- Beauty & Personal Care

- Herbal Toothpaste Market

Herbal Toothpaste Market Size, Share, and Growth Forecast, 2026 - 2033

Herbal Toothpaste Market by Ingredient (Neem, Charcoal, Clove, Mint, Aloe Vera), Form (Paste, Powder, Gel), Distribution Channel (Supermarkets, Online Retail), and Regional Analysis for 2026 - 2033

Herbal Toothpaste Market Share and Trends Analysis

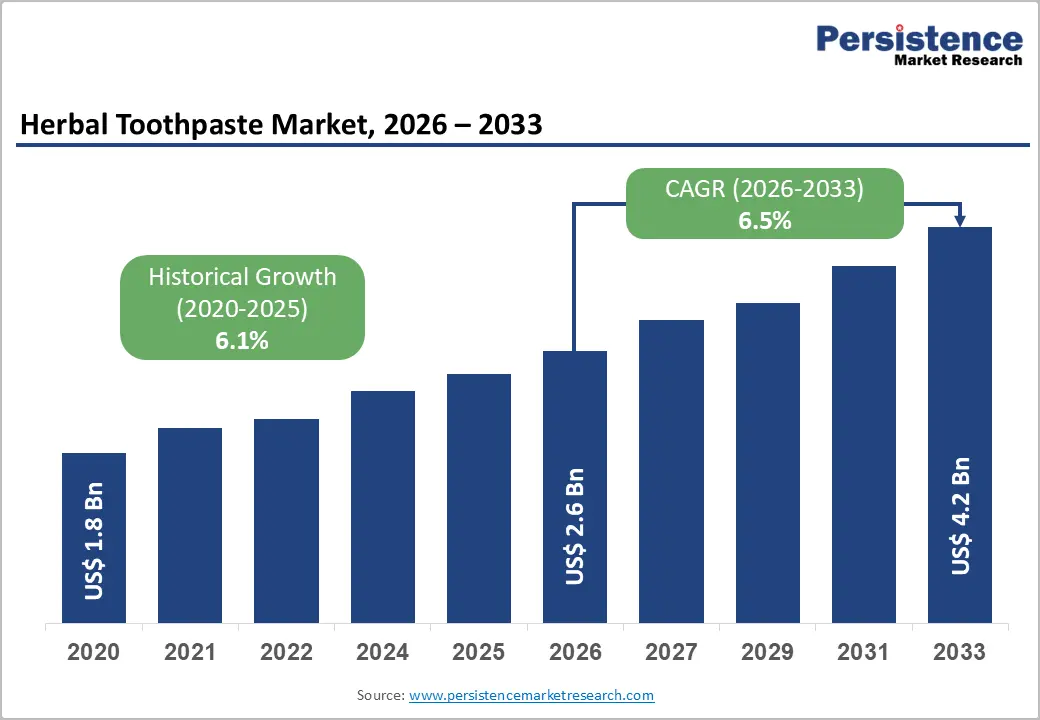

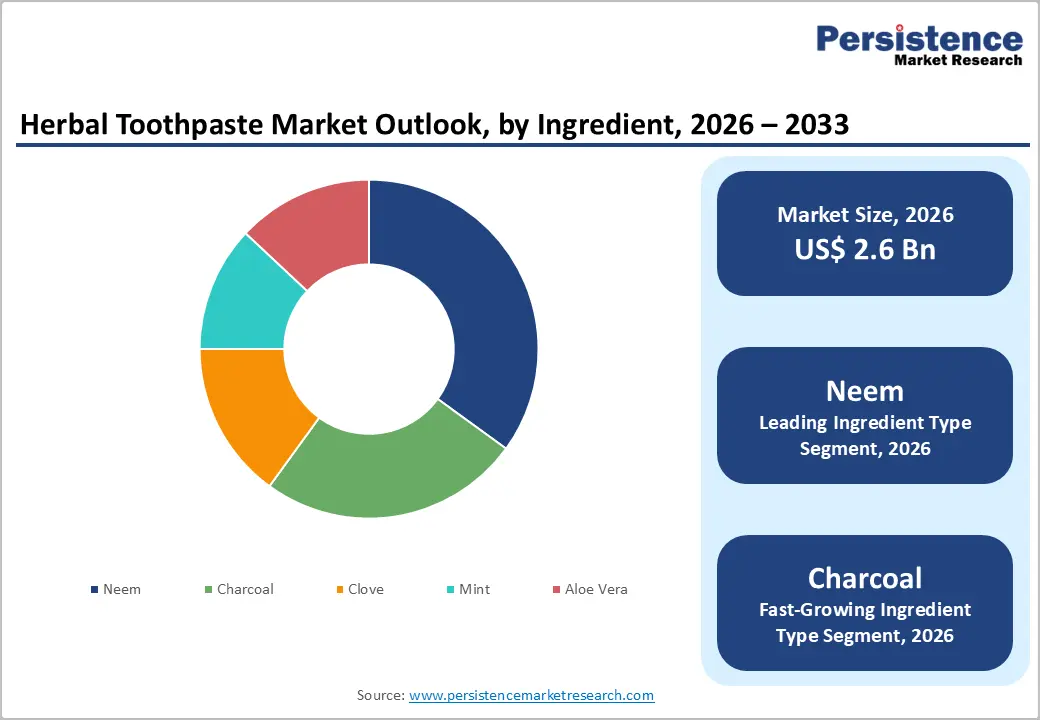

The global herbal toothpaste market size is likely to be valued at US$ 2.6 billion in 2026, and is projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 6.5% during the forecast period 2026 - 2033.

This expansion reflects rising consumer preference for natural oral care products, driven by increasing health consciousness and growing awareness of potential side effects associated with synthetic ingredients. The market benefits from expanding distribution networks in emerging economies, supportive regulatory frameworks for herbal products, and continuous product innovation targeting