- Healthcare Services

- Herbalist and Herbal Practitioner Market

Herbalist and Herbal Practitioner Market Size, Share, and Growth Forecast, 2025 - 2032

Herbalist and Herbal Practitioner Market By Practice Setting (Solo Herbal Practice, Naturopathic and CAM Clinics), Service Type (Herbal Consultation and Diagnosis), Patient Type (Adults, Geriatric Population), and Regional Analysis for 2025 - 2032

Herbalist and Herbal Practitioner Market Size and Trends Analysis

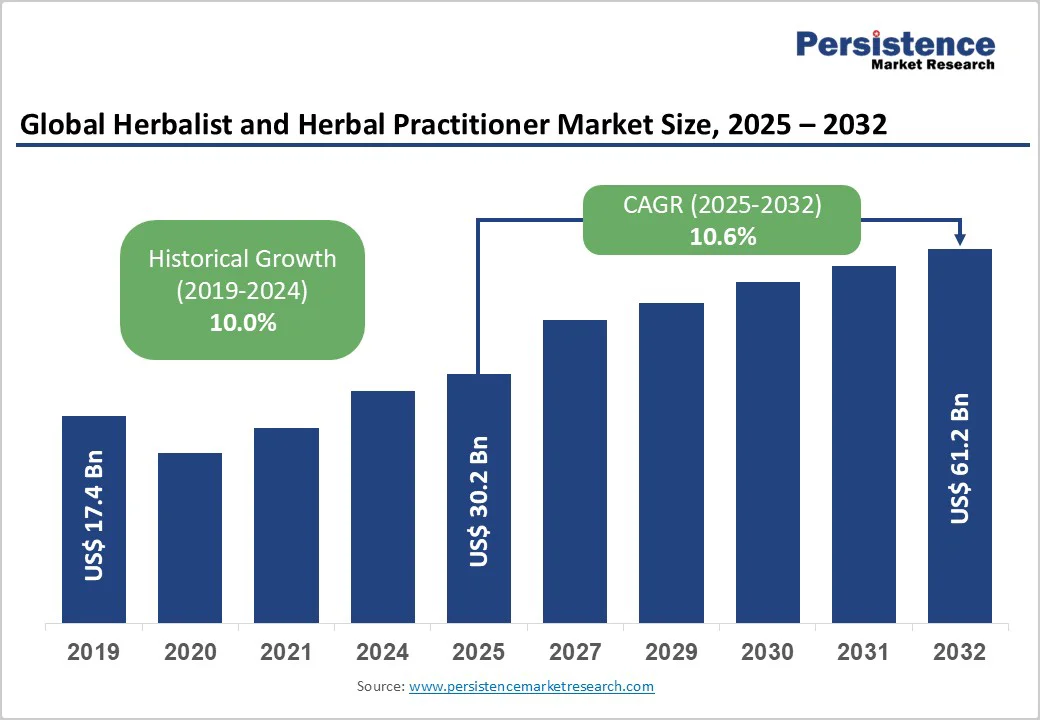

The global herbalist and herbal practitioner market size is likely to be valued at US$30.2 billion in 2025. It is estimated to reach US$61.2 billion in 2032, growing at a CAGR of 10.6% during the forecast period 2025 - 2032, driven by a surging shift toward natural, preventive, and holistic healthcare.

Consumers are becoming wary of the side effects of synthetic drugs and are turning to herbal remedies for chronic conditions.

