- Beverages

- Hydrating Drinks Market

Hydrating Drinks Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Hydrating Drinks Market by Product Type (Sports & Energy Drinks, Coconut Water, Natural Hydration Beverages), Application (Sports & Fitness, Daily wellness, Weight Management, Clinical Recovery), Distribution Channel (Supermarket, Online Retail), and Regional Analysis for 2026-2033

Hydrating Drinks Market Share and Trends Analysis

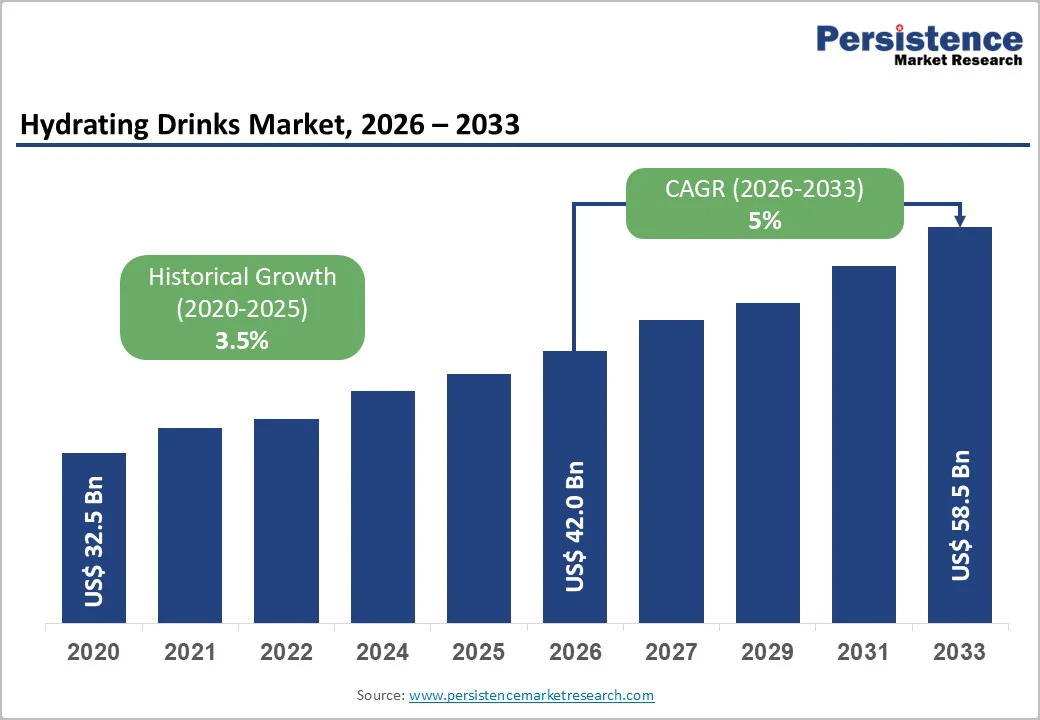

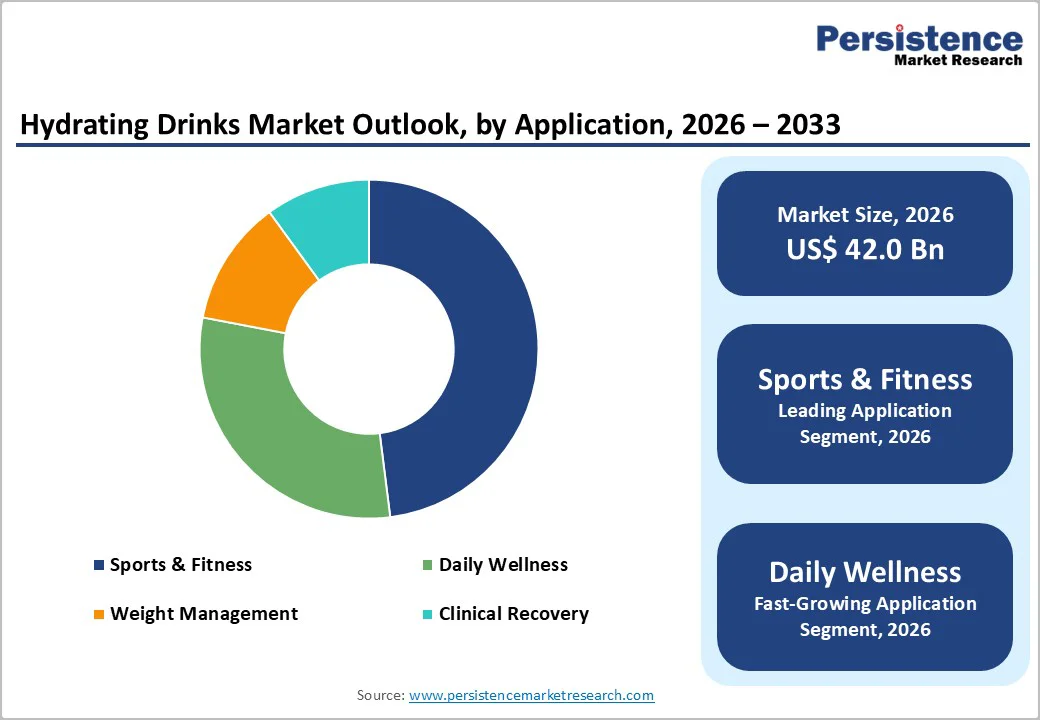

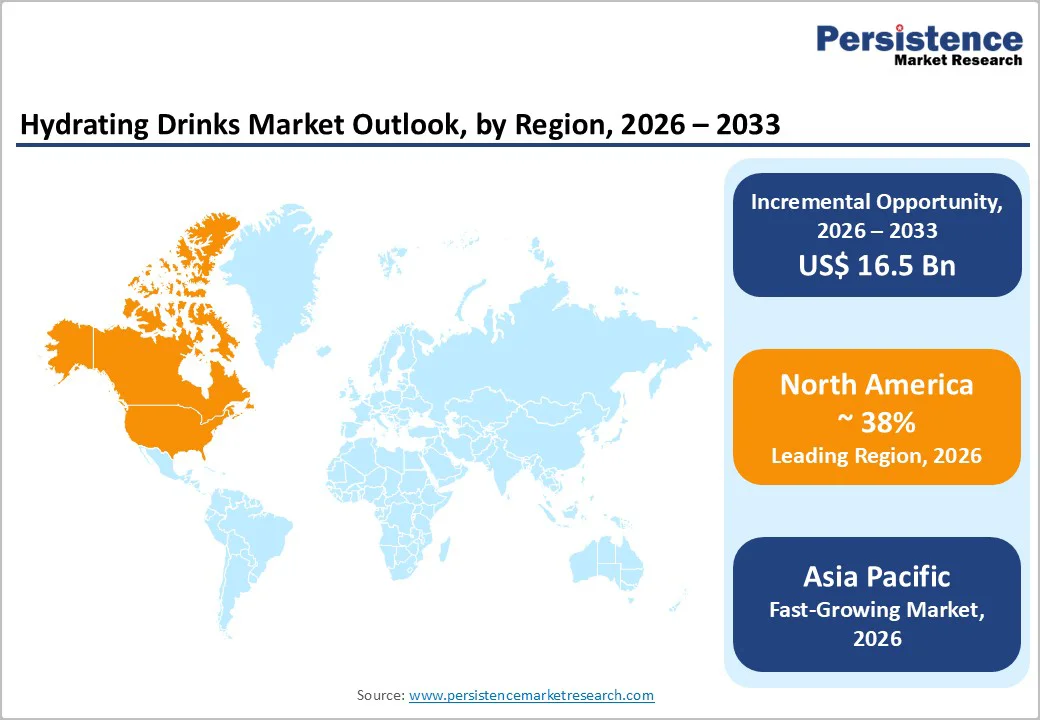

The global hydrating drinks market size is likely to be valued at US$ 42.0 billion in 2026, and is projected to reach US$ 58.5 billion by 2033, growing at a CAGR of 5.0% during the forecast period 2026−2033. The market's robust expansion is driven by escalating consumer health consciousness, increasing participation in fitness activities, and growing awareness of proper hydration's role in overall wellness. Rising disposable incomes in emerging economies, coupled with the proliferation of organized retail channels and e-commerce platforms, have significantly enhanced product accessibility. The shift from carbonated soft drinks toward functional beverages with enhanced nutritional profiles continues to reshape consumer preferences across demographic segments.

Key Industry Highlights

- Dominant Region: North America is expected to command about 38% market share in 2026, fueled by a deeply ingrained sports nutrition culture and a dense fitness infrastructure.

- Fastest-growing Regional Market: The Asia Pacific market is likely to be the fastest-growing through 2033, owing to rapid urbanization and increasing health awareness.

- Leading Application: Sports & fitness is slated to dominate with an estimated 48% revenue share in 2026, supported by continuous innovation in performance-specific formulations.

