- Medical Devices

- Incontinence and Ostomy Care Products Market

Incontinence and Ostomy Care Products Market Size, Share, and Growth Forecast, 2026-2033

Incontinence and Ostomy Care Products Market by Product Type (Incontinence: Disposable, Reusable, Skin Care; Ostomy: Pouches, Skin Barriers, Adhesives), Demographics (Pediatric, Adult, Geriatric), Clinical Indication (Urinary Incontinence, Fecal Incontinence, Ostomy), and Regional Analysis for 2026-2033

Incontinence and Ostomy Care Products Market Share and Trends Analysis

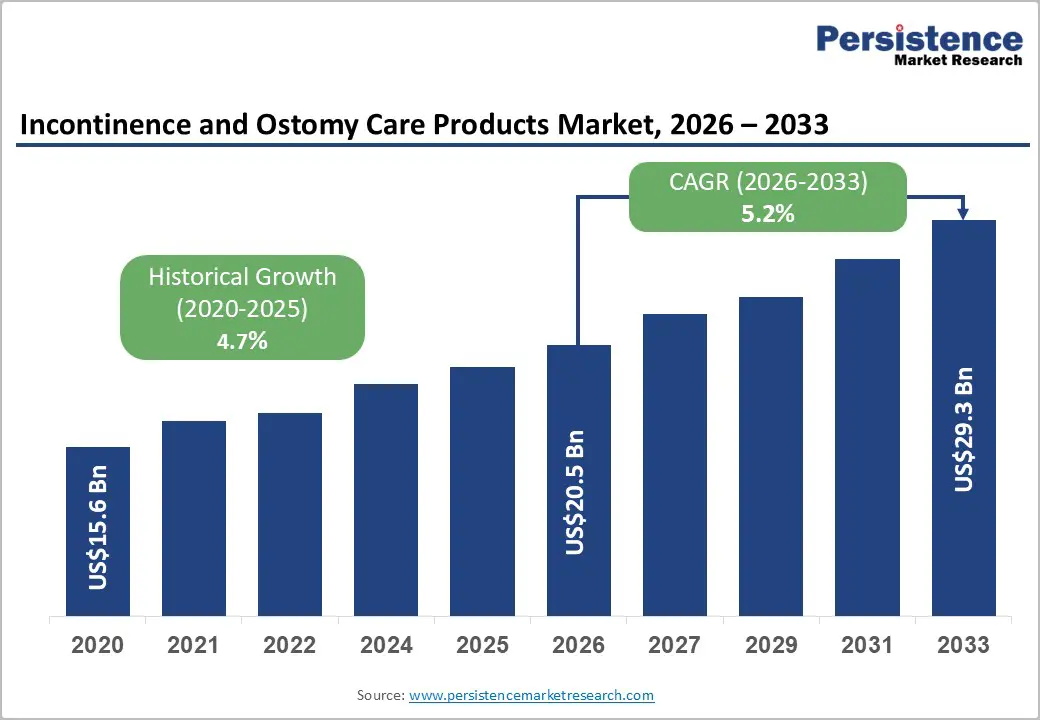

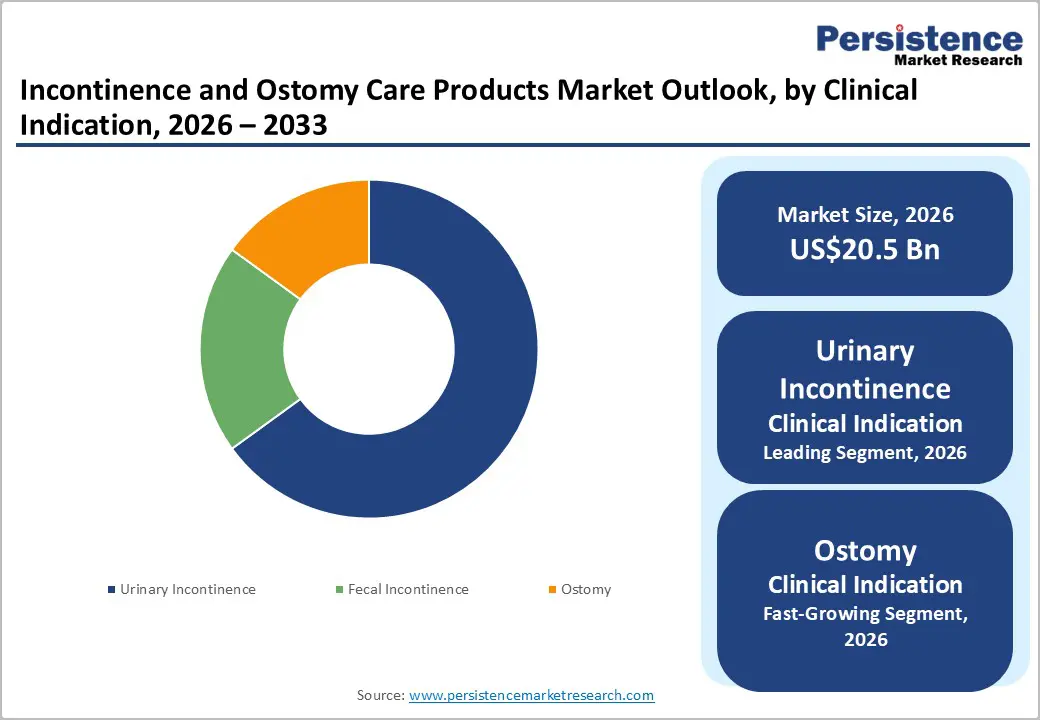

The global incontinence and ostomy care products market size is likely to be valued at US$ 20.5 billion in 2026, and is projected to reach US$ 29.3 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026–2033.

The demand for incontinence and ostomy care products is strongly driven by the growing geriatric population, as individuals aged 65 and above increasingly experience urinary and fecal incontinence or require post-surgical ostomy management. Aging-related physiological changes, coupled with higher prevalence of chronic conditions such as diabetes, neurological disorders, and colorectal cancer, create sustained and recurring need for reliable bladder and bowel care solutions. Manufacturers continue to introduce patient-centric innovations, including advanced absorbent materials, ergonomic designs, odor-control features, and skin-friendly adhesives, which improve comfort, compliance, and overall quality of life. These innovations actively support market expansion by meeting both clinical and home-care demands.

Key Industry Highlights

- Dominant Product Type: Disposable products are projected to command around 75% revenue share in 2026, while ostomy care accessories are likely to grow the fastest through 2033, driven by rising colorectal cancer prevalence.

- Leading Clinical Indication: Urinary incontinence is expected to lead with approximately 65% share in 2026, while ostomy care is anticipated to register the highest 2026-2033 CAGR of 6.5%, reflecting increased surgical interventions.

- Demographic Leadership: Geriatric populations are expected to account for roughly 60% revenue share in 2026, due to higher prevalence of chronic incontinence and post-surgical care needs.

