- Processed Food

- Infant Milk Formula Market

Infant Milk Formula Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Infant Milk Formula Market by Product Type (Starting Milk Formula, Follow-on Milk Formula, Toddlers Milk Formula), Age Group (0 to 6 Months, 6 to 12 Months, 12 to 24 Months, 24 to 36 Months), Sales Channel (Supermarkets/Hypermarkets, Chemists/Pharmacies/Drugstores, Specialty Stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Infant Milk Formula Market Share and Trends Analysis

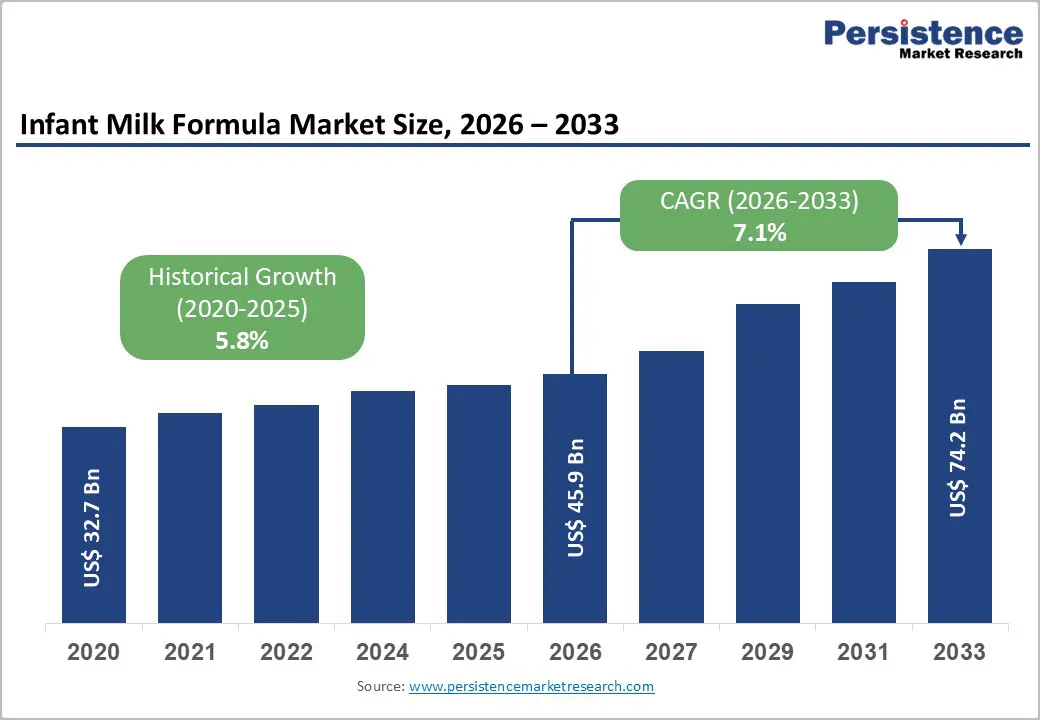

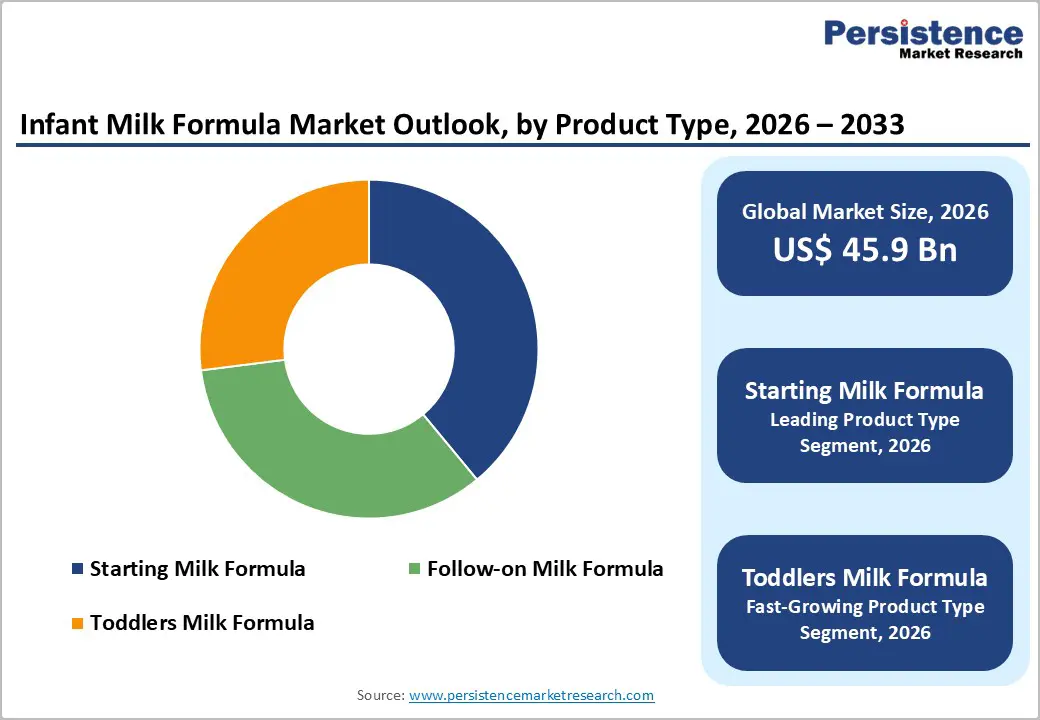

The global infant milk formula market size is expected to be valued at US$ 45.9 billion in 2026 and projected to reach US$ 74.2 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The market is primarily driven by the rise in the rate of female participation in the global workforce and a structural shift toward urban living, which necessitates convenient nutritional solutions. Rising disposable incomes in emerging economies, coupled with increased parental awareness of specialized infant nutrition, have moved the industry from mass-market products toward premium and functional formulations. Furthermore, significant investments from global leaders like Nestlé S.A. and Groupe Danone into Human Milk Oligosaccharides (HMOs) and probiotic enrichment are narrowing the nutritional gap between formula and breast milk, thereby fostering higher consumer trust and adoption rates.

Key Industry Highlights

- Leading Region: Asia Pacific dominated the market in 2025 with a 42% share, driven by rapid urbanization and the world's largest infant population in China and India.

- Fastest Growing Region: Middle East & Africa is identified as the fastest-growing region through 2033, fueled by improving birth rates and rising awareness of infant nutrition in the GCC countries.

- Dominant Product: Starting Milk Formula held a 39% share in 2025, as it remains the primary alternative for mothers unable to breastfeed during the first six months.

- Fastest Growing Product: Toddlers Milk Formula is the fastest-growing product type, benefiting from fewer marketing restrictions and a focus on growing-up nutrition for children aged 1 to 3 years.