- Fastest-growing Application: Daily wellness is expected to be the fastest-growing segment during the 2026-2033 forecast period, as hydrating drinks shift from occasional use to everyday beverage choices.

- October 2025: Coca-Cola launched Powerade Power Water, a zero-sugar electrolyte-enhanced functional water with 50% more electrolytes than competitors, in four flavors for everyday hydration.

| Key Insights | Details |

|---|---|

| Hydrating Drinks Market Size (2026E) | US$ 42.0 Bn |

| Market Value Forecast (2033F) | US$ 58.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Health and Wellness Consciousness

The global wellness economy is expanding rapidly as consumers increasingly prioritize preventive health measures and functional nutrition in their daily lives. In this context, the hydrating drinks market benefits directly from a clear shift toward beverages that offer more than basic fluid replacement. Consumers now actively seek products that provide added value through electrolyte replenishment, vitamin enrichment, and the use of natural or clean-label ingredients. This trend aligns with broader lifestyle changes, as individuals look for convenient formats that support sustained energy, effective recovery, and overall well-being.

Public health initiatives aimed at reducing sugar consumption have increased demand for low-calorie and sugar-free hydrating options that balance taste with nutritional value. Growing engagement in sports, fitness, and recreational activities has further reinforced the role of hydrating drinks as essential companions to active lifestyles. Consequently, the market has expanded beyond traditional sports enthusiasts to include a broader base of mainstream consumers who regard hydration as a fundamental aspect of everyday wellness. This shift positions hydrating beverages as integral components of holistic health routines, spanning casual users, office workers, older adults, and wellness-focused younger demographics.

Intensifying Competition from Alternative Beverage Categories

The global beverage industry offers consumers a wide array of alternatives, including enhanced water, ready-to-drink (RTD) tea, functional coffee, and plant-based beverages, which are competing for attention and household space. In this environment, hydrating drinks must work harder to stay relevant as shoppers confront an expanding range of options that promise benefits such as energy, relaxation, immune support, or indulgence. Competition extends beyond individual brands, as entire beverage categories are positioned against each other for specific occasions such as post-workout recovery, daily refreshment, or on-the-go consumption, making it more challenging for hydrating drinks to secure consistent demand.

Market competition has intensified further as retailer-owned brands increasingly challenge established manufacturers, particularly in the sports and functional drink segments. Rapidly shifting consumer preferences shaped by social media trends and influencer recommendations have made demand patterns less predictable and have shortened product lifecycles. Retailers are responding by continually reviewing their assortments and favoring categories that deliver higher margins or stronger basket-building potential. As a result, hydrating drinks face mounting pressure to justify their shelf presence and must differentiate through clear positioning, product innovation, and distinctive branding to retain visibility within limited retail space and evolving consumer repertoires.

