- Transportation & Logistics

- Loader Crane Market

Loader Crane Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Loader Crane Market by Crane Type (Knuckle Boom and Straight Boom), By Capacity (<10 MT, 10-30 MT and 30+ MT), End-user (Construction, Logistics, Marine and Utilities), and Regional Analysis for 2026 - 2033

Loader Crane Market Size and Trends Analysis

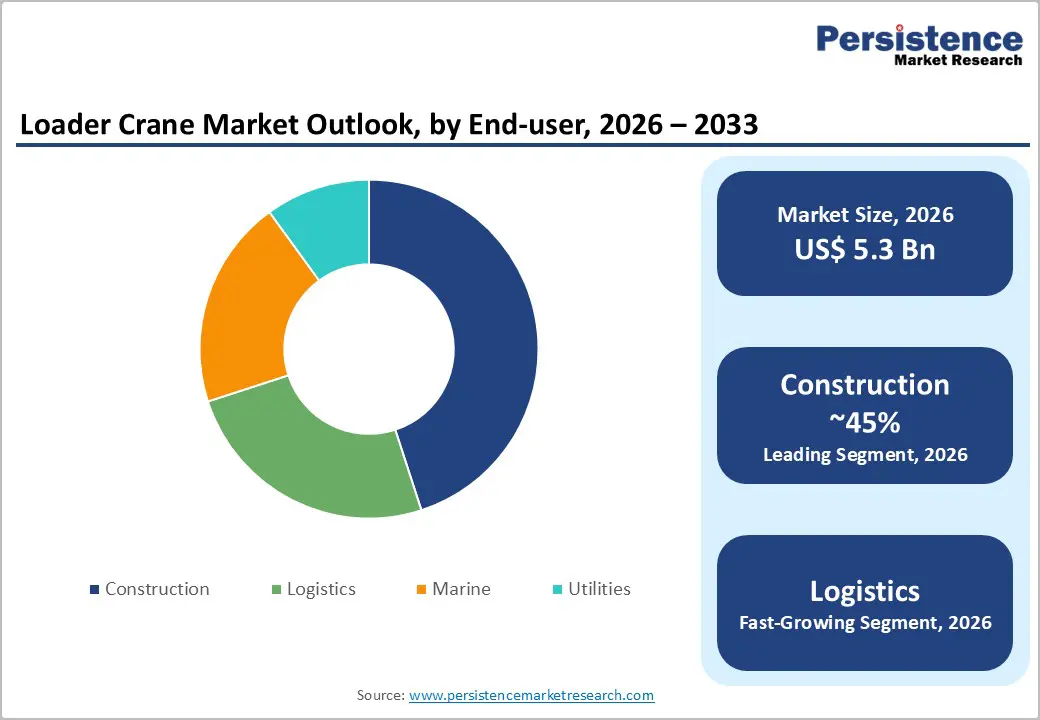

The global loader crane market size is likely to be valued at US$ 5.3 billion in 2026 and is projected to reach US$ 7.2 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033. The market is driven by the expansion of e-commerce and last-mile delivery operations, creating proportionate loader crane demand; the adoption of advanced technologies, including IoT monitoring and automation, enhancing operational efficiency; and a shift toward lightweight truck-mounted lifting equipment to address urban space constraints.

Key Industry?Highlights:

- Leading Crane Type: Knuckle boom cranes dominate with 55% market share through urban maneuverability advantages; Straight boom represents the fastest growing at 6-10% CAGR, driven by industrial specialization and cost-effectiveness.

- Dominant Capacity: <10 MT capacity commands 48.4% market share through broad applicability and cost-effectiveness; 10-30 MT capacity is the fastest-growing segment at a 6% CAGR, driven by expansion in heavy-duty applications.

- Leading End-use Application: Construction maintains 45% market share through material handling requirement scale; Logistics represents the fastest-growing at 5.8% CAGR, driven by e-commerce fulfilment and last-mile delivery expansion.

