- Industrial Machinery

- High-Performance Butterfly Valve Market

High-Performance Butterfly Valve Market Size, Share, Trends, Growth, Forecasts 2025 - 2032

High-performance Market by Product (Double Offset Butterfly Valve, Triple Offset Butterfly Valve), Seat Type (Soft Seat, Metal Seat), Valve Size (Small, Medium, Large), Industry and Regional Analysis 2025 - 2032

High-performance Butterfly Valve Market Share and Trends Analysis

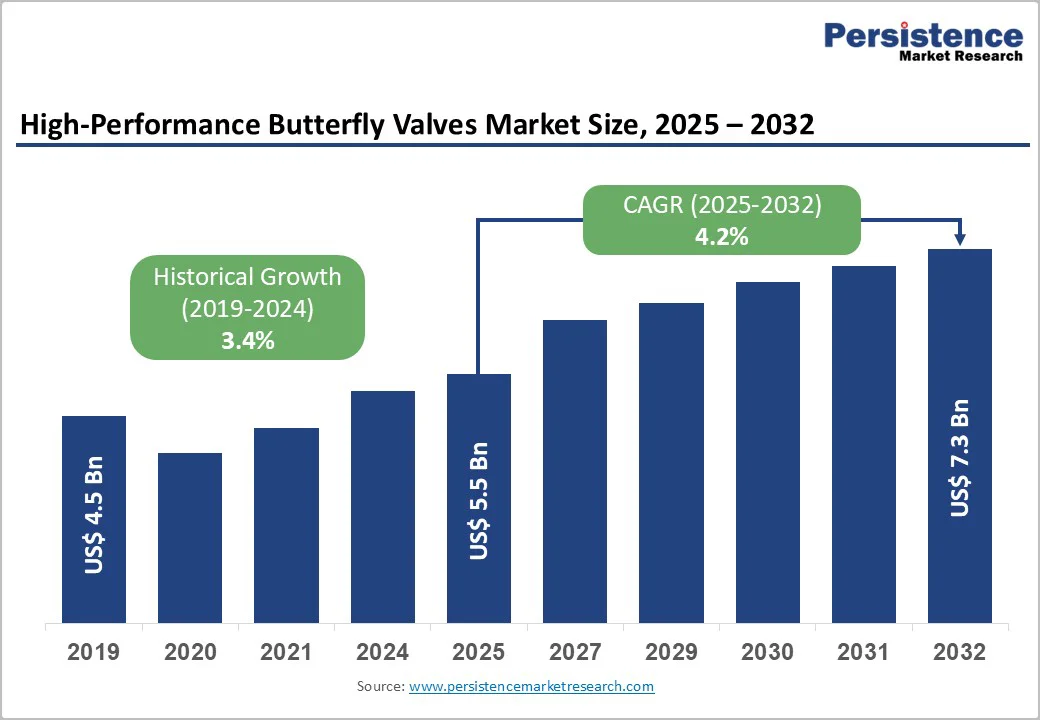

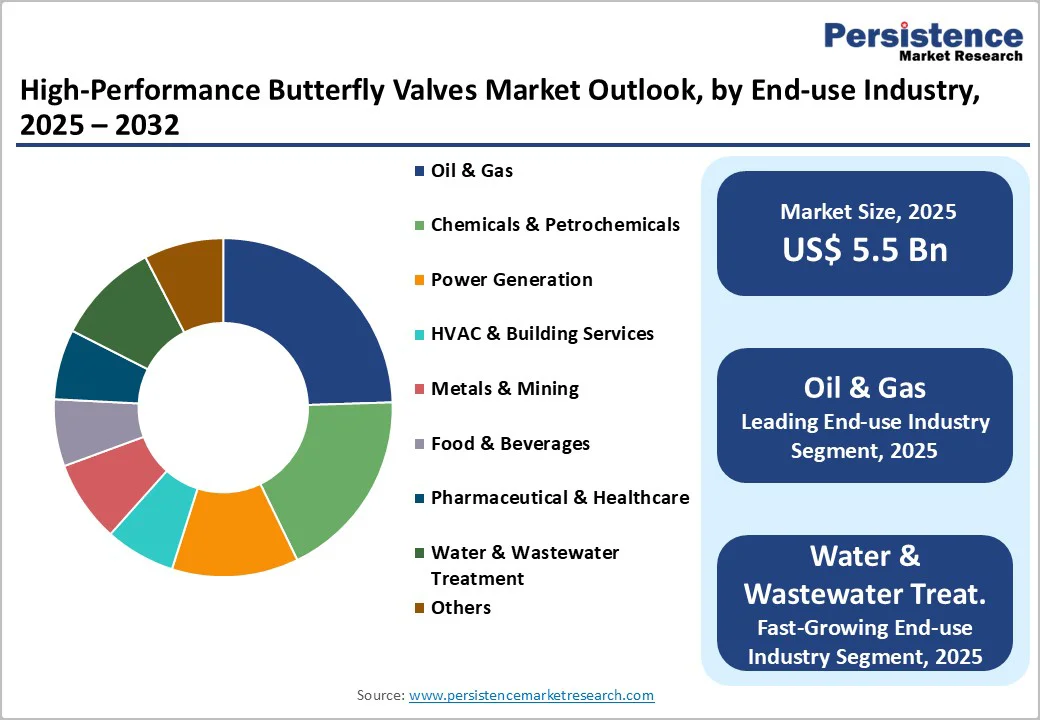

The global high-performance butterfly valve market size is valued at US$5.5 billion in 2025 and is expected to reach US$7.3 billion by 2032, growing at a CAGR of 4.2% between 2025 and 2032.

This growth is driven by increased infrastructure investments in water and wastewater treatment, the adoption of Industry 4.0 automation technologies, and the energy transition, demanding advanced flow control solutions. In 2024, US$19.6 billion was committed to water projects, mainly for low- and middle-income countries that need robust valve infrastructure.

High-performance butterfly valves, known for their metal-seated designs and triple offset geometry, are essential in demanding applications across oil & gas, power generation, chemical processing, and municipal water systems.

Key Industry Highlights:

- Product Configuration Leadership: Double offset butterfly valves hold ~67% market share for mainstream applications, while triple offset valves emerge as the fastest-growing segment at 4.8% CAGR driven by extreme service requirements and green hydrogen applications

- Seat Type Dynamics: Soft seat valves maintain 61% market share across diverse applications, with metal seat valves growing fastest at 5.1% CAGR, addressing high-temperature, high-pressure, and fire-safe service demands

- Size Segment Performance: Medium valves (10-25 inches) hold 43% market share, balancing flow capacity and cost-effectiveness, while small valves (up to 10 inches) grow fastest at 4.7% CAGR, driven by building automation and pharmaceutical applications

- Industry Patterns: Oil & gas leads with a 25% market share, the most demanding sector. In comparison, water & wastewater treatment is the fastest-growing industry, with a 5.5% CAGR, fueled by substantial development bank commitments in 2024.