- Key Opportunity: The surge in Hypoallergenic and Specialty Formulas represents a significant revenue pocket as pediatric allergies and digestive sensitivities become more prevalent globally.

| Key Insights | Details |

|---|---|

| Global Infant Milk Formula Market Size (2026E) | US$ 45.9 Bn |

| Market Value Forecast (2033F) | US$ 74.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Dynamics

Driver - Increasing Workforce Participation and Rapid Urbanization

One of the most powerful growth catalysts in the global infant milk formula market is the steady increase in working mothers, particularly across emerging economies in Asia Pacific and Latin America. As female labor force participation expands, time constraints around breastfeeding and home-based infant feeding intensify, driving greater reliance on scientifically formulated breast milk alternatives. Parents are increasingly prioritizing products that deliver nutritional adequacy alongside preparation convenience, which has strengthened demand for premium follow-on and ready-to-feed formats.

Rapid urbanization is amplifying this structural shift. Urban households typically operate with nuclear family setups and limited traditional caregiving support, making packaged infant nutrition a practical necessity rather than a discretionary purchase. At the same time, post-pandemic recovery in maternal employment levels has reinforced consumption momentum. Together, these demographic and lifestyle transformations are creating a durable demand foundation for infant milk formula across both developing and mature urban markets.

Restraints - Stringent Regulatory Frameworks and Safety Standards

The infant milk formula industry operates under one of the most stringent regulatory environments in the global food sector, creating substantial entry barriers and elevated compliance costs. Authorities such as the U.S. Food and Drug Administration and the European Food Safety Authority enforce rigorous requirements covering ingredient safety, contaminant limits, clinical validation, and labeling accuracy. Meeting these standards demands significant investment in quality systems, testing infrastructure, and documentation, which can strain both new entrants and mid-sized manufacturers.