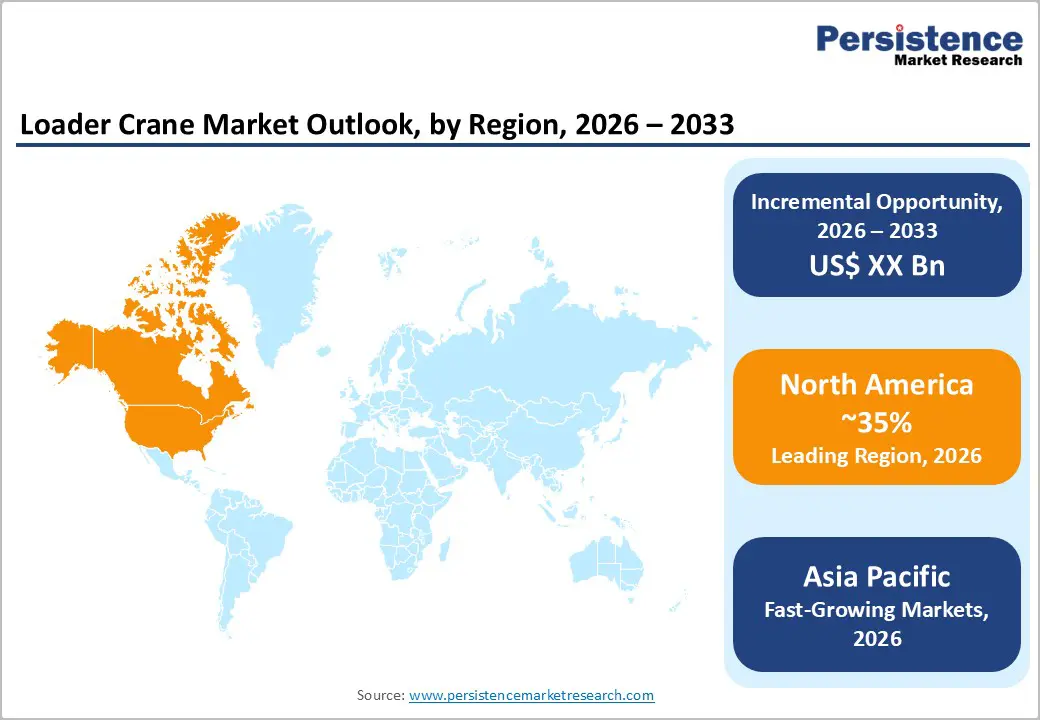

- Regional Market Dominance and Growth: North America maintains 35% global market share, driven by infrastructure investment; Asia Pacific demonstrates the fastest regional growth at 7% CAGR, expanding from 30% current share to 40% by 2033 through urbanization.

- Technology and Market Innovation: Top 10 suppliers control 55% market share (Palfinger, HMF, Fassi leading); Electrification technology is advancing, with 50-70% emission reduction through eHydraulic systems; IoT integration is enabling predictive maintenance, reducing downtime by 25-35%; Autonomous capabilities development is establishing future market positioning.

| Key Insights | Details |

|---|---|

|

Loader Crane Market Size (2026E) |

US$ 5.3 Bn |

|

Market Value Forecast (2033F) |

US$ 7.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.6% |

|

Historical Market Growth (CAGR 2020 to 2024) |

3.8% |

Market Dynamics

Drivers - E-Commerce Expansion and Last-Mile Delivery Infrastructure Development

Global e-commerce market reached approximately US$ 5.8-6.2 trillion in 2024-2025, representing 15-20% year-over-year growth and establishing proportionate logistics infrastructure requirements. Last-mile delivery market expansion, with global last-mile delivery valued at US$ 161+ billion in 2024 and growing at 18-22% annually, creates systematic demand for efficient material-handling equipment. Urban delivery concentration, with 23.5% of retail commerce conducted online by 2025 and growing 20-25% annually, drives microfulfilment center development requiring compact loader cranes for loading/unloading operations.

