- Medical Devices

- Micro Injection Molding Medical Devices Market

Micro Injection Molding Medical Devices Market Size, Share, and Growth Forecast 2026 - 2033

Micro Injection Molding Medical Devices Market by Product Type (Drug delivery devices, Surgical instruments, Implantable components, Microfluidic devices, others), Material (Thermoplastics, Elastomers, Silicone, Biodegradable polymers), Application (Clinical Diagnostics, Therapeutics, Research Purpose), and Regional Analysis, 2026 - 2033

Micro Injection Molding Medical Devices Market Share and Trends Analysis

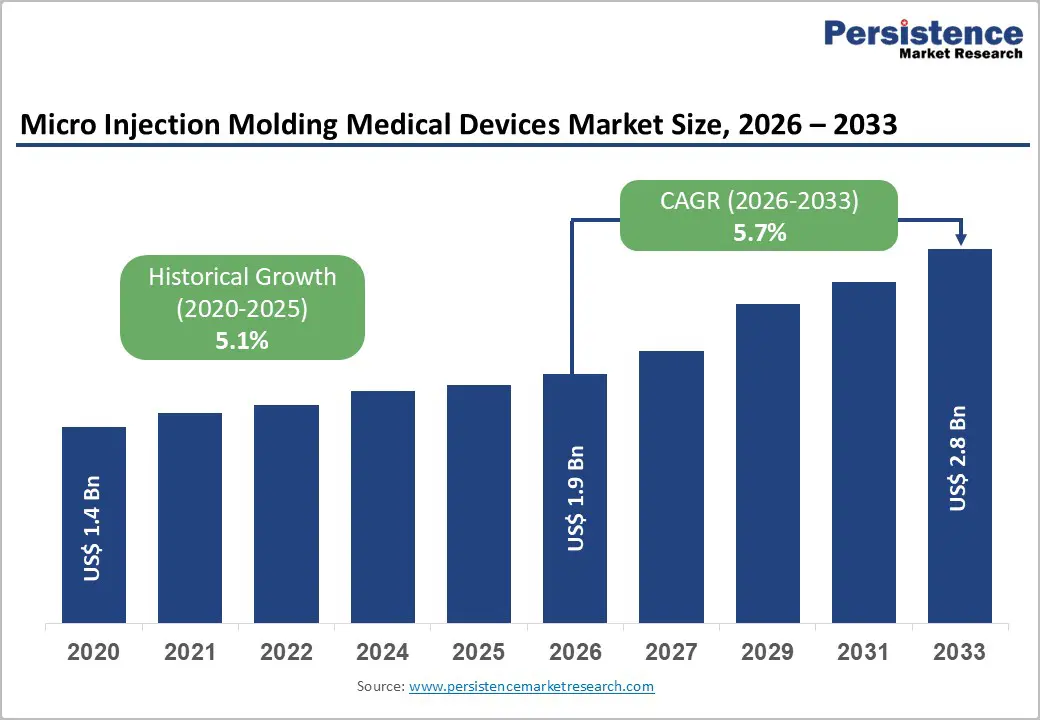

The global micro injection molding medical devices market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

This growth trajectory is propelled by the accelerating demand for miniaturized medical components in minimally invasive surgical procedures, expanding adoption of advanced drug delivery systems, and increasing prevalence of chronic diseases requiring sophisticated diagnostic and therapeutic interventions. The market is further supported by stringent regulatory frameworks emphasizing precision manufacturing standards such as ISO 13485:2016 and FDA 21 CFR Part 820, coupled with technological advancements enabling micron-level tolerances below ±10 μm in component fabrication for critical applications, including neurovascular devices, intraocular lenses, and microfluidic diagnostic platforms.

Key Industry Highlights:

