- Beauty & Personal Care

- Herbal Beauty Products Market

Herbal Beauty Products Market Size, Share, and Growth Forecast 2026 - 2033

Herbal Beauty Products Market by Product Type (Skin Care, Hair Care, Fragrance, Body Care, Cosmetics, Other), End-user (Men, Women), Distribution Channel (Online, Hypermarkets, Specialty Stores, Other), and Regional Analysis for 2026 - 2033

Herbal Beauty Products Market Size and Trend Analysis

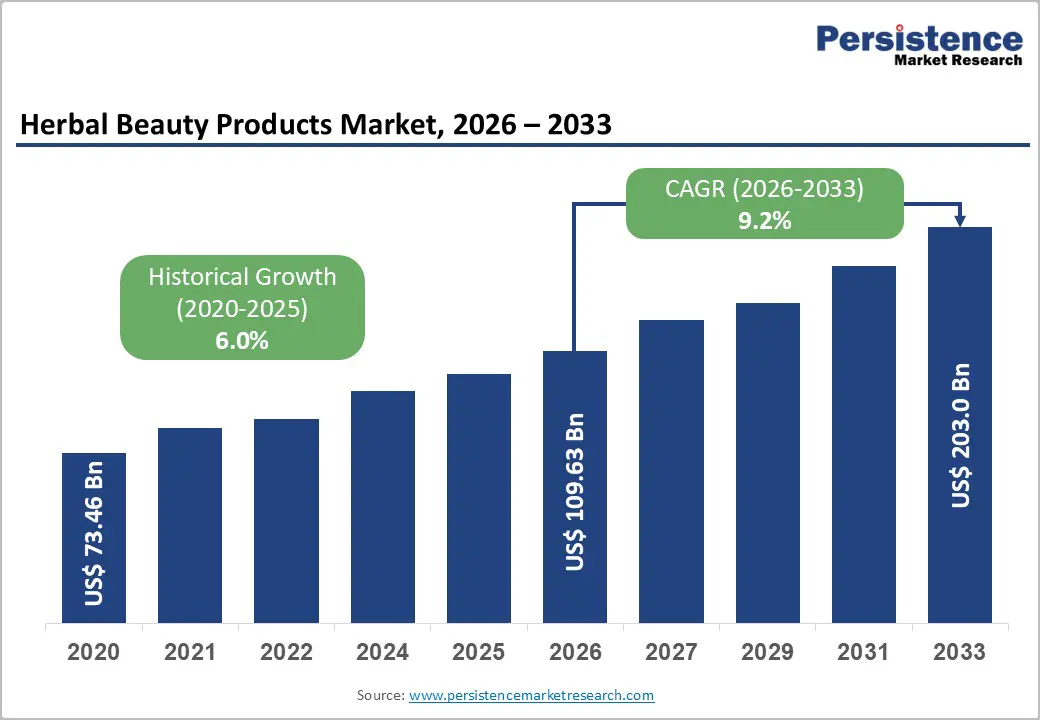

The global herbal beauty products market size is supposed to be valued at US$ 109.63 Bn in 2026 and is projected to reach US$ 203.0 Bn by 2033, growing at a CAGR of 9.2% between 2026 and 2033.

The market growth is driven by three key factors, including increasing awareness of health risks from synthetic chemicals, global adoption of wellness practices such as Ayurveda and Traditional Chinese Medicine, and the rise of herbal beauty trends through digital platforms. Around 70% of consumers prioritize environmental and health considerations when choosing skincare, reinforcing demand for herbal products. Regulatory frameworks like COSMOS certification and the European Cosmetics Regulation (EC) No 1223/2009 further strengthen trust by enforcing stringent safety and transparency standards.

