- Specialty & Fine Chemicals

- Hypophosphorous Acid Market

Hypophosphorous Acid Market Size, Share, and Growth Forecast, 2026 - 2033

Hypophosphorous Acid Market by Grade (Industrial Grade, Others), Application (Electroplating, Catalyst in Chemical Synthesis, Others), End-user Industry (Chemical Manufacturing, Others), and Regional Analysis for 2026 - 2033

Hypophosphorous Acid Market Size and Trends Analysis

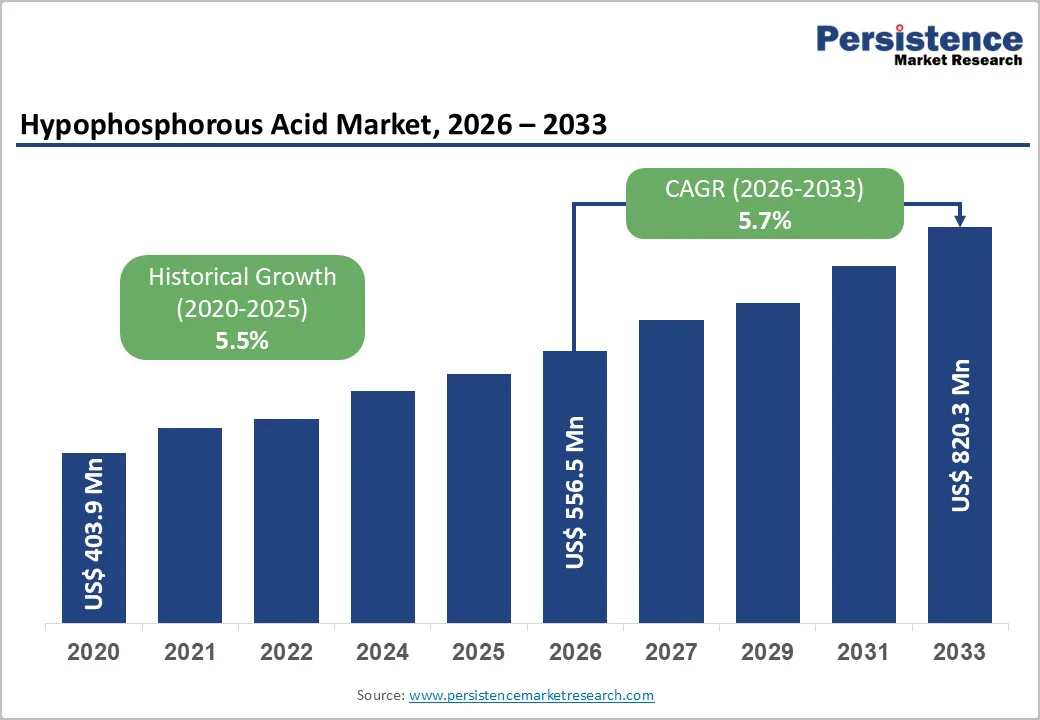

The global hypophosphorous acid market size is likely to be valued at US$556.5 million in 2026, and is expected to reach US$820.3 million by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of electroplating applications, rising demand for reducing agents in textile and agrochemical industries, and advancements in high-purity battery-grade formulations.

Rising demand for stable, non-toxic hypophosphorous acid in chemical and pharmaceutical applications is driving market growth, supported by advances in efficient, eco-friendly grades and expanding use in metal finishing and chemical synthesis across emerging industrial hubs.

Key Industry Highlights:

