- Automation & Robotics

- Glass Testing Equipment Market

Glass Testing Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Glass Testing Equipment Market by Product Type (Measurement Gauges, Stress Viewers, Coating Detectors, Analysis Accessories, Mechanical Testing Equipment, Optical & Thermal Testing Systems, Chemical Resistance Testing Equipment), Testing Method (Non Destructive Testing (NDT), Destructive Testing, IoT enabled Testing Systems, Semi automated Testing Systems), End-User (Automotive, Construction & Building Materials, Consumer Electronics, Glass Manufacturers & Fabricators, Packaging Industry, Testing Laboratories & Research Institutions), and Regional Analysis for 2026 - 2033

Glass Testing Equipment Market Share and Trends Analysis

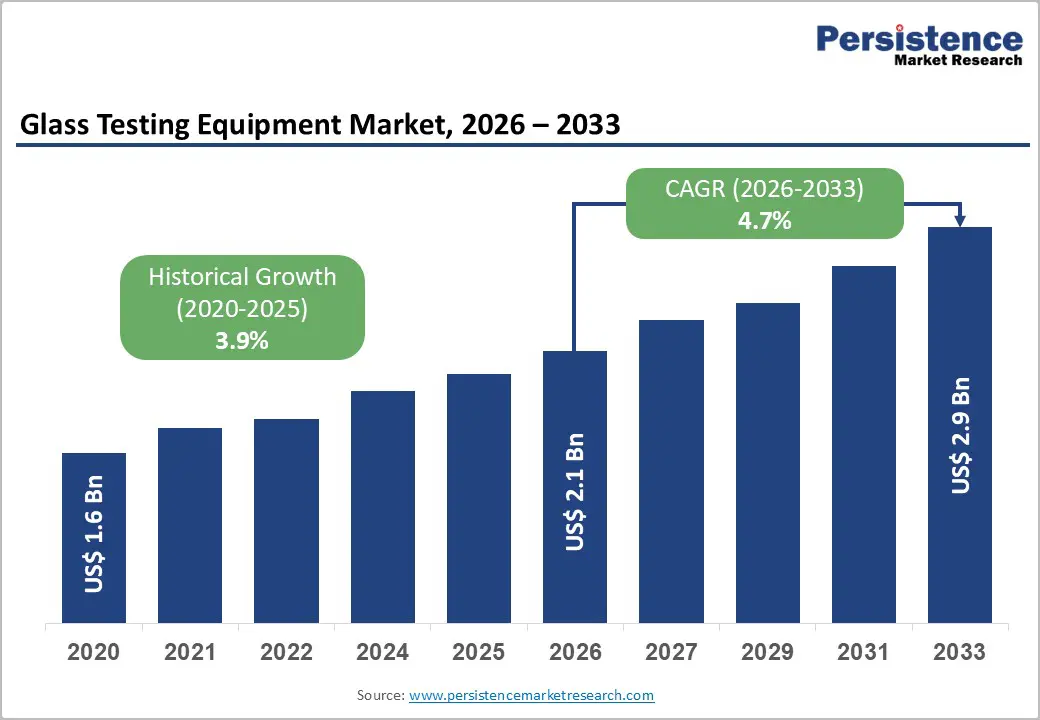

The global glass testing equipment market size is likely to be valued at US$ 2.1 billion in 2026, and is projected to reach US$ 2.9 billion by 2033, growing at a CAGR of 4.7% during the forecast period 2026−2033. Rising demand for quality assurance in glass production drives growth, as manufacturers seek to meet regulatory standards and consumer expectations for safety and durability.

Technological integration in testing equipment enhances accuracy and efficiency, supporting adoption across industrial and laboratory settings. Urbanization and construction expansion stimulate the need for glass validation, particularly in commercial infrastructure projects. Automotive industry adoption of high-performance glass necessitates precise testing, ensuring compliance with safety and optical standards. Emerging digital testing solutions enable predictive maintenance and data analytics, improving operational outcomes. Healthcare and consumer electronics applications generate secondary demand, as transparent materials require rigorous quality assessment.

