Magnesium Alloy Market Size and Trends

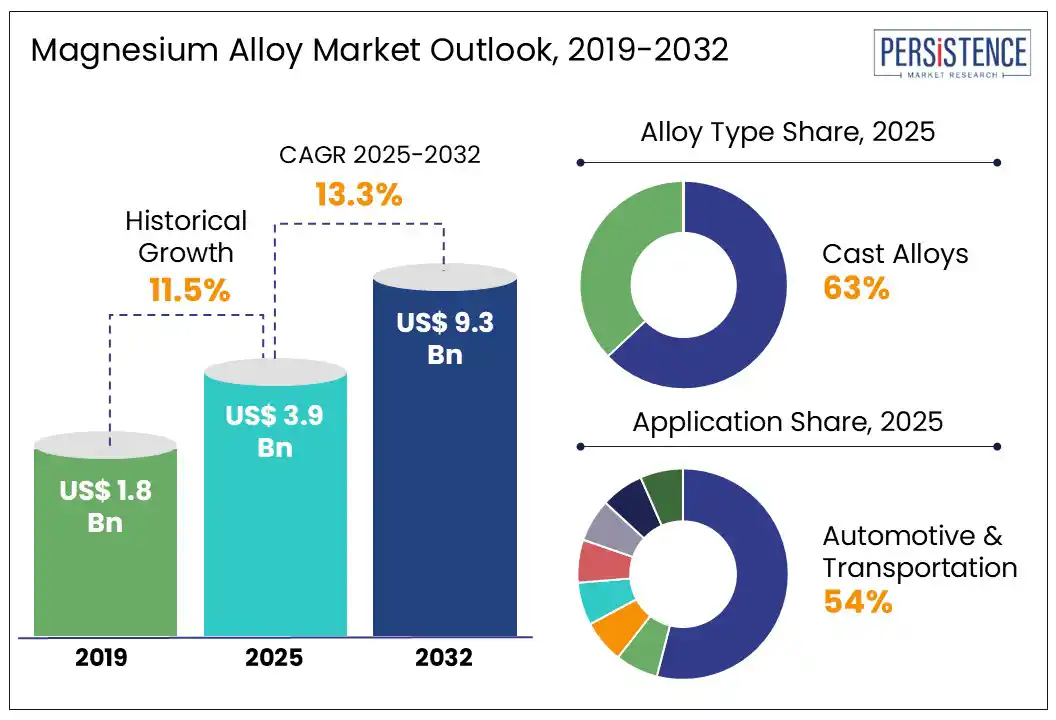

The global magnesium alloy market size is likely to be valued at US$ 3.9 Bn in 2025 and is estimated to reach US$ 9.3 Bn in 2032, growing at a CAGR of 13.3% during the forecast period 2025 - 2032. From aerospace to automotive, electronics, and medical devices, magnesium alloys are redefining the future of high-performance engineering. Weighing 30-35% less than aluminum and nearly 60% lighter than titanium, these alloys offer an unmatched strength-to-weight ratio, superior thermal stability, and mechanical integrity outperforming many plastics and composites such as PEEK.

Between 2019 and 2024, the market witnessed a CAGR of 11.5%, however the pace is further accelerating. As industries aggressively chase fuel efficiency, component miniaturization, and sustainability goals, magnesium alloys are becoming a game-changing material for next-gen product design and manufacturing.

Key Industry Highlights:

- Magnesium alloys are widely adopted in EV components such as engine cradles and battery housings. Automakers such as Tesla and SAIC are prioritizing these alloys for light weighting and fuel efficiency.

- Aerospace and defense sectors increasingly adopt magnesium alloys for aircraft fuselage parts and landing gears. These applications reduce weight, increase payload capacity, and improve fuel economy.

- Consumer electronics manufacturers use magnesium alloys for devices requiring thermal management and durability. Apple and Lenovo utilize magnesium frames in lightweight laptops, smartphones, and tablets.

- Magnesium’s biocompatibility enables its use in orthopedic implants and cardiovascular stents.

- FDA approvals are accelerating the medical adoption of biodegradable magnesium devices.