Key Market Highlights:

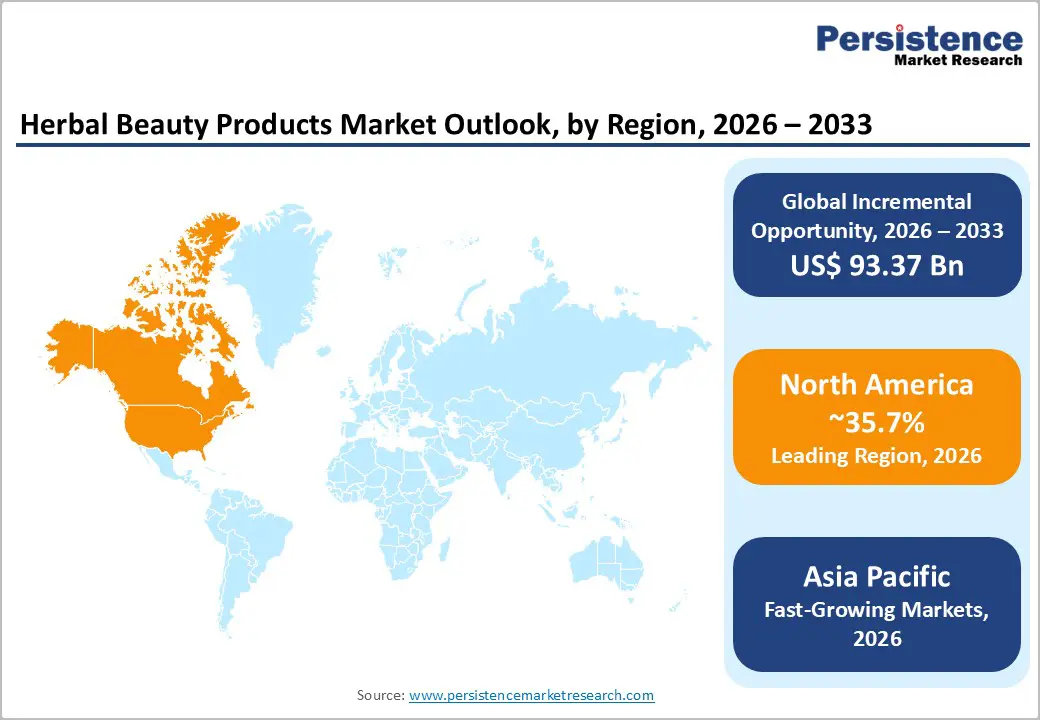

- Regional Leader: North America leads the Herbal Beauty Products Market with 35.7% share, driven by premium natural demand and regulatory support for clean beauty innovations.

- Fastest Growing Region: Asia Pacific fastest-growing region, propelled by cultural affinity for Ayurveda and Traditional Chinese Medicine, rising disposable incomes, and 40% surge in e-commerce penetration across India, China, and ASEAN nations.