Key Industry Highlights

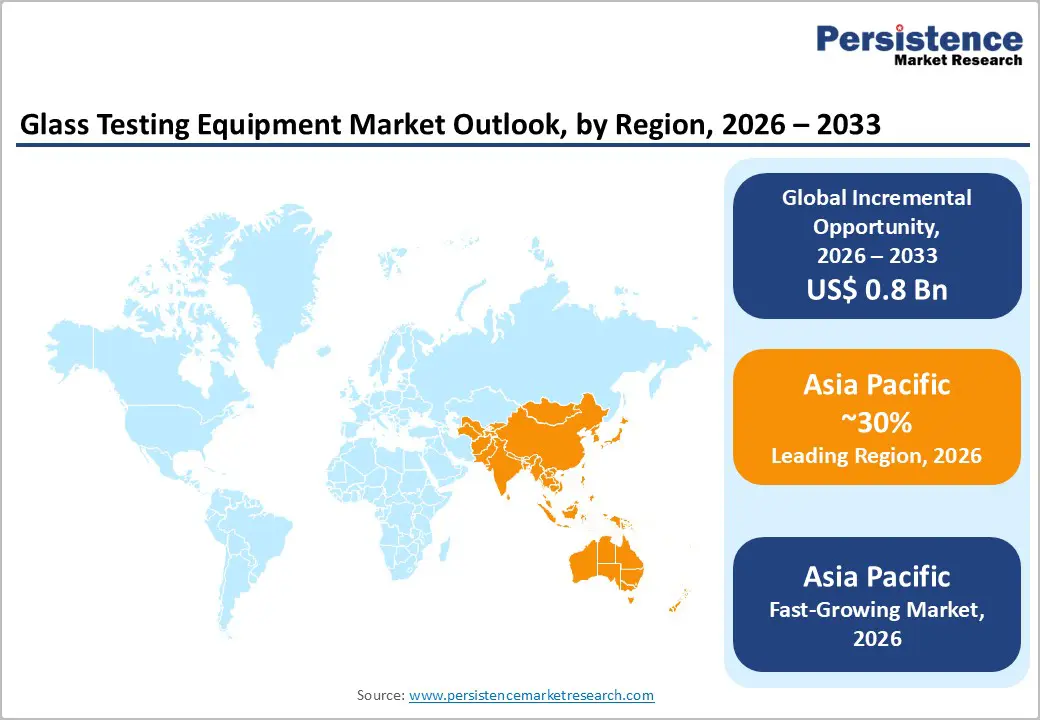

- Dominant Region: Asia Pacific is projected to capture roughly 30% of the market share by 2026, driven by large manufacturing hubs and improving government support.

- Fastest-growing Market: The Asia Pacific market is forecasted to record the fastest growth between 2026 and 2033, fueled by strengthening regulatory compliance.