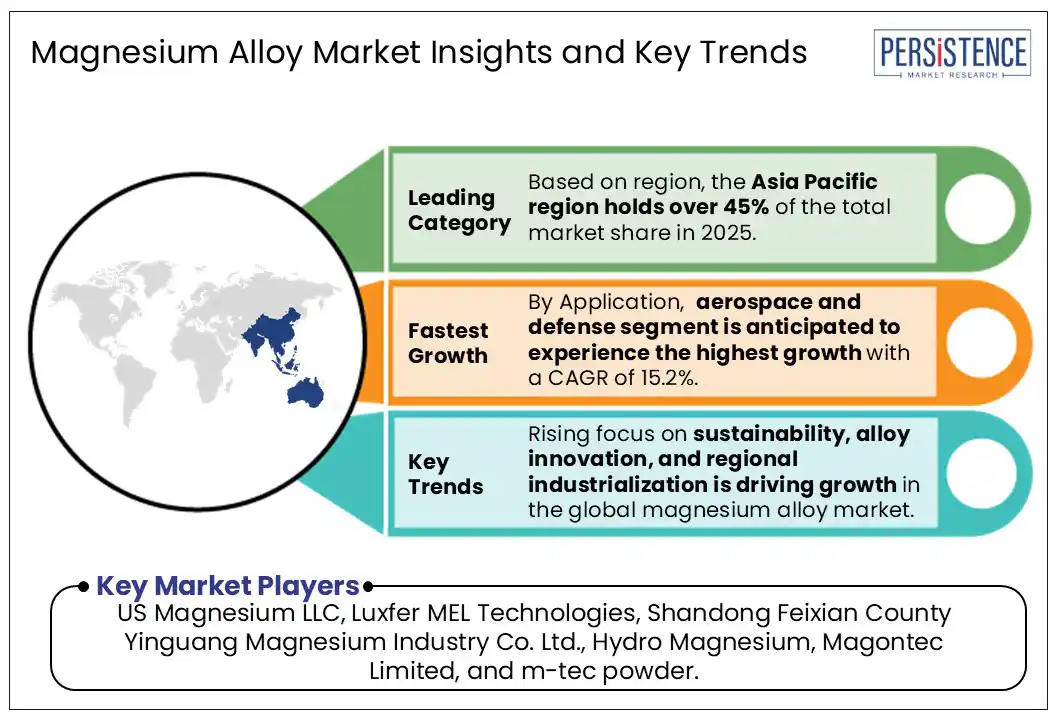

- Asia Pacific is anticipated to hold over approximately 45% market share in 2025, with China leading production due to vast reserves, government policy, and a mature industrial base.

- Sustainability concerns are promoting magnesium recycling in the U.S. and Europe. Circular economy efforts are supported by scrap reuse programs and low-carbon material initiatives.

- Wrought magnesium alloys offer better ductility and are ideal for structural and precision applications, making them popular in the aerospace and transportation industries.

- OEMs are forging partnerships with alloy producers to co-develop next-generation magnesium solutions.

|

Global Market Attribute |

Key Insights |

|

Magnesium Alloy Market Size (2025E) |

US$ 3.9 Bn |

|

Market Value Forecast (2032F) |

US$ 9.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

13.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.5% |

Market Dynamics

Drivers - Growing Demand in the Automotive Industry

The automotive industry is a significant driver of the magnesium alloy market due to stringent emission regulations and the global trend toward lightweight vehicles. Magnesium alloys offer a superior strength-to-weight ratio, making them suitable for engine blocks, transmission cases, and EV structural components. Automakers use these alloys to improve fuel efficiency and enhance performance. In 2025, SAIC Motor introduced a mass-produced magnesium alloy case for electric drive systems, utilizing a semi-solid AZ91D alloy, which weighs just 13.7 kg. Tesla and Audi also integrate magnesium components for energy efficiency.

Magnesium alloys are witnessing increased adoption across aerospace, defense, and consumer electronics sectors owing to their lightweight nature, structural strength, and energy efficiency benefits. In aerospace and defense, these alloys are used in aircraft fuselage components, landing gear systems, satellite parts, and reusable space vehicles to reduce fuel consumption, improve payload capacity, and lower launch costs.

Companies such as Airbus and Luxfer MEL Technologies have started utilizing specialized alloys such as Elektron® 43 and 21 in commercial and space-grade applications. Major OEMs such as Apple and Lenovo have incorporated magnesium alloy frames into their products, leveraging recyclability and design flexibility.

Restraint - Magnesium Alloy Adoption is Limited by High Costs, Corrosion Issues, and Poor Room-temperature Formability

The high cost of raw materials and price volatility act as major market restraints. Magnesium production is energy-intensive and depends on limited sources such as dolomite and brine. With China being the largest supplier, environmental regulations and output restrictions often cause global price spikes. For instance, in 2022, China's production curbs led to a sharp increase in magnesium prices, disrupting supply chains and raising input costs worldwide.