Key Industry Highlights

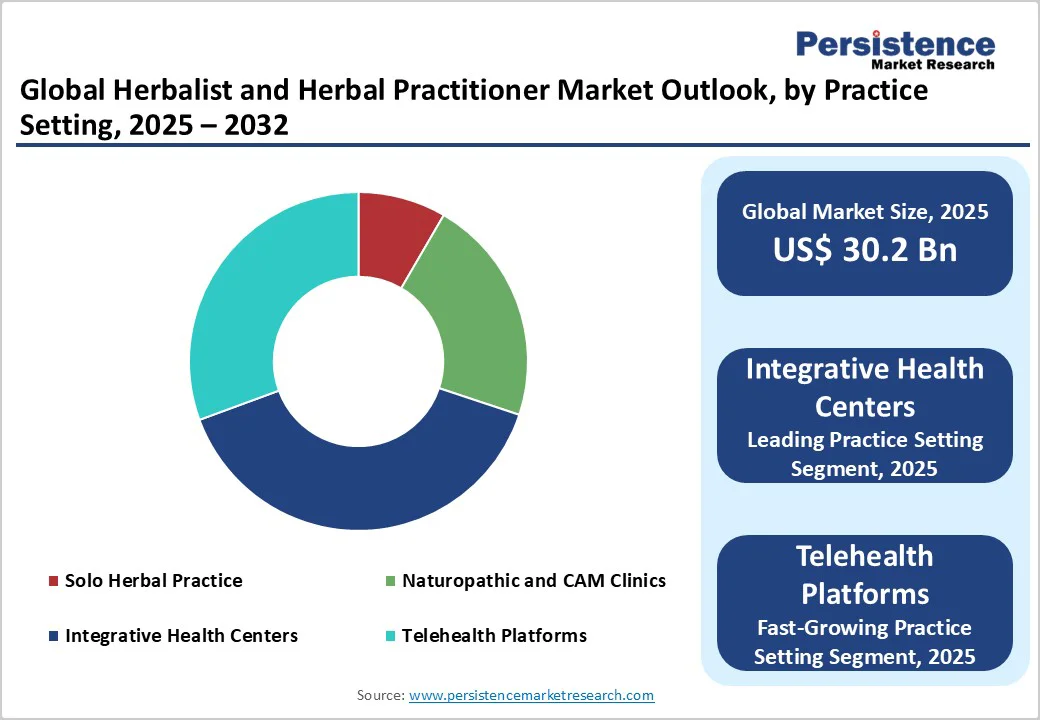

- Leading Practice Setting: Integrative health centers hold nearly 39.3% share in 2025, owing to rising consumer demand for holistic care combining herbal, nutritional, and lifestyle therapies.

- Dominant Service Type: Herbal consultation and diagnosis, accounting for approximately 43.7% of the herbalist and herbal practitioner market share in 2025, as patients seek personalized herbal advice tailored to specific health concerns.

- Key Patient Type: Adults accounted for about 49.6% in 2025, as they are more prone to stress, metabolic issues, and chronic diseases.

