- Food Ingredients & Additives

- Horticultural Ingredients Market

Horticultural Ingredients Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Horticultural Ingredients Market by Ingredient Type (Fruits, Nuts, Herbs & Spices), Nature (Organic, Conventional), Application (Food & Beverages, Foodservice, Retail/Household, Others), and Regional Analysis from 2025 - 2032

Horticultural Ingredients Market Share and Trends Analysis

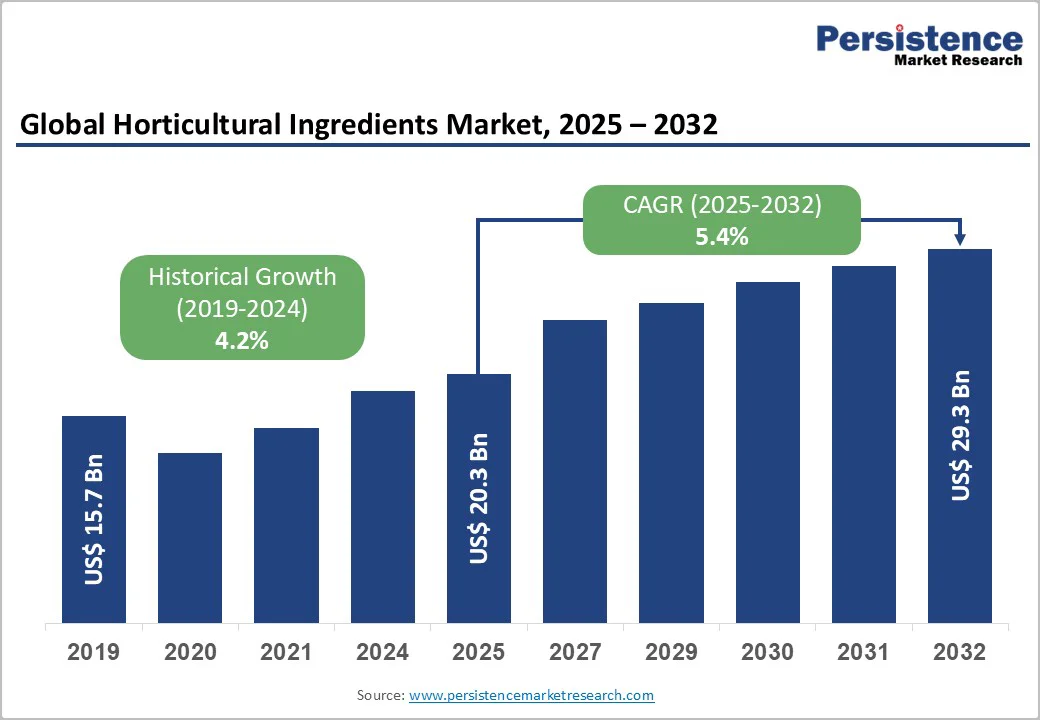

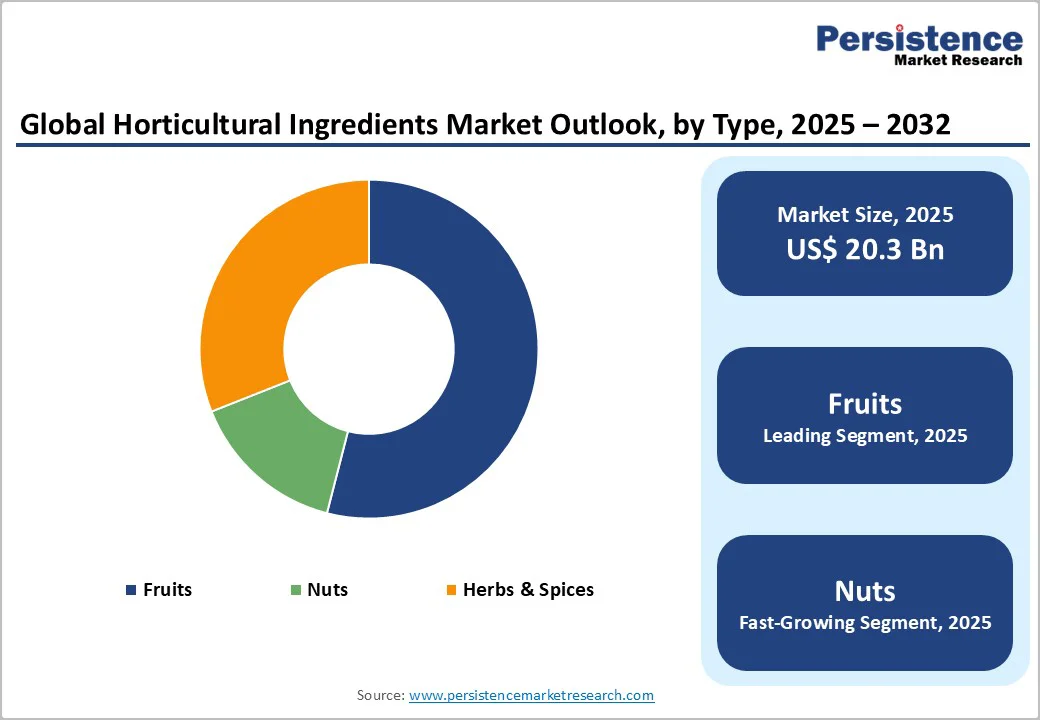

The global horticultural ingredients market size is valued at US$ 20.3 billion in 2025 and is projected to reach US$ 29.3 billion at a CAGR of 5.4% during the forecast period from 2025 to 2032. The global horticultural ingredients ecosystem is shifting rapidly as cleaner cultivation, efficient processing, and natural preservation technologies redefine how fruits, vegetables, herbs, and botanicals move from farm to formulation. The demand is surging across food, beverage, and wellness categories, fueled by sustainability expectations and premium quality benchmarks that are reshaping competitive strategies worldwide.