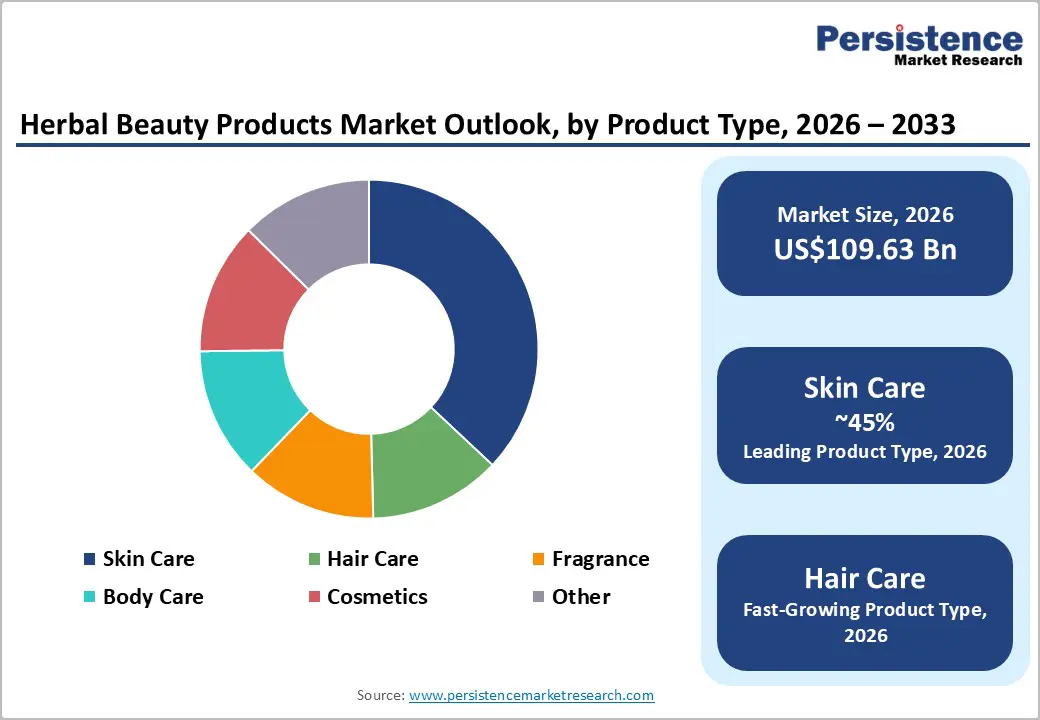

- Leading Segment: The Skin Care product category represents the dominant segment, commanding 37% market share, driven by universal prevalence of skin concerns, effectiveness of herbal alternatives, and superior consumer adoption rates.

- Fastest Growing Segment: Online emerges as the fastest-growing distribution segment, boosted by digital marketing and e-commerce penetration in urban areas.

- Key Market Opportunity: The expansion of Herbal Cosmetics and Color Cosmetics categories presents significant growth opportunities, driven by rising awareness of synthetic ingredient risks and emerging innovation in mineral-based foundations, herbal lipsticks, and eye cosmetics formulated with organic ingredients.

| Key Insights | Details |

|---|---|

| Herbal Beauty Products Market Size (2026E) | US$ 109.63 Bn |

| Market Value Forecast (2033F) | US$ 203.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 9.2% |

| Historical Market Growth (2020 - 2025) | 6.0% |

Market Dynamics

Drivers - Increasing Consumer Awareness of Health and Wellness

The global clean beauty movement is expanding rapidly as consumers increasingly prefer products free from parabens, sulfates, phthalates, and synthetic fragrances. Industry data reveals that nearly 80% of Indian women experience uneven skin tone and dark spots, fueling demand for herbal skincare enriched with natural ingredients such as turmeric, niacinamide, and glycolic acid. In 2023, the U.S. FDA issued over 200 warnings to cosmetic firms for mislabeling products as organic without meeting USDA standards, emphasizing the need for authenticity.

Social media and influencers have heightened awareness of ingredient transparency, prompting brands to adopt sustainable sourcing and eco-friendly packaging. Rising concerns over synthetic chemicals and growing wellness trends continue to drive the adoption of plant-based solutions, reinforcing long-term growth in the herbal beauty sector.

Growth of E-Commerce and Digital Distribution Channels

The rapid expansion of e-commerce and digital platforms has significantly transformed the distribution of herbal beauty products. Online beauty sales have grown from 14% market penetration in 2015 to 26% by 2024, with projections reaching 33% by 2030. The global beauty e-commerce market generated US$ 257.5 billion in 2025, reflecting a 3.4% annual increase. Social commerce now accounts for nearly 68% of online beauty purchases through platforms such as TikTok, Instagram, and Facebook, enabling niche brands and direct-to-consumer models to access global audiences without traditional retail infrastructure.

Mobile platforms represent 59% of digital checkouts, with TikTok ranking as the eighth-largest beauty retailer in the U.S. Concurrently, growing consumer preference for sustainability drives demand for eco-friendly, cruelty-free products, supported by ethical sourcing and biodegradable packaging, reinforcing brand loyalty and premium positioning.

Restraints - Higher Production Costs and Supply Chain Complexity

Manufacturing herbal beauty products involves significantly higher costs compared to conventional synthetic formulations, creating notable challenges for market expansion and profitability. These elevated expenses stem from sourcing premium botanical ingredients, employing specialized extraction techniques to obtain active compounds from herbs such as aloe vera, neem, turmeric, and amla, and maintaining rigorous quality control standards. Cost pressures are further intensified by supply chain vulnerabilities, including fluctuating agricultural yields, geographic concentration of raw material sources, and the rising costs associated with certified organic farming and fair trade compliance.

Furthermore, diverse regulatory requirements across global markets necessitate substantial investments in documentation, testing, and certification. These factors result in premium pricing, which may restrict accessibility for price-sensitive consumers and limit overall market growth in developing economies where purchasing power remains constrained.