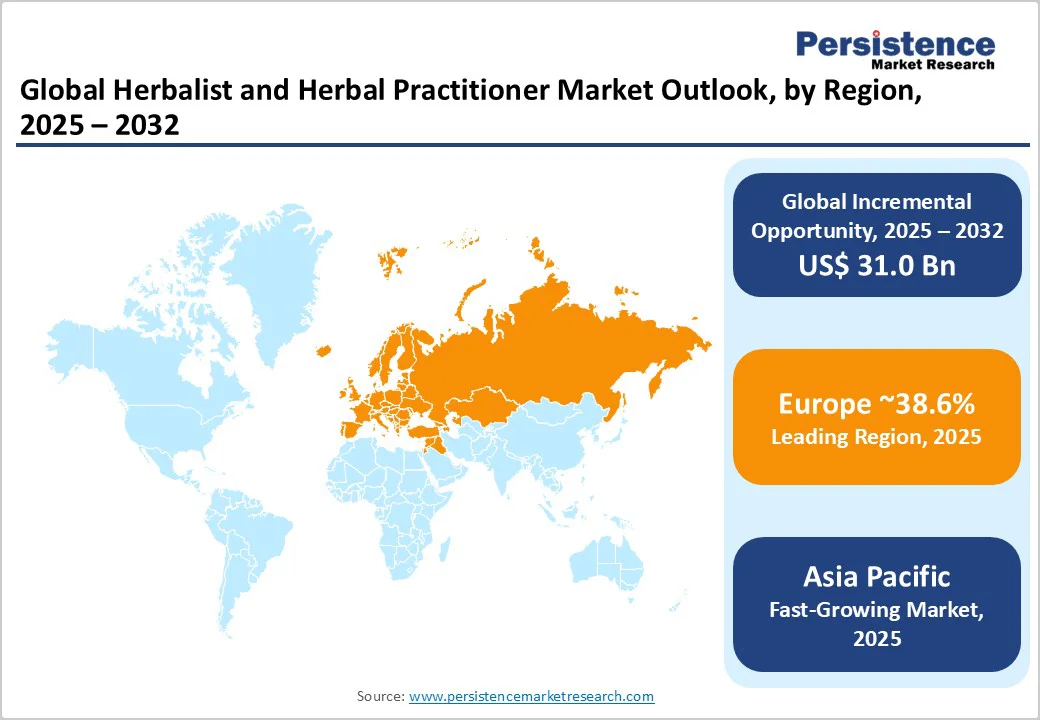

- Leading Region: Europe, with about 38.6% share in 2025, spurred by a high concentration of certified herbal practitioners and formal training institutions.

- Fastest-growing Region: Asia Pacific, backed by deep cultural roots of herbal medicine in India, China, and Japan.

- Government Initiative: India hosted the prestigious WHO-International Regulatory Cooperation for Herbal Medicines (IRCH) Workshop from August 6 to 8, 2025. The workshop brought together global experts and regulators to strengthen capacity in the regulation of herbal medicines.

| Key Insights | Details |

|---|---|

| Herbalist and Herbal Practitioner Market Size (2025E) | US$30.2 Bn |

| Market Value Forecast (2032F) | US$61.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Inclination toward Holistic and Preventive Wellness

A surging number of consumers are moving away from symptom-based treatments and embracing herbal and holistic approaches that focus on prevention and long-term wellness. This trend is pushed by increasing awareness of side effects associated with synthetic drugs and a rising preference for natural healing methods.

For instance, surveys in 2024 across the U.K. and Germany revealed that over 45% of respondents preferred herbal remedies for managing mild conditions, including anxiety and digestive issues. The integration of herbal therapies into preventive health plans, workplace wellness programs, and spa-based treatments is further fueling this shift, positioning herbal practitioners as essential partners in maintaining everyday well-being.

Expanding Academic and Certification Opportunities

The global rise in accredited herbal medicine programs and standardized certification frameworks is strengthening the credibility of herbal practitioners. Institutions such as the American Herbalists Guild and the European Herbal & Traditional Medicine Practitioners Association have expanded their accredited courses, ensuring practitioners meet professional safety and efficacy standards.

In Australia, for example, the 2024 expansion of the Bachelor of Health Science (Western Herbal Medicine) program attracted record enrollments. These developments not only professionalize the market but also encourage more medical collaborations and insurance recognition, improving public trust and broadening patient access to certified herbal experts.

Barrier Analysis - Delays in Identifying and Treating Serious Medical Conditions

One key concern in herbal practice is that patients often turn to herbalists as a first line of care, which can delay timely diagnosis and treatment of serious illnesses. For instance, cancer and cardiovascular conditions may progress unnoticed if individuals rely solely on herbal remedies without medical evaluation.

In the U.K., the Medicines and Healthcare Products Regulatory Agency (MHRA) has repeatedly warned patients about using unlicensed herbal products instead of prescribed treatments. Such delays not only compromise patient safety but also undermine trust in herbal systems. It often prompts calls for better integration between herbal practitioners and conventional healthcare providers to ensure early detection of life-threatening conditions.

Discouragement from Continuing Conventional Medical Care

Another major challenge is that some herbal practitioners, due to inadequate training or overconfidence in herbal efficacy, may advise patients to stop using prescribed medications. This practice can lead to severe health complications, especially in chronic cases such as diabetes or hypertension.

In 2024, reports from the U.S. National Center for Complementary and Integrative Health highlighted several cases where discontinuing allopathic drugs led to hospitalizations. Such incidents underscore the need for strict regulatory oversight and continuous professional education, ensuring that herbal consultations complement rather than replace evidence-based medical treatments.

Opportunity Analysis - Integrating Sustainability and Ethical Sourcing into Herbal Training

An emerging market opportunity lies in educational institutions that emphasize sustainability and ethical sourcing in their curricula. Modern programs now combine traditional herbal knowledge with courses on sustainable botany and biodiversity conservation.

