- Pharmaceuticals

- Non-infectious Macular Edema Treatment Market

Non-infectious Macular Edema Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Non-infectious Macular Edema Treatment Market Drug Type (Anti-VEGF, Corticosteroids, Immunosuppressant, Biologics, Others), Indication (Non-infectious Uveitic Macular Edema, Diabetic Macular Edema, Retinal Vein Occlusion with Macular Edema), Route of Administration, Distribution Channel, and Regional Analysis from 2026 to 2033

Non-infectious Macular Edema Treatment Market Share and Trends Analysis

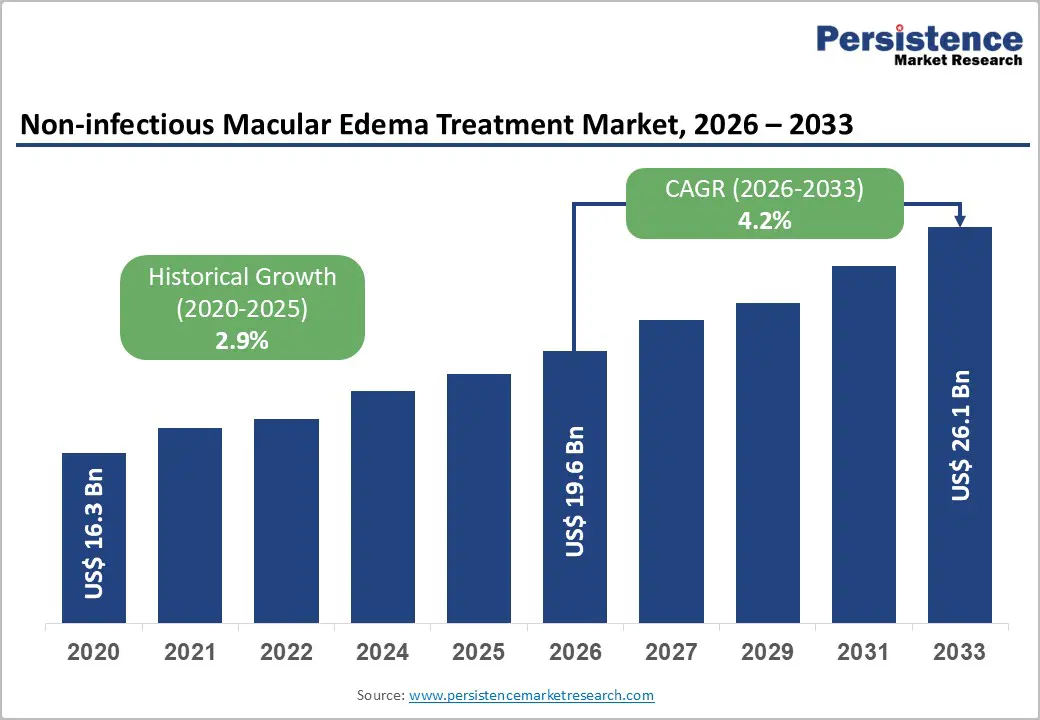

The global non-infectious macular edema treatment market size is estimated to be valued at US$19.6 billion in 2026 to US$26.1 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033.

The global market is experiencing robust growth, driven by the rising prevalence of diabetic macular edema, improved diagnostic technologies, and increasing awareness of vision-related complications. Anti-VEGF therapies dominate first-line treatment, with corticosteroids, immunosuppressants, and sustained-release implants reserved for refractory cases. Advances in long-acting drug delivery, combination therapies, and emerging biologics are enhancing efficacy, reducing side effects, and improving patient compliance. Expanding healthcare infrastructure in emerging economies further fuels market adoption. Overall, the market reflects a dynamic landscape where innovation, patient-centric therapies, and growing disease burden collectively shape opportunities for stakeholders worldwide.

Key Industry Highlights

- The NIME treatment market is projected to expand significantly over the next decade, fueled by rising diabetes prevalence, increased screening, and early intervention strategies.