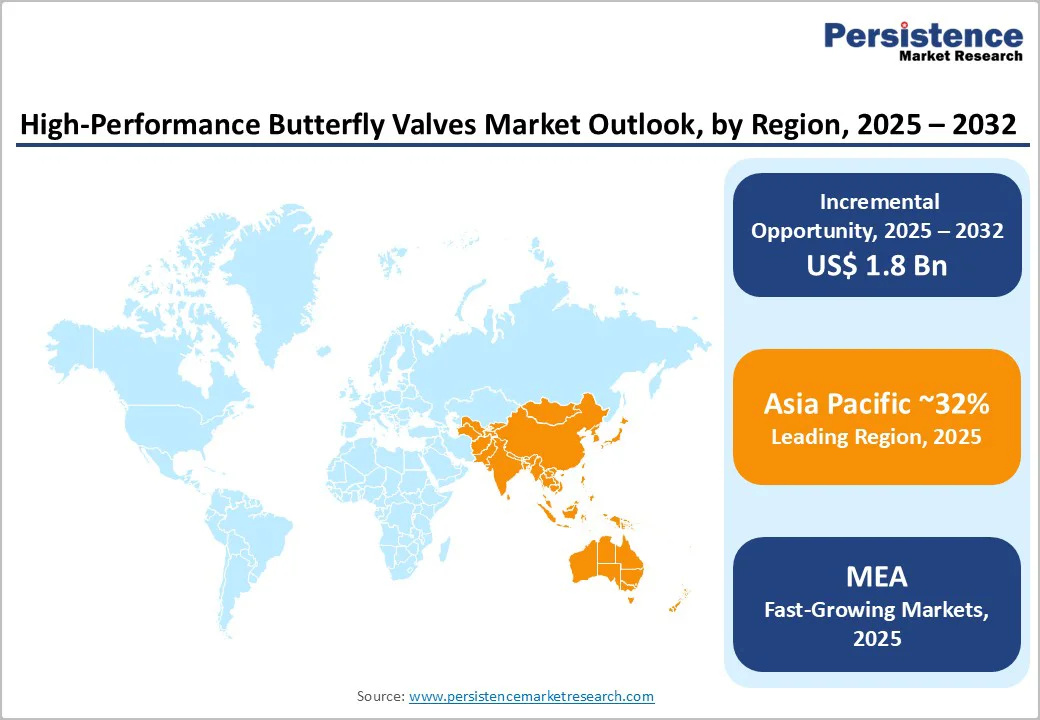

- Regional Market Distribution: Asia Pacific dominates with 32% global market share and 5.1% CAGR, led by China and India's infrastructure expansion; Europe holds 27% share at 3.4% CAGR; North America grows at 3.9% CAGR, supported by infrastructure modernization

- Strategic Industry Developments: Triple-offset valve innovations, smart valve IoT integration, and cross-border acquisitions, including ARI-Armaturen/Warren Controls, exemplify competitive strategies that address digital transformation, geographic expansion, and application specialization trends.

| Key Insights | Details |

|---|---|

| High-Performance Butterfly Valve Market Size (2025E) | US$ 5.5 billion |

| Market Value Forecast (2032F) | US$ 7.3 billion |

| Projected Growth CAGR (2025 - 2032) | 4.2% |

| Historical Market Growth (2019 - 2024) | 3.4% |

Market Dynamics Analysis

Drivers - Massive Global Investment in Water and Wastewater Infrastructure

Water infrastructure modernization represents the most significant driver propelling high-performance butterfly valve demand globally. The World Bank estimates an annual funding gap of US$138 billion between 2017 and 2030 to achieve universal access to safe drinking water and sanitation, which would require a near tripling of annual spending.

India's wastewater treatment sector is expanding, bolstered by the Jal Jeevan Mission with Rs 701.63 billion (around US$8.4 billion) for 2024-25, and Rs 80 billion (US$960 million) for AMRUT 2.0 for urban projects. As of July 2024, 889 sewerage and septage projects and 1,390 water supply projects were initiated, providing 14.9 million sewer connections.

Notable projects include Asia's largest sewage treatment plant in Delhi (564 MLD capacity) and the Nemmeli Water Desalination Plant in Tamil Nadu (150 MLD capacity). High-performance butterfly valves dominate these applications due to their cost-effectiveness, compact design, and ability to regulate high-volume flow with minimal pressure drop.

Butterfly valves accounted for ~37% of revenue in the global water and wastewater treatment segment in 2024, establishing municipal infrastructure as the dominant application driving sustained market growth.

Power Generation Industry Modernization and Steam Service Applications

Power generation facilities represent a critical end-use sector driving high-performance butterfly valve adoption, particularly for demanding steam service applications. The power generation industry accounts for about 20% of the global valve market, with butterfly valves increasingly replacing traditional gate and globe valves in thermal and nuclear plants.

High-performance triple-offset butterfly valves are designed for high-temperature and high-pressure steam applications, effectively handling conditions up to 400°F (204°C) and 1,000°F (538°C), depending on materials.

Power plants rely on them for flow regulation, maintenance isolation, and protecting sensitive equipment through pressure/temperature control, which is driving their adoption as global power demand increases and new plants are established, including those focused on renewable energy.

Asia Pacific regions particularly demonstrate rapid expansion in renewable energy projects including solar and wind power installations, where butterfly valves function in cooling systems and control processes. Germany's robotics and automation sector, while distinct, parallels power industry trends, with over 450 FDI projects between 2019 and 2024, indicating broader industrial modernization that supports advanced valve infrastructure investments.