For example, universities in Germany and the Netherlands have introduced herbal medicine degrees focusing on responsible wildcrafting and ecological balance. This not only ensures the long-term availability of medicinal plants but also complies with global movements toward green healthcare and ethical consumerism.

Evidence-based Validation through Clinical Research

Another promising growth avenue is the increasing scientific evaluation of herbal treatments through structured clinical trials. Research institutions in Japan, Australia, and India are conducting studies to assess herbs such as ashwagandha for stress relief and turmeric for the management of inflammation.

These investigations help bridge traditional wisdom with modern evidence, improving credibility among healthcare professionals and regulators. For instance, the European Medicines Agency (EMA) has expanded its list of approved traditional herbal monographs based on new clinical data.

Category-wise Analysis

Practice Setting Insights

Integrative health centers are speculated to account for around 39.3% of the market share in 2025, since they combine herbal medicine with other evidence-based therapies such as acupuncture, physiotherapy, and nutritional counseling under one roof. This multidisciplinary model appeals to patients seeking holistic yet credible care. These centers often collaborate with licensed physicians and dietitians, which improves their acceptance in mainstream healthcare.

Telehealth platforms are witnessing steady growth as more patients embrace digital consultations for convenience and accessibility. Herbal practitioners, who traditionally relied on in-person visits, now conduct video-based assessments and prescribe herbal formulations online. This model has expanded rapidly after the pandemic, with platforms such as TeleAyurveda in India and Herbalist Online in the U.S. providing 24/7 consultations and doorstep delivery of prescribed remedies.

Service Type Insights

Herbal consultation and diagnosis are poised to capture approximately 43.7% of the share in 2025, as it is the foundation of all herbal therapies. Practitioners invest significant time in understanding a patient’s constitution, diet, and lifestyle before recommending herbs, making it the most frequent and essential service interaction. The rise in chronic conditions such as anxiety, insomnia, and digestive issues has also increased demand for continuous follow-ups and lifestyle-based consultations.

Personalized herbal formulations have become a key service type as modern consumers move away from generic supplements toward customized blends tailored to their individual health needs. Practitioners now prepare bespoke tinctures and powders based on body type, allergies, and coexisting medical conditions. Such personalization not only improves efficacy but also builds patient loyalty through exclusive, practitioner-guided care.

Patient Type Insights

Adults are likely to hold a share of nearly 49.6% in 2025, as they seek preventive and lifestyle-based healthcare solutions. Adults in their 30s to 50s are increasingly turning to herbal medicine for managing work-related stress, metabolic issues, and sleep disorders. A 2024 report by the National Center for Complementary and Integrative Health (NCCIH) found that over 36% of U.S. adults use some form of herbal or natural therapy annually, showcasing a steady mainstream shift.

The geriatric population is a key patient segment because older adults often prefer herbal and natural treatments for chronic illnesses such as arthritis, hypertension, and cognitive decline, where long-term drug use causes side effects. Herbal therapies are perceived as gentler and more sustainable, complying with preventive aging trends. Traditional systems such as TCM and Ayurveda have dedicated geriatric care modules emphasizing rejuvenation and vitality enhancement.

Regional Insights

Europe Herbalist and Herbal Practitioner Market Trends

In 2025, Europe is expected to account for nearly 38.6% of the share. The U.K., Germany, and France have formal associations and accreditation systems, but the profession is not uniformly recognized across the continent. The EU Traditional Herbal Medicinal Products Directive (THMPD) requires all herbal medicines to undergo safety and quality testing. It has increased consumer trust but also made it difficult for small practitioners to market their remedies.

Various local herbalists now collaborate with pharmacists and integrative clinics to remain compliant. The region has also seen a rise in educational programs, such as those offered by the European Herbal and Traditional Medicine Practitioners Association (EHTPA), which focus on clinical herbalism and evidence-based practice. Public demand for natural alternatives to pharmaceuticals remains strong, with the U.K.’s National Health Service (NHS) funding pilot programs that include herbal and complementary therapies for chronic pain management.