- Anti-VEGF therapies remain the cornerstone of NIME treatment, widely preferred for their efficacy in reducing retinal swelling.

- Next-generation biologics and immune modulators are gaining attention for their potential to target inflammatory pathways in uveitic macular edema.

- Advanced imaging technologies, such as OCT and fluorescein angiography, facilitate early detection, precise monitoring, and personalized adjustments to therapy.

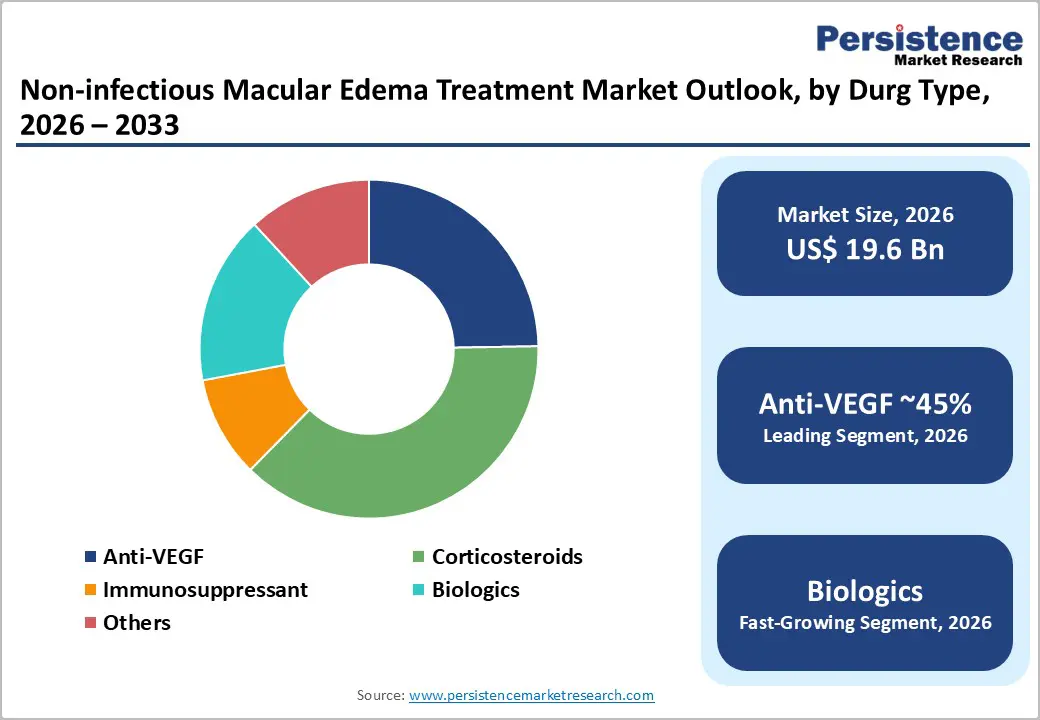

- Leading Drug: Anti-VEGF drugs are the recommended first-line treatment for most NIME cases, including Diabetic Macular Edema (DME) and macular edema associated with retinal vein occlusion.