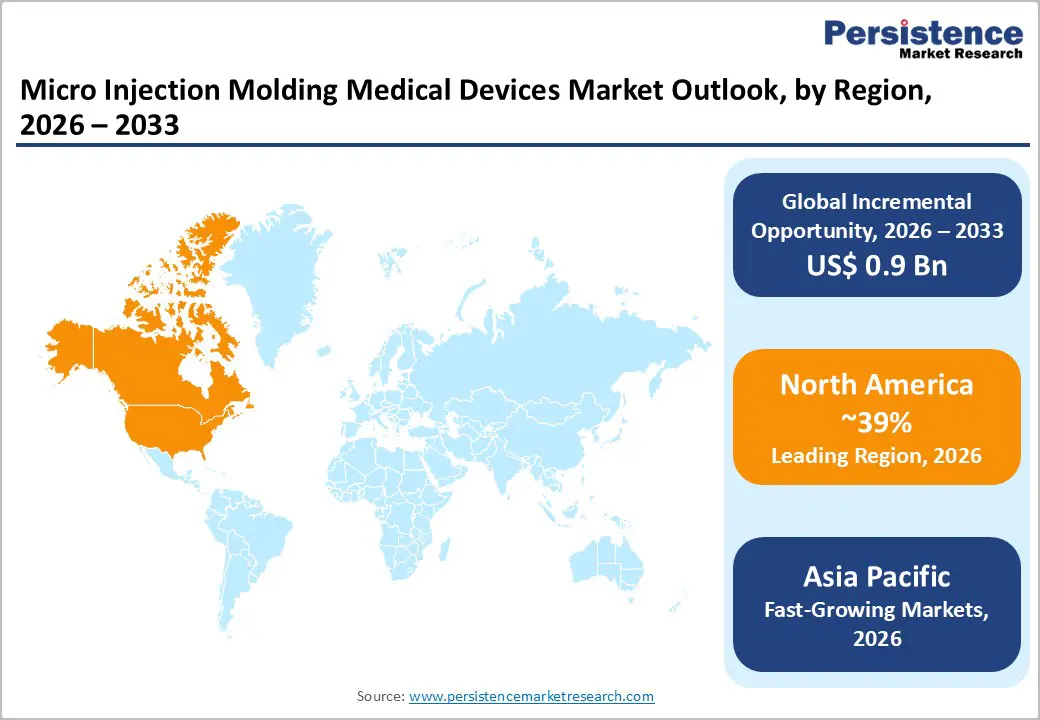

- Regional Leadership: North America maintains market leadership commanding 39% share in 2025, supported by concentration of specialized micro molding manufacturers, stringent regulatory frameworks establishing quality benchmarks, and substantial investments in advanced manufacturing technologies, including all-electric injection molding systems, automated cleanroom production cells, and comprehensive metrology capabilities enabling sub-micron dimensional verification for critical medical device components.

- Fast-growing Region: Asia Pacific emerges as the fastest-growing regional market with a CAGR exceeding 6.8% through 2033, propelled by expanding healthcare infrastructure across China, India, Japan, and Southeast Asian nations, favorable manufacturing cost structures attracting multinational medical device production, growing domestic consumption supporting localized supply chains, and government initiatives promoting medical technology innovation and regulatory alignment with international quality standards.