Restraints - High Initial Capital Costs and Specification Complexity

High-performance butterfly valves, especially triple-offset models with metal-to-metal sealing, are more expensive than standard resilient-seated versions, creating challenges for budget-limited municipalities and small-to-medium industrial facilities. These valves require significant upfront investment and incur additional costs for specialized installation, integration with existing infrastructure, and compliance with standards such as API 6D and ASME B16.34.

The specification process is complex, involving factors like pressure ratings (Class 150-2500), temperature tolerances (cryogenic to 1,500°F), and material compatibility. Incorrect specifications can lead to failures and costly replacements, posing difficulties for small and medium enterprises that often resort to lower-cost alternatives despite their performance limitations.

Material Degradation and Lifecycle Maintenance Challenges

High-performance butterfly valves in severe service conditions face material degradation, impacting reliability and lifecycle costs. In oil and gas applications involving corrosive substances, valve components experience wear and chemical attack, compromising sealing integrity. While metal seats are better for high-temperature and high-pressure uses, they are prone to scoring and thermal damage.

Soft-seated butterfly valves occasionally face lining delamination under low pressure, especially with paste-extrusion linings. Power generation steam services contribute to seat wear and disc distortion due to thermal stress. Although advanced materials like Stellite alloys are used, they add costs and require maintenance.

Predictive maintenance in conventional setups is lacking, with operators often missing real-time monitoring to anticipate failures. In contrast, IoT-enabled smart valve systems offer predictive analytics, but their adoption is slow due to retrofit costs and integration challenges with existing control systems.

Opportunities - Digital Transformation and Smart Valve Technology Integration

Industry 4.0 digitalization presents substantial growth opportunities for high-performance butterfly valve manufacturers incorporating IoT connectivity, predictive analytics, and automated control capabilities. Smart valve platforms now incorporate sensor networks enabling real-time monitoring of flow rates, torque requirements, seal integrity, pressure differentials, and temperature profiles.

Smart valves leverage LoRaWAN and NB-IoT low-power wide-area network technologies to transmit data and receive commands over distances up to 30 km in outdoor environments, enabling comprehensive facility-wide valve monitoring from centralized control rooms.

Predictive maintenance capabilities analyze valve performance data, identifying patterns and anomalies, forecasting maintenance requirements before failures occur, reducing unplanned downtime and extending asset life.

Germany's Siemens and Endress+Hauser launched intelligent valve control platforms interfacing directly with SCADA and building management systems. At the same time, Norway's Equinor integrated digital butterfly valves into offshore oil and gas platforms, enhancing process efficiency and reducing unplanned downtime.

Specialty Applications in Pharmaceutical and Food Processing

Healthcare, pharmaceutical, and food & beverage sectors present high-value opportunities for specialized high-performance butterfly valves that meet stringent hygiene and regulatory requirements. The pharmaceutical industry notably increased automation for FDA-compliant packaging by about 60% in December 2020, driven by reshoring and supply chain vulnerabilities.

High-performance butterfly valves ensure contamination-free operation, precise flow control, and compatibility with sterilization-in-place (SIP) and cleaning-in-place (CIP) processes, all while satisfying Good Manufacturing Practices (GMP). In the food and beverage sector, the Italian National Institute for Insurance against Accidents at Work (INAIL) mandates the use of lined valves to prevent contamination and ensure hygiene.

Soft-seated butterfly valves, made from materials such as PTFE and EPDM, provide bubble-tight sealing and reduce wear. Stainless steel constructions and smooth finishes help prevent bacterial growth, facilitating easier cleaning.

Moreover, the Swedish Environmental Protection Agency reports an increase in the use of lined butterfly valves in effluent management, highlighting their versatility. As pharmaceutical companies ramp up biologics production and food processors enhance automation for traceability, the demand for these specialized valves will rise.

Category-wise Analysis

Product Type Insights

Double offset butterfly valves dominate the high-performance butterfly valve market with approximately 67% market share, representing the mainstream configuration for refinery, power plant, and general industrial isolation applications.

Double offset geometry features two geometric deviations: the shaft is positioned behind the centerline of the sealing surface, enabling disc rotation without scraping the seat, and shaft placement off-center from the valve body's centerline reduces contact between seat and seal during operation. This design minimizes wear, extends valve service life, and delivers reliable shut-off for applications involving moderate pressures and temperatures.