Key Industry Highlights:

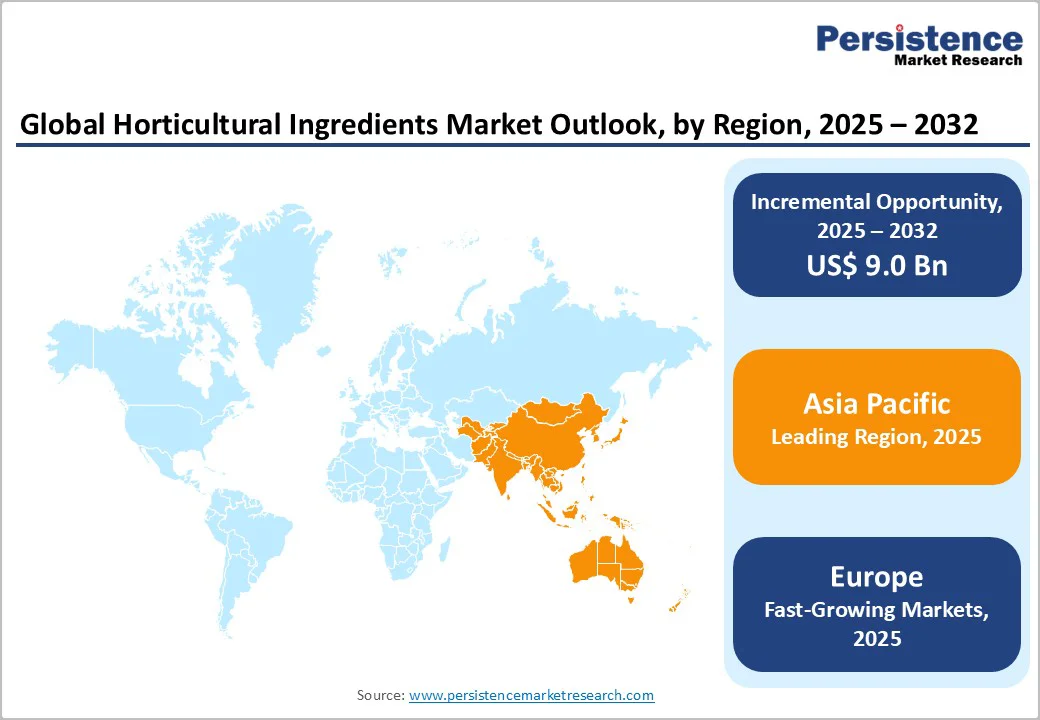

- Leading Region: Asia Pacific, holding around 37% market share, supported by strong demand for fruit, spice, and botanical ingredients across China, India, Japan, and Indonesia, along with rapid growth in foodservice and functional beverages.

- Fastest-Growing Region: Europe, driven by Germany, the UK, Spain, and Russia as manufacturers scale clean-label, plant-forward, and minimally processed horticultural ingredients for bakery, beverages, and gourmet formulations.

- Fastest-Growing Type Segment: Fruits, propelled by expanding use of concentrates, purees, powders, and natural sweeteners. Nuts, herbs, and spices add further momentum with rising adoption in snacks, functional foods, and premium culinary blends.

- Growth Indicator: Rising adoption of biological and organic inputs as growers shift toward microbial inoculants, botanical extracts, and residue-free systems. With 78% of consumers preferring organic and pesticide-free ingredients, producers are enhancing regenerative protocols and certification standards.