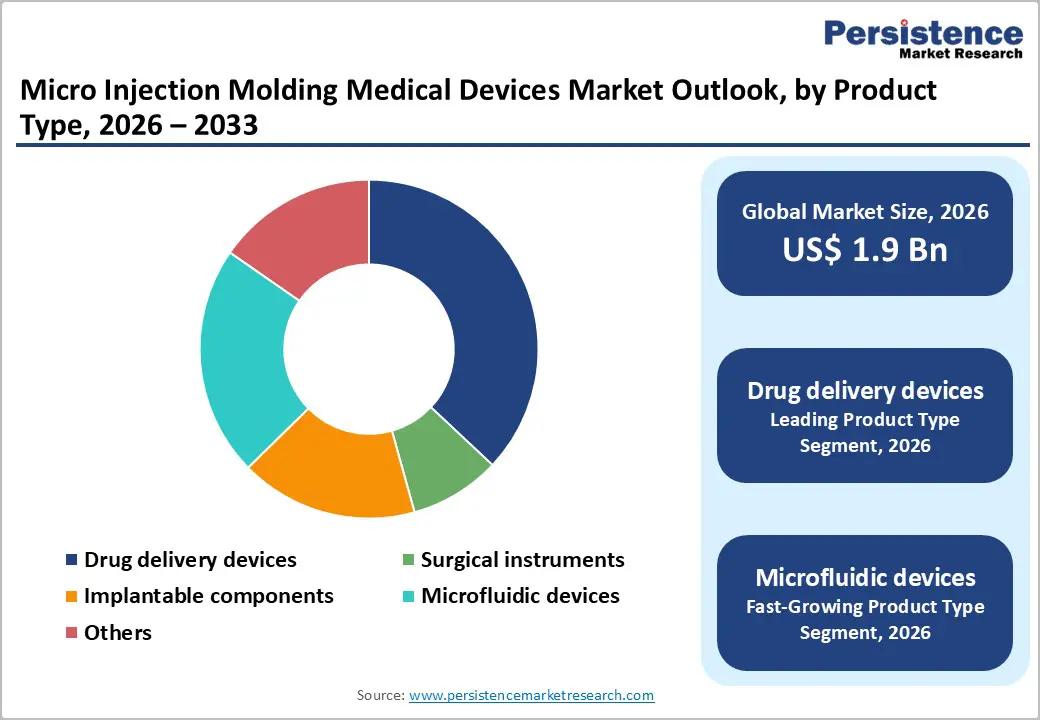

- Dominant Product: Drug delivery devices dominate product type with 37% share, reflecting a critical role in advanced therapeutic administration systems, including GLP-1 autoinjectors, insulin delivery platforms, and wearable infusion pumps requiring precision-molded mechanical actuation components, integrated safety features, and miniaturized assemblies enabling patient-centric self-administration of biologics, biosimilars, and specialty pharmaceuticals driving pharmaceutical industry growth.

| Key Insights | Details |

|---|---|

| Micro Injection Molding Medical Devices Size (2026E) | US$ 1.9 billion |

| Market Value Forecast (2033F) | US$ 2.8 billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Increasing Adoption of Minimally Invasive Surgical Procedures Driving Precision Component Demand

The global shift toward minimally invasive surgical techniques is fundamentally transforming demand patterns for micro-molded medical components with exceptional dimensional accuracy. These procedures require surgical instruments, implantable components, and drug delivery devices with feature sizes as small as a few microns, wall thicknesses reaching 0.15 mm, and component weights under 0.001 grams. The expansion of neurovascular interventions, ophthalmic surgeries, and cardiovascular procedures necessitates components manufactured through micro injection molding to achieve the tight tolerances essential for patient safety and device efficacy. Medical device manufacturers are increasingly leveraging cleanroom molding capabilities meeting ISO Class 7 and ISO Class 8 standards to produce contamination-free components for direct patient contact applications, creating sustained momentum for specialized micro molding technologies across therapeutic categories.

Surging Prevalence of Chronic Diseases Amplifying Demand for Advanced Drug Delivery Systems

The escalating global burden of chronic diseases including diabetes, cardiovascular conditions, and obesity is catalyzing unprecedented growth in sophisticated drug delivery device manufacturing. The glucagon-like peptide-1 (GLP-1) drug delivery market exemplified this trend, expanding from approximately US$ 40 billion in 2023 to around US$ 53 billion in 2024, representing growth of 16-18% annually. This therapeutic category requires precision-molded components for autoinjectors, pen devices, and wearable insulin delivery systems, with manufacturers emphasizing component integration, miniaturization, and patient-centric design. The US$ 16.5 billion acquisition of Catalent by Novo Holdings in February 2024 underscored the strategic importance of fill-finish and injection device manufacturing capacity. Micro injection molding enables the production of complex drug delivery components, including micro-gears, valves, lattice features, and microfluidic channels that enhance dosing accuracy, improve patient compliance, and facilitate the administration of next-generation biologics and biosimilars requiring specialized delivery mechanisms.

Restraints - High Capital Investment Requirements and Process Validation Complexity

The micro injection molding medical devices sector faces significant barriers related to substantial upfront capital investments and rigorous process validation protocols mandated by regulatory authorities. Establishing manufacturing capabilities requires specialized all-electric machinery, advanced tooling with micro-venting strategies below 5 μm, high-magnification in-line metrology systems, and integrated cleanroom facilities complying with ISO 14644 classifications. Process validation following ISO 13485 and FDA Quality System Regulation (21 CFR Part 820) demands extensive documentation, including Design Verification and Design Validation (DV/DV) protocols, Process Failure Mode and Effects Analysis (PFMEA), and Production Part Approval Process (PPAP) documentation. The complexity intensifies for implantable devices and drug-contact components requiring comprehensive biocompatibility testing per ISO 10993 standards, extractables and leachables studies, and sterilization compatibility validation. These stringent requirements extend development timelines, increase cost structures, and create entry barriers, particularly challenging for small and medium-sized medical device manufacturers seeking to adopt micro molding technologies.