specific oral health concerns. Demographic shifts toward preventive healthcare and the millennial generation's affinity for organic products further accelerate market penetration across developed and developing regions.

Key Industry Highlights

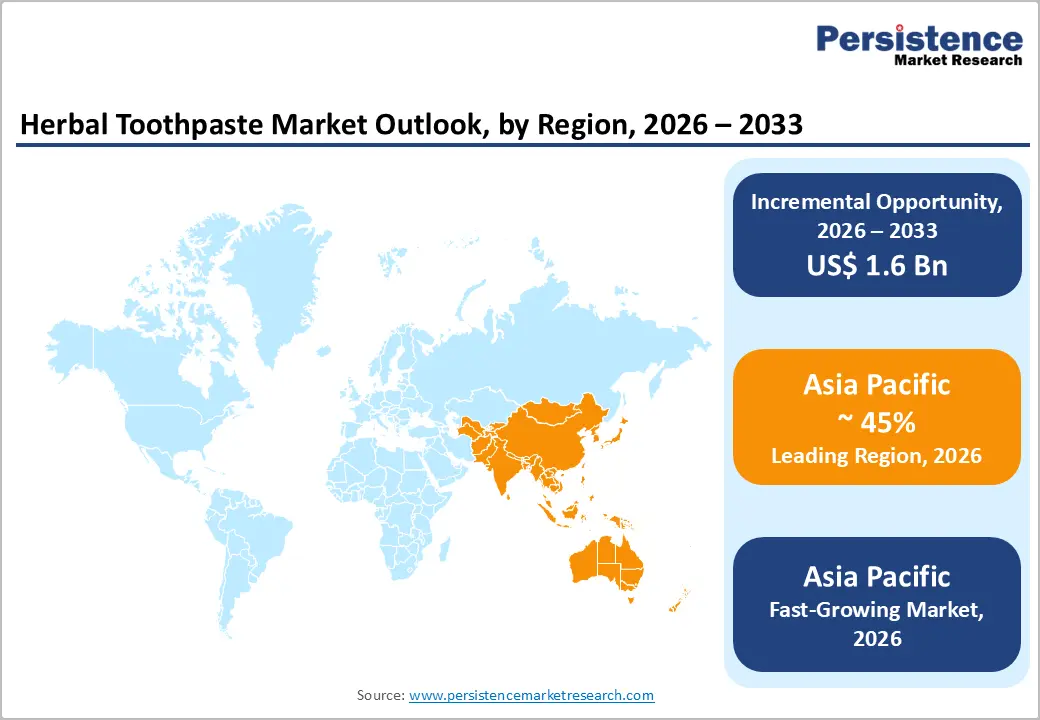

- Dominant Region & Fastest-growing Regional Market: Asia Pacific is likely to be both the leading and fastest-growing regional market for herbal toothpaste in 2026, accounting for approximately 45% of market share.

- Leading & Fastest-growing Ingredient: Neem is set to dominate with an estimated 2026 share of 35%, with charcoal growing the fastest during the 2026 - 2033 forecast period.

- Leading & Fastest-growing Form: Paste is anticipated to hold the largest revenue share at about 78% in 2026, while powder is projected to be the fastest-growing segment over the 2026 - 2033 forecast period.

- Major Driver: Oral health concerns now influence broader lifestyle and purchasing decisions, as people increasingly prioritize long-term well-being and product safety.

