- Advanced Materials

- U.S. Magnesium Oxide Board Market

U.S. Magnesium Oxide Board Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Magnesium Oxide Board Market by Thickness (Thin (<8 mm), Medium (8 to 15 mm), and Thick (>15 mm)), Application (Residential, Commercial, and Industrial), and Regional Analysis for 2026 to 2033

U.S. Magnesium Oxide Board Market Size and Share Analysis

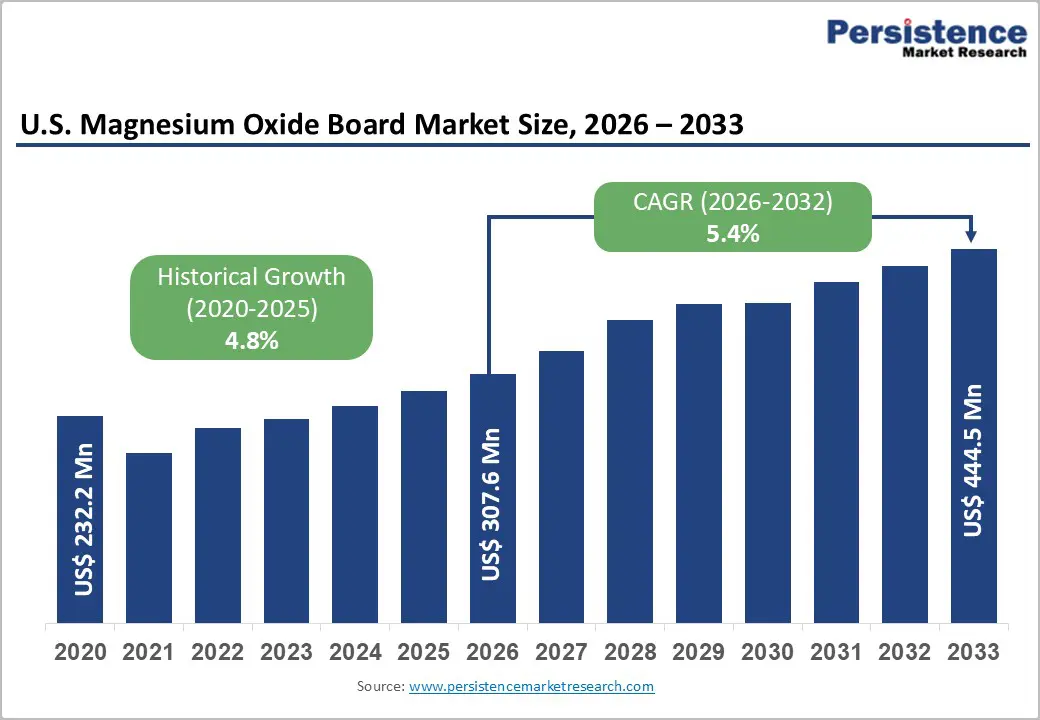

The U.S. magnesium oxide board market size is likely to be valued at US$ 307.6 million in 2026 and is projected to reach US$ 444.5 million by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Rising emphasis on non-combustible, moisture-resistant, and low-maintenance building materials is encouraging specifiers to shift from conventional gypsum and wood-based boards toward magnesium oxide (MgO) solutions in both structural and architectural applications. Stricter fire-safety requirements under U.S. model building codes, combined with a growing pipeline of multifamily, healthcare, and institutional projects, further reinforce demand for MgO boards that can achieve 1-hour to 2-hour fire ratings in wall and floor assemblies.

Key Industry Highlights:

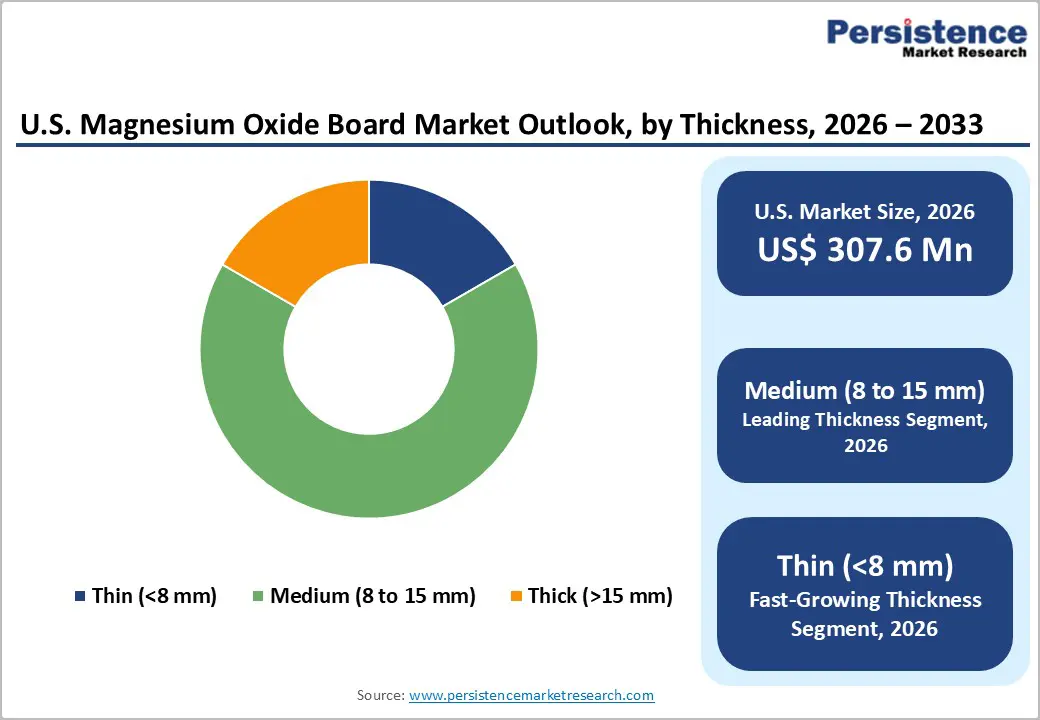

- Dominant Thickness: Medium-thickness MgO boards dominate demand due to widespread use in interior partitions, ceilings, and exterior sheathing. Their compatibility with tested fire-rated assemblies and standard framing systems makes them the preferred specification choice in commercial and multifamily construction.

- Fastest-Growing Thickness: Thin MgO boards are expanding rapidly in modular construction, renovation overlays, and lightweight ceiling systems. Growth is supported by rising prefabrication trends, weight reduction requirements, and increasing integration into composite insulated panel systems.

- Dominant Application: Commercial buildings, including healthcare, education, hospitality, retail, and offices, represent the largest consumption base. Stricter fire-resistance codes, durability expectations, and lifecycle cost considerations are driving higher specification rates in high-occupancy environments.

- Growth Indicator: Stricter enforcement of ASTM E119 fire-resistance ratings, non-combustibility standards such as ASTM E136, and façade fire-propagation requirements are increasing the specification of MgO boards in high-occupancy and high-rise projects. Insurance underwriting pressures further reinforce demand for non-combustible materials.

- Market Restraint: Higher upfront costs relative to gypsum drywall, combined with lingering perception concerns from earlier product generations, require additional documentation, testing, and engineering approvals, extending specification timelines and limiting uptake in cost-sensitive residential segments.

- Key Opportunity: Rising emphasis on embodied carbon reduction, green building certifications such as LEED, and expansion of mass-timber construction are positioning MgO boards as a high-performance, non-combustible complementary material in next-generation building envelope systems.

| Key Insights | Details |

|---|---|

| U.S. Magnesium Oxide Board Market Size (2026E) | US$ 307.6 Mn |

| Market Value Forecast (2033F) | US$ 444.5 Mn |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - tringent fire-safety codes and resilience-driven construction standards are accelerating MgO board adoption

Growing awareness of fire risk in residential, commercial, and industrial buildings is a primary driver for MgO board adoption in the U.S. High-quality magnesium oxide boards can withstand temperatures of around 800°C (1,472°F) for several hours and help assemblies meet 1-hour and 2-hour ratings under ASTM E119 and related fire tests, substantially outperforming many gypsum and cement boards. In parallel, NFPA-driven requirements for exterior wall assemblies, such as NFPA 285 for multi-story non-load-bearing façades containing combustible components, are pushing architects to specify non-combustible sheathing and panel systems where MgO has proven compatibility and compliance.

Insurance providers are increasingly tightening underwriting criteria for high-occupancy and high-rise buildings, encouraging the use of non-combustible materials that minimize fire propagation risk. Municipal building departments in wildfire-prone and dense urban regions are also reinforcing fire-resistance standards, indirectly supporting demand for MgO sheathing and interior linings. Rising investment in resilient infrastructure, particularly in schools, healthcare facilities, hospitality assets, and multifamily developments, further strengthens specification rates. As performance-based building codes gain traction, MgO boards are positioned as a dependable solution within tested and code-compliant wall assemblies.

Superior Moisture Resistance and Long-Term Durability Advantages are Strengthening Mgo’s Competitive Position

Superior resistance of MgO boards to moisture, mold, and biological attack compared with standard gypsum wallboard and many wood-based substrates remains a strong growth catalyst. Magnesium oxide panels maintain dimensional stability and mechanical strength in high-humidity environments, passing aggressive mold and mildew exposure tests that often degrade gypsum or paper-faced products. These properties make them especially attractive for bathrooms, basements, coastal buildings, and exterior sheathing applications.