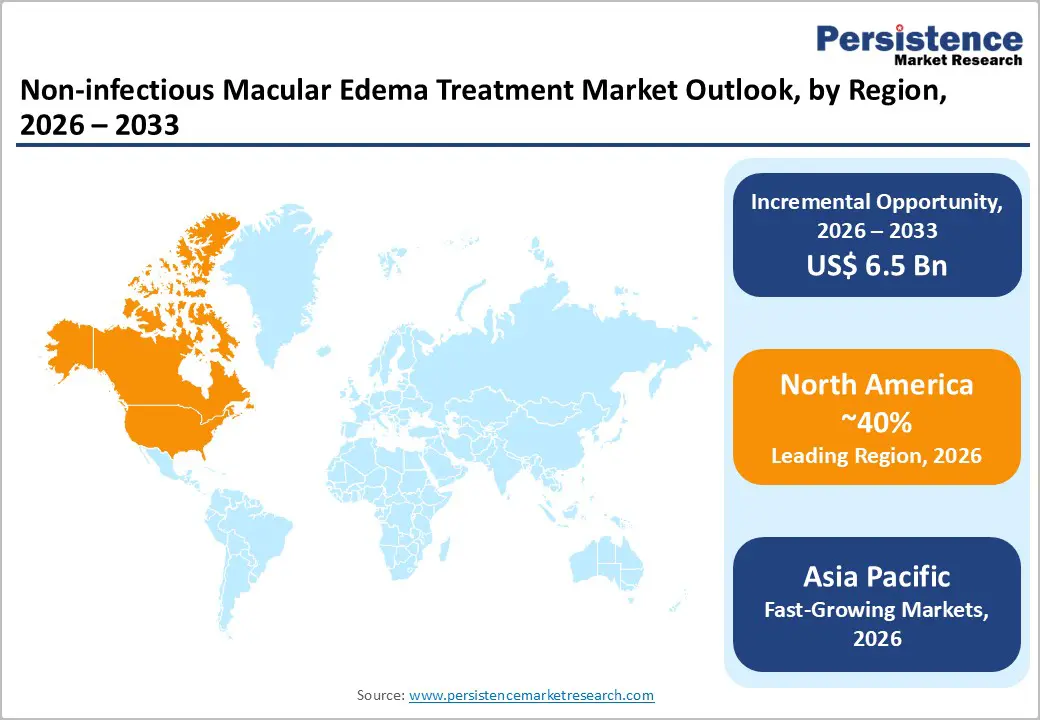

- Leading Region: The North America region has well-equipped hospitals, specialized ophthalmology centers, and experienced retina specialists, enabling widespread diagnosis and treatment of macular edema.

| Key Insights | Details |

|---|---|

| Non-infectious Macular Edema Treatment Market Size (2026E) | US$19.6 Bn |

| Market Value Forecast (2033F) | US$26.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.9% |

Market Dynamics

Driver - Rising Diabetes and Metabolic Disorders

The global surge in diabetes and related metabolic disorders is a key driver of the growth of the non-infectious macular edema (NIME) treatment market. Diabetic macular edema (DME), a leading subset of NIME, arises from chronic hyperglycemia-induced damage to retinal blood vessels, leading to fluid accumulation in the macula and progressive vision impairment. As diabetes prevalence rises, fueled by sedentary lifestyles, unhealthy diets, and increasing obesity rates, the number of individuals at risk of developing DME grows proportionally. This expanding patient pool significantly increases demand for effective treatment options, particularly first-line therapies such as anti-VEGF injections and corticosteroid implants.

Moreover, the rising incidence of metabolic syndrome, hypertension, and dyslipidemia further exacerbates microvascular complications, increasing susceptibility to macular edema. Governments, healthcare providers, and private organizations are responding with increased screening programs and early diagnosis initiatives, creating opportunities for timely therapeutic intervention. Consequently, the intersection of chronic disease prevalence, growing awareness of vision-related complications, and heightened clinical vigilance underscores why rising diabetes and metabolic disorders are a major market driver, shaping investment, research, and adoption trends within the NIME treatment landscape.

Restraints - Treatment-Related Adverse Effects

One of the significant restraints in the Non-infectious Macular Edema treatment landscape is the potential for treatment-related adverse effects, which can limit patient acceptance and long-term therapy adherence. Corticosteroids, commonly administered via intravitreal injections or sustained-release implants, are highly effective in reducing retinal inflammation and edema but carry notable risks. Prolonged corticosteroid use can lead to elevated intraocular pressure, increasing the likelihood of glaucoma, and contributing to cataract formation, both of which may necessitate additional surgical intervention. Similarly, systemic immunosuppressants, while critical in controlling inflammatory pathways in uveitic macular edema, may expose patients to increased susceptibility to infections, liver or kidney toxicity, and other systemic complications.