- Key Opportunity: Rising interest in natural oral care creates significant headroom for innovation in herbal toothpaste portfolios.

| Key Insights | Details |

|---|---|

| Herbal Toothpaste Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 4.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Consumer Awareness about Chemical-Free Oral Care Products

According to the World Health Organization (WHO), oral diseases affect nearly 3.5 billion people globally. Oral health concerns now influence broader lifestyle and purchasing decisions, as people increasingly prioritize long-term well-being and product safety. Consumers are paying closer attention to what they put in their mouths, favoring formulations that rely on botanical ingredients and traditional knowledge systems rather than purely synthetic chemistry. This mindset aligns with a growing preference for transparency, where clear labeling, traceable sourcing, and simple ingredient lists help build trust. Accordingly, herbal oral care is evolving from a niche option into a credible component of mainstream preventive health routines, particularly among digitally informed, research-oriented buyers who actively compare products before making a choice.

For manufacturers, this shift creates both strategic risk and opportunity. Companies that adapt by integrating herbal actives, investing in clinical validation, and educating consumers about benefits can reposition their brands as responsible and forward-looking. Reformulating existing product ranges with plant-based alternatives, such as neem, clove, or mint extracts, allows established players to protect market share while meeting rising expectations around safety and sustainability. At the same time, younger consumers, especially those in the millennial and Generation Z segments, are reshaping category dynamics by rewarding brands that demonstrate authenticity, ethical sourcing, and alignment with broader wellness lifestyles, which prompts incumbents to accelerate innovation and reconsider their long-term portfolio strategies.

Limited Clinical Evidence and Standardization Challenges

Limited clinical evidence remains a critical constraint for herbal toothpaste companies, particularly compared with well-studied fluoride-based formulations. Many products enter the market with only basic in-house testing, which falls short of expectations from regulators, dental professionals, and increasingly informed consumers. Authorities in developed markets now expect well-designed clinical trials that demonstrate outcomes such as plaque reduction, cavity prevention, and improvements in gum health under realistic use conditions. For brands, the lack of rigorous evidence makes it difficult to secure professional endorsements, justify premium positioning, or defend claims during regulatory review, thereby limiting acceptance in pharmacies and specialist retail channels.

Standardization of herbal ingredients adds another layer of complexity that directly affects product reliability and brand credibility. The potency and composition of plant extracts can vary significantly depending on factors such as geography, season, cultivation practices, and extraction method, which makes it challenging to guarantee consistent performance from batch to batch. Without harmonized quality benchmarks and validated testing protocols, manufacturers struggle to align supply chains, maintain uniform efficacy, and reassure skeptical consumers who compare herbal offerings with established conventional brands. Companies that invest in robust sourcing standards, third-party certifications, and transparent communication about testing practices can mitigate these concerns and position themselves as more trustworthy within an increasingly competitive oral care landscape.

Product Innovation and Diversification

Rising interest in natural oral care creates significant headroom for innovation in herbal toothpaste portfolios. As consumers seek products that are both gentle and effective, brands can develop targeted formulations that address specific needs such as sensitivity relief, gum support, enamel protection, and stain management, using clinically supported botanical actives. There is also meaningful potential in incorporating lesser-known but potent herbs from systems such as Ayurveda, Traditional Chinese Medicine, and indigenous practices, provided companies invest in robust safety assessments and efficacy validation to strengthen confidence among both professionals and consumers.

Developing a multifunctional herbal toothpaste that offers several benefits in a single product can appeal to time-constrained users who prefer streamlined routines. Flavor innovation represents another growth lever, as milder, child-friendly variants and more sophisticated adult flavors can improve acceptance across age groups and cultural preferences. Segmented offerings for children, teenagers, adults, and seniors can align formulations with life-stage-specific oral health priorities and reinforce brand relevance. Finally, sustained investment in evidence-based marketing, digital education, and collaboration with dental professionals can demystify herbal ingredients, reduce skepticism, and position herbal toothpaste as a credible choice within preventive oral care strategies.

Category-wise Analysis

Ingredient Insights

Neem is slated to maintain a dominant position, with an estimated 35% of the herbal toothpaste market revenue share in 2026, due to its well-established antibacterial properties and strong cultural acceptance across South Asia. Neem is widely recognized for its strong antibacterial and anti-inflammatory properties, which makes it a valuable component in formulations that support cavity prevention and gum health. Its use in oral care has deep roots in Ayurvedic traditions, particularly in India, where chewing neem twigs has long served as a traditional method of cleaning teeth and maintaining oral hygiene.

Modern herbal toothpaste brands draw on this heritage by incorporating neem extracts to help control harmful bacteria, reduce plaque, and support fresher breath, reinforcing its position as a core ingredient in many natural oral care products.