Stringent Regulatory Requirements and Quality Standardization Challenges

The regulatory framework for herbal beauty products poses significant challenges due to increasingly stringent safety and efficacy standards across major markets. The European Union’s Cosmetics Regulation (EC) No 1223/2009 mandates comprehensive ingredient disclosure, safety assessments, and labeling requirements, while restricting the use of 372 substances under defined conditions. Similarly, the NATRUE standard requires that 95% of natural substances in certified organic products originate from controlled organic farming or certified wild collection.

In the U.S., the Modernization of Cosmetics Regulation Act (MoCRA) enforces facility registration and product listings, alongside state-level restrictions on chemicals such as PFAS and titanium dioxide. These complex regulations impose substantial compliance costs, disproportionately affecting smaller brands while favoring established companies with robust regulatory infrastructure. The lack of global standardization further complicates international expansion and delays product launches.

Opportunity - Premiumization and High-Performance Herbal Formulations

The herbal beauty market is experiencing a strong premiumization trend, with consumers increasingly willing to pay higher prices for products that emphasize superior ingredient quality, clinically validated botanical actives, and sustainable sourcing practices. This premium segment is projected to grow, reflecting a shift in perception where herbal products are viewed as long-term investments in skin and hair health rather than basic functional items.

Leading brands are capitalizing on this trend by combining traditional herbal wisdom with advanced cosmetic science. For instance, Amway introduced its Artistry Skin Nutrition Defying and Correcting Serums in 2025, incorporating 16 plant extracts such as White Chia Seed and Microalgae Complex. Similarly, KORA Organics launched plant-powered alternatives like rosehip oil and bakuchiol, offering brightening, hydration, and anti-aging benefits without irritation.

Expansion of Herbal Cosmetics and Color Cosmetics Categories

Although skincare currently dominates the herbal beauty products market, cosmetics and color cosmetics represent substantial growth opportunities. Rising consumer demand for herbal alternatives to conventional color cosmetics, often containing synthetic dyes and harmful preservatives, is accelerating as awareness of ingredient safety grows.

Innovations include mineral-based foundations infused with botanical extracts, herbal lipsticks crafted from natural waxes and plant-derived pigments, and eye cosmetics formulated with organic ingredients for sensitive skin. Organic Harvest, India’s certified organic beauty brand, exemplifies this trend through its comprehensive makeup line featuring certified organic components. Furthermore, the herbal hair care segment is expanding rapidly, driven by products enriched with aloe vera, neem, hibiscus, amla, and tea tree oil.

Category-wise Analysis

Product Type Insights

The skincare segment remains the largest and most established category in the herbal beauty products market, accounting for approximately 37% of market share in 2025 and maintaining its leadership throughout the forecast period. This dominance is driven by widespread skin concerns across demographics, the adoption of daily skincare routines globally, and the proven efficacy of herbal alternatives in addressing issues such as acne, sensitivity, dryness, and premature aging.

Consumers value herbal formulations for their gentleness and therapeutic benefits, with ingredients like turmeric for anti-inflammatory properties, neem for antimicrobial action, aloe vera for hydration, and sandalwood for skin conditioning. Continuous product diversification, including masks, serums, moisturizers, and targeted treatments, combined with innovations in botanical actives and extraction technologies, supports premium pricing and mass adoption. Influencer-driven education and social media engagement further reinforce skincare’s position as the leading segment through 2033.

End-user Insights

Women constitute the dominant end-user segment in the herbal beauty products market, accounting for approximately 72% of market share across major regions. This strong presence is driven by both biological and sociocultural factors. Women experience more frequent and varied skin concerns throughout their lives, including hormonal changes during menstruation, pregnancy, and menopause, which require specialized skincare solutions. Surveys indicate greater concern among women for conditions such as acne, sensitivity, redness, and enlarged pores compared to men.

Cultural norms and beauty standards further reinforce greater investment in personal care routines, with women typically using an average of five skincare products daily and actively engaging with beauty content on social media. Their preference for premium and specialized products positions women as the primary growth driver, shaping future strategies around targeted formulations and female-focused marketing initiatives.

