- Pharmaceuticals

- Antifungal Drugs Market

Antifungal Drugs Market Size, Share, and Growth Forecast, 2025 - 2032

Antifungal Drugs Market By Drug Class (Azoles, Echinocandins, Polyenes, Allylamines, Others), Indication (Candidiasis, Aspergillosis, Dermatophytosis, Mucormycosis, Others), Route of Administration (Oral, Topical, Injectable, Others), and Regional Analysis for 2025 - 2032

Antifungal Drugs Market Share and Trends Analysis

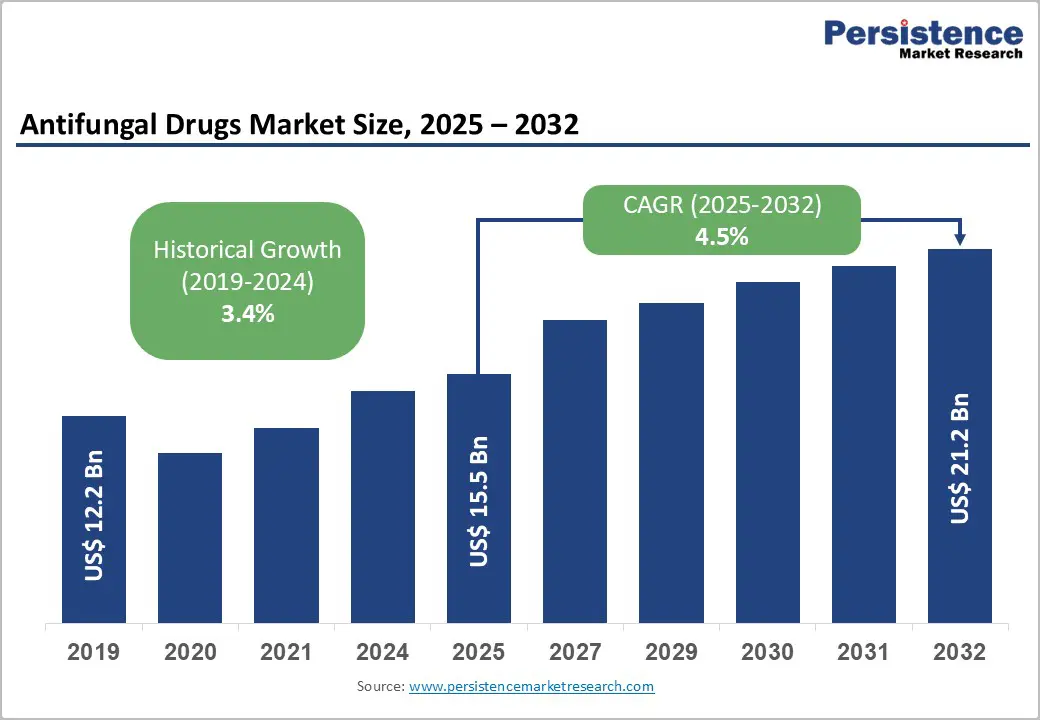

The global antifungal drugs market size is likely to be valued at US$15.5 Billion in 2025, and is estimated to reach US$21.2 Billion by 2032, growing at a CAGR of 4.5% during the forecast period 2025 - 2032, driven by an increasing prevalence of fungal infections worldwide, a growing geriatric and immunocompromised patient population, and technological advances in diagnostics and drug formulations.

In terms of diseases, invasive fungal infections such as candidiasis and aspergillosis are significantly contributing to the demand for effective antifungal therapies. Emerging novel antifungal agents with improved safety profiles are expanding treatment options, fueling market growth.