Climate variability and increasing humidity exposure in certain U.S. regions are driving builders to adopt materials with higher tolerance to environmental stress. Reduced susceptibility to swelling, delamination, and structural weakening translates into fewer warranty claims and lower lifecycle repair costs. Builders focused on envelope integrity also appreciate MgO’s resistance to insect infestation and rot, which supports longer service life in demanding climates. Such durability credentials align with the growing preference for high-performance building materials that lower operational risk over decades.

Restraints - Higher Initial Material And System Costs Continue to Limit Broader Penetration in Price-Sensitive Segments

Higher upfront costs compared with commodity gypsum and selected fiber-cement boards remain a notable restraint. Contractors accustomed to optimizing bids around low-cost drywall systems often hesitate to shift toward board solutions that increase per-square-foot installation expenses, particularly in speculative residential projects where margins are tight. Although lifecycle savings from enhanced durability and fire resilience are recognized in institutional and commercial developments, those benefits are not always reflected in initial procurement decisions.

Limited contractor familiarity can also result in perceived installation complexity, further affecting adoption rates. Supply-chain concentration and dependence on select manufacturers may contribute to pricing volatility and freight-related costs. In projects governed by strict budget ceilings, value engineering exercises frequently prioritize minimum first cost over total cost of ownership. This pricing dynamic slows conversion from conventional drywall systems, especially in entry-level housing and cost-driven retrofit applications.

Performance variability in earlier product generations has created lingering perception and specification challenges

Performance variability in some earlier MgO board formulations, particularly high-chloride variants, led to issues such as efflorescence and fastener corrosion under certain climatic conditions, shaping cautious market perceptions. Although modern sulfate-based and low-chloride products have significantly improved chemical stability and now comply with rigorous standards such as ASTM E136 and ICC-ESR certifications, residual skepticism persists among certain architects and engineers.

Specifiers often request additional technical documentation, third-party test data, and mock-up evaluations before approving MgO in critical fire-rated or exterior assemblies. Extended approval processes can lengthen project timelines and increase transactional complexity. Conservative procurement policies in public-sector projects may further favor well-established materials with long historical track records. Overcoming these perception barriers requires sustained education, transparent performance data, and broader publication of successful case studies across U.S. climate zones.

Opportunities - Rising demand in high-rise, multifamily, and mass-timber construction is creating substantial specification opportunities

Expansion of high-density urban construction, including high-rise multifamily, mixed-use developments, and mass-timber buildings, presents a major opportunity for MgO boards. Fire-separation requirements in vertical construction demand non-combustible protection layers that can meet NFPA 285 criteria and support compliant exterior wall assemblies incorporating combustible insulation. MgO sheathing, shaftwall liners, and fire-rated partitions are increasingly evaluated as part of tested wall and floor systems.

Growth in mass-timber construction further enhances opportunity, as engineered wood systems require robust fire-protective cladding and lining materials. Urban redevelopment initiatives and transit-oriented housing projects are amplifying demand for durable, fire-resilient envelope components. As manufacturers expand their catalog of tested assemblies and code-evaluation listings, architects gain greater confidence specifying MgO in large-scale projects. This momentum is expected to translate into stronger penetration across multifamily, hospitality, and institutional segments.

Alignment with sustainability goals and green-building certifications is opening new strategic avenues

Growing emphasis on sustainability and embodied-carbon reduction within the U.S. construction sector is creating favorable conditions for MgO board positioning. Compared with certain cement-intensive alternatives, optimized MgO formulations can offer competitive embodied-carbon profiles and enable thinner, lighter assemblies that maintain high fire and moisture performance. Such characteristics support project teams pursuing LEED, Green Globes, and similar green-building certifications.

Resistance to mold and moisture also contributes to healthier indoor air quality, aligning with wellness-focused building standards and occupant health priorities. Increasing demand for Environmental Product Declarations (EPDs) and transparent material sourcing presents opportunities for manufacturers that invest in verified sustainability documentation. Durability-driven reduction in replacement frequency and material waste supports circular-economy objectives. These sustainability attributes enable MgO producers to differentiate their offerings in environmentally conscious commercial and institutional markets.

Category-wise Analysis

Thickness Insights

The medium (8 to 15 mm) thickness band is expected to remain the dominant segment in the U.S. MgO board market, accounting for an estimated 60% of demand in 2026, driven by its suitability for interior partitions, ceilings, and exterior sheathing in standard framing systems. Boards in the 10 mm to 16 mm range are commonly used in tested fire-rated wall and ceiling assemblies, delivering the mechanical strength and fire performance demanded in commercial and multifamily projects. Their balance of rigidity, ease of handling, and compatibility with common fasteners and finishing systems makes them the default choice for many architects and contractors seeking a “drop-in” upgrade from gypsum wallboard to a non-combustible, moisture-resistant solution.

