- Pharmaceuticals

- Asthma Treatment Market

Asthma Treatment Market Size, Share and Growth Forecast, 2026 - 2033

Asthma Treatment Market by Drug Class (ICS, Bronchodilators, Biologics, Leukotriene Modifiers, Combination Therapies), Route of Administration (Inhaled, Oral, Injectable), Patient Demographics (Pediatric, Adolescents, Adults, Geriatric), and Regional Analysis for 2026 - 2033

Asthma Treatment Market Share and Trends Analysis

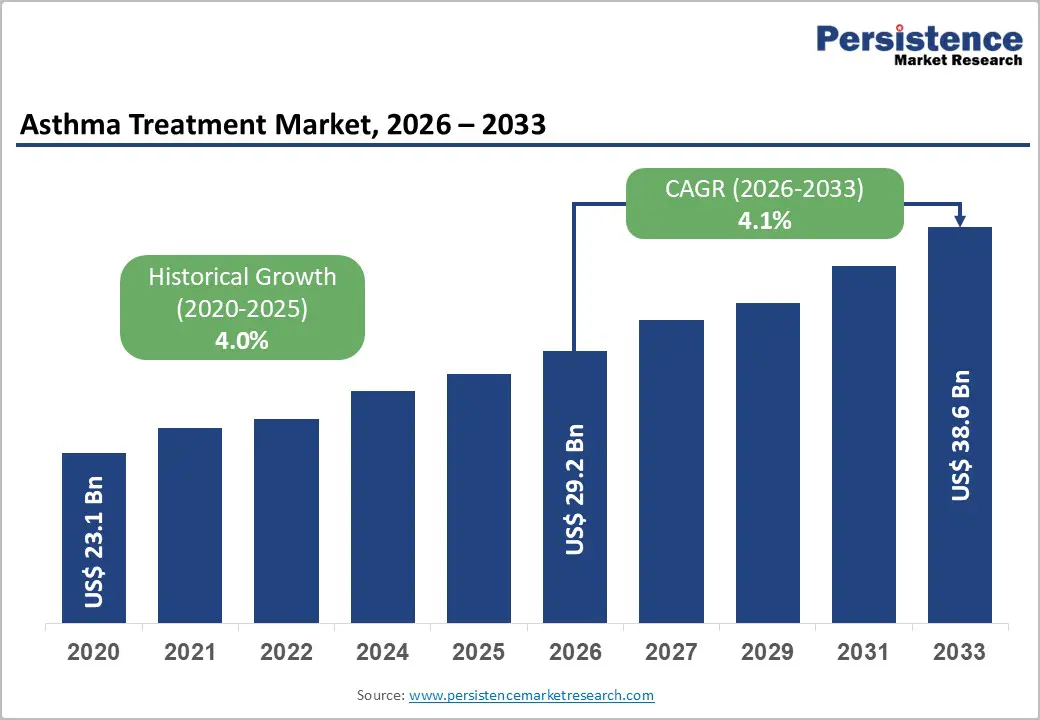

The global asthma treatment market size is likely to be valued at US $29.2 billion in 2026 and is projected to reach US $38.6 billion by 2033, growing at a CAGR of 4.1% during the forecast period 2026-2033.

The market is expanding due to shifting consumer preferences toward personalized and convenient therapies, coupled with industry trends emphasizing digital health integration and smart inhaler technologies. Clinicians increasingly favor biologics and combination therapies for moderate-to-severe asthma, driven by demonstrated efficacy in reducing exacerbations and improving lung function. Rising adoption of these advanced treatments across both developed and emerging markets strengthens overall market demand, while regulatory support for innovative drug delivery systems accelerates product uptake. Additionally, urbanization, higher disposable incomes, and expanding healthcare access in the Asia Pacific and Latin America drive patient awareness and treatment penetration. Growth in adult and geriatric populations further increases reliance on long-term asthma management solutions, creating premium opportunities for inhaled and injectable therapies, particularly in regions experiencing industrialization-related air pollution.

Key Industry Highlights

- Dominant Drug Class: ICS (Inhaled Corticosteroids) therapies are set to command around 43% of the revenue share in 2026, while biologics are likely to grow the fastest at 4.9% CAGR through 2033, driven by precision-targeted therapies and increasing adoption in severe asthma cases.