Key Industry Highlights

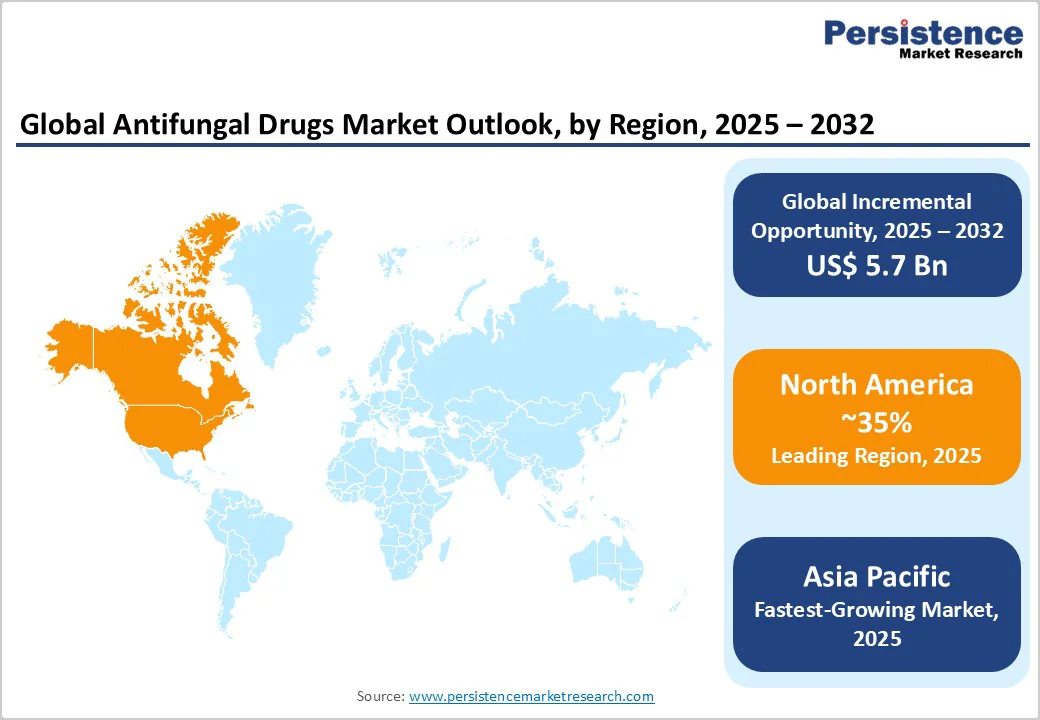

- Regional Dynamics: North America is set to dominate with a 35% share in 2025, Europe is likely to hold 30%, and Asia Pacific is set to be the fastest-growing regional market through 2032.

- Dominant & Fastest-growing Drug Classes: The azoles segment is poised to lead with a 48.2% revenue share in 2025, while echinocandins are slated to exhibit the fastest growth from 2025 to 2032.

- Leading & Fastest-growing Indications: Candidiasis is anticipated to remain the primary indication with over 35% market share in 2025, whereas aspergillosis is expected to grow the fastest during 2025-2032.

- Leading Route of Administration: Oral route is predicted to command approximately 46% market share in 2025, but topical antifungals are likely to grow the fastest.

- Key Trend: Regulatory incentives in North America and Europe are accelerating novel antifungal drug approvals and clinical development.

- Investment Opportunity: Combination antifungal therapies are an emerging growth opportunity, projected to exceed US$3 Billion by 2032 with a high CAGR.

- Competitive Developments: Recent key developments cover critical trial resumptions, collaborations among large pharmaceutical giants for drug formulations, and timely FDA approvals between 2024 and 2025.

- August 2025: Glenmark Pharmaceuticals announced plans to launch the antifungal drug Micafungin, a therapeutic equivalent to Astellas Pharma's Mycamine, in the U.S. market starting September 2025, to be available in single-dose vials, and is expected to expand Glenmark’s institutional channel portfolio.

| Key Insights | Details |

|---|---|

| Antifungal Drugs Market Size (2025E) | US$15.5 Bn |

| Market Value Forecast (2032F) | US$21.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of the Immunocompromised Population to Fuel Market Growth

The relentless increase in immunocompromised individuals, including those undergoing cancer chemotherapy, organ transplantation, and living with autoimmune diseases, constitutes a critical driver for the antifungal drugs market growth.

This is a mounting concern across the healthcare community, as advances in medical treatments that prolong life have increased the susceptibility to fungal infections. For instance, oncology patients are seeing a growing incidence of invasive fungal infections, with candidiasis and aspergillosis rates rising annually as well.

Governments and health agencies, such as the U.S. Centers for Disease Control and Prevention (CDC) and the World Health Organization (WHO), report that these infections drastically increase morbidity and mortality among this vulnerable group, intensifying the urgency for effective antifungal therapies.

Consequently, pharmaceutical companies are channeling research investments into developing targeted antifungal formulations with enhanced efficacy and fewer side effects.

Regulatory Hurdles in Drug Approval for Novel Antifungals

One formidable market restraint arises from stringent regulatory frameworks governing antifungal drug approvals, which can impede timely market entry for novel therapeutics. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) require extensive clinical trials demonstrating both safety and efficacy, given the potential toxicity and adverse effects associated with antifungal agents.

For example, drugs such as echinocandins and polyenes face prolonged approval processes due to concerns over liver and kidney toxicity, limiting swift commercialization. Furthermore, regulatory demands for combination therapies and novel drug classes to address resistance add complexity and cost, creating barriers particularly for smaller companies and emerging markets.

Delays in approvals and post-market surveillance obligations increase development costs, which translate into higher treatment prices and limited accessibility, especially in low- and middle-income countries where fungal infections are prevalent.