Distribution Channel Insights

The online distribution channel has become the leading platform for herbal beauty products, accounting for approximately 31% of global beauty retail sales in 2026. This shift reflects fundamental changes in consumer purchasing behavior, driven by convenience, product variety, price transparency, access to customer reviews, and seamless integration of social media discovery with online shopping.

In advanced markets such as China, e-commerce dominates the skincare segment, representing nearly 87% of total beauty and skincare purchases, while in the U.S., online sales comprise 41% of beauty and personal care transactions, surpassing traditional retail. The rise of specialized platforms, Amazon’s expansion into herbal segments, and social commerce, accounting for 68% of online beauty purchases, have democratized access and strengthened direct-to-consumer models.

Regional Insights

North America Herbal Beauty Products Market Trends

The North American herbal beauty products market reflects advanced consumer sophistication, emphasizing ingredient transparency, regulatory compliance, and premium positioning. Market dynamics are shaped by heightened awareness of synthetic chemical risks, stringent safety regulations, and alignment with wellness and sustainability values. The Modernization of Cosmetics Regulation Act (MoCRA) has reinforced compliance, mandating facility registration and product listings by July 2024, alongside state-level restrictions on harmful substances such as PFAS, lead, titanium dioxide, and diethanolamine.

Consumer preferences strongly favor clean beauty, cruelty-free certifications, and sustainably sourced ingredients, positioning herbal products as premium alternatives. Illustrating this trend, Bloomy Bliss launched an organic product line in July 2024, including face oils, packs, soaps, and bath salts. E-commerce penetration reaches 41% of beauty transactions, with mobile commerce at 59%, creating significant opportunities for herbal brands through social media-driven direct-to-consumer strategies.

Europe Herbal Beauty Products Market Trends

Europe represents the most stringent regulatory environment for herbal beauty products, creating both barriers to entry and enhancing consumer trust. The EU Cosmetics Regulation (EC) No 1223/2009 mandates comprehensive ingredient disclosure, safety assessments, and labeling, while Annex III restricts 372 substances under defined conditions. Certification standards such as NATRUE and Ecocert Cosmos set benchmarks for natural and organic cosmetics, requiring 95% of natural substances to originate from certified organic farming or controlled wild collection.

Countries like Germany, France, Spain, and the U.K. have emerged as innovation hubs, driven by strong brand heritage and demand for premium, sustainably sourced products. European consumers prioritize transparency, ethical practices, and eco-conscious packaging, fueling growth in cruelty-free and vegan cosmetics. The Natural and Organic personal care market is projected to reach US$ 28.4 billion by 2025, supported by robust e-commerce and specialty retail channels.

Asia Pacific Herbal Beauty Products Market Trends

Asia Pacific is the fastest-growing market for herbal beauty products, projected to expand at a CAGR of 14.4% during the forecast period. Growth is driven by strong cultural traditions in herbal and Ayurvedic remedies, rising disposable incomes, rapid urbanization, and accelerating e-commerce adoption. China leads in market value with advanced beauty technology and premium positioning, while India contributes significantly through authentic Ayurvedic heritage and export capacity.

Japan and South Korea influence global trends via K-beauty and J-beauty, emphasizing natural ingredients, and ASEAN nations show dynamic growth fueled by an expanding middle class. India, with approximately 80% of the population following Ayurvedic traditions, has positioned itself as the authentic hub for herbal beauty innovation. The Herbal soap market, a specific subcategory within personal care, demonstrates the broader herbal product expansion, with manufacturers incorporating traditional ingredients such as turmeric, neem, aloe vera, and sandalwood into formulations addressing modern consumer concerns. Regional advantages such as raw material availability, cost-efficient production, and robust supply chains position the Asia Pacific as a global hub for herbal beauty innovation and sourcing.

Competitive Landscape

The herbal beauty products market demonstrates a moderately consolidated structure, characterized by the presence of global multinationals, regional heritage brands with strong Ayurvedic credibility, and emerging direct-to-consumer players. Leading corporations such as Procter & Gamble, Unilever, L’Oréal, and Estée Lauder dominate premium segments through extensive distribution networks, robust R&D capabilities, and strategic acquisitions of herbal and natural beauty brands. Regional leaders, including Dabur Ltd., The Himalaya Drug Company, Marico Ltd., and Lotus Herbals, maintain significant market share by leveraging authentic Ayurvedic positioning, consumer trust, and integrated retail networks. Emerging trends include subscription-based models for herbal products, AI-driven personalized skincare recommendations using skin mapping technologies, experiential retail through wellness-focused boutiques, and collaborative partnerships integrating herbal beauty with complementary wellness categories. These innovations reflect a shift toward personalization, sustainability, and holistic beauty experiences.

