- Transportation & Logistics

- Side Loader Refuse Trucks Market

Side Loader Refuse Trucks Market Size, Share, and Growth Forecast, 2025 - 2032

Side loader refuse trucks Market by Vehicle Type (Standard Side Loader, Automated Side Loader, Rear-Loading Side Loader, Compactor Side Loader), Operational Mechanism (Hydraulic System, Pneumatic System, Manual Operation, Electric Operation), Vehicle Size and Load Capacity (Small Capacity (up to 6 tons), Medium Capacity (6 to 12 tons), Large Capacity (over 12 tons)), End-use, and Regional Analysis for 2025 – 2032

Side Loader Refuse Trucks Market Size and Trends Analysis

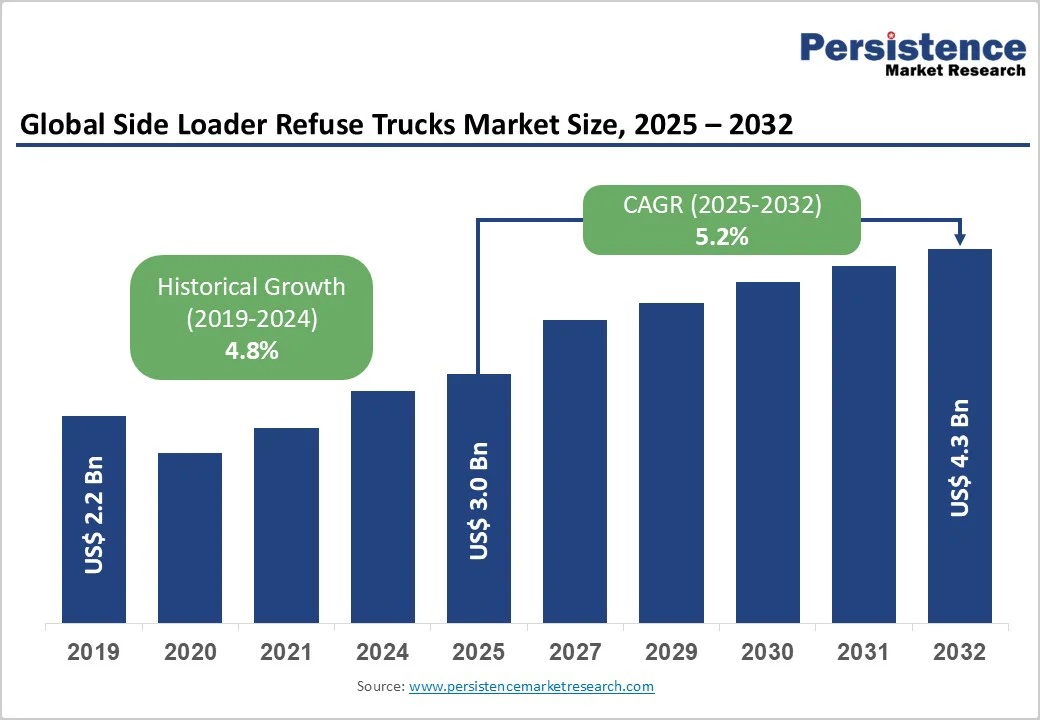

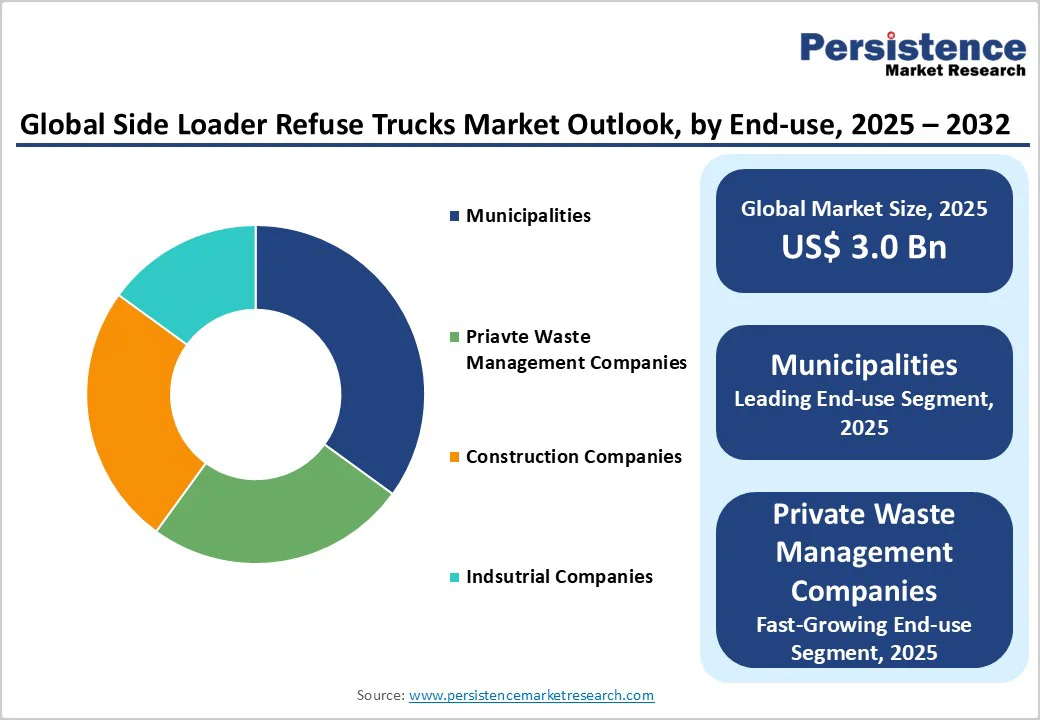

The global side loader refuse trucks market size is likely to be valued US$ 3.0 billion in 2025, estimated to reach US$ 4.3 billion by 2032 with growing at a CAGR of 5.2% during the forecast period from 2025 to 2032.

The market is experiencing robust growth driven by increasing urbanization, rising municipal waste generation, and advancements in automated waste collection technologies. The market is further propelled by innovative electric and hybrid models, catering to preferences for sustainable and cost-effective waste management. The growing acceptance of automated side loader trucks as alternatives to manual collection, especially in high-density urban environments, is a key growth factor.

Key Industry Highlights:

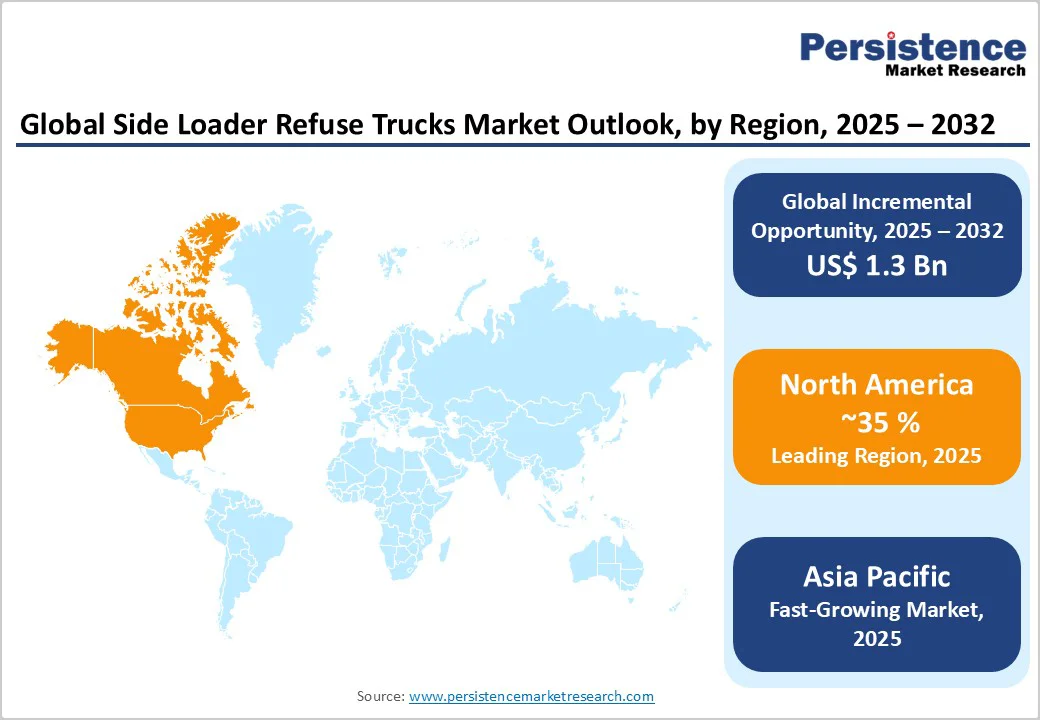

- Leading Region: North America, commanding a 35% market share in 2025, driven by advanced waste infrastructure and regulatory mandates in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing market due to rapid urbanization, government sanitation initiatives such as India’s Swachh Bharat Mission, and rising adoption of automated and electric side loader trucks.

- Dominant Vehicle Type: Automated Side Loader, holding approximately 40% of the market share, due to enhanced worker safety and efficiency.

- Leading Operational Mechanism: Hydraulic System, accounting for over 50% of market revenue, driven by reliability in heavy-duty operations.

- Leading Vehicle Size: Medium Capacity (6 to 12 tons), contributing nearly 45% of market revenue, owing to balanced load handling in urban settings.

- Key Market Driver: Rapid urban population growth and increasing environmental awareness are driving demand for efficient, automated, and electric side loader refuse trucks.

- Growth Opportunity: Advancements in electric operation for zero-emission fleets, enabling compliance with environmental regulations.

| Key Insights | Details |

|---|---|

| Side Loader Refuse Trucks Market Size (2025E) | US$ 3.0 Bn |

| Market Value Forecast (2032F) | US$ 4.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Dynamics

Driver - Rising urbanization and demand for efficient waste management

The increasing urbanization and need for efficient waste collection solutions are primary drivers of the automated side loader trucks market. Rapid population growth in urban areas has led to increased waste generation from households, commercial establishments, and industrial activities, creating a pressing need for streamlined collection and disposal solutions. Municipalities are under constant pressure to maintain cleanliness, reduce health hazards, and comply with environmental regulations, prompting investments in modern waste management fleets.

Side loader refuse trucks, especially automated and electric models, offer significant advantages in handling high-volume residential and commercial waste efficiently. Their ability to navigate narrow streets, perform rapid pick-ups, and integrate with smart waste management systems makes them highly suitable for densely populated cities. Additionally, governments worldwide are implementing policies and initiatives to promote sustainable urban sanitation, including subsidies for electric vehicles and automation technology. Private waste management companies are also expanding operations to meet commercial and industrial demand, deploying specialized trucks for bulk waste handling.

Restraint - High initial and maintenance costs

The high initial purchase prices and ongoing maintenance requirements of automated side loader trucks pose significant restraints on market growth. Electric side loaders often require substantial upfront investments due to advanced battery systems, electric drivetrains, and specialized components, making their purchase price considerably higher than conventional diesel trucks. This financial barrier can limit adoption, especially for smaller municipalities and private operators with constrained budgets.

Maintenance costs for advanced vehicles can be elevated, as electric and hybrid systems require specialized technicians, diagnostic tools, and replacement parts, which may not be readily available in all regions. Even routine servicing, such as battery checks or motor calibrations, can incur higher expenses compared with traditional diesel models. For automated side loaders, the integration of robotic arms, sensors, and telematics systems adds further complexity and cost to maintenance schedules. Depreciation of high-value components like lithium-ion batteries and electronic control units also affects long-term operational economics.