Rising Adoption of Combination Antifungal Therapies

The growing clinical adoption of combination antifungal therapies represents a high-potential market opportunity with significant revenue upside. Combination therapies, such as pairing echinocandins with azoles, are being increasingly employed to enhance treatment efficacy, reduce resistance development, and improve patient outcomes for invasive fungal infections.

Clinical trials evidence shows such combinations can lower mortality rates significantly, compared to monotherapies, appealing to healthcare providers managing complex cases. This opportunity is bolstered by growing diagnostic awareness and earlier infection detection, which support more aggressive treatment protocols using combinations.

From an investment perspective, companies able to innovate in this space stand to capture unmet medical needs and gain a competitive advantage in antifungal therapeutics.

Category-wise Analysis

Drug Class Insights

The azoles segment is expected to emerge as the market leader, capturing an estimated 48.2% of antifungal drugs market revenue share in 2025, reflecting its extensive clinical applications across various fungal infections due to the broad-spectrum efficacy, oral bioavailability, and established safety profiles.

Common azoles such as fluconazole and itraconazole dominate the systemic and superficial antifungal treatment landscapes, supported by well-established generic versions facilitating widespread use. This dominance is also backed by continuous clinical guideline endorsements and high physician preference globally.

Echinocandins are anticipated to witness the highest growth trajectory from 2025 to 2032. This is primarily driven by their targeted mode of action against Candida and Aspergillus species, particularly in systemic infections resistant to other classes.

The growing prevalence of invasive fungal infections in immunocompromised populations underpins this accelerated uptake, as echinocandins offer enhanced efficacy coupled with reduced toxicity compared to polyenes. Segmental expansion is further propelled by novel drug formulations and increased inclusion in treatment protocols.

Indication Insights

Candidiasis is poised to command an estimated 35% of the market share in 2025, primarily due to its high global prevalence across mucosal, cutaneous, and systemic clinical manifestations.

The dominance of this condition is bolstered by its frequent association with immunocompromised and critically ill patient groups, resulting in robust demand for both prophylactic and therapeutic antifungal regimens. Improving patient awareness regarding fungal infections and the widespread clinical adoption of antifungal prophylaxis regimens will contribute to sustained market revenue.

Aspergillosis, although currently smaller in share, is set to be the fastest-growing indication during 2025 - 2032. This growth is fueled by increasing stem cell and organ transplantation, prolonged ICU care, and a rise in corticosteroid therapies, which elevate invasive aspergillosis risk.

Advances in diagnostic approaches, such as galactomannan antigen testing, have improved early detection, enabling timely treatment initiation and further accelerating market growth. Pharmaceutical pipelines targeting aspergillosis-specific antifungals and emerging combination therapies are expected to enhance therapeutic outcomes, rendering this indication strategically significant for future market expansion.

Route of Administration Insights

Oral administration is likely to maintain a leading market share, projected at 46% in 2025, attributable to its systemic effectiveness, ease of administration, and enhanced patient adherence, especially for long-term treatment or prophylaxis. Oral antifungal formulations, primarily azoles and allylamines, dominate outpatient care and chronic infection management.

The topical route segment is anticipated to exhibit the fastest growth between 2025 and 2032. This surge is driven by an increase in superficial fungal infections treated with over-the-counter (OTC) antifungal products such as creams, powders, and ointments. Innovations in formulation technologies, improving drug penetration, and reducing skin irritation have expanded topical usage across demographics.

Regional Insights

North America Antifungal Drugs Market Trends

North America is slated to occupy the dominant position in 2025 with an estimated 35% of the antifungal drugs market share. This leadership is primarily attributable to the U.S., which boasts a highly developed healthcare infrastructure, widespread disease awareness, and early adoption of advanced antifungal therapies.

The U.S. regulatory environment, characterized by efficient FDA approval pathways such as priority reviews and breakthrough therapy designations, fosters innovation and accelerates time-to-market for novel antifungal drugs. The high prevalence of immunocompromised populations, including cancer patients, organ transplant recipients, and HIV/AIDS patients, is also sustaining the demand for antifungal drugs.

The North America market also benefits from a robust pharmaceutical R&D ecosystem with significant investments in pipeline antifungal agents and diagnostics. Competitive landscape dynamics here show major multinational companies with concentrated market shares while investing in technology partnerships and acquisitions to expand therapeutic offerings.

Investment trends point towards increased funding for next-generation antifungals and diagnostics, indicating steady market expansion potential into the 2032 horizon.

Europe Antifungal Drugs Market Trends

Europe is estimated to command around 30% of the global market by 2025. Its substantial share arises from key countries such as Germany, the U.K., France, and Spain, which have high healthcare expenditure and centralized regulatory agencies such as the EMA, facilitating harmonized approvals across member states.