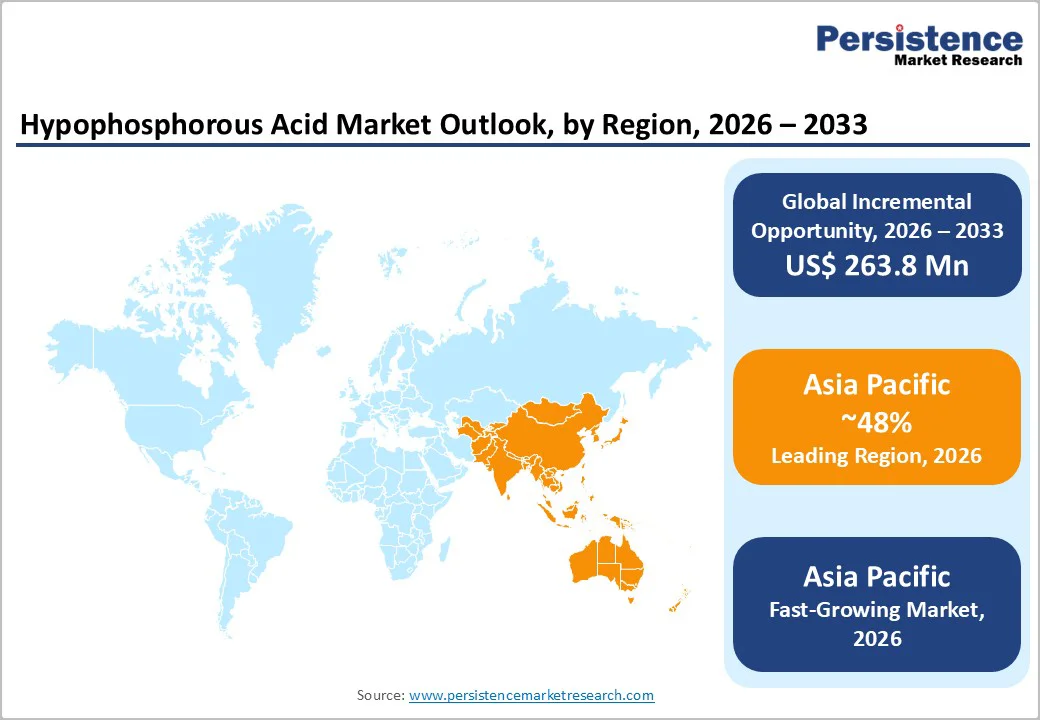

- Leading Region: Asia Pacific, anticipated to account for a 48% market share in 2026, driven by rapid industrialization, high electroplating activity, and strong chemical production in China and India.

- Fastest-growing Region: Asia Pacific, driven by expanding textile and agrochemical sectors, rising battery manufacturing, and growing investments in high-purity applications.

- Dominant Grade: Industrial grade, to hold approximately 60% of the revenue share in 2026, as it provides cost-effective performance for electroplating and reducing agents.

- Leading Application: Electroplating to account for over 35% of the market revenue in 2026, due to its critical role in metal finishing and corrosion resistance.

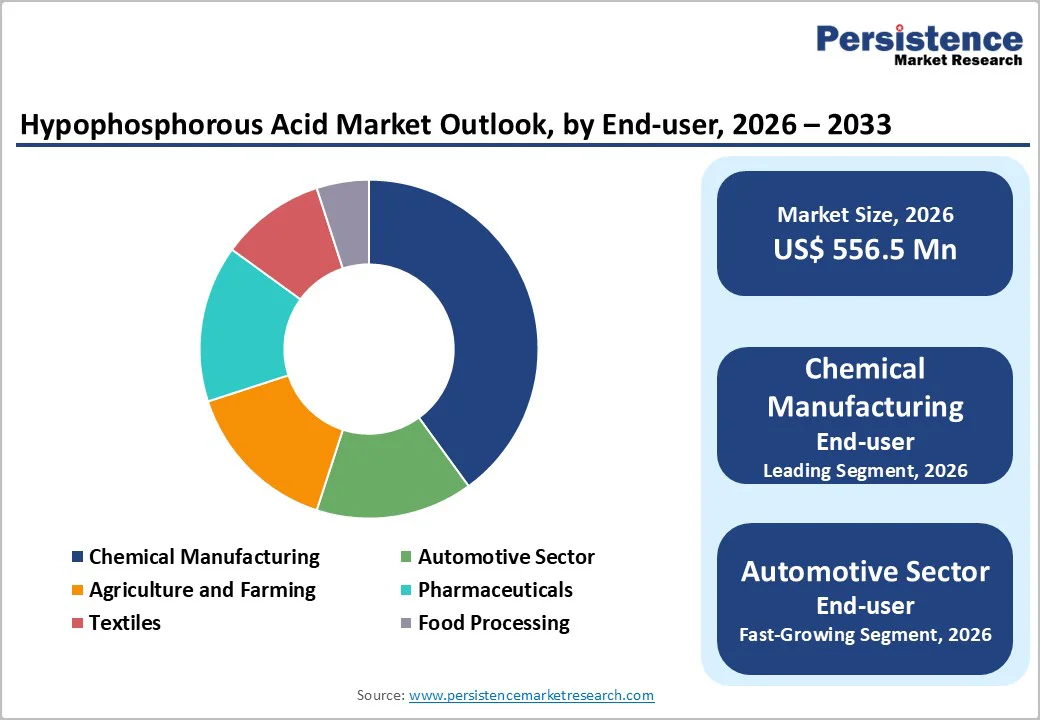

- Leading End-user Industry: Chemical manufacturing, to contribute nearly 40% of the market revenue in 2026, due to widespread use as a reducing agent and catalyst.