Another restraint is the inherent corrosion susceptibility and poor weldability of magnesium alloys. They corrode rapidly in moist or saline environments, requiring expensive protective coatings, which increases processing costs. Automakers such as BMW apply anti-corrosion coatings on magnesium engine parts, but these processes add to production complexity and time. Although new coating technologies and hybrid welding methods are under development, they are not yet cost-effective for large-scale use.

Magnesium alloys also suffer from limited formability at room temperature due to their hexagonal close-packed (HCP) crystal structure. This necessitates advanced processes such as thixomolding, increasing tooling costs. For example, Ford employed hot-forming techniques for magnesium parts in the F-150, but the high cost and complexity limited broader deployment. Such limitations restrict magnesium alloy adoption in regions including Japan, known for precision manufacturing.

Opportunity - Rising Demand from EVs and the Automotive Sector Offers Massive Upside for Magnesium Alloy Suppliers

As automakers increasingly prioritize vehicle light weighting for improved fuel economy and electrification, magnesium alloys, which are 32% lighter than aluminum, are becoming the material of choice for critical components such as wheels, seat frames, transmission cases, and engine cradles. For example, GM uses AE44 magnesium alloy in the Chevrolet Z06 Corvette for weight reduction and performance enhancement.

The rapid expansion in the EV market, which is projected to grow at a 14.6% CAGR between 2025 and 2032, also strengthens the magnesium alloy market. Drivers include advancements in battery technology, economies of scale in EV manufacturing, and declining vehicle costs that make EVs more accessible. Meanwhile, zero-emission mandates, tighter emission regulations, and generous government incentives are accelerating EV adoption, particularly in Europe, China, and North America, where charging infrastructure and policy frameworks are rapidly advancing.

Magnesium alloy suppliers align their offerings with EV-specific needs such as lightweight battery casings, motor housings, and chassis components. Strategic collaborations, such as CATL’s 2019 magnesium material joint venture, highlight the importance of integrating into the evolving EV supply chain.

Magnesium alloy manufacturers can also tap into high-growth verticals such as biomedical devices and advanced manufacturing technologies. Magnesium’s biocompatibility and biodegradability make it ideal for orthopedic implants, cardiovascular stents, and surgical screws, which naturally dissolve in the body, reducing the need for follow-up surgeries. The FDA’s Breakthrough Device designation for Magnesium Development Company’s bioresorbable HC orthopedic screw validates its clinical potential and paves the way for faster regulatory review and broader adoption in orthopedic care.

Category-wise Insights

Alloy Type Insights

Based on alloy type, the cast alloys segment is anticipated to dominate, accounting for a market share of approximately 63% in 2025, due to its widespread use in automotive, aerospace, and electronics applications, where lightweight and durable components are critical for energy efficiency and performance Cast alloys are produced by pouring molten magnesium into a mold, allowing it to solidify into the desired shape. These alloys typically contain aluminum, manganese, and zinc, each contributing to strength, corrosion resistance, and durability. Advanced compositions including zirconium and rare-earth metals have recently incorporated to enhance creep resistance, especially in high-temperature applications. Heat treatments further improve the mechanical properties of cast magnesium alloys, making them suitable for complex geometries in engine blocks, housings, and structural components.

The wrought magnesium alloys undergo mechanical deformation processes such as forging, extrusion, and rolling to achieve the required shapes and mechanical characteristics. These alloys use aluminum, manganese, and zinc as base alloying elements and are classified into heat-treatable and non-heat-treatable variants. Wrought alloys offer superior ductility and a clean-surface finish compared to cast alloys, making them ideal for structural applications in aerospace and transportation sectors where formability and strength-to-weight ratio are key performance factors.

Application Insights

By application, the automotive & transportation segment is expected to remain the dominant end-use sector, accounting for over 54% of the total market share by 2025. This is driven by the growing emphasis on lightweight materials that enhance fuel efficiency and support emission reduction goals, particularly in electric and hybrid vehicles.

Magnesium alloys are increasingly adopted across industries due to their advantageous properties, including low density (1.8 g/cm³), high strength-to-weight ratio, excellent castability, thermal conductivity, and recyclability. These attributes make them highly suitable for lightweight structural automotive parts such as engine cradles, transmission housings, seats, steering columns, and dashboard components. Despite the production costs, process limitations, and stringent regulatory standards, the push toward sustainable mobility will accelerate its market penetration.