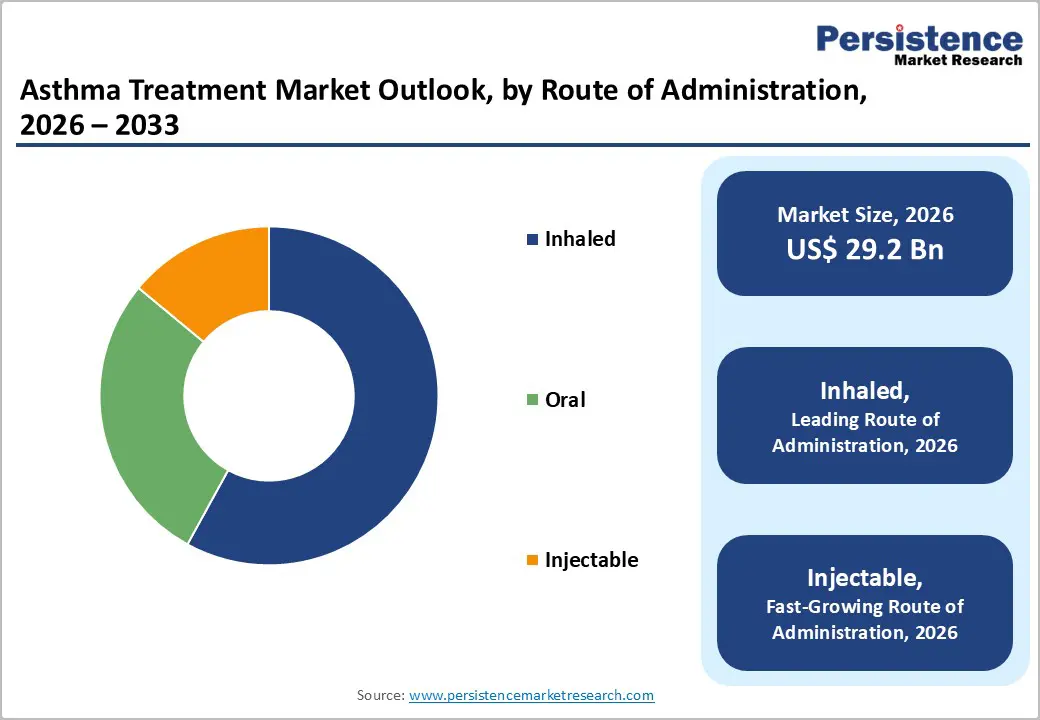

- Dominant Route of Administration: Inhaled therapies are anticipated to lead with an estimated 58% share in 2026, while injectables are slated to represent the fastest-growing segment at 5.1% CAGR from 2026 to 2033, reflecting the rise of biologic therapies.

- Patient Demographics: Adults are projected to hold the largest share at 49% in 2026, while the geriatric segment is expected to expand fastest at 4.8% CAGR, driven by aging populations and increased prevalence of chronic asthma.