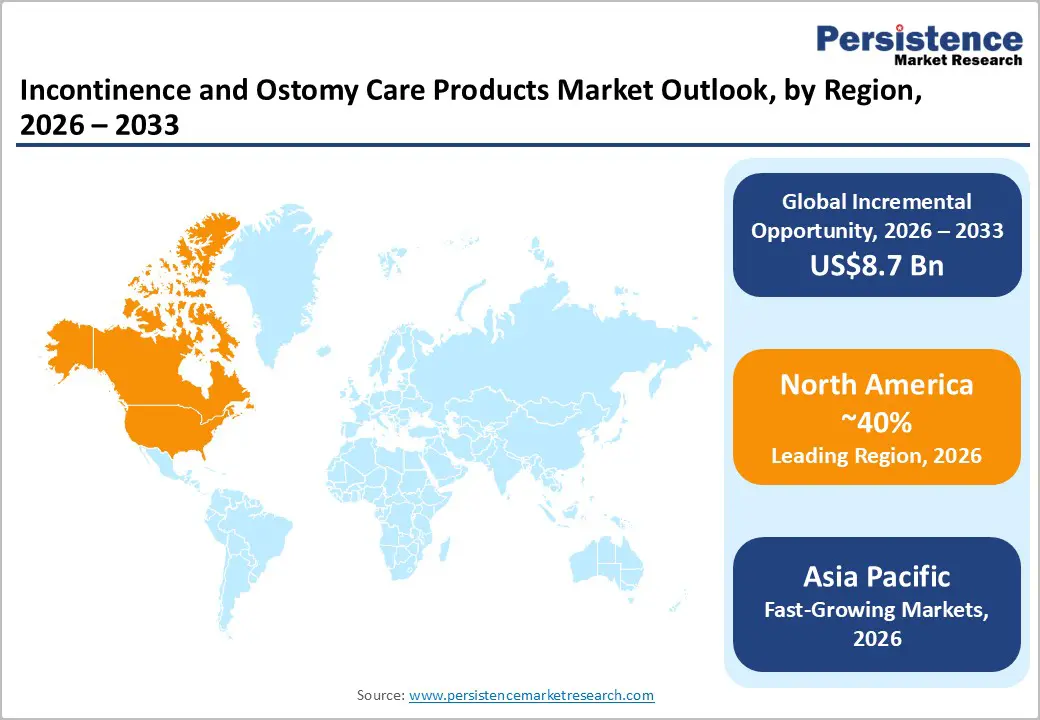

- Regional Leadership: North America is poised to dominate with an estimated 40% share in 2026, whereas Asia Pacific is projected to record the fastest CAGR of 7.2% through 2033, fueled by expanding healthcare infrastructure.

- Technological Innovation: Smart and skin-friendly solutions, including advanced adhesives, odor-control features, and ergonomic designs, are anticipated to drive adoption and improve patient compliance.

- Strategic Developments: Market expansion is supported by ongoing facility expansions, AI-integrated monitoring solutions, and innovation partnerships, targeting both developed and emerging regions for growth.

| Key Insights | Details |

|---|---|

|

Incontinence and Ostomy Care Products Market Size (2026E) |

US$ 20.5 Bn |

|

Market Value Forecast (2033F) |

US$ 29.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Aging Global Population and Rising Chronic Conditions

The global aging demographic (65+) remains a principal driver for the incontinence and ostomy care products market growth. Older adults show higher incidence of urinary incontinence, fecal incontinence, and post-surgical ostomy care needs, which increases demand for reliable management solutions. Aging correlates with chronic illnesses such as diabetes, neurological disorders, and colorectal disorders, reinforcing demand for products used in both clinical and home care settings. Growth in longevity continues to expand the addressable patient population, placing sustained pressure on healthcare systems to provide accessible care. This trend drives manufacturers to innovate products that combine comfort, absorbency, and skin protection.

Real world industry activity supports these demographic trends. For example, Gilgal Medical expanded its national home medical equipment distribution operations in 2025, opening new strategic facilities in Los Angeles and Dallas to shorten delivery times for critical medical supplies directly to patients, nursing homes, and hospitals, including incontinence and ostomy products. Additionally, major distributors such as Henry Schein expanded their homecare portfolio with acquisitions that broaden direct to home supply offerings for patients managing chronic conditions outside traditional clinical settings. These developments demonstrate tangible investment in home based care delivery infrastructure, reinforcing long term demand and improving patient access to essential care products.

Growing Awareness and Technological Advancements in Care Solutions

Heightened awareness and acceptance of incontinence and ostomy care has expanded patient engagement and broadened product utilization beyond clinical settings. Healthcare organizations and advocacy groups are actively reducing stigma and promoting early management strategies, which improves health literacy and consumer confidence. As a result, more individuals pursue proactive care through both institutional and home-based channels, increasing overall product adoption. Educational initiatives also support clinicians in recommending suitable solutions tailored to individual needs. Expanding awareness campaigns contribute to better adherence and sustained usage of advanced care products.

Supporting these awareness and innovation trends, verified industry reports note new product introductions in 2025–2026 that expand therapeutic options. For example, the launch of a novel female external catheter designed to ease severe urinary incontinence reflects ongoing innovation focused on patient comfort and usability. Moreover, regulatory bodies such as the U.S. Food and Drug Administration (FDA)’s Technology Enabled Meaningful Patient Outcomes (TEMPO) pilot announced in late 2025 are encouraging broader adoption of digital and integrated chronic care technologies by lowering barriers to real-world evidence-based device utilization. These developments amplify product value, support adoption of modern patient-centric tools, and drive overall market expansion.

Reimbursement Limitations and Policy Barriers

Even in developed markets, insurance coverage for advanced incontinence and ostomy care products remains inconsistent, especially for premium or specialty solutions. Patients often face significant out-of-pocket expenses, which can delay adoption of innovative products and reduce long-term adherence. Policy gaps, restrictive formularies, and variable reimbursement structures across regions further complicate access to high-quality care. These challenges affect both institutional procurement and direct-to-patient supply, impacting adoption in hospitals, nursing facilities, and home care. Manufacturers must navigate complex pricing and coverage frameworks to maintain market presence and patient reach.