Same-day and next-day delivery mandates, with 60-70% of e-commerce consumers expecting expedited delivery options, necessitate rapid material transfer capabilities at distribution facilities. Fleet optimization pressure, with logistics companies requiring compact, high-capacity equipment to maximize warehouse utilization and reduce operational bottlenecks, drives loader crane procurement.

Infrastructure Development and Urban Construction Expansion

The global construction market, valued at approximately US$ 15-17 trillion in 2024-2025 and growing at 5% annually, establishes foundational demand for loader cranes for material handling across project sites. The urbanization trajectory, with the global urban population projected to reach 68% by 2033 and the corresponding construction requirements, drives demand for compact, urban-adaptable equipment. Infrastructure investment expansion, with government spending on infrastructure globally reaching US$ 4-5 trillion annually through the 2033 forecast period, establishes systematic construction equipment demand.

Urban redevelopment projects, with major cities including London, Paris, Dubai, and Shanghai investing US$ 200-500 million annually in infrastructure modernization, drive advanced material handling equipment procurement. Modular construction advancement, with prefabricated building systems growing 15-20% annually and requiring specialized handling equipment for component placement, establish technical differentiation opportunity.

Restraints - High Capital Investment Requirements and Equipment Cost Barriers

Loader crane acquisition costs, with advanced knuckle boom cranes commanding purchase prices of US$ 150,000-500,000+, depending on capacity and technology sophistication, constrain SME adoption. Financing complexity, with equipment financing requiring 12–24-month approval timelines and stringent credit requirements, impairs purchasing flexibility for smaller operators. Maintenance cost escalation, with advanced technology integration increasing preventive maintenance costs to 8-12% of equipment acquisition cost annually, increase total cost of ownership. Skilled technician availability, with specialized maintenance requiring trained technicians commanding premium compensation, and limited cost-effective support availability, particularly in emerging markets.

Retrofit complexity, with integrating new equipment into existing fleet operations requiring system modifications and operational downtime, create implementation barriers. Used equipment market saturation, with secondary market oversupply in developed regions, constrains new equipment sales and compresses pricing margins.

Regulatory Complexity and Environmental Emission Standards

Emission regulation stringency, with EU Stage V, EURO VI, and equivalent standards requiring 90% emission reductions, increases equipment costs 15%, compressing manufacturer margins. Electrification mandate acceleration, with cities including London, Paris, and Singapore implementing zero-emission zones and restricting traditional-fuel vehicles, reduces the addressable market for conventional equipment. Safety certification requirements, with increasingly stringent ISO and regional standards, require comprehensive testing and validation, increasing product development costs and timelines.

Cross-border compliance complexity, with equipment requiring certification modifications across different regulatory jurisdictions creating operational burden. Retrofit cost requirements, with regulations often mandating retrofitting existing equipment to meet new standards at high cost, create an operator burden.

Opportunity - Electric and Hybrid-Electric Loader Crane Development

Electrification mandate compliance, with EU, China, and North American jurisdictions establishing mandates for electric and zero-emission equipment deployment, creates a systematic market opportunity. Total cost of ownership advantages, with electric loader cranes achieving 40-50% operating cost reductions through lower energy consumption and reduced maintenance, provide economic justification despite 20-30% higher capital costs. Urban deployment preference, with electric equipment enabling deployment in restricted zones and earning premium pricing, supports market penetration.

Incentive programs, with government subsidies and tax incentives supporting electric vehicle adoption, reaching US$ 10-20 billion globally annually, reduce customer acquisition barriers. Environmental brand positioning, with companies increasingly prioritizing sustainable equipment procurement to meet ESG commitments, drives demand for electric alternatives.