Opportunity - Expansion in electric and hybrid technologies

Advancements in electric and hybrid automated side loader trucks present significant growth opportunities for the market. Industry growth is driven by global sustainability initiatives and stricter emission regulations. Municipalities and private waste management companies are increasingly prioritizing low-emission fleets to reduce carbon footprints, comply with environmental standards, and improve urban air quality. Electric and hybrid side loader trucks offer substantial benefits, including lower operational costs, reduced fuel consumption, quieter operation, and minimal greenhouse gas emissions, making them ideal for densely populated urban areas.

Manufacturers are investing heavily in advanced battery technologies, regenerative braking systems, and lightweight materials to enhance vehicle efficiency and range, addressing traditional limitations of electric trucks. Hybrid models, combining electric motors with conventional diesel engines, provide flexibility for longer routes while maintaining environmental performance. Additionally, integration with automation and telematics systems allows for optimized routing, energy management, and predictive maintenance, further improving efficiency and cost-effectiveness.

Category-wise Analysis

Vehicle Type Insights

Automated Side Loader dominates the market, accounting for 40% of the share in 2025. Their popularity stems from enhanced worker safety, reduced labor requirements, and efficiency on high-volume residential routes. Equipped with robotic arms and smart controls, they streamline waste collection, lower operational costs, and meet growing municipal demands for automation and sustainable urban waste management.

Electric Operation is the fastest-growing mechanism, driven by global zero-emission mandates and sustainability goals. Integration with automation enhances operational efficiency, reduces noise, and cuts carbon emissions. Rapid adoption in urban areas is supported by government incentives, smart city initiatives, and advancements in battery and charging technologies.

Vehicle Size and Load Capacity Insights

Medium Capacity (6 to 12 tons) leads with nearly 45% share, offering an optimal balance between manoeuvrability and load capacity. Their versatility makes them ideal for urban and suburban waste collection, enabling efficient navigation through narrow city streets while maintaining strong performance and fuel efficiency for daily municipal operations.

Large Capacity (over 12 tons) is the fastest-growing, driven by increasing industrial waste volumes and the need for high-density compaction. These trucks offer greater efficiency for bulk waste handling, reducing collection frequency and operational costs, making them ideal for industrial zones, large municipalities, and high-population urban centers focused on sustainability.

End-use Insights

Municipalities hold over 50% share, as they remain primary users for large-scale public waste collection and sanitation services. Local governments increasingly deploy automated and electric side loader fleets to enhance collection efficiency, reduce operational costs, and meet environmental regulations while supporting urban sustainability and circular economy initiatives.

Private Waste Management Companies are the fastest-growing, driven by their focus on customized fleet solutions for commercial and municipal contracts. These companies increasingly invest in automated and electric trucks to enhance service efficiency, meet sustainability goals, and offer tailored waste collection solutions across industrial, retail, and residential sectors.

Regional Insights

North America Side Loader Refuse Trucks Market Trends

North America accounts for 35% in 2025, driven by stringent U.S. Environmental Protection Agency (EPA) emission regulations and widespread smart city initiatives. These factors are accelerating the adoption of automated and electric refuse collection vehicles to improve operational efficiency and reduce environmental impact. Municipalities across the U.S. and Canada are increasingly investing in advanced side loader trucks equipped with robotic arms, telematics, and energy-efficient propulsion systems to streamline waste collection and cut maintenance costs.

The transition toward zero-emission fleets is further supported by government incentives and funding for electric vehicle infrastructure. Interestingly, the U.K. market, though part of Europe, shows similar momentum under DEFRA’s waste management strategies, promoting cleaner technologies and hybrid truck adoption among urban councils. These efforts align with the country’s carbon reduction targets and circular economy goals.

Europe Side Loader Refuse Trucks Market Trends

Europe holds about 25% market share, led by Germany and France. The market’s growth is primarily driven by the European Union’s circular economy directives, which emphasize waste reduction, recycling, and the transition toward low-emission urban transport. These policies have encouraged municipalities and waste management companies to replace traditional diesel-powered trucks with electric and hybrid side loaders, supporting sustainability goals.