- Key Developments: In September 2025, SASI and MOVE-ComCashew signed an MoU with ofi to strengthen climate-resilient supply chains in cocoa, coffee, and cashew.

In May 2025, Givaudan unveiled new botanical wellness ingredients at Vitafoods Europe and earned an Innovation Award for its women’s health solution, Lifenol.

| Key Insights | Details |

|---|---|

|

Global Horticultural Ingredients Market Size (2025E) |

US$ 20.3 Bn |

|

Market Value Forecast (2032F) |

US$ 29.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.2% |

Market Dynamics

Driver - Rising Adoption of Biological and Organic Inputs

A striking shift toward cleaner agriculture is accelerating demand for biological and organic inputs across the global horticultural ingredients market. As per online studies, 78% of consumers prefer organic and pesticide-free food ingredients. Rising concerns over chemical residues, soil degradation, and long-term ecosystem health are pushing horticulture producers to integrate microbial inoculants, botanical extracts, bio-stimulants, and naturally derived pest-management solutions into mainstream production. This transition is reinforced by premium pricing opportunities for organic fruits, vegetables, herbs, and specialty crops. Food and beverage manufacturers are increasingly sourcing ingredients backed by regenerative practices, traceability systems, and residue-free certifications. The shift is reshaping supply chains, encouraging innovation in sustainable cultivation technologies, and redefining competitive differentiation across the horticultural ecosystem.

Restraints - Limited Cold-Chain and Post-Harvest Infrastructure

A critical bottleneck slowing the progress of the global horticultural ingredients market is the persistent gap in cold-chain and post-harvest infrastructure. Many high-value fruits, vegetables, herbs, and botanical raw materials require strict temperature control immediately after harvest to preserve nutrients, aroma profiles, and functional compounds. In regions where refrigerated transport, pack-houses, and controlled-atmosphere storage remain limited, spoilage rates rise sharply, shrinking usable yields and disrupting ingredient consistency for processors. Small and mid-scale farmers face the highest losses due to inadequate access to pre-cooling facilities and efficient aggregation networks. This instability pushes up procurement costs, reduces export competitiveness, and forces manufacturers to deal with variable quality, making reliable large-scale sourcing a challenge for the evolving horticultural ingredients landscape.

Opportunity - Developing Natural Post-Harvest Coatings as an Emerging Substitute for Synthetic Preservatives

A powerful opportunity is unfolding in the horticultural ingredients market as natural post-harvest coatings gain momentum as substitutes for synthetic preservatives. These plant-derived, edible coatings, often made from polysaccharides, lipids, and bioactive compounds, help slow respiration, reduce moisture loss, and extend freshness without relying on chemical additives. With retailers and exporters seeking longer shelf life and cleaner labeling, demand for such coatings is accelerating across fruits, vegetables, and minimally processed botanicals. Startups are experimenting with antimicrobial extracts, nano-emulsion delivery systems, and biodegradable film-forming agents to create coatings that enhance firmness, color stability, and nutrient retention. Established players see potential in partnering with growers and pack-houses to integrate these solutions into mainstream supply chains, aligning with the global push toward safer, sustainable post-harvest preservation.

Category-wise Analysis

By Ingredient Type

Fruits hold approximately 53.2% market share as of 2024, reflecting their unmatched versatility and relevance across processed foods, beverages, nutraceuticals, and premium culinary applications. Their widespread use in concentrates, purees, powders, and natural sweeteners keeps demand structurally high as brands focus on clean labels and functional nutrition. Tropical and berry-based ingredients are expanding fastest due to rising consumer preference for vibrant flavors and antioxidant-rich profiles. Nuts continue gaining traction for their protein density, healthy fats, and ability to enhance texture across bakery and snack formulations. Herbs & spices remain essential for natural flavor enhancement and are seeing renewed momentum as global cuisines influence mainstream product development. Collectively, these categories reinforce fruit’s leadership position in the horticultural ingredients landscape.

By Application Insights

Foodservice is projected to reach a CAGR of 6.5% during the forecast period, and the growth is shaped by rapid menu diversification and rising dependence on ready-to-use horticultural ingredients. Restaurants, cafés, QSR chains, and institutional kitchens are scaling operations faster than their supply teams can manually process fresh produce, pushing them toward standardized purees, concentrates, dried ingredients, and flavor extracts. Urban consumers expect consistent taste and premium presentation, compelling foodservice operators to adopt reliable ingredient formats that reduce prep time and waste. Seasonal volatility of fresh produce further encourages kitchens to rely on stable, shelf-ready horticultural inputs. With global expansion of delivery-first brands and cloud kitchens, demand intensifies for cost-efficient, flavor-rich ingredients that support speed, scalability, and operational precision.