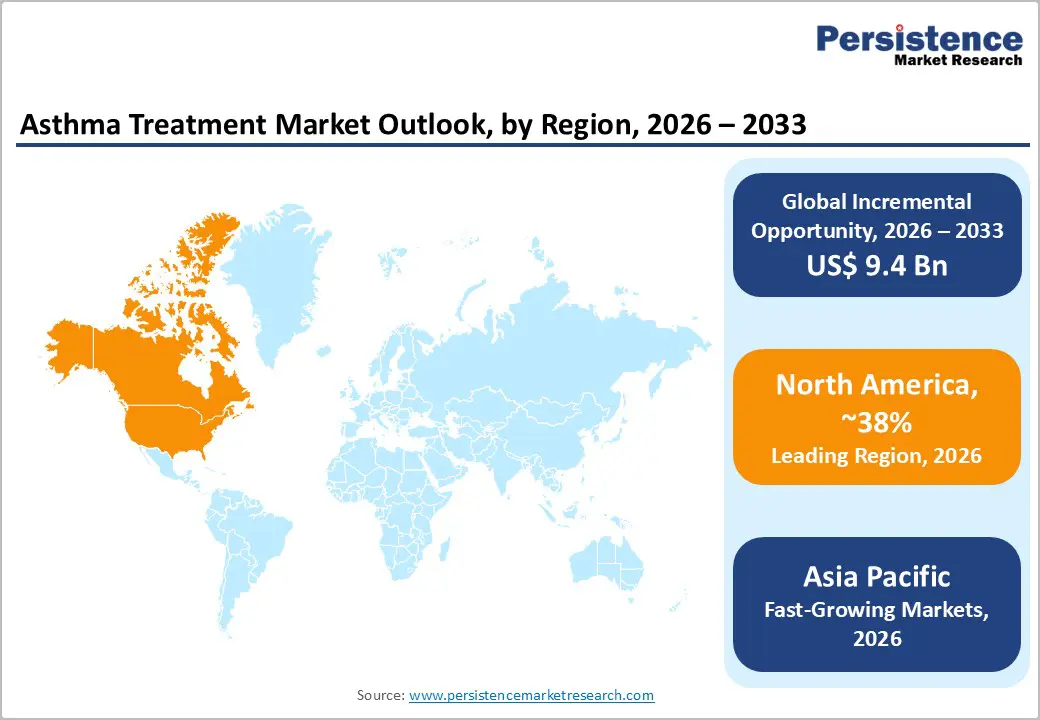

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026 and register a 4.5% CAGR through 2033, supported by advanced healthcare infrastructure and high adoption of digital inhaler technologies.

- Competitive Environment: Market dynamics include strategic product launches, digital inhaler platform integration, M&A activity, and expansion into emerging markets, particularly the Asia Pacific, to capture high-growth opportunities.

| Key Insights | Details |

|---|---|

|

Asthma Treatment Market Size (2026E) |

US$ 29.2 Bn |

|

Market Value Forecast (2033F) |

US$ 38.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.0% |

DRO Analysis

Driver - Rising Global Asthma Prevalence and Advanced Care Adoption

The global prevalence of asthma continues to rise due to urbanization, air pollution, and lifestyle changes, affecting hundreds of millions worldwide and increasing demand for effective therapies. Adoption of long-term controller medications, particularly inhaled corticosteroids (ICS) and combination therapies, is expanding as clinicians follow guideline-based care. Public health campaigns and improved diagnostic access in emerging economies have further increased treatment penetration and early intervention rates. Enhanced awareness programs and patient education initiatives also encourage adherence and proper disease management, thereby reducing hospitalizations and emergency visits.

The FDA approved a generic version of fluticasone propionate inhalation aerosol, improving affordability and patient access for long-term ICS therapy. In addition, updates from the American College of Chest Physicians (CHEST) emphasized personalized therapy and switching strategies, highlighting evidence-based care. These initiatives accelerate the adoption of standardized treatments, reduce uncontrolled asthma prevalence, and strengthen the market for advanced therapies. Combined with ongoing urbanization and rising healthcare access in emerging markets, these factors continue to drive robust market expansion.

Biologics and Innovative Drug Delivery Technologies

The rise of biologic therapies targeting immunologic pathways such as IgE and interleukins IL-5 and IL-4/13 is transforming treatment for moderate-to-severe asthma. Biologics are increasingly prescribed for patients inadequately controlled with conventional bronchodilators and ICS, offering reduced exacerbation rates, steroid-sparing benefits, and improved lung function. Regulatory approvals of next-generation biologics have expanded therapeutic options, supporting higher prescription volumes and revenue diversification. Growing acceptance of these therapies among healthcare providers and patients further reinforces their market penetration.

Technological innovations are further reshaping the market. In 2025, the FDA cleared HeroTracker® Sense, a Bluetooth-enabled device converting standard inhalers into smart devices for adherence tracking and real-world monitoring. Australia’s National Asthma Council updated guidelines to favor anti-inflammatory controllers over short-acting relievers, reinforcing patient-centric management. These developments improve treatment outcomes, adherence, and digital integration, boosting demand for advanced therapies and supporting market expansion across diverse geographies. Additionally, rising patient preference for convenient, technology-enabled monitoring solutions is expected to accelerate the adoption of connected inhalers and enhance long-term disease control.

Restraints - High Treatment Costs and Access Barriers

The high cost of advanced asthma therapies, particularly biologic agents and combination inhalers, remains a major barrier to widespread adoption. In lower-income and emerging regions, limited reimbursement coverage and reliance on out-of-pocket payments restrict patient access, slowing market penetration. Economic disparities influence patient adherence, resulting in suboptimal disease control and increased risk of exacerbations. These financial constraints also affect healthcare providers' prescribing patterns, as clinicians balance efficacy with affordability. Access issues are compounded by disparities in healthcare infrastructure, limiting the availability of specialty clinics and trained personnel for biologic administration.