In 2026, the U.S. Centers for Medicare & Medicaid Services (CMS) announced a nationwide moratorium on new Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) enrollment, which includes durable medical equipment and supplies for ostomy and incontinence care. This policy, intended to curb fraud, may reduce competition and delay entry of new suppliers into federal reimbursement programs. Combined with strict documentation requirements under CMS guidelines for ostomy supplies, these procedural and financial barriers continue to constrain patient access, limit market growth potential, and increase administrative costs for manufacturers, particularly affecting smaller players trying to enter the market.

Patient Stigma and Environmental & Sustainability Concerns

Despite ongoing awareness campaigns, social stigma surrounding incontinence and ostomy care continues to persist across many regions worldwide. Patients often delay seeking treatment or avoid using products consistently due to embarrassment, privacy concerns, or fear of social judgment, directly affecting adoption rates. Cultural norms, particularly in conservative societies, combined with low health literacy and limited community or caregiver support, exacerbate this challenge. Stigma can also influence clinicians’ and caregivers’ recommendations, leading to delayed interventions or reliance on basic solutions rather than advanced, patient-centric products. This not only reduces the uptake of premium or technologically advanced solutions but also limits opportunities for manufacturers to expand in-home care and institutional channels.

Environmental scrutiny adds another layer of restraint. In 2025, the European Union (EU) advanced stricter Single Use Plastics regulations, and the Packaging and Packaging Waste Regulation (PPWR) enforcement began in 2026, requiring higher recyclability standards and sustainable material usage. These policies increase operational complexity for manufacturers of disposable incontinence and ostomy products. Compliance with new regulations may raise costs, necessitate redesign of product materials, and slow production. Combined with lingering social stigma, these factors create a dual restraint that limits adoption and challenges global market expansion, particularly in environmentally and socially conscious regions.

Broadening Healthcare Access in Emerging Economies

Developing economies across Asia Pacific, Latin America, and the Middle East & Africa present substantial growth potential due to rapidly improvement in healthcare access, aging populations, expanding healthcare infrastructure, and rising hygiene awareness. Demographic shifts are driving higher prevalence of chronic conditions that require incontinence and ostomy care, including urinary and fecal incontinence among older adults. Governments in these regions are investing heavily in healthcare accessibility, building new clinics, community care centers, and senior-friendly infrastructure to support aging populations. These developments create new points of care for these products and enable manufacturers to expand their local footprint strategically.

For example, Singapore launched enhanced Home Personal Care services and 200 community care apartments in 2026, integrating tech-enabled monitoring and response services for seniors who choose to stay at home. Similarly, China is promoting elderly care services under its economic strategy, offering subsidies and home-care vouchers to meet the needs of its aging population. These initiatives highlight opportunities for manufacturers to capture underserved demand, develop tailored solutions, build partnerships with local providers, and secure long-term revenue growth in high-potential emerging markets, particularly in regions with rapidly growing geriatric populations.

Home Healthcare Services and Product Innovation Ecosystem

The rising adoption of home healthcare services and digital retail channels is creating a transformative opportunity for incontinence and ostomy care products. E-commerce platforms reduce distribution barriers, enabling direct-to-patient access, while telehealth integration supports remote care planning, personalized product recommendations, and adherence monitoring. These technologies allow healthcare providers to track product usage, monitor skin health, and alert caregivers to potential complications, which is critical for patients managing chronic bladder, bowel, or post-ostomy needs at home. Such systems enhance patient confidence, improve compliance, and reduce complications, directly driving consistent product utilization and repeat purchasing.

Real-world movements reinforce this trend. In Australia, St Vincent’s Health announced in 2025 a shift of 50% of care delivery to home and digital settings, expanding remote monitoring and telehealth initiatives. In Japan, telehealth and AI-enabled smart home healthcare adoption accelerated in 2025, allowing clinicians to remotely monitor ostomy pouch usage, skin integrity, and incontinence product adherence. These innovations directly improve patient outcomes, enable home-based care, and generate data-driven insights for manufacturers, supporting development of smarter, more patient-centric products while increasing brand loyalty and repeat revenue.

Category-wise Analysis

Product Type Insights

Disposable incontinence products are expected to dominate the market, accounting for approximately 75% of total revenue in 2026. Their widespread use across geriatric and adult populations is driven by high prevalence of urinary and fecal incontinence, making them essential in both clinical and home care settings. Enhanced absorbency, comfort, and skin protection features have strengthened adoption globally, while caregiver education and patient awareness campaigns reduce stigma and increase consistent usage. In 2025, Medline expanded supply and distribution agreements with the U.S. Department of Veterans Affairs and Ohio State University Wexner Medical Center, ensuring wider availability of incontinence products across hospitals and care networks. These initiatives support steady product adoption and reinforce disposable solutions as the primary revenue driver.