Region-wise Insights

Asia Pacific Horticultural Ingredients Market Trends

Asia Pacific holds approximately 37% share in the global horticultural ingredients market, and its momentum is being shaped by fast-evolving regional consumption patterns and supply-side innovation. China is pushing deeper into natural flavor extracts and botanical concentrates as beverage brands lean toward clean, functional profiles. India is witnessing a surge in demand for spice-derived oleoresins and fruit-based ingredients driven by rapidly expanding foodservice and snacking ecosystems. Japan is accelerating the adoption of high-purity, minimally processed horticultural inputs to meet its premium standards for packaged foods and nutraceuticals. Indonesia is emerging as a processing hub for tropical fruit derivatives, fueled by a booming domestic convenience-food culture. Across the region, brands are recalibrating toward freshness, traceability, and ingredient efficiency to stay competitive.

Europe Horticultural Ingredients Market Trends

Europe horticultural ingredients market is likely to achieve a CAGR of 5.2%, driven by a decisive shift toward clean-label reformulation and advanced processing technologies across the region. Germany is witnessing a strong demand for fruit concentrates and botanical extracts as manufacturers upscale functional beverages and premium bakery applications. The UK market is rapidly leaning toward plant-forward innovation, pushing higher use of natural colors, purees, and herb-based blends in snacks and ready meals. Spain’s robust fruit-processing ecosystem is strengthening the adoption of citrus derivatives, Mediterranean herbs, and infused oils across foodservice and gourmet products. Russia is expanding its reliance on domestically sourced berries, vegetables, and specialty crops as local processors invest in freeze-drying and cold-chain upgrades. Collectively, these trends underline Europe’s momentum toward premium, authentic, and sustainability-driven horticultural ingredients.

Competitive Landscape

The market nature remains moderately fragmented, creating a competitive landscape where established processors and agile innovators push the sector forward with distinct strategies. Leading companies are expanding vertically to secure raw materials, investing in controlled-environment farming, and scaling advanced extraction and concentration technologies to guarantee consistent flavor, color, and phytonutrient profiles. Many are strengthening certification portfolios, organic, Fairtrade, and Non-GMO to win premium positioning with global buyers. Startups are carving out space by focusing on regenerative agriculture partnerships, hyper-local sourcing models, and clean, minimally processed ingredient lines tailored for plant-based, functional, and gourmet applications. Across the board, firms are adopting energy-efficient drying systems, enzymatic processing, and purity-enhancing filtration tools to improve yield, reduce waste, and meet tightening sustainability expectations.

Key Industry Developments:

- In September 2025, the Sustainable Agricultural Supply Chains Initiative (SASI) and the MOVE-ComCashew programme formalized a partnership with ofi (Olam Food Ingredients) via a Memorandum of Understanding (MoU). This new phase of cooperation is dedicated to creating sustainable, fair, and climate-resilient agricultural supply chains, focusing on cocoa, coffee, and cashew in multiple regions through 2027.

- In May 2025, Givaudan showcased its extensive portfolio of science-backed botanical ingredients at Vitafoods Europe for key consumer wellness areas. The company also debuted a new stress management ingredient and won an Innovation Award for its women's health solution, Lifenol.

- In January 2024, dsm-firmenich entered a strategic partnership with Indena S.p.A. to pioneer the next generation of science-backed botanical and natural solutions for human health. This collaboration focuses on combining their expertise in essential nutrients and active botanical ingredients to create market-ready dietary supplements for key areas like immunity, brain health, and healthy aging.

Companies Covered in Horticultural Ingredients Market

- ABC Fruits

- AgroAmerica

- Ariza B.V.

- Givaudan

- dsm-firmenich

- Ceres Organics

- Chanthaburi Global Foods Co., Ltd.

- Edward & Sons Trading Co.

- FutureCeuticals, Inc.

- Grünewald Fruchtsaft GmbH

- Kim Minh International

- Lemonconcentrate S.L.U.

- Olam International

- Sleaford Quality Foods Ltd.

- Synthite Industries Ltd.

- Others

Frequently Asked Questions

The global horticultural ingredients market is valued at US$ 20.3 Bn in 2025.

Rising adoption of biological and organic inputs is fueling the demand for Horticultural Ingredients in the global market.

The global horticultural ingredients market is poised to witness a CAGR of 5.4% between 2025 and 2032.

Developing natural post-harvest coatings as an emerging substitute for synthetic preservatives represents a major market opportunity.

Major players in the global Horticultural Ingredients market include Olam International, AgroAmerica, Synthite Industries Ltd., FutureCeuticals Inc., Givaudan, dsm-firmenich, Ariza B.V., Lemonconcentrate S.L.U., and others.