| Key Insights | Details |

|---|---|

|

Hypophosphorous Acid Market Size (2026E) |

US$556.5 Mn |

|

Market Value Forecast (2033F) |

US$820.3 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for High-Purity & Specialty Grades

The demand for high-purity and specialty grades of hypophosphorous acid is rising steadily as end-use industries place greater emphasis on product quality, performance consistency, and regulatory compliance. In pharmaceutical manufacturing, hypophosphorous acid is widely used as a reducing agent and reaction stabilizer in active pharmaceutical ingredient (API) synthesis. Even trace impurities can negatively affect reaction yields, drug stability, or safety profiles, making high-purity grades essential for meeting stringent pharmacopeial and quality standards.

In electronics and electroless nickel plating applications, specialty grades with controlled impurity levels are critical to achieving uniform coatings, enhanced corrosion resistance, and reliable conductivity. As electronic components become smaller and more complex, tolerance for contamination decreases, directly increasing demand for refined and application-specific chemical inputs. Specialty chemical manufacturers are increasingly customizing hypophosphorous acid grades to suit niche applications, such as advanced polymers, specialty resins, and high-performance coatings.

Supply Chain and Production Challenges

Supply chain and production challenges represent a significant restraint for the hypophosphorous acid market due to the complexity of sourcing, manufacturing, and distribution. The production process depends heavily on phosphorus-based raw materials that are geographically concentrated and subject to mining regulations, export controls, and periodic supply disruptions. Any imbalance in raw material availability can quickly affect production continuity, pricing stability, and delivery timelines.

Manufacturing hypophosphorous acid also requires tightly controlled reaction conditions, specialized equipment, and strict safety protocols owing to the material’s reactive and reducing properties. These technical requirements increase capital investments and limit the number of facilities capable of producing consistent, high-quality output at scale. Smaller producers often face difficulties maintaining steady production volumes while meeting quality and safety standards. Logistics adds another layer of complexity. Hypophosphorous acid must be handled and transported carefully to prevent degradation, contamination, or safety incidents. Regulatory differences across regions further complicate cross-border movement, increasing lead times and administrative burdens.

Rising Focus on High-Purity and Specialty Chemical Grades

The growing focus on high-purity and specialty chemical grades is creating a strong opportunity for the hypophosphorous acid market as industries demand greater precision, reliability, and performance from chemical inputs. Modern manufacturing processes, particularly in pharmaceuticals, electronics, and advanced materials, operate under strict quality and regulatory frameworks where even minor impurities can disrupt reactions, reduce efficiency, or compromise end-product safety. This has increased reliance on chemicals with tightly controlled compositions and consistent performance.

In pharmaceutical synthesis, high-purity hypophosphorous acid is essential to ensure predictable reaction outcomes and compliance with global quality standards. Similarly, electronics and surface treatment applications require specialty grades that deliver stable reducing behavior and uniform results, supporting higher yields and improved product durability. As technologies advance and component tolerances become tighter, demand for customized chemical specifications continues to rise. Specialty grades also enable manufacturers to tailor hypophosphorous acid for specific industrial processes, such as advanced polymers, specialty resins, and performance coatings. These applications benefit from chemicals designed to meet exact functional requirements rather than general industrial use.

Category-wise Analysis

Grade Insights

The industrial grade segment is anticipated to dominate the market, accounting for approximately 60% of the market share in 2026. Its dominance is driven by cost-effectiveness, large-scale availability, and versatility, making it preferred for electroplating and reducing agents. Industrial grade provides reliable performance, ensures stability, and contributes to affordability, making it suitable for large-scale chemical campaigns.