A U.S. Senate report in early 2026 noted that replacement of commonly used inhalers with higher-priced alternatives disrupted insurance formularies, raising out-of-pocket costs and reducing access, particularly for vulnerable populations. Simultaneously, intermittent supply disruptions for key combination inhalers limited availability at community pharmacies, demonstrating how pricing and supply-chain issues collectively constrain treatment adoption. Even FDA-approved generics take time to achieve meaningful patient access, reinforcing affordability and access as persistent hurdles. These factors together slow market growth in regions with high unmet asthma needs.

Regulatory and Approval Challenges

Stringent regulatory requirements for novel drug approvals and medical device clearances, including FDA and EMA pathways, can delay market entry and elevate development costs. Approval timelines for next-generation biologics or enhanced delivery devices are often prolonged, creating uncertainties for manufacturers and investors. Compliance with post-market safety monitoring, reporting obligations, and pharmacovigilance further adds to the complexity of product life cycle management. These challenges can also limit small and mid-sized companies' entry into the market, consolidating opportunities among larger players.

Recent developments underscore these constraints. In 2025, Savara Inc. received an FDA Refusal to File (RTF) letter for its Biologics License Application (BLA) for MOLBREEVI, a respiratory therapy candidate, because the submission lacked complete Chemistry, Manufacturing, and Controls (CMC) data, delaying review despite potential clinical value. This illustrates how regulatory completeness requirements can extend development timelines and increase costs. Even with the 2026 FDA approval of a generic fluticasone propionate inhalation aerosol, distribution challenges and slow prescriber adoption prevented immediate resolution of access issues. Such regulatory and operational hurdles emphasize the complexity of launching advanced therapies, affecting R&D investment strategies and competitive positioning across regions.

Opportunities - Expansion in Emerging Asia Pacific Markets

Emerging economies in the Asia-Pacific region, including China, India, and Southeast Asia, are expected to see strong growth in asthma treatment demand. Rising asthma prevalence, coupled with increasing urbanization and environmental pollution, is expanding the patient population requiring effective therapies. Improved healthcare infrastructure and growing public and private investment in pharmaceuticals provide a supportive environment for market entry and expansion.

Recent government-supported initiatives reinforce this opportunity. In 2025, a quality improvement program across 31 hospitals emphasized guideline-based asthma care and structured ICS therapy, increasing treatment adoption and patient outcomes. Expanded reimbursement schemes and healthcare investments reduce out-of-pocket costs, while infrastructure growth in India and Southeast Asia enhances distribution networks. Strategic collaborations with local manufacturers and targeted awareness campaigns further improve patient access, enabling pharmaceutical companies to capture incremental demand for both standard and advanced asthma therapies, strengthening their long-term regional presence.

Personalized Medicine and Digital Health Integration

The shift toward precision medicine, including biomarker-guided therapy, offers significant growth potential in asthma management. Treatments tailored to patient-specific immunologic phenotypes, such as eosinophilic or allergic asthma, improve clinical outcomes, reduce exacerbations, and support premium product positioning. These innovations align with broader healthcare trends emphasizing outcome-based care and value-based pricing models, incentivizing the adoption of advanced therapies.

Digital health and telemedicine advancements further reinforce market expansion. At the HIMSS25 APAC Health Conference in 2025, leaders highlighted the adoption of remote monitoring, connected inhalers, and telehealth platforms to enhance chronic disease management in the Asia-Pacific. Additionally, in Japan, the 2026 regulatory approval of Dupixent for children aged 6–11 years expanded access to advanced biologic therapy, creating new patient segments. Combined with growing patient digital literacy and integration of wearable devices for adherence tracking, personalized therapies and technology integration increase adherence, generate real-world data, and support long-term revenue growth for asthma treatments, while creating opportunities for innovative care delivery models.

Category-wise Analysis

Drug Class Insights

Inhaled corticosteroid therapies are projected to lead the asthma drug class with an estimated 43% share in 2026, driven by robust clinical evidence and guideline recommendations as first-line controllers. They effectively reduce chronic inflammation, improve lung function, and lower exacerbation frequency across pediatric and adult populations. ICS combined with long-acting bronchodilators (LABA) provides symptom control and long-term maintenance, reinforcing clinician confidence. Sustained reliance on these therapies for initial management, ongoing guideline emphasis, and refinements in formulation enhance lung deposition and safety. Broad reimbursement coverage and prescriber familiarity further support market stability.