Charcoal is likely to be the fastest-growing segment during the 2026 - 2033 forecast period. Charcoal-based formulations have become one of the most dynamic areas of innovation in the herbal toothpaste category, driven by viral social media exposure, distinctive visual appeal, and strong relevance for younger, trend-conscious consumers. Activated charcoal toothpastes are typically positioned around perceived whitening and detox benefits, which helps them stand out on crowded shelves and across digital marketplaces, even though expert opinions on their long-term efficacy and abrasivity remain mixed. Influencer endorsements, aspirational branding, and premium packaging further strengthen their appeal, leading many companies to prioritize charcoal variants within new product development pipelines and recent launch portfolios.

Form Insights

Paste is forecasted to hold the highest revenue share, projected to touch 78% in 2026. It offers a smooth, easy-to-dispense texture, consistent foaming, and familiar flavors, which together reduce perceived switching risk when consumers move from conventional to herbal products. From a formulation standpoint, pastes enable uniform dispersion of herbal active ingredients in a hydrated base that typically includes humectants, mild abrasives, binders, and flavoring agents, helping balance efficacy with comfort and overall mouthfeel.

For manufacturers, paste formats are well-suited to high-speed production lines and standard tube packaging, which supports economies of scale, reliable quality control, and broad retail availability across supermarkets, pharmacies, and online channels.

Powder is projected to be the fastest-growing segment over the 2026 - 2033 forecast period. Powder formulations, by contrast, use a dry blend of abrasives, minerals, and herbal ingredients that consumers moisten with water or saliva at the point of use, rather than applying them in a pre-hydrated form. This format typically appeals to users who prefer minimal, low-water, or more traditional routines and who respond well to products positioned around natural, simple, or low-additive compositions, since powders generally do not require the same level of humectants, thickeners, or preservatives found in paste formulations.

Distribution Channel Insights

The supermarket segment is positioned to lead with an approximate 55% of the herbal toothpaste market share in 2026. Supermarkets continue to serve as a primary distribution channel for herbal toothpaste, as they allow shoppers to physically inspect packaging, textures, and claims before making a purchase. These large-format stores typically allocate prominent shelf space to personal care ranges, which enhances the visibility of herbal variants and encourages trial among mainstream consumers. Shoppers also benefit from the ability to compare multiple brands, formats, and price points in a single trip, which supports informed decision-making and basket-building behavior.

Online retail is expected to be the fastest-growing segment throughout the 2026 - 2033 forecast period. Online channels have become an increasingly important route to market for herbal toothpaste, as they allow consumers to research, compare, and purchase products without visiting a physical store. The expansion of digital marketplaces and brand-owned websites has broadened access to both mainstream and niche herbal brands, giving shoppers more choice in terms of ingredients, claims, and price points. These platforms also enhance value perception by bundling products, personalizing recommendations, and integrating user reviews that help guide purchase decisions.

Regional Insights

Asia Pacific Herbal Toothpaste Market Trends

Asia Pacific is expected to be both the leading and fastest-growing regional market for herbal toothpaste in 2026, accounting for approximately 45% of the market share. Asia Pacific has emerged as the strategic centre of gravity for the herbal toothpaste industry, with demand rooted in long-standing traditions of plant-based medicine and reinforced by rapid economic and demographic shifts. Oral care brands in this region benefit from a large and increasingly health-conscious population that understands systems such as Ayurveda and Traditional Chinese Medicine, which makes consumers more receptive to herbal formulations as credible alternatives to conventional pastes.

Urbanization, rising disposable incomes, and the expansion of modern retail and e-commerce networks convert this cultural openness into sustained category growth, particularly as younger households prioritize preventive health and actively choose products that support natural and holistic lifestyles.

Within the region, India, China, and Japan each play distinct strategic roles that influence competitive priorities and go-to-market strategies. India’s market is strongly shaped by Ayurvedic heritage, where brands such as Dabur, Patanjali, and Himalaya have translated traditional oral care practices into large-scale, packaged products that are supported by formal quality standards and policy backing from the Ministry of Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homeopathy (AYUSH), including codification through the Ayurvedic Pharmacopoeia of India.

China’s trajectory is characterized by sustained government support for Traditional Chinese Medicine, rising health awareness following recent public health events, and a highly developed digital commerce ecosystem that enables herbal brands to expand rapidly without depending solely on physical retail.