Advanced ostomy care products, particularly pouches with odor control and ergonomic adhesives, are projected to be the fastest-growing sub-segment, with an estimated CAGR of 7.5% from 2026–2033. Growth is fueled by rising incidence of colorectal cancer and increased post-surgical ostomy procedures, alongside greater awareness among healthcare providers and patients. Younger, more active patient cohorts are increasingly adopting these solutions due to enhanced comfort, discreetness, and ergonomic designs. In May 2025, Sumitomo Corporation acquired ActivStyle, LLC, a U.S. home medical supply provider, expanding distribution and accessibility of chronic care products including ostomy supplies Such developments highlight how product innovation, distribution expansion, and patient-centric design are driving growth in the ostomy segment.

Clinical Indication Insights

Urinary incontinence is poised to account for the largest clinical indication, representing an estimated 65% of the incontinence and ostomy care products market revenue share in 2026. The segment is driven by high prevalence in geriatric and adult populations, with disposable products serving as the primary management solution. Improved product designs that focus on absorbency, comfort, and skin health reinforce consistent usage in both hospitals and home care settings. Supporting this, the U.S. FDA approval of Medtronic’s Altaviva™ tibial neuromodulation device in September 2025 highlights ongoing clinical innovation targeting urinary incontinence, increasing patient engagement and interaction with care solutions Alongside Medline’s 2025 distribution expansions, these trends strengthen adoption, enhance product integration in treatment protocols, and maintain urinary incontinence as the primary revenue contributor in clinical indications.

Ostomy care is slated to be the fastest-growing clinical indication, projected to grow at a CAGR of 6.5% during the 2026–2033 forecast period. The growth is driven by increasing colorectal cancer and inflammatory bowel disease rates, which require post-surgical ostomy management. Improved pouches, skin barriers, and adhesives enhance patient comfort, safety, and convenience, supporting consistent use across age groups and care settings. Byram Healthcare’s 2025–26 ostomy catalog demonstrates increased product availability and tailored solutions for patients, reinforcing adoption in home and clinical care. These developments, combined with technological innovations such as ergonomic adhesives and odor control, reinforce patient adoption, premium pricing potential, and long-term segment growth. Ostomy care now represents a strategic growth engine among clinical indications.

Regional Insights

North America Incontinence and Ostomy Care Products Market Trends

North America is predicted to command an estimated 40% of the incontinence and ostomy care products market share in 2026, with the U.S. serving as the regional growth anchor. Rising healthcare expenditure, widespread insurance coverage, and established home and institutional care frameworks support strong product adoption. Regulatory oversight from the FDA ensures product quality, safety, and patient confidence, while reimbursement policies reduce cost barriers for end users. In 2025, Medline expanded supply agreements with the U.S. Department of Veterans Affairs and major hospital networks, improving access to disposable incontinence and ostomy products. Aging demographics and high chronic condition prevalence reinforce demand for both disposable and advanced ostomy care solutions.

Canada’s market mirrors U.S. dynamics, with provincial healthcare systems in Ontario, British Columbia, and Alberta investing in home healthcare expansion and chronic care delivery programs, including ostomy product supply. These initiatives support broader patient access and adoption across home and community care settings. The North America market is concentrated among global majors such as Medline, Coloplast, and Hollister, with domestic distributors driving tailored regional solutions. Competitive dynamics are further enhanced by innovation in patient-centric design, smart monitoring, and AI-enabled home care solutions, reinforcing North America’s leadership in the global market.

Europe Incontinence and Ostomy Care Products Market Trends

The Europe incontinence and ostomy care products market development is supported by harmonized regulatory standards enforced through the European Medicines Agency, ensuring consistent product safety and quality across member states. Germany, the U.K., France, and Spain lead adoption with mature reimbursement frameworks that facilitate patient access to both disposable incontinence solutions and advanced ostomy care products. In 2025, France’s Ministry of Health launched a national home care initiative, expanding distribution of incontinence and ostomy supplies to seniors in community care settings. High patient awareness, clinician-led guidance, and caregiver training further reinforce product integration across hospitals, long-term care facilities, and home healthcare programs, supporting steady market demand.