The EMA's regulatory framework supports streamlined market access while maintaining rigorous safety and efficacy standards, critical for antifungal therapies with potential toxicity concerns. Growing fungal infection awareness, proactive governmental healthcare policies, and initiatives aimed at combating antifungal resistance significantly contribute to stable market growth.

Market competition is moderately consolidated with leading pharmaceutical companies holding significant shares, complemented by a surge of biotech startups focusing on innovation and niche fungal diseases. Europe’s investment landscape highlights strategic partnerships and funding allocated towards antifungal resistance management programs and precision medicine approaches, underlining the region’s commitment to long-term market development.

Asia Pacific Antifungal Drugs Market Trends

Asia Pacific stands as the fastest-growing regional market, expected to register a robust CAGR through 2032. This rapid growth is propelled by expanding healthcare infrastructure, rising prevalence of fungal infections exacerbated by tropical climatic conditions, and a swelling middle class with improved access to healthcare services.

China, India, Japan, and ASEAN nations present diverse growth drivers, including increasing immunocompromised populations due to rising cancer and diabetes incidence, localized manufacturing capabilities, and ongoing regulatory reforms aimed at accelerating drug approvals.

Asia Pacific’s already strong and growing pharmaceutical manufacturing base offers cost advantages and is attracting global partnerships for generic as well as novel antifungal drugs. Furthermore, government initiatives focused on healthcare accessibility and antifungal disease awareness campaigns are enhancing market penetration.

The competitive environment here is becoming more dynamic with both multinational pharmaceutical corporations and indigenous companies investing heavily in R&D, production scale-up, and market expansion strategies, positioning the region as a strategic priority for antifungal market stakeholders.

Competitive Landscape

The global antifungal drugs market structure is moderately consolidated, with the top pharmaceutical companies collectively controlling approximately 68% of the total share. These industry leaders include Bayer AG, GlaxoSmithKline Plc, Merck & Co., Inc., Pfizer Inc., and Sanofi S.A., each leveraging extensive product portfolios, strong brand recognition, and widespread geographic presence.

The market also includes significant contributions from generic drug manufacturers such as Glenmark Pharmaceuticals and Alembic Pharmaceuticals Limited, intensifying competition and driving price sensitivity.

The competitive landscape is characterized by continuous innovation, patent expirations, and active mergers and acquisitions, shaping market dynamics and competitive positioning.

Aggressive R&D investments aim at developing novel antifungal agents with improved efficacy and safety, fortified by strategic alliances fostering technology sharing and co-development. Market participants are increasingly focusing on expanding presence in emerging markets through partnerships and licensing agreements to capture growth potential beyond mature regions.

Key Industry Developments

- In October 2025, the University of Exeter launched the £2.8 Million (US$3.4 Million) FAILSAFE project, uniting 135 global researchers to combat antifungal resistance by advancing drugs, vaccines, diagnostics, and surveillance, prioritizing equitable, impactful solutions for vulnerable low- and middle-income countries.

- In August 2025, Optics and Photonics Research Center scientists improved antifungal therapy against Candida albicans by combining blue light-activated curcumin with amphotericin B, markedly reducing drug-resistant biofilm growth and offering a promising alternative to combat fungal resistance in medical and food safety applications.

- In May 2025, Brown University researchers created a penetratin-tagged liposomal nanodelivery system enhancing antifungal efficacy against Candida species, enabling lower-dose treatment, preventing biofilm formation, and showing no human cell toxicity, reducing fungal burden by 60% in mice versus conventional therapies.

Companies Covered in Antifungal Drugs Market

- Bayer AG

- GlaxoSmithKline Plc

- Merck & Co., Inc.

- Pfizer Inc.

- Sanofi S.A.

- Glenmark Pharmaceuticals Limited

- Alembic Pharmaceuticals Limited

- SCYNEXIS, Inc.

- Biocon Limited

- Cipla Limited

- Abbott Laboratories

- Astellas Pharma, Inc.

- Gilead Sciences, Inc.

- Enzon Pharmaceuticals, Inc.

- F2G Ltd.

Frequently Asked Questions

The global antifungal drugs market is projected to reach US$15.5 Billion in 2025.

The increasing prevalence of fungal infections worldwide and a growing geriatric and immunocompromised patient population are driving the market.

The antifungal drugs market is poised to witness a CAGR of 4.5% from 2025 to 2032.

Technological advances in diagnostics and drug formulations, emerging novel antifungal agents with improved safety profiles that are expanding treatment options, and timely regulatory approvals to novel antifungal therapies are key market opportunities.

Bayer AG, GlaxoSmithKline Plc, and Merck & Co., Inc. are some of the key players in the antifungal drugs market.