Key Market Developments:

- November 2024: KORA Organics introduced innovative plant-powered alternatives to conventional skincare actives, including rosehip oil as a niacinamide replacement and bakuchiol as a retinol alternative, featuring brightening, hydration, and anti-aging benefits while minimizing irritation.

- October 2025: Amway India unveiled Artistry Skin Nutrition Defying and Correcting Serums, incorporating 16 plant extracts and exclusive Nutrilite-grown White Chia Seed to target early and advanced signs of visible skin aging.

- October 2025: Himalaya Wellness launched its Turmeric Range featuring a gentle facewash, potent serum, and dark spot clearing cream with the campaign 'Unspot Your Natural Glow.

Top Companies in the Herbal Beauty Products Market

- Procter & Gamble (U.S.) maintains a commanding position in the global herbal beauty products market through its extensive portfolio spanning skincare, haircare, cosmetics, and wellness categories, supported by unparalleled research and development investments, global distribution infrastructure encompassing over 180 countries, and strategic acquisitions of herbal and natural beauty brands. The company's market influence is evident in its ability to integrate herbal ingredients into premium product lines while maintaining rigorous safety and efficacy standards, commanding significant market share through both mass-market and premium retail channels.

- Dabur Ltd. (New Delhi, India) represents the largest Ayurvedic and herbal beauty products manufacturer in India and a significant global player, with a comprehensive portfolio including Vatika, Dabur Amla, Dabur Red (toothpaste), Gulabari (rose water), and Dabur Chyawanprash. The company's market dominance is anchored in authentic Ayurvedic heritage, extensive rural and urban distribution networks, and strategic marketing emphasizing traditional ingredients and wellness benefits, generating substantial revenue from herbal skincare, haircare, and oral care segments.

- The Himalaya Drug Company (Bangalore, India) commands premium positioning in the global herbal beauty products market through its commitment to Ayurvedic principles, rigorous quality control standards, and innovative product development. The company's brand portfolio includes Himalaya Herbals, recognized internationally for facial skincare and cleansing products, supported by WHO-GMP certifications and certifications from global regulatory bodies, enabling substantial international export revenue and premium market positioning across North America, Europe, and the Asia Pacific regions.

Companies Covered in Herbal Beauty Products Market

- Amway

- Pfizer Inc.

- Givaudan Active Beauty

- Herbalife Nutrition

- LR Health and Beauty

- Marico Ltd.

- Lotus Professional

- Vasa Global Cosmetics

- Klienz Herbal

- Hemas Holding PLC

- Procter & Gamble Company

- Dabur Ltd.

- The Himalaya Drug Company

Frequently Asked Questions

The global herbal beauty products market is projected to reach US$ 203.0 billion by 2033, growing from US$ 109.63 billion in 2026 at a CAGR of 9.2%.

The herbal beauty products market growth is driven by escalating consumer awareness regarding the harmful effects of synthetic chemicals, rising disposable incomes enabling premium product adoption, expanding e-commerce penetration, and stringent regulatory frameworks like COSMOS and ECOCERT ensuring product authenticity across Europe and North America.

The Skin Care segment dominates the market with approximately 37% market share in 2026, driven by consumer awareness of herbal benefits for improved skin texture, acne reduction, and anti-aging properties.

North America with 35.7% share, is driven by premium clean beauty demand.

The expansion of the Herbal Cosmetics and Color Cosmetics categories presents the most significant growth opportunity, driven by rising consumer preference for natural alternatives to conventional color cosmetics containing synthetic dyes and potentially harmful preservatives.

Leading companies include Procter & Gamble, L'Oréal, Unilever, Estée Lauder, Dabur Ltd., The Himalaya Drug Company, Marico Ltd., Amway, and emerging direct-to-consumer brands representing diverse competitive strategies spanning multinational corporations, heritage Ayurvedic companies, and digital-native brands.