Computational fluid dynamics optimization now enhances disc profiles, reducing pressure drop by 10-15% versus legacy patterns. Major manufacturers, including Emerson, Flowserve, and AVK Holding, produce extensive double offset portfolios serving water treatment, HVAC, and chemical processing sectors where their balanced performance-to-cost ratio optimizes total cost of ownership.

Triple-offset butterfly valves are the fastest-growing segment, with a CAGR of 4.8%, driven by their superior zero-leakage performance and durability in extreme service conditions. Their conical sealing design ensures tight, reliable metal-to-metal seals and allows for bidirectional, bubble-tight shut-off at high temperatures (up to 1,000°F) and pressures.

The global triple offset butterfly valves market is expected to grow from US$1.8 billion in 2025 to US$2.5 billion by 2032. These valves are ideal for upstream oil and gas operations, petrochemical plants, power generation facilities, and emergency shutdown systems where leak prevention and reliability are crucial.

Seat Type Insights

Soft-seat butterfly valves maintain market leadership with an approximately 61% market share, reflecting their widespread deployment in low- to medium-pressure and temperature applications where tight sealing, cost-effectiveness, and vibration damping are prioritized.

Soft seats utilize elastomeric materials, including PTFE, Viton, EPDM, Nylon, and PEEK, providing bubble-tight shut-off superior to metal seats in many applications. The soft seal material offers specific advantages: it absorbs vibrations, reducing valve wear and tear, conforms to mating surfaces, compensating for minor imperfections, and operates quietly compared to metal-seated alternatives.

HVAC systems, power generation facilities, and food and beverage sectors deploy soft-seated valves for processes requiring reliable sealing at operating temperatures typically not exceeding 400°F (204°C). Applications include potable water systems where NSF/ANSI certification mandates lead-free materials, pharmaceutical manufacturing requiring contamination-free operation, and food processing adhering to hygiene standards.

Metal seat butterfly valves are the fastest-growing seat type, with a CAGR of 5.1%, due to their suitability for extreme conditions like high temperatures, pressures, and abrasive media. Made from stainless steel, Inconel, or exotic alloys with Stellite overlays, these valves can handle temperatures up to 1,500°F (815°C) and pressures up to ASME Class 1500 (PN 260).

They provide zero-leakage metal-to-metal sealing, essential for applications in power plants, gas pipelines, and emergency isolation per API-607 standards. Additionally, they are gaining traction in emerging sectors like green hydrogen production and carbon capture systems.

Valve Size Insights

Medium-sized butterfly valves (10-25 inches) hold the largest market share, at approximately 43%, offering the optimal balance among flow capacity, installation feasibility, and cost-effectiveness for mainstream industrial and municipal applications. This size range addresses the majority of pipeline installations across water treatment facilities, power generation plants, chemical processing units, and HVAC systems.

Medium valves accommodate substantial flow volumes while maintaining manageable weight, actuator torque requirements, and installation costs compared to large-diameter alternatives. Water and wastewater treatment applications, which dominated the global butterfly valve market with a 37.5% revenue share in 2024, primarily use medium-sized valves for trunk lines, treatment process streams, and distribution mains.

Power generation cooling water systems, steam condensate returns, and auxiliary service lines similarly concentrate in this size category. The segment benefits from mature manufacturing ecosystems, extensive actuator compatibility, and established installation practices reducing project risks and total ownership costs.

Small butterfly valves (up to 10 inches) are the fastest-growing valve segment, with a CAGR of 4.7%, driven by applications in building services, pharmaceuticals, food processing, and distributed utilities. Their compact design suits space-constrained installations, offering quick response times and lower installation costs.

The pharmaceutical and food sectors prefer these valves for precise flow control and frequent cycling. Advancements in miniaturization and electronic actuators enhance performance, making these valves essential as industries shift toward modular architectures and continuous processing methods.

Industry Insights

Oil & gas maintains market leadership with approximately 25% market share, representing the most demanding and mature end-use sector for high-performance butterfly valves. The industry's extensive upstream exploration and production operations, midstream pipeline transportation networks, and downstream refining and petrochemical complexes create diverse applications spanning isolation, throttling, emergency shutdown, and process control.

High-performance valves address critical services including sour gas handling with hydrogen sulfide exposure, high-pressure wellhead applications, crude oil transportation through long-distance pipelines, refinery process units handling elevated temperatures and corrosive streams, and petrochemical production involving aggressive chemicals.