The thin (<8 mm) boards are projected to be the fastest-growing segment, albeit from a smaller base, as they find increasing use in specialty applications such as laminated assemblies, ceilings with weight constraints, renovation overlays, and certain modular or prefabricated components. Their lighter weight and easier cutting make them attractive where structural loading, ergonomics, or geometry require slimmer panels, while still offering better moisture and fire performance than many fiber-reinforced or paper-faced alternatives. As system providers develop composite panels and interior solutions that integrate thin MgO layers with insulation or decorative faces, growth in this segment is expected to outpace that of thick boards used mainly in niche structural or high-impact environments.

Application Insights

The commercial application segment, including offices, retail, education, healthcare, hospitality, and institutional buildings, holds the leading share of U.S. MgO board consumption, estimated at roughly 55% in 2026. These buildings must meet more stringent fire-resistance, acoustic, and durability requirements than typical single-family residences, leading specifiers to favor non-combustible, mold-resistant boards in corridors, stairwells, shafts, wet areas, and high-traffic partitions. Hospitals, schools, and hotels face strong incentives to minimize downtime and remediation costs, reinforcing the case for durable MgO board systems over commodity drywall.

The industrial segment is emerging as the fastest-growing application area, driven by the need for robust, fire-resistant wall and ceiling systems in factories, warehouses, logistics hubs, data centers, and energy facilities. These environments often present elevated fire loads, mechanical impacts, and moisture or chemical exposure, making MgO’s non-combustible and durable nature especially valuable compared with traditional sheathing materials. Growth in e-commerce and cold-chain logistics infrastructure across the U.S. is spurring investment in large-footprint buildings where fire safety, insurance requirements, and long-term maintenance costs are key decision factors, positioning MgO boards as an attractive upgrade in new industrial and mission-critical facilities.

Competitive Landscape

The U.S. magnesium oxide board market is moderately fragmented, with a combination of domestic specialists and international suppliers offering a range of panel thicknesses and performance grades. Companies compete on fire-rating credentials, moisture resistance, environmental certifications, and system-level solutions that integrate boards with framing, fasteners, and finishing systems.

Leading players emphasize investments in testing to achieve compliance with ASTM, NFPA, and ICC-ESR requirements, along with product differentiation through proprietary formulations, sulfate-based chemistries, and enhanced structural strength. Emerging business models include collaboration with prefab and modular builders, distribution partnerships with specialty building-material dealers, and technical support services for architects and engineers designing MgO-based assemblies.

Key Developments:

- In November 2024, MagMatrix introduced a new sulfate MgO board certified to ASTM E136 and compliant with NFPA 285 wall-assembly requirements, expanding options for fire-rated façades in multifamily and commercial buildings.

- In June 2024, Foreverboard California, Inc. continued to promote U.S.-manufactured MgO drywall with enhanced resistance to mold, mildew, water, fire, and insects, targeting the substitution of conventional gypsum wallboard and cement backer boards in demanding applications.

Companies Covered in U.S. Magnesium Oxide Board Market

- Magnum Board Products, LLC

- Ambient Bamboo Products Inc.

- North American MgO LLC

- Foreverboard California, Inc.

- Ambient Building Products Inc.

- Huber Engineered Woods LLC

- DragonBoard USA

- James Hardie Building Products Inc.

- US MgO Company

- Sulfycor

Frequently Asked Questions

The U.S. magnesium oxide board market is valued at about US$ 307.6 million in 2026 and is projected to reach around US$ 444.5 million by 2033, reflecting a CAGR of roughly 5.4%.

Key demand drivers include stringent fire-safety regulations, the need for 1-hour to 2-hour fire-rated assemblies under ASTM and NFPA standards, and growing preference for moisture-, mold-, and insect-resistant boards in resilient, low-maintenance buildings.

Medium (8 to 15 mm) thickness boards and the commercial application segment lead U.S. demand, supported by widespread use in walls, ceilings, and sheathing for offices, hospitals, schools, hotels, and other high-occupancy facilities.

Major opportunity lies in supplying MgO boards for high-rise, multifamily, and mass-timber projects and for green-building certified developments, where superior fire performance, durability, and potential embodied-carbon benefits are increasingly sought by developers and regulators.

Key players include Magnum Board Products, LLC, Ambient Bamboo Products Inc., North American MgO LLC, Foreverboard California, Inc., Ambient Building Products Inc., Huber Engineered Woods LLC, DragonBoard USA, James Hardie Building Products Inc., along with specialists such as MagPanel and MagMatrix.