Material Selection Constraints and Supply Chain Dependencies

Micro injection molding for medical applications confronts inherent limitations in material selection driven by biocompatibility requirements, sterilization compatibility, and dimensional stability considerations. Medical-grade thermoplastics including polyetheretherketone (PEEK), liquid crystal polymers (LCP), cyclic olefin copolymers (COC/COP), and medical-grade silicones must satisfy USP Class VI specifications and demonstrate stable behavior through autoclaving, gamma radiation, and ethylene oxide sterilization cycles. The specialized nature of these materials creates supply chain vulnerabilities, with manufacturers dependent on certified polymer grades featuring documented lot traceability and consistent performance characteristics. Material costs for medical-grade resins can exceed standard engineering plastics by 300% or more, impacting production economics particularly for high-volume disposable device components. Furthermore, the technical challenges of processing ultra-thin walls and complex geometries with biocompatible polymers require extensive material characterization and process optimization, potentially limiting design flexibility and constraining innovation in emerging application segments.

Opportunity - Exponential Growth in Microfluidic Diagnostic Devices and Point-of-Care Testing Platforms

The convergence of diagnostic testing miniaturization and decentralized healthcare delivery models presents transformative opportunities for micro injection molding technologies. Medical-grade thermoplastics for diagnostic devices and consumables reached US$ 10.2 billion in 2025 and are projected to achieve US$ 23.6 billion by 2032, growing at a 12.7% CAGR. This expansion reflects increasing diagnostic test volumes, molecular and immunoassay diagnostics proliferation, and rising adoption of single-use diagnostic consumables requiring cost-effective, high-volume manufacturing. Micro injection molding enables the production of laboratory consumables, microfluidic cartridges, housings, and fluid-handling components with the chemical resistance, dimensional stability, optical clarity, and sterilization compatibility essential for diagnostic applications. Point-of-care testing devices, lab-on-a-chip platforms, and automated diagnostic systems incorporate complex microfluidic channels, reagent reservoirs, and integrated biosensing components manufactured through precision molding techniques. The ongoing shift from centralized laboratory testing to decentralized diagnostic platforms in emerging markets and home healthcare settings creates sustained demand for affordable, scalable micro-molded diagnostic components across clinical and research applications.

Expansion of Biodegradable Polymer Applications in Implantable Medical Devices

The accelerating adoption of biodegradable polymers for temporary implantable medical devices and tissue engineering scaffolds represents a high-growth opportunity segment for specialized micro injection molding capabilities. Biodegradable polymers including polylactic acid (PLA), polyglycolic acid (PGA), and polycaprolactone (PCL) enable the fabrication of medical implants that gradually resorb within the body, eliminating secondary removal procedures and reducing long-term complications. Micro injection molding of biodegradable polymers addresses applications including drug-eluting cardiovascular stents, orthopedic fixation devices, controlled-release drug delivery systems, and absorbable surgical fasteners. Manufacturers developing expertise in processing biodegradable materials with precise degradation profiles, controlled porosity, and biocompatibility characteristics position themselves strategically for emerging applications in regenerative medicine, personalized implants, and next-generation therapeutic delivery systems requiring temporary mechanical support with programmed resorption kinetics.

Category-wise Analysis

Product Type Insights

Drug delivery devices command a dominant 37% market share within the micro injection molding medical devices sector, reflecting the critical role of precision-molded components in enabling advanced therapeutic administration systems. This leadership position stems from the expanding market for self-administered biologics, including GLP-1 agonists projected to exceed US$ 100 billion by 2030, alongside insulin delivery systems, autoinjectors, and wearable infusion pumps requiring miniaturized mechanical actuation components. Manufacturing innovations enabling all-plastic micro-molded cannulas utilizing polypropylene, PEBAX, or Teflon materials demonstrate the technology's capacity to replace traditional extruded metal components, reducing costs while improving patient comfort through enhanced flexibility. Leading manufacturers, including Accumold, Tegra Medical, and Biomerics have developed specialized capabilities in insert molding, two-shot molding, and overmolding techniques essential for producing complex drug delivery assemblies integrating multiple materials with dissimilar properties within single manufacturing operations.