Asia Pacific Herbalist and Herbal Practitioner Market Trends

In Asia Pacific, herbal practice is deeply rooted in traditional healthcare systems and enjoys significant government backing. China’s Traditional Chinese Medicine (TCM) and India’s Ayurveda are officially integrated into public health services, with government hospitals employing licensed practitioners. China has over 70,000 TCM hospitals and clinics, and the sector continues to surge through modernization and digitization, including AI-assisted herbal diagnosis tools.

India’s AYUSH Ministry (Ayurveda, Yoga, Unani, Siddha, and Homeopathy) has expanded practitioner training programs and partnered with Japan and Australia to promote Ayurveda care abroad. In Southeast Asia, Thailand and Indonesia are developing standardized training programs for herbal healers to meet rising demand for wellness tourism. The Asia Pacific market also benefits from easy access to native medicinal plants, enabling rapid innovation in personalized herbal treatments.

North America Herbalist and Herbal Practitioner Market Trends

In North America, the market is more fragmented but rapidly evolving. There is no federal licensing for herbalists in the U.S. or Canada, so most practitioners operate under voluntary professional bodies such as the American Herbalists Guild (AHG) or hold naturopathic or acupuncture licenses. Despite regulatory gaps, herbal therapy is becoming mainstream as consumers shift toward plant-based wellness.

A 2024 survey by the National Center for Complementary and Integrative Health (NCCIH) found that nearly four in ten U.S. adults use herbal or natural products regularly, with demand particularly high among millennials. Integrative clinics across key cities now employ herbalists alongside physicians, while online education platforms, including Herbal Academy and Chestnut School of Herbal Medicine, are professionalizing the field. Canada has begun recognizing herbal medicine under its complementary healthcare framework, giving practitioners greater legitimacy within provincial health systems.

Competitive Landscape

The global herbalist and herbal practitioner market is highly diverse and fragmented, comprising small-scale local herbalists, naturopathic doctors, and large integrative health centers.

While individual practitioners dominate local markets by delivering personalized care and traditional expertise, established Ayurvedic and Traditional Chinese Medicine (TCM) institutions are gaining global visibility through branded clinics and wellness chains. Large corporations are also entering the market through mergers and partnerships.

Business Strategies

Digital transformation has introduced new layers of competition in the herbalist and herbal practitioner market. Several practitioners have moved online through telehealth platforms, enabling remote consultations and prescription services.

This shift became more pronounced post-COVID-19, with herbal consultations now integrated into large telemedicine platforms in the U.S., Europe, and Asia. For example, Herbal Medicine Academy and Herb Rally now provide practitioner-led online consultations and virtual herbal training programs.

Key Industry Developments

- In April 2025, Nyarkotey College of Holistic Medicine and Technology, in collaboration with the Vanuatu Trade Commission Ghana, announced a new curriculum through a Massive Open Online Course (MOOC) platform. The partnership aims to train one million practitioners in herbal medicine and naturopathy through fully funded scholarships.

- In March 2025, Chief Minister Devendra Fadnavis and Union Minister Nitin Gadkari inaugurated the Patanjali Food and Herbal Park in Nagpur. The collaboration between Patanjali and the government aims to ensure sustainable development and economic upliftment.

Companies Covered in Herbalist and Herbal Practitioner Market

- The Ayurvedic Clinic

- Chopra Global

- Shang Han Tang Traditional Chinese Medicine Clinic

- Ayushakti Ayurved Health Center

- Balance Point Natural Medicine

- Banyan Botanicals Wellness

- Eu Yan Sang International

- Kottakkal Arya Vaidya Sala

- Pukka Herbs Wellness Partnerships

- Modern Herbal Medicine Clinic

Frequently Asked Questions

The herbalist and herbal practitioner market is projected to reach US$30.2 Billion in 2025.

Expansion of accredited herbal medicine education and increasing integration of herbal therapy are the key market drivers.

The herbalist and herbal practitioner market is poised to witness a CAGR of 10.6% from 2025 to 2032.

Increased adoption of herbal care in wellness tourism and collaboration with pharmaceutical companies are the key market opportunities.

The Ayurvedic Clinic, Chopra Global, and Shang Han Tang Traditional Chinese Medicine Clinic are a few key market players.