Autonomous and Partially Autonomous Material Handling Solutions

Autonomous lifting system development, with autonomous loader cranes reducing operator requirements and improving safety, establishes market differentiation. Labor shortage mitigation, with skilled operator availability declining globally and autonomous systems offering a solution for operational continuity, drives adoption incentives. Safety improvement achievement, with autonomous systems reducing human error and workplace injuries by 70-80%, justify investment for safety-conscious operators.

Industry 4.0 alignment, with autonomous equipment integrating seamlessly with smart warehouse and manufacturing systems, supports digital transformation initiatives. Cost reduction potential, with autonomous systems operating 24/7 without operator fatigue and reducing labor costs by 30-40%, establishes ROI justification.

Category-wise Analysis

Crane Type Insights

The knuckle boom crane segment holds 55% market share, driven by superior maneuverability and efficiency in space-constrained environments. Its articulated boom design allows compact stowage and flexible operation, making it ideal for urban construction, narrow streets, and congested job sites. The ability to position loads precisely around obstacles enhances application versatility, while reduced boom extension improves safety in confined spaces. Faster setup times and shorter operating cycles, compared with straight-boom cranes, further strengthen productivity and justify premium pricing.

The straight boom crane segment is the fastest-growing, projected to expand at a 5% CAGR through 2033. Growth is driven by demand for higher load capacity and greater vertical reach in industrial, warehouse, and logistics applications. A 15–20% cost advantage over knuckle boom cranes supports adoption in price-sensitive markets, while advancements in hydraulics and controls improve performance.

Capacity Insights

The <10 MT capacity segment holds 48.4% market share, driven by broad applicability and compatibility with standard commercial vehicle platforms. Vehicle chassis weight limits typically restrict payload capacity to around 10 MT, establishing a natural manufacturing baseline. Sub-10 MT cranes offer strong urban mobility, enabling access to weight-restricted city areas. They support diverse applications across construction, utilities, municipal services, and logistics while meeting 60–70% of typical lifting requirements. A 35% cost advantage over higher-capacity models and widespread manufacturing accessibility through standardized components reinforce adoption and market leadership.

The 10–30 MT segment is the fastest-growing, projected to expand at a 6% CAGR through 2033. Growth is driven by rising demand from heavy-duty construction, industrial operations, infrastructure projects, and specialized logistics. Advances in hydraulics and vehicle chassis design enable safe mid-capacity deployment, while a favorable capacity-to-cost ratio compared to larger cranes supports investment for specialized lifting needs.

End-user Insights

The construction sector holds a 45% market share, driven by intensive material-handling needs across all project phases. The global construction market, valued at US$ 15–17 trillion and growing 5–7% annually, creates a strong demand base for loader cranes. Construction activities require frequent loading, unloading, and precise placement of materials, particularly in urban environments, where cities invest US$200–500 million annually in infrastructure and modernization projects. Increasing safety regulations mandating certified equipment and advanced safety features, along with pressure to meet tight project timelines, further accelerate the adoption of efficient lifting solutions.

The logistics segment is the fastest-growing, projected to expand at a 6.1% CAGR through 2033. Growth is driven by rapid e-commerce expansion, scaling of last-mile delivery networks, integration of warehouse automation, and proliferation of distribution centers. Logistics operators increasingly demand compact, high-capacity cranes to improve fleet efficiency, optimize space utilization, and support same-day delivery requirements.

Regional Insights

North America Crane Loader Market Insights

North America commands approximately 35% of global Loader crane market share, valued at approximately US$ 1.9 billion in 2026 with projections approaching US$ 2.5 billion by 2033. The United States represents a dominant regional market contributor, accounting for 80% of the North American market value, driven by construction activity and logistics infrastructure expansion.