Functional Benefits Expansion and Personalization

Advancements in nutritional science and bioavailability are enabling hydrating drinks to deliver a broader range of functional benefits, including immune support, cognitive performance, digestive health, and beauty-from-within applications. Evidence from sports nutrition organizations highlights growing validation for specialized hydration formulations designed to support endurance, recovery, and muscle function across different activity levels. Functional ingredient innovation such as adaptogens, nootropics, and probiotics is extending the role of hydrating beverages beyond traditional electrolyte replacement, allowing brands to address more specific wellness needs and usage occasions.

Personalized nutrition trends, supported by growing consumer interest in genetic testing and wearable device integration, and are creating new opportunities for customized hydration solutions tailored to individual metabolic profiles and activity patterns. In parallel, the rapid expansion of digital health ecosystems is enabling connected beverage platforms that offer real-time hydration tracking, behavioral nudges, and automated product replenishment through subscription or smart-dispensing models. Together, these developments are reshaping the value proposition of hydrating drinks, positioning them as dynamic, data-informed wellness tools rather than static, one-size-fits-all products.

Category-wise Analysis

Product Insights

Sports & energy drinks are poised to be the leading segment with an approximate 42% of the market revenue share in 2026. The growth of this segment is boosted by strong brand equity, deep consumer recognition, and long-standing associations with athletic performance. Major global players reinforce this position through sustained marketing investment, securing prominent shelf space, eye-level placement, and high-visibility sponsorships across professional sports and major events. Over time, the segment has also benefited from scientific support for electrolyte replacement and performance enhancement, which strengthens consumer trust. These factors have created a powerful demand cycle, where familiarity, perceived efficacy, and ubiquitous availability keep sports and energy drinks at the center of performance-oriented hydration choices.

Coconut water and natural hydration beverages are likely to be the fastest-growing segment during the 2026-2033 forecast period, driven by consumers shifting toward clean?label options with minimal processing and easily recognizable ingredients. Major beverage companies are increasingly acquiring or partnering with specialized coconut water and natural beverage brands to gain rapid access to this high?growth space and to strengthen their credentials in better?for?you hydration. The natural positioning of these products, combined with the absence of artificial additives and their inherent electrolyte content, strongly appeals to health?conscious millennials and Generation Z consumers, who tend to favor naturally sourced functional beverages over more synthetic?seeming formulations.?

Application Insights

Sports & fitness is slated to dominate with an estimated 48% of the hydrating drinks market revenue share in 2026, supported by continuous innovation in performance-specific formulations that target pre-workout energy needs, intra-workout hydration, and post-workout recovery. These products are now deeply embedded in gym and training routines. Regular exercisers increasingly view specialized hydration as a core component of their regimen rather than an optional add-on. Professional athlete endorsements and partnerships with sports teams further enhance credibility, while recreational athletes are adopting the same products and protocols once associated primarily with elite performers, reinforcing category leadership across performance-oriented segments.

Daily wellness is expected to be the fastest-growing segment between 2026 and 2033. Hydrating drinks have gradually shifted from being consumed occasionally to becoming everyday beverage choices that compete directly with water, juice, and carbonated soft drinks. This reflects a broader integration of hydration products into daily routines, where consumers increasingly seek beverages that align with their health and lifestyle goals.? Product innovations that emphasize immune support, stress management, and sustained energy without stimulants now address needs that go well beyond athletic performance. Brands are targeting office workers, students, and general wellness-focused consumers who want functional benefits throughout the day, rather than only around workouts or sports activities. This evolution is significantly broadening the total addressable market for hydrating drinks.