Eastern European countries are emerging as growth markets as healthcare infrastructure strengthens and disposable incomes rise, enabling broader access to quality care products. Germany, the U.K., and France continue to promote innovation through partnerships between manufacturers and clinical institutions, focusing on patient-centric designs and ergonomic ostomy solutions. Policy-driven elder care programs, chronic disease management initiatives, and hospital based product adoption contribute to a balanced market environment. The competitive landscape features established regional players and multinational companies offering premium portfolios, educational programs, and tailored solutions, ensuring high standards of quality, compliance, and service across the region.

Asia Pacific Incontinence and Ostomy Care Products Market Trends

Asia Pacific is projected to be the fastest-growing regional market for incontinence and ostomy care products market, with an estimated CAGR of 7.2% from 2026 to 2033, driven by demographic shifts toward older age structures in China, Japan, India, and ASEAN nations. Rising healthcare expenditure, expanding middle-class populations, and heightened hygiene awareness are significantly increasing adoption of incontinence and ostomy care products. In 2025, Japan’s Ministry of Health expanded telehealth and home-based monitoring programs, enabling remote care and improved compliance for ostomy and incontinence patients. China is implementing home care pilot programs for seniors, integrating remote supply distribution for chronic care products, while India is accelerating early adoption through digital health and e-commerce channels.

Manufacturing cost advantages and regional production investments support supply chain efficiency and expand product availability across urban and semi-urban areas. Governments are streamlining medical device approvals and incentivizing domestic production, while private distributors enhance e-commerce and home delivery networks. Key market drivers include aging populations, rising chronic condition prevalence, and increasing awareness of patient-centric care. Competitive dynamics involve multinational companies entering emerging markets alongside local distributors offering tailored, affordable, and culturally appropriate products, positioning Asia Pacific as a major growth engine for the global market.

Competitive Landscape

The global incontinence and ostomy care products market structure is moderately consolidated, with leading players such as Coloplast, Hollister, ConvaTec, and Medline capturing a significant revenue share. These companies leverage strong hospital, home care, and long-term care networks while investing in R&D for skin-friendly materials, ergonomic ostomy pouches, odor control, and smart monitoring solutions. Their focus on patient-centric innovation ensures consistent adoption and brand loyalty. Strategic facility expansions and product portfolio enhancements reinforce their market leadership.

Regional and niche competitors, including Byram Healthcare and Sumitomo Corporation, target specialized segments and local distribution channels in underserved markets. Barriers such as regulatory approvals, reimbursement policies, and strict quality compliance limit new entrants. However, digitalization through e-commerce, telehealth, and AI-enabled care solutions enables innovative startups to participate. Consolidation is expected as global leaders pursue acquisitions and strategic partnerships, while smaller firms integrate digitally to enhance service offerings and patient outcomes.

Key Industry Developments

- In February 2026, Nonwovenn expanded its PFAS-free ostomy care filtration range, introducing activated carbon filter media designed for ostomy pouches. The new materials deliver effective odor and gas adsorption while meeting growing regulatory requirements and sustainability expectations.

- In February 2026, Coloplast completed its acquisition of Uromedica, a U.S. medtech company specializing in implantable balloon therapies for stress urinary incontinence. The transaction, with undisclosed financial terms, expands Coloplast’s Interventional Urology portfolio and integrates Uromedica’s talent and technology.

- In January 2026, Axena Health partnered with Mayo Clinic to develop AI-driven solutions for urinary incontinence and overactive bladder. Supported by its US$ 25 million Series A investment in 2023, the collaboration aims to deliver personalized care pathways and improve patient adherence.

Companies Covered in Incontinence and Ostomy Care Products Market

- Essity AB

- Coloplast A/S

- Kimberly Clark Corporation

- Hollister Incorporated

- B. Braun SE

- Convatec Group PLC

- Becton Dickinson

- Salts Healthcare Ltd

- Byram Healthcare Centers, Inc.

- Unicharm Corporation

- Medline Industries LP

Frequently Asked Questions

The global incontinence and ostomy care products market is projected to reach US$ 20.5 billion in 2026.

Rising number of geriatric individuals, increasing chronic conditions, and patient-centric product innovations are driving market growth.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Expansion in emerging economies and growth of home healthcare and e-commerce channels are creating novel market opportunities.

Coloplast, Hollister, ConvaTec, Medline, Byram Healthcare, and Sumitomo Corporation are some of the leading players in the market.