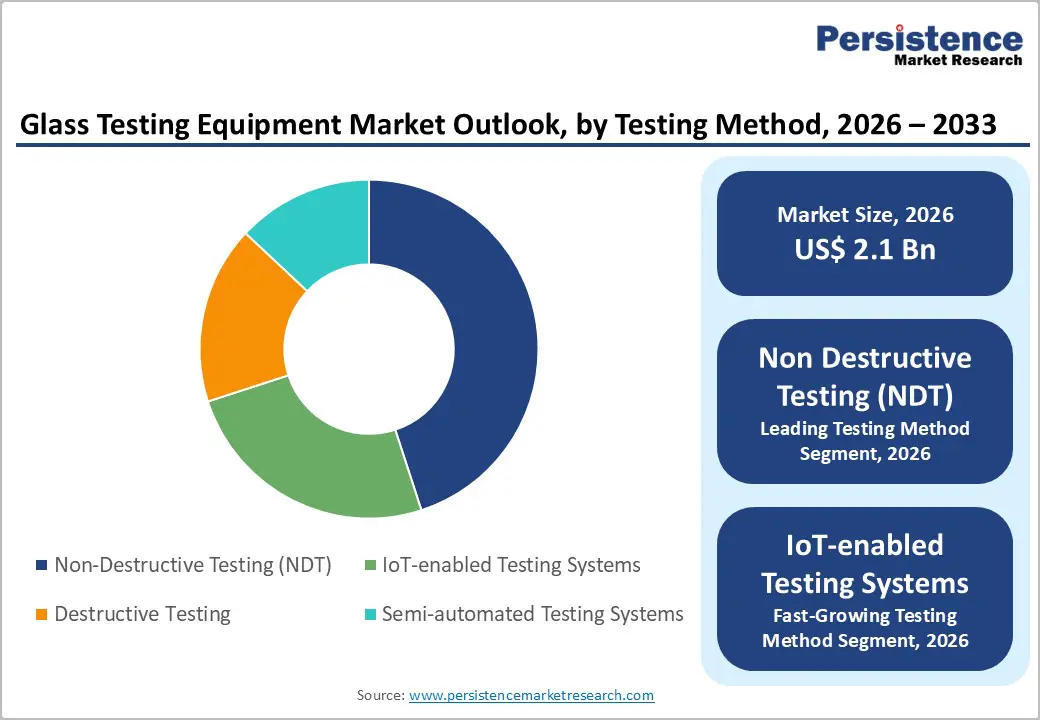

- Leading Testing Method: Non-destructive testing (NDT) is set to hold around 45% revenue share in 2026, supported by material integrity checks, compliance, and portable on-site use.

- Fastest-growing Testing Method: IoT-enabled testing systems are projected as the fastest-growing segment from 2026 to 2033, driven by real-time monitoring and smart manufacturing.

| Key Insights | Details |

|---|---|

|

Glass Testing Equipment Market Size (2026E) |

US$ 2.1 Bn |

|

Market Value Forecast (2033F) |

US$ 2.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancements in Testing Equipment

Technological advancements in testing equipment fundamentally shift how manufacturers ensure product quality and compliance with regulatory standards, driving higher precision and operational agility. The U.S. government identifies advanced digital systems, sensors, connectivity, and automation as core components of modern manufacturing transformation that improve efficiency and quality in industrial operations. For instance, the National Institute of Standards and Technology (NIST) reports that in 2025 it plans to award up to $70 million for an institute focused on artificial intelligence (AI) to increase resilience in manufacturing processes, highlighting federal prioritization of technology-enabled quality and performance improvements.

Investments in advanced testing technologies also align with broader government initiatives to modernize industrial ecosystems and maintain competitiveness in a global market landscape. Government programs emphasize digital tools and standards that help manufacturers comply with increasingly stringent safety, environmental, and performance regulations efficiently. By embedding technology into testing workflows, firms gain faster certification cycles and actionable insights that support continuous improvement and risk mitigation. This shift enables enterprises to adapt to evolving regulatory frameworks and market expectations without significant delays in production or release schedules.

Industrial and Infrastructure Expansion

Rapid expansion in manufacturing facilities and public infrastructure drives demand for equipment that ensures materials meet performance and safety benchmarks. Large-scale construction of industrial plants, logistics hubs, energy facilities, and transportation corridors requires stringent quality assurance during fabrication and installation. Testing equipment for structural, thermal, and impact properties becomes indispensable as project specifications tighten and regulatory compliance requirements escalate. Government-led capital deployment in transportation and utilities directly increases project volume, compelling contractors and fabricators to invest in precise assessment tools to verify adherence to standards throughout construction lifecycles.

Federal initiatives promoting infrastructure modernization illustrate the scale of this trend. Funding allocated for roads, bridges, railways, energy networks, and public facilities translates into substantial construction activity across multiple sectors. Elevated investment levels accelerate industrial and civil works, expanding the base of projects requiring validated performance testing of glass and other materials. Increased construction output drives firms to adopt specialized testing solutions to mitigate risk, ensure regulatory compliance, and support long-term asset integrity in an environment shaped by sustained industrial and infrastructure development.

High Capital Investment Requirements

Capital intensity remains a primary restraint due to technology platforms for material evaluation and performance validation demand advanced mechanical and analytical systems that require large upfront expenditure. These systems integrate precision sensors, automation, environmental chambers, and digital controls to meet regulatory and quality assurance benchmarks, inflating acquisition costs versus simpler inspection tools. Federal financial regulations acknowledge that special-purpose equipment generally requires significant approval for capital expenditure classification when unit costs exceed US$ 10000, underscoring that high-end laboratory and industrial apparatus are treated as major investments for institutions and enterprises alike.