Distribution Channel Insights

Supermarket is anticipated to lead with an approximate 55% revenue share in 2026. Supermarkets and hypermarkets leverage wide geographic coverage, strong footfall, and established consumer shopping habits within grocery environments. These formats combine competitive pricing, driven by volume purchasing and scale, with prominent in-store visibility through chilled displays and secondary placements that encourage impulse purchases. Large retail chains also use their negotiating power to secure favorable terms from manufacturers, while simultaneously developing private-label hydrating drink ranges that enhance margins and strengthen their overall influence within the category.

Online channel is positioned to be the fastest-growing segment during the 2026-2033 forecast period. Online and direct-to-consumer (D2C) channels are showing the strongest growth trajectory, reshaping hydrating drinks distribution through subscription models, personalized recommendations, and direct relationships between manufacturers and consumers that bypass traditional retail intermediaries. These channels benefit from rising comfort with digital purchasing, especially among younger cohorts, and from seamless integration with mobile apps and digital payment ecosystems, which makes repeat buying and trial of new products considerably easier. E-commerce adoption in beverage categories is expanding rapidly in both developed and emerging markets, with digital platforms becoming a core route to market rather than a secondary option.

Regional Insights

North America Hydrating Drinks Market Trends

North America is set to command a significant portion of the hydrating drinks market share at approximately 38% in 2026. The North America market is underpinned by a deeply ingrained sports nutrition culture, a dense fitness infrastructure, and highly developed retail and foodservice channels. The United States leads regional consumption, with hydrating beverages firmly embedded in everyday routines and athletic practices, supported by broad product availability across supermarkets, convenience stores, gyms, and vending locations. The market also benefits from a supportive regulatory environment, where strict quality and labeling standards coexist with the ability to communicate substantiated functional and performance claims, favoring manufacturers with strong R&D and scientific capabilities. A vibrant innovation ecosystem, concentrated in key states, continually introduces new formulations, formats, and sub-brands, although category maturity and intense competition put pressure on differentiation and margin expansion.

Consumer preferences in North America are increasingly shifting toward natural, organic, and plant-based hydrating options, with clean-label positioning becoming a critical purchase driver. Shoppers actively seek beverages free from artificial colors, flavors, and preservatives, which is pushing brands to simplify ingredient lists and adopt more transparent sourcing narratives. Digital channels have also become central to market development, as e-commerce and subscription services play a growing role in both routine replenishment and the discovery of new hydration concepts. At the same time, investment activity remains strong, with substantial capital flowing into startups focused on functional hydration, personalization technologies, and sustainable packaging, reinforcing North America’s position as a leading test bed for next-generation hydrating drink propositions.

Europe Hydrating Drinks Market Trends

Europe is a major market for hydrating drinks, shaped by diverse consumption patterns across countries and by a regulatory environment that is stringent yet supportive. The region’s demand profile reflects differences in sports participation, lifestyle, and beverage culture in markets such as Germany, the United Kingdom, France, and Spain, which requires tailored country?level strategies rather than a one?size?fits?all approach. A rigorous framework overseen by the European Union (EU) demands robust substantiation for nutritional and functional claims, as well as thorough ingredient safety assessments, which raises barriers to entry but enhances trust in approved products. At the same time, EU?level regulatory harmonization facilitates cross?border trade and portfolio scaling, even as strong national preferences for local brands, flavors, and packaging formats continue to encourage localized innovation and positioning.

The sports nutrition and fitness ecosystem continues to experience regional expansion, with hydrating drinks increasingly integrated into mainstream wellness routines rather than remaining confined to niche athletic users. Retail competition has intensified, particularly through the rapid growth of private-label ranges from major grocery chains, forcing branded players to differentiate through superior functionality, stronger sustainability credentials, and more compelling brand storytelling. While Western markets are relatively mature, Southern and Eastern European countries still offer meaningful headroom for volume and value growth as fitness participation rises and as modern retail and e-commerce channels deepen their penetration.