Even anti-VEGF therapies, although generally safer, can occasionally trigger ocular complications such as intraocular inflammation, retinal detachment, or hemorrhage. These adverse effects not only pose clinical challenges but also impact patient confidence, particularly among those requiring long-term therapy with frequent injections. Consequently, safety concerns remain a key factor shaping treatment decisions, influencing physician recommendations, and restraining broader market adoption, especially in patients with comorbidities or heightened risk profiles.

Opportunity - Emerging Biologics for Uveitic ME

Emerging biologics for uveitic macular edema (ME) represent a promising frontier in the treatment of non-infectious macular edema, particularly for patients who are unresponsive to traditional anti-VEGF therapies. Uveitic ME arises from intraocular inflammation rather than vascular endothelial growth factor-driven mechanisms, making conventional therapies less effective for a subset of patients. Novel biologics, including monoclonal antibodies, fusion proteins, and cytokine inhibitors, are being developed to selectively target specific inflammatory pathways implicated in uveitic ME, such as interleukins (IL-6, IL-1) and tumor necrosis factor-alpha (TNF-α). These therapies aim to reduce retinal edema, preserve photoreceptor integrity, and improve visual acuity while minimizing systemic immunosuppressive side effects.

The niche market for these biologics is driven by increasing awareness of unmet needs in refractory uveitic ME, advances in immunology, and improved regulatory support for orphan or specialty ophthalmic treatments. Early clinical trials have demonstrated encouraging efficacy and safety profiles, attracting interest from both established pharmaceutical companies and biotech startups. As these biologics progress through development, they hold the potential to redefine treatment paradigms, offering personalized, targeted therapy for patients who previously had limited options and enhancing overall quality of life.

Category-wise Analysis

By Drug Type Insights

Anti-VEGF therapies lead the non-infectious macular edema treatment market due to their established efficacy, broad applicability, and strong adoption among ophthalmologists worldwide. These drugs are the recommended first-line treatment for most NIME cases, including Diabetic Macular Edema (DME) and retinal vein occlusion-related macular edema, because they directly inhibit vascular endothelial growth factor, reducing retinal swelling and improving visual acuity. Their safety profile is favorable compared to long-term corticosteroids, which carry risks like elevated intraocular pressure and cataracts, or systemic immunosuppressants, which can cause significant systemic side effects. Anti-VEGF therapies are widely accessible in both developed and emerging markets, supported by reimbursement policies and physician familiarity. Additionally, multiple branded options and biosimilars enhance patient access and affordability. While corticosteroids, biologics, and immunosuppressants serve as secondary or niche options-often for refractory or inflammatory cases-their adoption remains limited, reinforcing Anti-VEGF’s dominance as the leading segment in the NIME treatment market.

By Distribution Channel Insights

Hospital pharmacies dominate the Non-infectious Macular Edema (NIME) treatment market due to the specialized nature of therapy administration and integrated care requirements. Most treatments, including anti-VEGF injections and corticosteroid implants, must be administered under the supervision of trained ophthalmologists in clinical settings, making hospital pharmacies the primary distribution channel. Hospitals provide a comprehensive care ecosystem, combining advanced diagnostics such as Optical Coherence Tomography (OCT) and fundus imaging with treatment and post-procedure monitoring, which reinforces reliance on hospital-based drug dispensing.

Additionally, hospital pharmacies benefit from higher patient volumes, particularly in tertiary care and specialized eye hospitals where macular edema cases are concentrated. Reimbursement mechanisms and insurance coverage are also more streamlined within hospital systems, incentivizing patients to obtain medications directly from hospital pharmacies rather than retail or online sources. In contrast, retail and online pharmacies play a supplementary role, mostly catering to follow-up prescriptions or maintenance therapies, resulting in comparatively lower market share.