Are biologic therapies the fastest-growing drug class, projected to expand at a 4.9% CAGR through 2033, by precisely targeting immunologic drivers such as IL-5, IL-4/13 in severe asthma that remains uncontrolled with conventional treatment. Their strong clinical efficacy in reducing exacerbations and improving lung function has accelerated adoption in adult and adolescent populations who require advanced care. In late 2025, the UK and European regulators advanced approvals for GSK’s ultra-long-acting biologic depemokimab as a twice-yearly add-on treatment for eosinophilic severe asthma, expanding access to injectable biologics in key markets. Continued guideline integration and broader reimbursement support are expected to further elevate clinician confidence and patient uptake, reinforcing biologics as a key growth pillar in the asthma drug landscape.

Route of Administration Insights

The inhaled route remains dominant, with an estimated 58% share in 2026, due to its direct delivery to the airways, enabling rapid symptom control and sustained management with lower systemic exposure. Devices including MDIs, DPIs, soft-Mist inhalers and nebulizers are preferred by clinicians for routine care and are supported by guideline updates that reinforce inhaled corticosteroids and combination therapies as foundational treatment components. A 2026 clinical update in asthma diagnosis and management reinforced that all symptomatic asthma patients should receive an inhaled corticosteroid regimen, even those with mild symptoms, to improve outcomes and reduce flare-ups, underlining the continued reliance on inhaled care.

Injectable therapies, mainly biologics, are the fastest-growing route of administration, with an estimated 5.1% CAGR through 2033, driven by expanding use in severe and phenotype-specific asthma populations. Injectables such as monoclonal antibodies provide targeted reductions in airway inflammation and have demonstrated clinical benefits, including reduced hospitalizations and steroid dependence. In December 2025, the U.S. FDA approved the ultra-long-acting biologic depemokimab (Exdensur) for add-on maintenance therapy in adolescents and adults with severe eosinophilic asthma, offering a convenient twice-yearly administration model that may improve adherence compared with more frequent dosing schedules. These approvals and broader acceptance across major markets are expanding the clinical footprint of injectable delivery, strengthening its role as a high-growth segment in asthma treatment.

Regional Analysis

North America Asthma Treatment Market Trends

North America remains the largest asthma therapeutics market, with an estimated 38% revenue share in 2026, driven by high disease prevalence, advanced healthcare infrastructure, and broad payer support for combination inhalers and advanced biologics. The U.S. accounts for the majority of demand, with clinicians integrating phenotype-based regimens into routine care and placing a strong emphasis on evidence-based treatment. Regulatory pathways, including FDA expedited review programs, support innovation while robust reimbursement coverage enhances patient access and adherence. Telehealth expansion and smart inhaler adoption improve remote monitoring and long-term management, reducing acute episodes and costs.

In the regulatory landscape, 2025 saw the U.S. FDA expand Tezspire (tezepelumab) for chronic rhinosinusitis with nasal polyps, expanding use beyond severe asthma and reinforcing biologic uptake in inflammatory respiratory care. This milestone underscores the region’s innovation ecosystem, anchored by substantial clinical research activity in targeted therapies. Integrated care networks and population health initiatives increase early diagnosis and preventive care. Investment in respiratory research and expansion of smart inhaler technology further consolidate North America’s leadership position.

Europe Asthma Treatment Market Trends

Europe is supported by mature universal healthcare systems, robust national reimbursement frameworks, and evidence-driven clinical guidelines that prioritize controller therapies and advanced biologics. Key markets such as Germany, the U.K., France, Italy, and Spain provide structured access to a wide range of asthma medications, fostering broad treatment penetration across patient demographics. Regulatory harmonization via the EMA enables coordinated approvals, reducing cross-border variability and speeding market entry for innovative therapies. Environmental pressures, including rising urban air pollution and aging populations, sustain chronic care demand and clinician focus on adherence optimization.