Investors and operators face extended payback periods as complex testing systems often serve niche applications and have slow utilization rates in early operational stages. Advanced machines also entail ancillary infrastructure costs such as dedicated power supplies, vibration isolation, controlled environments, and skilled technicians for setup and calibration, cumulatively elevating total cost of ownership. For example, mid-to-upper tier analytical and specialty testing instruments in general laboratory classifications can range from tens of thousands to several hundred thousand U.S. dollars per unit in 2025, reflecting broader cost escalation trends in precision equipment procurement.

Regulatory Complexity and Compliance Challenges

Stringent regulatory frameworks require manufacturers and suppliers to secure multiple conformity assessments and certifications before products can be legally sold or tendered for use in end-applications. In India, for instance, the national standards body mandates compulsory certification under Quality Control Orders for many categories of laboratory glassware used in analytical and industrial testing, forcing entities to obtain licenses and affix a recognized conformity mark to demonstrate compliance with published Indian Standards. The number of products subject to mandatory certification has expanded sharply in recent years, rising from 106 products under 14 quality control orders to 773 products under 191 quality control orders by October 2025, signifying expanded regulatory oversight across industries.

Operational units are often obliged to invest in accredited testing facilities or engage third-party laboratories, align internal quality systems with specified criteria and navigate evolving compliance timelines. Authorities may impose sanctions or disqualification from public procurement if certifications are not secured, while different markets impose distinct conformity schemes with varying documentation and laboratory accreditation requirements. In addition, overlapping international and domestic standards add complexity for organizations exporting products, necessitating reconciliation of multiple regulatory regimes to ensure acceptance in different jurisdictions.

Growing Construction Activities in Emerging Economies to Boost Glass Demand

Rapid urbanization and industrial expansion in emerging economies are fueling significant demand for construction materials, including glass, across residential, commercial, and infrastructure projects. Modern architectural trends emphasize large glass facades, curtain walls, and energy-efficient windows, requiring high-quality glass that meets stringent safety and durability standards. Manufacturers must ensure compliance with these standards to maintain structural integrity, reduce defect rates, and meet regulatory requirements. Glass testing equipment plays a critical role in assessing mechanical strength, thermal resistance, optical clarity, and chemical composition, enabling producers to deliver consistent performance while adhering to evolving building codes. Rising investment in smart cities and high-rise developments further intensifies the need for precise testing tools capable of supporting diverse glass types such as tempered, laminated, and low-emissivity variants.

Expansion of construction projects creates a demand for large-scale production of specialized glass, which increases reliance on advanced testing solutions to prevent material failures and optimize product performance. Equipment capable of automated inspections, digital measurements, and real-time quality monitoring allows manufacturers to maintain efficiency while minimizing wastage. The integration of architectural innovation with safety requirements elevates the importance of rigorous testing across every production batch. Growing consumer preference for aesthetically appealing, durable, and energy-efficient glass enhances adoption of testing technologies that verify compliance with international quality standards.

Widening Non-Destructive Testing Adoption

Stringent inspection protocols mandated by government and regulatory bodies drive demand for advanced testing processes that evaluate integrity of components without causing damage. Federal agencies such as the U.S. Federal Highway Administration (FHWA) operate dedicated Nondestructive Evaluation (NDE) Laboratories focused on developing and implementing nondestructive methods to assess conditions of infrastructure assets such as bridges, tunnels, and pavements, enabling continuous monitoring and reducing lifecycle costs of critical assets without impairing them at the point of inspection.

The application of nondestructive evaluation enhances quality assurance outcomes while reducing costs associated with product failure and rework. Adoption enables early identification of surface and subsurface defects in materials, including composites and glass, avoiding the need for destructive sampling and minimizing scrap rates. As industries such as energy, transportation, and manufacturing increase deployment of advanced materials and complex assemblies, testing without impairing the asset preserves operational readiness and extends service life of components subject to fatigue and environmental stress.

Category-wise Analysis

Product Type Insights

Measurement gauge is anticipated to secure around 30% of the glass testing equipment market revenue share in 2026, reflecting high adoption across industrial and laboratory settings. Precision measurement facilitates compliance with manufacturing and safety standards, making it essential for automotive, construction, and packaging applications. Ease of use, reliability, and consistent performance drive preference among manufacturers and testing facilities. Equipment integration with digital readouts and calibration systems enhances operational efficiency and accuracy. Accessibility of measurement gauges in both centralized and decentralized facilities supports broad adoption.