Tangshan Moneide Trading Co., Ltd., a China-based chemical supplier, offers industrial-grade hypophosphorous acid that is extensively used in electroless nickel and nickel electroplating applications. In these surface finishing processes, hypophosphorous acid serves as the reducing agent, allowing nickel ions in solution to deposit evenly onto metal surfaces without the use of an external electrical current.

Battery grade represents the fastest-growing segment, due to its ultra-purity and expanding use in lithium-ion electrolytes. Its low-impurity profile makes it ideal for targeted energy storage, reducing degradation. Continuous innovations in purification are further strengthening their performance, driving rapid adoption across North America and Europe, where demand for high-efficiency battery materials is accelerating.

Innophos, a specialty phosphates manufacturer, supplies battery-grade phosphoric acid and high-purity phosphate materials tailored for lithium-ion battery production, including LiFePO4 and LiMnFePO4 cathodes and electrolyte components. These materials are engineered with tightly controlled impurity levels to ensure critical performance attributes such as thermal stability, ionic conductivity, and long cycle life required for high-efficiency energy storage systems used in electric vehicles and grid-scale applications.

Application Insights

Electroplating is expected to lead the market, holding approximately 35% of the revenue share in 2026, driven by persistent corrosion protection needs, large manufacturing programs, and strong global demand for metal finishing. Their dominance continues as industries expand electronics and automotive plating. The rising adoption of catalysts in chemical synthesis and expanded textile campaigns highlights the growing focus on multi-sector use.

Armoloy Corporation, a global surface engineering provider, uses electroless nickel-phosphorus plating to deliver corrosion- and wear-resistant coatings on critical industrial parts such as automotive components, aerospace hardware, and oil & gas equipment. In electroless nickel plating, a nickel salt solution is chemically reduced by a phosphorus-containing reducing agent, typically sodium hypophosphite derived from hypophosphorous acid, without requiring an electrical current.

Pharmaceuticals and agrochemicals are the fastest-growing segment, due to strong momentum in synthesis and expanding inclusion of hypophosphorous acid as a reducing agent. The growing shift toward efficient, green platforms, along with better yield, accelerates the adoption.

Advancements in pharma-grade purity and continued progress of agrochemical stabilizers entering regulatory trials drive market growth. As a reducing agent, hypophosphorous acid is used in the synthesis of pharmaceutical intermediates. It facilitates the reduction of arene diazonium salts to produce specific compounds, contributing to the development of effective medicinal products.

End-user Industry Insights

Chemical manufacturing is projected to dominate the market, with approximately 40% share in 2026, due to the high volume of synthesis and strong global emphasis on reducing agents. Regular reaction schedules, process requirements, and widespread access to industrial-grade solutions drive consistent demand. Rising focus on the automotive sector and agriculture further strengthens chemical leadership.

Tangshan Moneide Trading Co., Ltd. is a chemical supplier that highlights the widespread use of industrial-grade hypophosphorous acid in chemical manufacturing processes, particularly where reducing agents are critical. According to product information from Moneide, hypophosphorous acid is used as a reducing agent in the production of phosphorus-derived chemicals and intermediates that are essential across multiple chemical sectors.

The automotive sector is the fastest-growing field, driven by the rising need for corrosion-resistant coatings, vulnerability to harsh environments, and expanding adoption of plated components. Improved durability, tailored grades, and stronger adhesion for EV batteries support rapid uptake. The growing use of energy & utility, textiles, and others among high-tech sectors further accelerates market growth.

Armoloy Corporation, a global surface-engineering company, supplies electroless nickel-phosphorus coatings extensively used in the automotive industry for components such as fuel system parts, brake components, transmission parts, and EV battery housings. These coatings provide high corrosion resistance, uniform thickness, and strong adhesion, even on complex geometries exposed to moisture, heat, road salts, and chemical stress.

Regional Insights

North America Hypophosphorous Acid Market Trends

Market growth in North America is fueled by the region’s advanced chemical infrastructure, strong research and development capabilities, and high public awareness of industrial benefits. Processing systems in the U.S. and Canada provide extensive support for application programs, ensuring wide accessibility of hypophosphorous acid across electroplating, pharmaceuticals, and agrochemical populations. Increasing demand for battery-grade, convenient, and easy-to-use forms is further accelerating adoption, as these formats improve performance and reduce barriers associated with alternatives.