Germany’s strong environmental regulations and commitment to carbon neutrality by 2045 are accelerating the deployment of green fleets across major cities. France is investing heavily in modern waste collection infrastructure, supported by public-private partnerships and EU funding programs. The widespread use of automation, telematics, and IoT-enabled fleet management systems enhances route efficiency and reduces operational costs. Additionally, growing public awareness of recycling and resource recovery strengthens market demand for advanced refuse trucks.

Asia Pacific Side Loader Refuse Trucks Market Trends

Asia Pacific commands around 25% share and is the fastest-growing region, driven by rapid urbanization, expanding municipal infrastructure, and government-led sanitation initiatives. China’s accelerating urban population and stringent waste management regulations are prompting cities to adopt automated waste collection systems, enhancing operational efficiency and environmental compliance. India’s Swachh Bharat Mission, focused on promoting cleanliness and sustainable waste disposal, has spurred significant investments in modern refuse collection vehicles.

Local governments and private contractors are increasingly shifting toward automated and electric side loader trucks to address rising waste volumes while reducing labor dependency and carbon emissions. Moreover, countries such as Japan and South Korea are integrating smart technologies and IoT-based waste monitoring solutions to optimize collection routes and improve recycling efficiency. Growing industrialization and foreign investments in waste management infrastructure are further supporting market expansion.

Competitive Landscape

The global side loader refuse trucks market is highly competitive, characterized by the presence of several established manufacturers focusing on technological innovation and strategic partnerships. Companies such as Heil, McNeilus, and Bucher Municipal are emphasizing automation and electrification to align with global sustainability goals and reduce carbon emissions. The integration of advanced telematics, automated arms, and sensor-based waste collection systems enhances operational efficiency and minimizes human intervention, addressing urban waste management challenges.

Government initiatives promoting electric vehicle adoption and stricter emission regulations are accelerating the shift toward eco-friendly automated side loader trucks. Manufacturers are also investing in battery technology, lightweight materials, and AI-based route optimization to improve fuel economy and performance.

Key Developments

- In May 2025, McNeilus Truck and Manufacturing, Inc., an Oshkosh Corporation (NYSE: OSK) business, today announced the expansion of its industry-leading side loader refuse and recycling collection vehicle production line. The expansion is supported by a significant modernization of the company’s manufacturing operations at its Dodge Center, Minnesota headquarters, marking a major step forward in product innovation, operational efficiency, and customer-focused growth.

- In May 2023, Heil Environmental has recently expanded its production of hydraulic compactors for medium-capacity refuse trucks, notably the PT1100 model. Designed for urban and suburban waste collection, the PT1100 offers a 13–20 cubic yard capacity and features a high-tensile steel construction for durability.

Regional analysis includes:

- North America (U.S., Canada)

- Latin America (Mexico, Brazil)

- Western Europe (Germany, Italy, France, U.K, Spain)

- Eastern Europe (Poland, Russia)

- Asia Pacific (China, India, ASEAN, Australia & New Zealand)

- Japan

- Middle East and Africa (GCC Countries, S. Africa, Northern Africa)

The report is a compilation of first-hand information, qualitative and quantitative assessment by industry analysts, inputs from industry experts and industry participants across the value chain.

The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

Companies Covered in Side Loader Refuse Trucks Market

- Heil

- New Way

- Amrep

- Rush Truck Centers

- McNeilus

- Curbtender

- STG

- Bucher Municipal

- NTM

- CLW Group

Frequently Asked Questions

The global side loader refuse trucks market is projected to reach US$3.0 Bn in 2025, driven by urbanization and efficient waste collection needs.

Policies promoting waste management modernization, smart city projects, and rising industrial and commercial waste volumes are encouraging the adoption of advanced side loader fleets.

The market is poised to witness a CAGR of 5.2% from 2025 to 2032, supported by electric innovations and sustainability mandates.

Expansion in electric fleets and smart city projects offers key opportunities for automated side loader refuse trucks in emerging markets.

Key players include Heil, McNeilus, New Way, Rush Truck Centers, and Bucher Municipal, leading through automated and electric truck innovations.