Infrastructure investment prioritization, with the US federal government allocating US$ 150-200 billion annually for infrastructure modernization through the 2033 forecast period, establishes systematic equipment demand. Construction sector expansion, with residential and commercial construction growing 6-9% annually driven by urbanization and housing demand, and drive material handling equipment procurement. E-commerce logistics acceleration, with North American e-commerce growing 12-15% annually and requiring proportionate logistics infrastructure investment, establish proportionate equipment demand.

Europe Crane Loader Market Analysis

Europe represents approximately 22% of the global Loader crane market share, valued at approximately US$ 1.2 billion in 2026. Germany, Italy, France, and Spain collectively represent 70% of the European market value, reflecting established construction manufacturing presence and logistics infrastructure.

Environmental regulatory leadership, with EU emission standards and circular economy directives driving equipment modernization and adoption of electrification, establishes a market transformation opportunity. Construction activity concentration, with the European construction market valued at US$ 2.0-2.3 trillion and growing 4-6% annually, establishes proportionate equipment demand. Logistics modernization emphasis, with European logistics companies investing heavily in warehouse automation and advanced equipment, drives technical specialization. Urban density challenges, with dense European urban environments requiring compact, maneuverable equipment, favor the knuckle boom market.

Asia Pacific Crane Loader Market Insights

Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share and projected to increase to 40% by 2033. The region valued at approximately US$ 1.70 billion in 2026 is anticipated to reach US$ 2.9 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 12% in the upcoming years.

Infrastructure investment expansion, with China, India, and Southeast Asia investing US$ 300-500 billion annually in infrastructure through the forecast period, establishes substantial equipment demand. Construction sector acceleration, driven by urbanization and building development, creates 20-30% annual growth in construction activity across emerging markets, driving material handling equipment procurement. E-commerce logistics boom, with e-commerce sales growing 25% annually in emerging Asian markets and driving proportionate investment in logistics infrastructure, establishing a primary growth catalyst.

Loader Crane Market Competitive Landscape

The global Loader Crane market demonstrates moderate consolidation with established equipment manufacturers and specialized crane designers maintaining competitive positions. The top 10 suppliers, including Palfinger, HMF, Fassi, Copma, Tadano, PM Cranes, Atlas, AMCO, Hetronic, and Advanced Lifting, collectively control approximately 55% of global market share, reflecting technology leadership and established manufacturing infrastructure.

Market structure reflects bifurcation between large multinational conglomerates offering comprehensive material handling solutions and specialized crane manufacturers focusing exclusively on loader crane development.

Key Industry Developments

- In July 2025, SANY (China) expanded its manufacturing footprint by opening a new facility in Southeast Asia, aimed at catering to the growing demand in that region. This expansion not only enhances SANY's production capacity but also underscores its commitment to local markets, enabling quicker responses and tailored solutions that meet regional needs.

- In June 2024, Swedish company Hiab launched the Hiab iQ.708 HiPro knuckle boom loader crane, continuing its legacy in loader crane manufacturing dating back to 1944. The iQ.708 HiPro features the advanced V12-Power boom, engineered to deliver an outstanding power-to-weight ratio, enhancing lifting efficiency while reducing structural mass.

Companies Covered in Loader Crane Market

- PALFINGER AG

- Cargotec (Hiab)

- Fassi Gru S.p.A.

- ATLAS Group

- Tadano Ltd.

- Cormach S.r.l.

- PM Group S.p.A.

- XCMG

- Next Hydraulics s.r.l.

- Hyva Group

- Prangl GmbH

- Others Key Players

Frequently Asked Questions

The Loader Crane market is estimated to be valued at US$ 5.3 Bn in 2026.

The key demand driver for the Loader Crane market is the rising demand for efficient material handling and lifting solutions across construction, logistics, utilities, and infrastructure maintenance, driven by urbanization and infrastructure expansion.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Loader Crane market.

Among the end-user, construction accounts for the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other end-user type.

The key players in Loader Crane are PALFINGER AG, Cargotec (Hiab), Fassi Gru S.p.A. and ATLAS Group.