Innovation in hypophosphorous acid technology, including stable purification, improved reducing delivery, and targeted battery enhancement, is attracting significant investments from both public and private sectors. Government initiatives and manufacturing campaigns continue to promote use against corrosion, chemical inefficiency, and emerging EV threats, creating sustained market demand. The growing focus on pharmaceutical grades and specialty uses, particularly for automotive and other applications, is expanding the target applications for hypophosphorous acid.

Europe Hypophosphorous Acid Market Trends

Europe is supported by increasing awareness of reducing benefits, strong chemical systems, and government-led sustainability programs. Countries such as Germany, France, and the U.K. have well-established industrial frameworks that support routine synthesis and encourage adoption of innovative hypophosphorous acid delivery methods. These efficient formulations are particularly appealing for chemical populations, regulation-conscious operators, and automotive users, improving yield and coverage rates.

Technological advancements in hypophosphorous acid development, such as enhanced purity, application-targeted delivery, and improved eco-grades, are further boosting market potential. European authorities are increasingly supporting research and trials for chemicals against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-waste options is aligned with the region’s focus on preventive efficiency and reducing environmental impact. Public awareness campaigns and transition drives are expanding reach in both urban and rural areas, while suppliers are investing in purification and novel variants to increase efficacy.

Asia Pacific Hypophosphorous Acid Market Trends

Asia Pacific is projected to dominate and is the fastest-growing, accounting for 48% market share in 2026, fueled by rising industrial awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting chemical campaigns to address electroplating growth and emerging battery needs. Hypophosphorous acid is particularly attractive in these regions due to its cost-effective administration, ease of scaling, and suitability for large-scale manufacturing drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-use hypophosphorous acid, which can withstand challenging production conditions and minimize impurity dependence. These innovations are critical for reaching remote facilities and improving overall process coverage. Growing demand for electroplating, agrochemicals, and battery applications is contributing to market expansion. Public-private partnerships, increased chemical expenditure, and rising investments in synthesis research and manufacturing capacity are further accelerating growth. The convenience of hypophosphorous acid delivery, combined with improved reducing power and reduced risk of waste, positions hypophosphorous acid as a preferred choice.

Competitive Landscape

The global hypophosphorous acid market features competition between established chemical producers and emerging regional suppliers. In North America and Europe, BASF and Lubrizol lead through strong R&D, distribution networks, and industry ties, bolstered by innovative grades and reduction programs. In Asia Pacific, Hubei Lianxing Chemical advances with localized solutions, enhancing accessibility. High-purity delivery boosts efficacy, cuts impurity risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand capacities, and speed commercialization. Battery-grade formulations solve energy issues, aiding penetration in EV-focused areas.

Key Industry Developments

- In January 2025, Paradeep Phosphates launched a INR 3,600 crore (US$434 million) expansion to add 1 million tonnes of granulation capacity and strengthen phosphoric and sulfuric acid production, paving the way for growth into downstream derivatives like hypophosphorous acid and specialty chemical markets.

- In February 2023, Arkema completed the divestment of its phosphorus derivatives business, including products linked to hypophosphorous acid chemistry, by selling the Febex unit to Prayon, a global phosphorus chemicals producer. This divestment is part of Arkema’s broader strategy to concentrate investment and R&D on higher-growth specialty materials while allowing the hypophosphite and related hypophosphorous acid segments to be developed under Prayon’s dedicated phosphorus chemistry platform, which can pursue targeted innovation and market expansion more effectively.

Companies Covered in Hypophosphorous Acid Market

- Minakem

- Occidental Petroleum Corporation

- Ataman Kimya A.Ş.

- Arkema

- Ambica Chemicals

- Hubei Lianxing Chemical

- Qingyuan RGDC Chemicals

- Fuerxin

- Kangxiang, Kailida

- Fang Chemicals

- LobaChemie Pvt. Ltd.

Frequently Asked Questions

The global hypophosphorous acid market is projected to reach US$556.5 million in 2026.

The rising prevalence of electroplating applications and demand for reducing agents are key drivers.

The hypophosphorous acid market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Advancements in high-purity and battery-grade delivery platforms are the key opportunities.

Hubei Lianxing Chemical, Qingyuan RGDC Chemicals, Kangxiang, Fuerxin, and Kailida are the key players.