Triple-offset butterfly valves have served over half a million installations globally across oil and gas facilities, a testament to their proven reliability in extreme service conditions. Infrastructure expansion, facilitating the development of new reserves, including offshore platforms, subsea pipelines, and LNG terminals, requires sophisticated valve solutions to support exploration and production in challenging environments.

Water and wastewater treatment is the fastest-growing Industry, with a CAGR of 5.5%. Global investments in aging infrastructure, population growth, environmental regulations, and water scarcity drive this growth. In India, the wastewater sector is anticipated to reach $4.3 billion by 2025, supported by significant government allocations for related missions.

As of July 2024, numerous sewerage and water supply projects are underway, providing millions of connections. High-performance butterfly valves are favored for their cost-effectiveness, compact designs, low pressure drops, and durability. Key growth drivers include strict discharge regulations, water reuse initiatives, and smart city developments leveraging IoT technologies.

Regional Market Insights

North America High-performance Butterfly Valve Market Trends

North America demonstrates robust growth with a CAGR of 3.9%, characterized by mature industrial infrastructure, stringent regulatory frameworks, and ongoing modernization investments across water treatment, oil and gas, and power generation sectors.

The United States leads regional demand, supported by aging water infrastructure requiring systematic replacement, shale gas production necessitating midstream pipeline expansion, and power plant efficiency upgrades. The region benefits from established API standards, including API 6D for pipeline valves and API 600 for steel gate valves, ensuring product quality and performance consistency.

North American regulations, particularly OSHA safety requirements and EPA environmental mandates, drive preference for API-certified high-performance valves meeting stringent testing criteria. The oil and gas sector, while experiencing commodity price volatility, maintains substantial valve demand across upstream unconventional drilling operations, midstream infrastructure connecting production to markets, and downstream refining capacity optimization.

The competitive landscape features major global valve manufacturers such as Emerson Electric Co., Flowserve Corporation, and Crane Co., as well as specialized regional suppliers. Recent M&A activity includes May River Capital's acquisition of Cashco, a pressure-management solutions provider, and Integrated Water Services' acquisition of Hi-Line Industries, which enhances water treatment capabilities.

The focus on safety, environmental compliance, and operational efficiency drives the adoption of smart valve technologies with IoT connectivity and predictive maintenance. Manufacturing reshoring, backed by federal incentives, creates opportunities for domestic valve manufacturers and strengthens supply chain resilience.

Europe High-performance Butterfly Valve Market Trends

Europe maintains a considerable market share of 27% globally while growing at a steady CAGR of 3.4%, supported by advanced industrial infrastructure, stringent environmental regulations, and comprehensive standards harmonization across European Union member states.

Germany dominates the regional market, holding 21.5% of European butterfly valve revenues in 2024, attributed to the country's robust industrial base encompassing chemicals, automotive, machinery manufacturing, and power generation. Germany's leadership in Industry 4.0 integration is driving the adoption of smart butterfly valves equipped with digital actuators and condition-monitoring features.

Germany's push for automation, exemplified by over 450 FDI robotics and automation projects between 2019 and 2024, parallels the valve industry digitalization trends. Europe's regulatory environment emphasizes environmental compliance, with the Swedish Environmental Protection Agency mandating lined butterfly valve usage in industrial effluent management and Italy's INAIL requiring specific valve standards in food processing facilities.

The United Kingdom remains a key market, and EuroValve supplies products from Birmingham to over fifty countries for HVAC, waterworks, and marine applications. France shows strong demand in nuclear power, water infrastructure, and chemical processing.

The European market benefits from industry-academic collaborations that enhance valve technology, focusing on fire-safe designs, high-temperature materials, and advanced polymer linings. Emphasizing sustainability, there is a growing need for durable, high-performance valves that reduce the need for replacements, while the expansion of renewable energy is driving applications in wind turbine cooling, biomass plants, and district heating networks for effective flow control.

Asia Pacific High-performance Butterfly Valve Market Trends

Asia Pacific dominates the global high-performance butterfly valve market with 32% market share and leads growth with a CAGR of 5.1%, establishing the region as the epicenter of industrial expansion and infrastructure development. China represents the largest single market, driven by a vast manufacturing base, continuous industrial modernization, and government environmental regulations mandating efficient flow control systems.