Optical & thermal testing systems are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by increasing demand for high-precision defect detection and temperature-resilient glass applications. Advanced optical systems enable detection of micro-cracks, stress patterns, and coating uniformity, supporting industrial quality compliance. Thermal testing ensures material stability under varying operational conditions, critical for automotive, aerospace, and electronics sectors. Growth is further supported by integration with IoT-enabled data analytics, providing real-time monitoring and predictive insights.

Testing Method Insights

NDT extracts are poised to dominate with a forecasted market share of over 45% in 2026, powered by ability to assess material integrity without compromising usability. NDT adoption supports compliance with regulatory standards while maintaining production throughput. Techniques such as ultrasonic testing, eddy current analysis, and optical inspection enable rapid evaluation, reducing operational downtime. Consumer trust in validated products and regulatory endorsement for safety-critical applications enhance acceptance. Availability of portable NDT instruments supports deployment in decentralized and on-site testing environments, facilitating widespread use in automotive, construction, and electronics sectors.

IoT-Enabled testing systems are estimated to be the fastest-growing segment from 2026 to 2033, fueled by digital integration for real-time monitoring, predictive analytics, and remote diagnostics. Adoption enables manufacturers to optimize quality control processes, reduce defect rates, and ensure compliance with dynamic regulatory standards. Connectivity with enterprise systems supports operational insights, driving efficiency and cost savings. Expansion of digital infrastructure and demand for smart manufacturing solutions accelerates deployment in automotive, electronics, and industrial glass applications. Growth is supported by scalable adoption in both centralized laboratories and on-site production facilities, offering a competitive advantage for early adopters.

Regional Insights

North America Glass Testing Equipment Market Trends

North America accounts for a significant share of the glass testing equipment market, driven by a mature industrial base and stringent regulatory frameworks across construction, automotive, and electronics sectors. High standards for safety, durability, and performance create sustained demand for advanced testing solutions, including automated impact testers, optical measurement systems, and environmental simulation equipment. Industrial facilities increasingly integrate testing apparatus into production lines to ensure compliance with national and international standards, reducing risk of product failures and liability costs. Strong presence of key manufacturers and technology providers enables rapid adoption of innovative testing methodologies, including digital sensor networks and real-time data analytics. Capital investment toward process optimization and quality assurance further strengthens market penetration, while collaboration between manufacturers and certification bodies supports standardization of testing procedures.

Integration of predictive analytics and automated inspection systems allows manufacturers to detect defects early, improving production efficiency and reducing waste. Expansion of niche applications, such as energy-efficient glazing and reinforced safety glass, drives incremental investment in equipment capable of precise characterization and multi-parameter testing. Government initiatives promoting sustainable construction and industrial innovation encourage adoption of environmentally friendly and energy-efficient testing solutions. Strategic partnerships and continuous product refinement create opportunities for differentiation, supporting long-term growth while addressing evolving quality requirements and maintaining alignment with international market expectations.

Europe Glass Testing Equipment Market Trends

The market for glass testing equipment in Europe is characterized by mature industrial infrastructure and stringent regulatory standards. Demand is concentrated in sectors requiring high precision, including automotive glazing, construction materials, and electronics displays. Emphasis on product safety, durability, and performance drives adoption of automated testing systems and non-destructive evaluation methods. Investment in research and development enables equipment providers to introduce solutions capable of handling complex material properties, such as multi-layered glass and energy-efficient panels. Skilled workforce and technical expertise facilitate effective deployment of advanced systems, minimizing downtime and improving production efficiency. Regulatory frameworks mandate thorough verification of glass performance across applications, reinforcing the need for reliable testing solutions and consistent quality monitoring.

Advanced glazing for architectural and electronic applications requires high-precision evaluation, encouraging implementation of real-time analytics and integrated digital inspection tools. Expansion of mid-sized manufacturers upgrading production lines generates incremental demand for versatile testing equipment. Collaborative initiatives between equipment suppliers and manufacturers support innovation tailored to evolving product requirements, including specialized solutions for performance-critical applications. As material compositions and product specifications advance, investment in adaptive and precise testing platforms continues to rise.