Asia Pacific Hydrating Drinks Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing hydrating drinks market from 2026 to 2033. The prospects of the market here are brightened by the skyrocketing rate of urbanization in India and China, higher disposable incomes, and increasing health awareness across a wide range of consumer segments. China anchors regional demand, driven by government initiatives that promote sports participation and by a large, expanding middle class, while Japan functions as a mature market with a strong emphasis on innovation, premium quality, and sophisticated functional positioning. India, by contrast, is at an earlier stage of category development but shows strong momentum as fitness culture spreads and modern retail and organized sports infrastructure extend their reach. Manufacturing cost advantages, proximity to key raw materials, and well-developed beverage production capabilities also position Asia Pacific as a critical global supply base for hydrating products.

Within the region, ASEAN markets add further dynamism, with economic integration supporting cross?border trade and creating a sizeable, increasingly connected consumer base for both international and local hydrating drink brands. Leading coconut water producing countries benefit from natural resource advantages, reinforcing Asia Pacific’s role in the natural hydration value chain. Regulatory regimes vary widely, ranging from highly stringent systems in markets such as Japan and Singapore to more flexible, evolving frameworks in emerging economies that aim to balance consumer protection with rapid category growth.

Competitive Landscape

The global hydrating drinks market structure exhibits moderate concentration, with major corporations such as PepsiCo, The Coca-Cola Company, Monster Beverage Corporation, and Red Bull GmbH commanding approximately 55% to 60% of the revenues. These industry leaders maintain their positions through continuous innovation, aggressive marketing campaigns, and substantial investment in research & development (R&D), packaging design, and distribution infrastructure. Their extensive retail networks, powerful brand recognition, and significant financial resources enable them to preserve leadership while rapidly adapting to shifting consumer preferences.

Emerging challengers, particularly in functional and organic beverage segments, intensify rivalry and catalyze a new wave of product innovation. These entrants target specific consumer micro-segments with sharply differentiated offerings, forcing established players to refine their portfolios. This dynamic creates opportunities for collaboration, acquisition, or organic development of niche brands. Stakeholders must monitor these trends closely and consider strategic partnerships or investments in specialized categories to maintain growth trajectories and defend their positions.

Key Industry Developments

- In June 2025, I.T.S introduced a range of natural, plant-based, clean label flavors designed specifically for hydration drinks, including electrolyte RTDs, powders and tablets, to mask off-notes from electrolytes and functional ingredients while maintaining strong taste and functionality.

- In February 2025, Shed launched Clear Protein Hydration, a sugar-free, clear whey beverage in three flavors – Blue Razz, Peach Mango, and Coconut Lime – that combines hydration benefits with 15 grams of protein per serving, targeting consumers who dislike or struggle to digest thick protein shakes.

- In February 2025, Reliance Consumer Products Ltd entered India’s sports hydration segment with Spinner, a low-priced sports drink co-created with Sri Lankan cricket legend Muttiah Muralitharan and positioned at INR 10 for a 150 ml bottle, significantly undercutting rivals such as Gatorade and Powerade.

Companies Covered in Hydrating Drinks Market

- PepsiCo, Inc.

- The Coca-Cola Company

- Monster Beverage Corporation

- Red Bull GmbH

- Nestlé S.A.

- Vita Coco Company

- Danone S.A.

- Keurig Dr Pepper Inc.

- Abbott Laboratories

- Bai Brands LLC

- Harmless Harvest

- Electrolit

- Arizona Beverages

- Lucozade Ribena Suntory

- Otsuka Pharmaceutical Co., Ltd.

Frequently Asked Questions

The global hydrating drinks market is projected to reach US$ 42.0 billion in 2026.

Rising health consciousness, growing sports and fitness participation, and increasing demand for low-sugar, functional beverages are driving the market.

The market is poised to witness a CAGR of 5% from 2026 to 2033.

Key opportunities lie in natural and clean-label formulations, personalized and functional hydration solutions, and expansion in high-growth emerging markets and digital sales channels

PepsiCo, The Coca-Cola Company, Monster Beverage Corporation, and Red Bull GmbH are some of the key players in the market.