In the aerospace and defense sector, alloys such as WE43, RZ5, MSR, and EQ21 are gaining traction for use in rotor gearboxes, compressor casings, and auxiliary systems, with WE43 increasingly replacing legacy alloys in platforms such as the Sikorsky S92 and Eurocopter EC120. In motorsports, advanced alloys such as WE54 are used in high-performance applications, including Formula-one engine components and forged pistons, due to their superior strength and thermal resistance.

Regional Insights

Asia Pacific Magnesium Alloy Market Trends

The Asia Pacific region will continue to lead the market, holding over 45% of the total market share in 2025. This leadership stems from rapid urbanization, the region’s strong manufacturing base, and expanding end-use industries such as automotive, aerospace, and consumer electronics. Countries including China, Japan, and South Korea have become global hubs for magnesium alloy production, supported by rising demand for lightweight materials in EVs, aircraft structures, and portable devices. China remains at the forefront, contributing nearly 80-90% of global primary magnesium production, followed by India and Japan.

Automotive demand is particularly strong, with over 49 million vehicles produced in Asia in 2023. Magnesium alloys are increasingly used in EV battery casings, structural parts, and lightweight frames. Similarly, the electronics and aerospace sectors are driving the demand for high-precision, corrosion-resistant magnesium components. Healthcare applications such as biodegradable implants are also gaining momentum. Key regional players include Shanghai Regal Magnesium Ltd., Taiyuan Tongxiang Magnesium Co., and Nippon Kinzoku Co.

Government support has been pivotal. China’s MIIT lists magnesium alloys as strategic, with dedicated clusters in Shaanxi and Xinjiang, while Japan and India offer incentives under green and manufacturing initiatives. China’s 3.4 billion tonnes of magnesite reserves and export leadership with 58% of magnesium exports in May 2025 solidify Asia Pacific’s role.

North America Magnesium Alloy Market Trends

North America holds a significant position in the global magnesium alloy market. The region’s robust automotive industry continues to be a major driver of magnesium alloy demand, particularly due to the increasing need for lightweight materials to enhance fuel efficiency and meet stringent emission norms.

According to the National Automobile Dealers Association (NADA), North America's automotive sector generates over US$ 500 Bn in annual sales and supports over 1.7 million jobs. Despite challenges such as fluctuating sales, rising vehicle prices, and shifting consumer preferences, the industry has adapted through advancements in EV technologies and material engineering. The region produces over 17 million vehicles annually, making it one of the largest manufacturing bases globally. This sustained output, combined with the rising demand for electric and fuel-efficient vehicles, is propelling the adoption of magnesium alloys.

Competitive Landscape

The global magnesium alloy market is advancing rapidly, driven by facility expansions, technology upgrades, and strategic partnerships across the automotive, aerospace, and industrial sectors. Manufacturers are strengthening R&D and collaborating with OEMs to co-develop advanced, lightweight alloys for next-generation vehicles. Growth in Asian production hubs is boosting supply for mobility and aerospace, while innovations in high-strength magnesium alloys are enhancing durability and performance in critical applications.

Key Industry Developments:

- In May 2025, Magrathea, a California-based startup, launched its next-generation magnesium chloride electrolyzer at its Oakland pilot facility as a strategic move to establish carbon-neutral magnesium production from seawater and strengthen domestic supply chain resilience.

- In March 2025, Great Wall Motor (GWM) and Baowu Magnesium signed a strategic cooperation framework agreement at the Haval Technology Center, unveiling a joint laboratory for magnesium product development, according to a post on GWM's WeChat account.

Companies Covered in Magnesium Alloy Market

- US Magnesium LLC

- Luxfer MEL Technologies

- Shandong Feixian County Yinguang Magnesium Industry Co. Ltd.

- Hydro Magnesium

- Magontec Limited

- m-tec powder

- Smiths Advanced Metals.

- Weijie Magnesium Industry Co.

- US Magnesium LLC

- Meridian Lightweight Technologies.

- AMACOR

- Globe Specialty Metals, Inc.

- Spartan Light Metal Products

- Posco

- Norsk Hydro ASA

Frequently Asked Questions

The global magnesium alloy market is estimated to be valued at US$ 3.9 Bn in 2025.

Surging EV demand and automotive applications drive magnesium alloy growth, while medical use and innovation open new revenue streams, driving the market.

In 2025, the Asia Pacific region will dominate the market with over 45% share in the market.

Among applications, the preference for the aerospace and defense segment is expected to grow rapidly at 14.8% CAGR from 2025-2032.

US Magnesium LLC, Luxfer MEL Technologies, Shandong Feixian County Yinguang Magnesium Industry Co. Ltd., Hydro Magnesium, Magontec Limited, and m-tec powder are some key industry players.