Application Insights

Clinical Diagnostics constitutes the leading end-use application segment, capturing approximately 42% of micro injection molding medical devices demand, propelled by the global expansion of diagnostic testing infrastructure and the proliferation of point-of-care testing platforms. This dominance reflects the intensive consumption of precision-molded consumables, including microfluidic cartridges, specimen collection vessels, reagent containers, pipette tips, and laboratory automation components requiring dimensional accuracy, optical clarity, and chemical compatibility with diverse biological samples and reagents. In-vitro diagnostic device manufacturing leverages micro injection molding's scalability advantages for single-use consumables, with production volumes often exceeding millions of units annually per device platform. The segment benefits from favorable regulatory pathways for diagnostic consumables compared to implantable devices, shorter product development cycles, and recurring revenue models based on consumable reagent and cartridge sales. Major diagnostic companies including Abbott, Dexcom, and Roche integrate micro-molded components throughout their glucose monitoring systems, point-of-care testing devices, and automated laboratory instruments, establishing sustained demand patterns supporting long-term market expansion.

Regional Insights

North America Micro Injection Molding Medical Devices Market Trends and Insights

North America leads the Micro Injection Molding Medical Devices Market due to its advanced healthcare infrastructure, strong medical device manufacturing base, and early adoption of precision manufacturing technologies. The region benefits from high demand for minimally invasive procedures, driving the use of micro-molded components in drug delivery devices, surgical tools, and diagnostic systems. Rising prevalence of chronic diseases, including diabetes and cardiovascular disorders, further supports demand for high-precision, small-scale medical components. Additionally, the presence of stringent regulatory standards has encouraged manufacturers to adopt micro injection molding for consistent quality, accuracy, and repeatability. Continuous investments in R&D, rapid integration of automation, and strong collaboration between medical device companies and material suppliers continue to reinforce North America’s leadership position.

Asia Pacific Micro Injection Molding Medical Devices Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the Micro Injection Molding Medical Devices Market, supported by rapid healthcare expansion, growing medical device manufacturing, and increasing demand for cost-effective precision components. Countries such as China, Japan, South Korea, and India are strengthening domestic production capabilities and reducing reliance on imports. Rising incidence of chronic diseases, expanding diagnostic testing, and growing adoption of minimally invasive and point-of-care technologies are accelerating the use of micro-molded medical parts. Favorable government initiatives promoting local manufacturing and foreign investments further enhance market growth. In addition, the availability of skilled labor at competitive costs is attracting global medical device companies to establish manufacturing bases in the region. Technological advancements in micro-manufacturing, along with increasing healthcare access and patient awareness, are expected to sustain strong growth momentum across Asia Pacific.

Competitive Landscape

The competitive landscape of the micro injection molding medical devices market is moderately fragmented, characterized by the presence of specialized manufacturers focusing on high-precision and customized solutions. Competition is primarily driven by technological expertise, material innovation, and the ability to deliver consistent micro-scale accuracy. Market participants emphasize investments in advanced tooling, automation, and quality control to meet stringent medical regulatory requirements. Product differentiation is achieved through design flexibility, rapid prototyping capabilities, and support for complex geometries.

Key Developments:

- In September 2025, Resonetics announced that it had acquired Eden Holdings, which included Eden Manufacturing and Eden Tool. The acquisition expanded Resonetics’ capabilities by adding micro-molding, insert-molding, and advanced machining and tooling expertise. It complemented the company’s existing strengths in metal processing while also enhancing its Swiss machining and EDM machining offerings for critical medical device applications.

Companies Covered in Micro Injection Molding Medical Devices Market

- Accumold, Biomerics

- BMP Medical

- Tegra Medical

- MTD Micro Molding

- PEXCO

- Micromolding Solution

- Sovrin Plastics

- Makuta Technics

- Stack Plastics

- Polyzen

- Isometric Micro Molding

- Epson

- OptiMIM

- GianMIM

- Parmaco

- CN Innovations

- NBTM New Materials Group

Frequently Asked Questions

The global micro injection molding medical devices market is expected to be valued at US$ 1.9 billion in 2026.

The market is primarily driven by the accelerating shift toward minimally invasive surgical techniques requiring precision components with micron-level tolerances, the surging prevalence of chronic diseases including diabetes and cardiovascular conditions, necessitating advanced drug delivery devices, and the exponential growth in microfluidic diagnostic platforms supporting point-of-care testing and lab-on-a-chip applications.

North America dominates the global market with a 39% share in 2025, supported by the region's concentration of specialized precision manufacturers.

The expansion of biodegradable polymer applications in implantable medical devices and tissue engineering scaffolds represents the premier growth opportunity, enabling temporary implants that gradually resorb within the body and eliminate secondary removal procedures.

Leading market participants include specialized precision manufacturers Accumold, Biomerics, BMP Medical, Tegra Medical, MTD Micro Molding, PEXCO, Micromolding Solution, etc.