Regulatory tightening in major markets has further intensified pressure. Recent upgrades to formula registration rules in China have already forced market consolidation by raising technical and financial thresholds. While these measures strengthen infant safety and product credibility, they also lengthen approval timelines and inflate operating costs. Moreover, periodic product recalls in the category tend to erode consumer trust quickly, creating lingering reputational risks and making demand recovery slower for affected brands.

Opportunity - Surging Demand for Specialty and Hypoallergenic Formulas

A significant growth avenue in the infant milk formula market lies in developing clinically targeted products for infants with specific nutritional sensitivities, including lactose intolerance, cow’s milk protein allergy (CMPA), and prematurity-related needs. Globally, the reported rise in pediatric food allergies and digestive disorders is expanding the addressable market for specialty nutrition. This shift is positioning hypoallergenic, extensively hydrolyzed, and amino-acid-based formulas as one of the fastest-advancing product niches, supported by increasing pediatric diagnosis rates and stronger physician recommendations.

Industry momentum is already visible. In September 2024, Perrigo Company plc announced a strategic partnership to introduce a 100% plant-based, lactose-free infant formula, signaling growing commercial interest in dairy-free innovation. As parents become more medically informed and outcomes-focused, brands that invest in clinically validated, condition-specific formulations are well placed to secure premium pricing power and expand penetration across both hospital procurement and retail channels.

Category-wise Analysis

Product Type Insights

Starting Milk Formula remains the leading segment, capturing a 39% market share. This dominance is attributed to the critical role these products play during the first six months of life, where formula often serves as the sole source of nutrition for non-breastfed infants. However, Toddlers Milk Formula (Stage 3 and above) is the fastest-growing segment through 2033. This trend is driven by the increasing awareness of the specific nutritional requirements of children aged 12 to 36 months, such as higher iron and vitamin D needs. Brands are successfully positioning these products as growing-up milks, extending the customer lifecycle, and ensuring that the formula remains a staple in the child's diet for a longer duration.

Sales Channel Analysis

Supermarkets/Hypermarkets continue to be the dominant sales channel in 2025, providing the scale and physical visibility required for mass-market reach. Parents value the one-stop-shop convenience and the presence of established global brands like Similac and NAN. However, Chemists/Pharmacies/Drugstores hold a significant share of the market for specialized and premium products, where medical endorsements play a key role in the purchase decision. Online Retail is the fastest-growing channel. The rise of direct-to-consumer (DTC) brands and automated subscription services has transformed the purchasing cycle, providing parents with a reliable, hassle-free supply of nutrition while allowing brands to collect valuable first-party consumer data.

Regional Insights

North America Infant Milk Formula Market Trends and Insights

North America remains a critical hub for high-value innovation, characterized by a sophisticated consumer base that prioritizes organic and clean-label products. The United States leads the region, where recent regulatory shifts have encouraged the entry of new domestic and European players to ensure supply chain resilience. In 2025, the market saw a notable rise in demand for A2-protein and grass-fed formulas, driven by health-conscious millennial parents. The presence of major research centers and a robust innovation ecosystem allows for the rapid scaling of new ingredients like probiotics and HMOs.

The U.S. market is also seeing a transition toward DTC models, with brands like Bobbie and ByHeart disrupting traditional retail dominance. Regulatory frameworks are evolving to be more inclusive of international safety standards while maintaining strict domestic oversight. Furthermore, the recovery of hospital channels for clinical infant nutrition has bolstered the sales of premature and specialty formulas. With high disposable incomes and a mature retail infrastructure, North America continues to set the global benchmark for premium infant nutrition trends and packaging innovations.

Asia Pacific Infant Milk Formula Market Trends and Insights

Asia Pacific is the dominant regional market, holding a 42% share in 2025. This leadership is driven by the massive urban populations of China and India, which combined represent the largest infant demographic in the world. In China, the elimination of the one-child policy and the recent implementation of subsidy programs such as the 1.2 billion yuan fund announced by China Feihe Ltd in 2025 aim to boost birth rates and support expectant families. The region is also the manufacturing powerhouse for the industry, with significant investments in local dairy supply chains to reduce import reliance.