Asia Pacific Glass Testing Equipment Market Trends

Asia Pacific is expected to lead with an estimated 30% of the glass testing equipment market share by 2026, reflecting the concentration of high-volume manufacturing clusters in automotive, electronics, and architectural glass sectors. Demand for rigorous mechanical, thermal, and optical testing is amplified by adoption of advanced laminated and tempered glass, which requires precise calibration of equipment for safety and performance validation. Integration of local fabrication and supply networks enables manufacturers to embed testing solutions directly into production workflows, minimizing downtime and improving throughput. Government programs encouraging industrial modernization and technology adoption have accelerated deployment of automated and high-throughput testing systems. Competitive manufacturing costs and growing domestic procurement of capital equipment create favorable conditions for scaling testing operations efficiently.

Asia Pacific is forecasted to be the fastest-growing market for glass testing equipment between 2026 and 2033, stimulated by expansion of next-generation glass applications that demand complex evaluation protocols. High-performance glazing for energy-efficient buildings and advanced display panels introduces material and structural complexities, requiring digital sensing and real-time analytical testing systems. Industrial modernization initiatives are driving adoption of predictive quality control, while emerging manufacturers upgrading production capabilities generate incremental demand for versatile testing solutions. Increasing regulatory alignment with international standards further reinforces investment in automated equipment to ensure compliance and maintain export competitiveness.

Competitive Landscape

The global glass testing equipment market landscape is characterized by moderate fragmentation, with a mix of established multinational corporations and specialized regional suppliers. Key players, including Instron, Presto Testing Equipment, Ceralabel-Green, Merlin Laser, Glass Technology Services Ltd., and ZwickRoell, compete by leveraging technological differentiation, advanced testing capabilities, and comprehensive service offerings. Adoption of automated and high-throughput testing solutions is increasing as manufacturers seek to enhance quality assurance across automotive, construction, and electronics segments. Integration of digital monitoring, real-time data analytics, and precision measurement systems enables faster defect detection and operational efficiency. Strategic collaborations between equipment providers and industrial clients allow tailored solutions that align with production requirements, safety standards, and regulatory compliance frameworks.

Market dynamics are further shaped by evolving regulatory standards and rising demand for high-performance and specialty glass products, which require sophisticated testing protocols. Players such as Instron and ZwickRoell focus on precision and automation, while Presto Testing Equipment and Ceralabel-Green emphasize cost-efficient solutions for mid-tier manufacturers. Merlin Laser and Glass Technology Services Ltd. provide niche capabilities, including laser-based inspection and customized testing services, broadening accessibility to advanced quality control technologies. The combination of innovation, service differentiation, and regional customization underpins resilience in a moderately fragmented environment.

Key Industry Developments

- In March 2026, Northern Glass Solutions opened a US$ 21 million advanced manufacturing facility in East Arm, Darwin, to produce specialty glass products locally and strengthen Northern Territory supply chains. The plant will manufacture high-performance glass such as laminated, cyclone-resistant, and bullet-resistant variants.

- In February 2025, Toray Engineering announced the launch of a large glass substrate inspection system featuring an industry-first double-sided and internal defect detection designed to support advanced semiconductor packaging.

Companies Covered in Glass Testing Equipment Market

- Instron

- Presto Testing Equipment

- Ceralabel-Green

- Merlin Laser

- Glass Technology Services Ltd.

- ZwickRoell

- GSR Laser Tools

- Arg International

- Duran Group

- Laser Tools

- Canned Instrument Ltd.

Frequently Asked Questions

The global glass testing equipment market is projected to reach US$ 2.1 billion in 2026.

Strengthening demand for high-quality, durable, and safety-compliant glass across automotive, construction, and electronics sectors is driving the market.

The market is poised to witness a CAGR of 4.7% from 2026 to 2033.

Expansion of next-generation glass applications, adoption of automated and digital testing solutions, and growth in emerging industrial hubs present key market opportunities.

Some of the key market players include Instron, Presto Testing Equipment, Ceralabel-Green, Merlin Laser, Glass Technology Services Ltd., and ZwickRoell.