In 2025, the EMA’s Committee for Medicinal Products for Human Use issued a positive opinion on GSK’s ultra-long-acting biologic depemokimab as add-on therapy for severe type 2 asthma, with final approval expected in 2026. The anticipated launch of this twice-yearly biologic reflects growing interest in less frequent dosing and improved adherence. Cost-containment policies and growing emphasis on real-world outcomes influence formulary negotiations for expensive therapies, encouraging manufacturers to demonstrate pharmacoeconomic value. Digital health initiatives and integrated patient monitoring further enhance treatment effectiveness and support sustained regional growth.

Asia Pacific Asthma Treatment Market Trends

Asia Pacific is the fastest-growing regional asthma market, with a projected CAGR of 4.5% through 2033, supported by rising asthma prevalence, expanding healthcare access, and increasing disposable income across key markets. China and India represent substantial patient populations, with environmental risk exposures and urbanization driving demand for controller therapies, combination inhalers, and advanced biologics. Healthcare reforms that broaden insurance coverage and reimbursement accelerate access to guideline-based care and specialty treatments. Telemedicine, outpatient clinic expansion, and digital adherence platforms strengthen chronic disease management beyond metropolitan centers.

In 2025, the World Health Organization launched global initiatives focused on universal access to affordable inhaled therapies and strengthening primary care systems for respiratory diseases, advocating inclusion of inhalers on essential medicine lists worldwide. This global advocacy supports policy changes and domestic health planning across the Asia Pacific, particularly in low and middle-income countries. Local manufacturing partnerships with multinational pharma companies enhance cost-effective distribution and supply reliability. Public education campaigns, school-based screening efforts, and investment in respiratory care infrastructure further deepen diagnosis and treatment uptake. These factors position the Asia Pacific as a key long-term growth engine in the global asthma therapeutics landscape.

Competitive Landscape

The global asthma treatment market is moderately consolidated, with leading pharmaceutical and biotech companies such as GlaxoSmithKline, AstraZeneca, Novartis, Sanofi, and Teva accounting for a significant share of the market. These companies leverage extensive healthcare networks, regulatory expertise, and broad portfolios across ICS, combination therapies, and biologics. They continue to invest heavily in R&D, focusing on next-generation biologics, patient-centric digital inhalers, and adherence monitoring technologies. Their established clinical relationships, guideline-aligned products, and robust distribution channels reinforce market leadership and ensure sustained revenue streams.

Regional and niche players, including Hikma Pharmaceuticals, Cipla, and Lupin, are focusing on generics, localized manufacturing, and emerging market penetration. Entry barriers such as regulatory compliance, high treatment costs, and complex clinical trials limit new competitors. However, digital health adoption, including telemedicine platforms, connected inhalers, and remote patient monitoring, provides growth opportunities for innovative smaller firms. Strategic acquisitions and partnerships by global leaders are further driving geographic expansion and portfolio diversification, creating a dynamic competitive environment.

Key Industry Developments:

- In January 2026, GSK acquired RAPT Therapeutics for US$ 2.2 billion, gaining access to experimental therapies targeting inflammation. The deal strengthens GSK’s long-acting asthma portfolio and supports innovation for severe and uncontrolled cases.

- In January 2026, Sanofi completed the US$ 9.5 billion acquisition of Blueprint Medicines, expanding its late-stage portfolio to offset upcoming patent expirations. This move enhances targeted treatment options and secures its leadership in respiratory therapies.

- In October 2026, Novartis purchased Avidity Biosciences for US$ 12 billion, reinforcing its respiratory immunology pipeline. The acquisition accelerates the development of biologics for severe asthma and supports precision therapy strategies.

Companies Covered in Asthma Treatment Market

- GlaxoSmithKline plc

- AstraZeneca plc

- Teva Pharmaceutical Industries Ltd.

- Sanofi

- Merck & Co., Inc.

- Boehringer Ingelheim International GmbH

- Novartis AG

- Sunovion Pharmaceuticals Inc.

- Cipla Ltd.

- Roche Diagnostics

Frequently Asked Questions

The global asthma treatment market is projected to reach US$ 29.2 billion in 2026.

Rising global asthma prevalence, adoption of advanced therapies, and improved access in emerging markets drive market growth.

The market is expected to grow at a CAGR of 4.1% from 2026 to 2033.

Expansion in emerging Asia Pacific markets and adoption of biologics and digital inhalers present significant opportunities.

GlaxoSmithKline, AstraZeneca, Novartis, Sanofi, Teva, and Cipla are among the leading market players.