Region-wise Insights

North America Non-infectious Macular Edema Treatment Trends

North America leads the Non-infectious Macular Edema (NIME) treatment market, driven by advanced healthcare infrastructure, high disease awareness, and widespread access to specialized ophthalmic care. In the U.S., the rising prevalence of diabetes and an aging population have escalated demand for effective therapies, particularly anti-VEGF injections, which dominate first-line treatment. Hospitals and specialized eye centers are the primary care settings, supported by robust insurance coverage and reimbursement policies that enhance patient access. Technological integration, including OCT imaging and AI-assisted diagnostics, enables early detection and personalized therapy, improving outcomes. Additionally, ongoing clinical trials and rapid adoption of sustained-release corticosteroid implants and emerging biologics reflect a strong focus on innovation. Collectively, these trends reinforce North America, and especially the U.S., as the benchmark market for NIME treatment globally.

Asia Pacific Non-infectious Macular Edema Treatment Market Trends

Asia-Pacific is the fastest-growing region in the Non-infectious Macular Edema (NIME) treatment market, driven by rising diabetes prevalence, an expanding geriatric population, and improving healthcare infrastructure. Countries like India, China, Japan, and South Korea are witnessing increased adoption of advanced ophthalmic therapies, including anti-VEGF injections and corticosteroid implants, as awareness about vision-related complications grows. The region benefits from expanding hospital networks, specialized eye-care centers, and better diagnostic capabilities such as OCT imaging, enabling early detection and management. Government initiatives, health insurance expansion, and increasing patient affordability are further accelerating market growth. Moreover, pharmaceutical companies are targeting Asia-Pacific with localized distribution, cost-effective formulations, and educational programs, making it a key emerging market with high potential for both revenue generation and long-term adoption of innovative NIME therapies.

Competitive Landscape

The non-infectious macular edema (NIME) treatment market exhibits a highly competitive landscape, driven by innovation in drug development, delivery technologies, and biologic therapies. Market players focus on introducing advanced anti-VEGF formulations, sustained-release corticosteroid implants, and emerging immunomodulators to address diverse patient needs. Strategic initiatives, including partnerships, clinical trials, and regional expansions, are intensifying competition. Differentiation through improved efficacy, safety, and patient-centric delivery mechanisms remains key to capturing market share.

Key Industry Developments:

- In October 2025, ANI Pharmaceuticals, Inc. received the U.S. Food and Drug Administration (FDA) approval for an expanded label for ILUVIEN (fluocinolone acetonide intravitreal implant), which included an indication for the treatment of chronic non-infectious uveitis affecting the posterior segment of the eye (NIU-PS).

Companies Covered in Non-infectious Macular Edema Treatment Market

- Novartis AG

- Regeneron Pharmaceuticals, Inc.

- F. Hoffmann-La Roche Ltd.

- Bayer AG

- Allergan plc (AbbVie)

- Pfizer, Inc.

- Alimera Sciences, Inc.

- Bausch Health Companies, Inc. (Bausch + Lomb)

- Santen Pharmaceutical Co., Ltd.

- Boehringer Ingelheim

- Coherus BioSciences

- Amgen, Inc.

- Kodiak Sciences

- GlaxoSmithKline plc

- ANI Pharmaceuticals

Frequently Asked Questions

The global non-infectious macular edema treatment market is projected to be valued at US$19.6 Bn in 2026.

Increasing cases of diabetic macular edema (DME) and retinal vein occlusion elevate demand for effective NIME therapies.

The global non-infectious macular edema treatment market is poised to witness a CAGR of 4.2% between 2026 and 2033.

Integrating anti-VEGF, corticosteroids, and immunomodulators for refractory or recurrent cases presents high clinical value.

Novartis AG, Regeneron Pharmaceuticals, Inc., F. Hoffmann-La Roche Ltd., Allergan plc (AbbVie), and others.