China's smart city initiatives, water conservation programs, and energy infrastructure investments create sustained demand for butterfly valves across the municipal, industrial, and power sectors. The country's position as an industrial hub attracts both domestic manufacturers and global suppliers, establishing local production and service capabilities to capture market share.

Japan maintains sophisticated valve manufacturing capabilities with companies focusing on precision engineering, advanced materials, and automation integration serving domestic and export markets across the Asia Pacific.

India is set to be the fastest-growing market in the region, expected to grow at a 5.1% CAGR and capture 5.2% of the global butterfly valve market by 2024. The "Make in India" initiative supports domestic manufacturing, while infrastructure projects like Jal Jeevan Mission and AMRUT 2.0 boost water sector investments.

The country’s industrial growth in chemicals, power generation, and manufacturing drives the demand for process control solutions. Meanwhile, Southeast Asian nations benefit from urbanization, infrastructure development, and foreign direct investment, thereby increasing butterfly valve adoption.

Government policies promoting environmental protection and industrial efficiency align well with the capabilities of high-performance butterfly valves, fostering continued regional growth.

Competitive Landscape

The global high-performance butterfly valve landscape remains moderately consolidated, with global leaders such as Emerson Electric Co., Flowserve Corporation, AVK Holding A/S, and Alfa Laval AB driving market momentum through broad product capabilities, strong service networks, and long-term industrial partnerships.

Their dominance is reinforced by stringent certification requirements, material innovation needs, and the critical importance of proven reliability in oil & gas, power, and process industries.

Strategic Developments

Crane Co. Triple-Eccentric Butterfly Valve Launch (January 2024)

In January 2024, Crane Co. introduced a compact triple-eccentric butterfly valve line in Germany aimed at space-restricted refinery and petrochemical applications. The design enhances thermal stability and sealing performance, enabling retrofits in constrained facilities and supporting rising triple-offset adoption driven by high-temperature, high-pressure operational demands.

ARI-Armaturen Acquisition of Warren Controls (August 2024)

In August 2024, ARI-Armaturen acquired Warren Controls to expand its presence in the U.S. control valve market. The deal integrates Warren’s distribution reach and technical expertise, strengthening ARI’s competitive position and enhancing customer access to broader valve solutions aligned with both European and North American standards.

The high-performance butterfly valve landscape is shaped by four core strategies: advanced material and triple-offset design innovation, rapid digitalization through IoT-enabled smart valves, acquisition-driven global expansion, and deep application specialization.

Leading players strengthen competitiveness by emphasizing total cost-of-ownership benefits, longer service life, energy efficiency, and reduced downtime, countering lower-cost regional alternatives focused primarily on price.

Companies Covered in High-Performance Butterfly Valve Market

- Emerson Electric Co.

- Flowserve Corporation

- AVK Holding A/S

- Alfa Laval AB

- Crane Co.

- L&T Valves Limited

- Curtiss-Wright Corporation

- NIBCO Inc.

- Valmet Oyj

- Bray International, Inc.

- KSB SE & Co. KGaA

- Georg Fischer AG (GF Piping Systems)

- Belimo Holding AG

- Parker-Hannifin Corporation

- SAMSON AG

Frequently Asked Questions

The global high-performance butterfly valve market was valued at US$5.50 billion in 2025 and is projected to reach US$7.33 billion by 2032.

The butterfly valve market is driven by global water infrastructure, oil and gas industry growth, and the adoption of Industry 4.0, which enables IoT-connected smart valves with predictive maintenance features.

The high-performance butterfly valve market is projected to grow at a CAGR of 4.2% between 2025 and 2032.

Key market opportunities include digital transformation through IoT-enabled smart valves, infrastructure in emerging markets, energy transition applications such as green hydrogen electrolyzers, and specialized segments in pharmaceuticals and food processing requiring hygienic designs compliant with FDA regulations.

The key players in the global high-performance butterfly valve market include Emerson Electric Co. (United States), Flowserve Corporation (United States), AVK Holding A/S (Denmark), Alfa Laval AB (Sweden), Crane Co. (United States), L&T Valves Limited (India), and other key companies collectively controlling prominent market share globally.