The innovation ecosystem in the Asia Pacific is unique, with a heavy emphasis on localized nutrition and functional ingredients that cater to regional digestive patterns. India and ASEAN countries are witnessing a boom in e-commerce penetration, making global brands accessible to tier-2 and tier-3 cities. In China, the National Standard for formula milk, overhauled in 2023, has consolidated the industry, favoring large-scale players with superior R&D capabilities. As disposable incomes rise and urban working patterns become more entrenched, the Asia Pacific is expected to remain the primary engine for global volume and value growth through 2033.

Middle East & Africa Infant Milk Formula Market Trends and Insights

The Middle East & Africa infant milk formula market is being reshaped by tightening regulatory oversight, localization strategies, and affordability pressures. The GCC remains a high-value hub, projected to hold around 37% share in 2025, supported by strong purchasing power and strict compliance enforcement. Authorities such as the Saudi Food and Drug Authority are intensifying scrutiny on Breast-Milk Substitute (BMS) formulations and marketing practices, reinforcing quality benchmarks while raising compliance costs. Despite continued dominance by multinational brands, regional production partnerships are gaining traction, improving halal compliance, supply resilience, and price control across Gulf markets.

Across the North Africa region, the market narrative is increasingly defined by food security initiatives and economic volatility. Egypt’s push toward large-scale domestic manufacturing is lowering import dependence and improving affordability, while price inflation in Morocco and subsidy removals in Lebanon are straining household access.

Market Competitive Landscape

The Infant Milk Formula Market is characterized by moderate-to-high consolidation, where a handful of global conglomerates namely Nestlé S.A., Danone, Abbott, and Reckitt Benckiser command the majority of the market share. These leaders leverage their extensive global distribution networks and massive R&D budgets to maintain dominance. However, the landscape is becoming increasingly dynamic with the rise of digital-native boutique brands that focus on transparency and artisanal quality. Market concentration is particularly high in the Starting Milk Formula segment due to the specialized manufacturing and regulatory barriers involved.

Key differentiators in the current market include proprietary ingredient mixes (such as HMOs and Prebiotics), sustainable sourcing certifications, and advanced digestive-health positioning (e.g., A2 Milk). Emerging business models are pivoting toward an omnichannel approach, combining high-visibility supermarket presence with direct-to-consumer subscription platforms. Research and development are currently focused on using Artificial Intelligence (AI) for personalized infant nutrition and improving the mouthfeel of hydrolyzed formulas to ensure they are more palatable for infants with allergies.

Key Developments:

- In January 2026, Nara Organics announced its first retail launch, expanding distribution of its award-winning organic whole milk infant formula to Target stores nationwide and through the retailer’s online platform.

- In December 2025, Aiwibi announced the launch of a new infant formula developed in partnership with ViPlus, strengthening its global baby care portfolio and expanding its presence in the infant nutrition segment.

- In April 2025, Bobbie revealed plans to launch Bobbie Organic Whole Milk Formula, positioning it as the first USDA Organic whole milk infant formula available in the United States.

Companies Covered in Infant Milk Formula Market

- Abbott Laboratories

- Groupe Danone

- Nestlé S.A.

- Reckitt Benckiser Group plc

- A2 Milk Company

- Royal FrieslandCampina N.V.

- Ausnutria Dairy Corporation

- HiPP GmbH & Co. Vertrieb KG

- Almarai

- Holle baby food AG

- Bobbie Baby

- ByHeart

- Others

Frequently Asked Questions

The global Infant Milk Formula market is projected to be valued at US$ 45.9 Bn in 2026.

Increasing Workforce Participation and Rapid Urbanization is driving demand for Infant Milk Formula market.

The Global Infant Milk Formula market is poised to witness a CAGR of 7.1% between 2026 and 2033.

Surging Demand for Specialty and Hypoallergenic Formulas is creating opportunity for key players in the Infant Milk Formula market.

Key industry leaders include Abbott Laboratories, Groupe Danone, Nestlé S.A., Reckitt Benckiser Group plc, A2 Milk Company, Royal FrieslandCampina N.V., HiPP GmbH & Co. Vertrieb KG, and Others