Europe Herbal Toothpaste Market Trends

Europe is a strategically important market for herbal toothpaste manufacturers, underpinned by strong awareness of natural products and close alignment with environmental values. Consumers in key countries such as Germany, the United Kingdom, France, and Spain tend to assess products through the lens of safety, sustainability, and ingredient transparency, which naturally favors herbal and organically positioned formulations. For companies, this means that success depends not only on offering plant-based ingredients but also on meeting expectations for eco-friendly packaging, responsible sourcing, and clear communication of product benefits that remain fully aligned with applicable regulatory requirements.

From a regulatory and competitive standpoint, Europe offers both structure and opportunity for herbal toothpaste brands. The European Union Cosmetics Regulation provides a harmonized framework for safety assessment, ingredient control, and labelling, which enables companies to design portfolios that can be marketed across multiple countries while remaining compliant. In parallel, sustainability policies and circular-economy objectives encourage investment in low-impact materials and processes, thereby reinforcing the appeal of herbal toothpaste as a greener alternative.

North America Herbal Toothpaste Market Trends

North America is an innovation-driven market for herbal toothpaste, shaped by high purchasing power, sophisticated retail infrastructure, and a clear shift toward clean-label personal care. Consumers in the United States, in particular, often scrutinize ingredient lists and prefer formulations that use recognizable, plant-based components with limited synthetic additives. This behavior makes herbal toothpaste a logical fit within broader wellness and lifestyle trends, where products must demonstrate safety, transparency, and alignment with environmental and ethical values to secure and maintain shelf presence. For manufacturers, the region rewards brands that combine credible natural positioning with strong performance, supported by clear claims and accessible consumer education.

The regulatory and competitive context in North America sets a high benchmark for success in the herbal toothpaste category. Oversight by authorities such as the United States Food and Drug Administration (FDA) and the Federal Trade Commission (FTC) requires companies to substantiate both safety and marketing claims, which encourages serious players to invest in rigorous testing, thorough documentation, and responsible communication practices. Third-party certifications and recognized natural product standards further help distinguish credible brands and reduce perceived risk for retailers and consumers.

Competitive Landscape

The global herbal toothpaste market structure is moderately fragmented, dominated by leading players such as Colgate-Palmolive Company, Dabur India Limited, The Himalaya Drug Company, GlaxoSmithKline plc, and Patanjali Ayurved Limited. These players collectively capture 35-40% of market share. The competitive environment is characterized by ongoing innovation, collaboration, and brand-building efforts.

Leading players are broadening their herbal toothpaste ranges to address different consumer needs, including specific oral health concerns, flavour preferences, and life-stage requirements. As interest in natural and organic formulations grows alongside higher awareness of oral hygiene, rivalry has intensified, with brands seeking to differentiate on ingredient quality, sustainability, and perceived efficacy.

Key Industry Developments

- In December 2025, Tick My Health launched Dr. Aayu Green Triphala Toothpaste, an Ayurvedic, chemical-free toothpaste formulated without SLS, parabens, artificial colors, or foaming agents, targeting health-conscious consumers seeking safer daily oral care.

- In March 2025, Himalaya Wellness Company introduced HiOra-D, a medicated toothpaste tailored for diabetics to address heightened oral health risks such as dry mouth, periodontitis, gingivitis, and bad breath. This sugar-free, vegetarian formula with herbal ingredients such as clove and cinnamon provides 12-hour germ protection, reduces salivary glucose, balances pH, and supports gum health amid diabetes-related complications.

- In February 2025, Dabur emerged as the second-largest player in India’s oral care segment within modern trade channels, driven by strong growth in Dabur Red Toothpaste, premium brand Meswak, and the newer Dabur Gel Toothpaste portfolio, which recorded over 50% year-on-year growth in the latest quarter.

Companies Covered in Herbal Toothpaste Market

- Colgate-Palmolive Company

- Dabur India Limited

- The Himalaya Drug Company

- GlaxoSmithKline plc

- Church & Dwight Co., Inc.

- The Procter & Gamble Company

- Unilever PLC

- Patanjali Ayurved Limited

- Henkel AG & Co. KGaA

- Dental Expert Limited (Vicco)

- Tom's of Maine

- Desert Essence

- Weleda AG

- Auromere Ayurvedic Imports

- The Humble Co.

Frequently Asked Questions

The global herbal toothpaste market is projected to reach US$ 2.6 billion in 2026.

Growing consumer preference for natural, chemical-free oral care products and rising awareness of the side effects of conventional fluoride are driving the market.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Premium, functional, and fluoride‑free herbal formulations, eco‑friendly packaging, and e‑commerce/D2C channels are key market opportunities.

Colgate-Palmolive Company, Dabur India Limited, The Himalaya Drug Company, GlaxoSmithKline plc, and Patanjali Ayurved Limited are some of the key players in the market.