- Transportation & Logistics

- Freight Trucking Market

Freight Trucking Market Size, Share, and Growth Forecast, 2025 - 2032

Freight Trucking Market By Truck Type (Dry Van & Box, Refrigerated, Others), End-user Industry (Retail & E-commerce, Industrial & Manufacturing, Others), Vehicle Size (Light-Duty Trucks (LDTs), Others), Cargo Type (Dry Goods, Perishables, Hazardous Materials), and Regional Analysis for 2025 - 2032

Freight Trucking Market Share and Trends Analysis

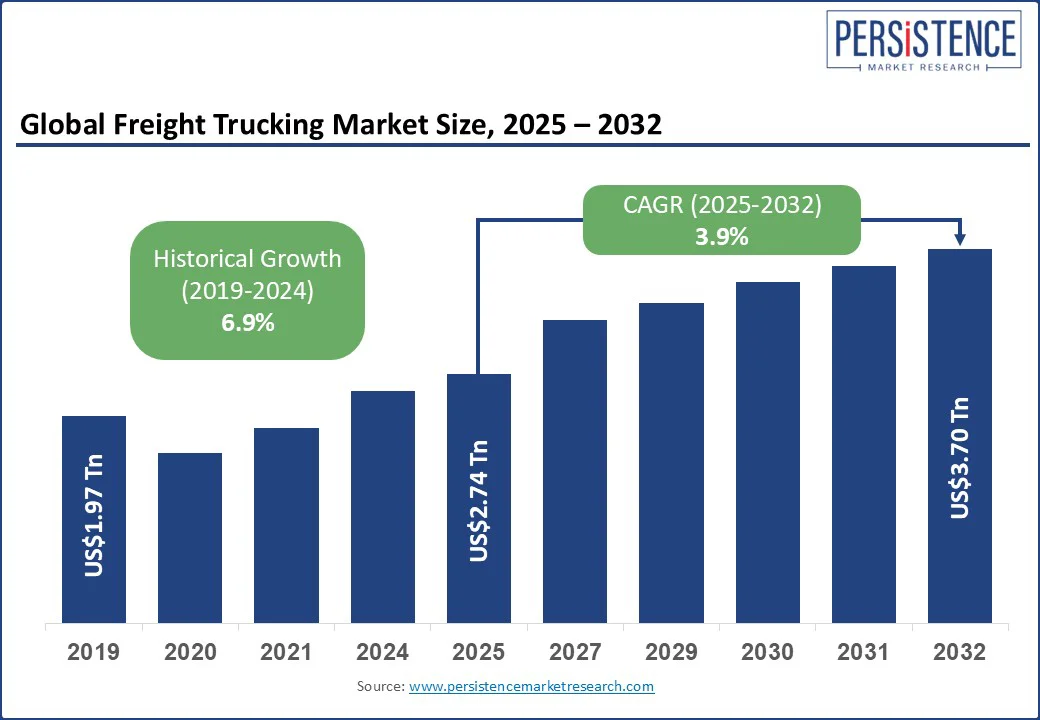

The global freight trucking market size is likely to be valued at US$2.74 Tn in 2025 and reach US$3.70 Tn by 2032, growing at a CAGR of 3.9% during the forecast period from 2025 to 2032. Rising fuel prices worldwide and stringent regulations to curb vehicular emissions are accelerating investments in electric and hydrogen-powered trucks, unlocking innovation opportunities and strengthening market prospects in the logistics sector. Freight trucking is the mainstay of the logistics & transport sector worldwide, helping move the majority of goods across regions and building resilient supply chains. With economies undergoing urbanization and e-commerce scaling rapidly, the freight transport industry is evolving to meet the growing demand for last-mile delivery, route optimization, and greener logistics operations.

New models are being developed to offset the intensifying driver shortages, particularly in developed nations, fueling interest in autonomous freight, digital freight platforms, and alternative powertrains. For instance, Aurora’s autonomous truck pilots in Texas and Uber Freight’s AI route planning are early signals of this shift toward tech-enabled, low-emission logistics.

Key Industry Highlights:

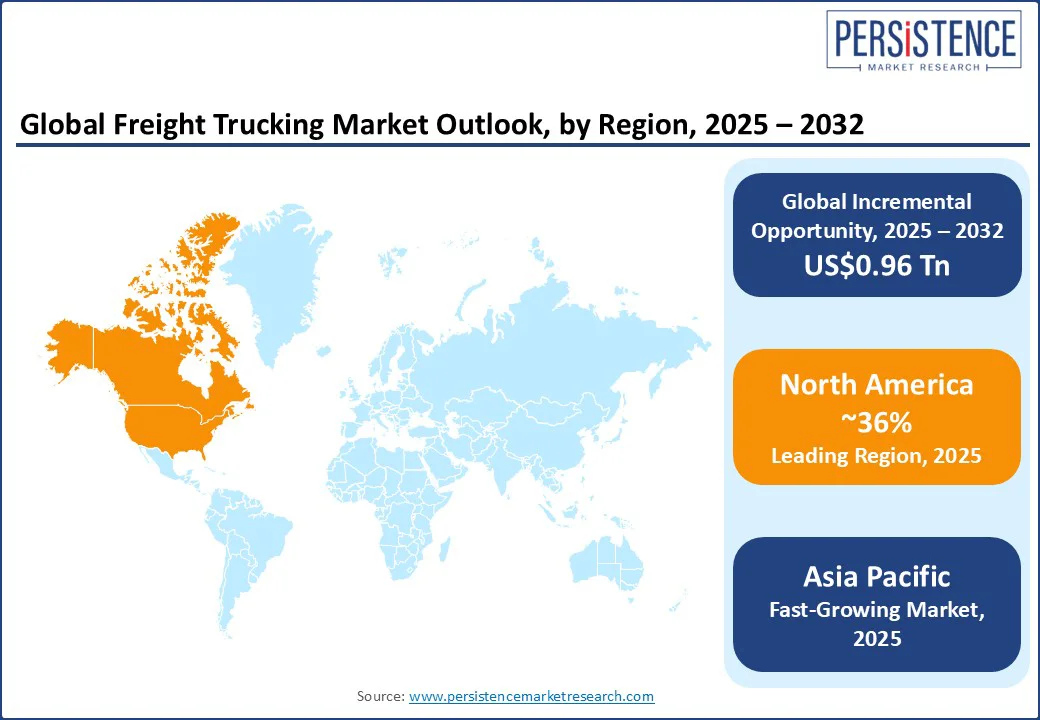

- Leading Region: North America, 36% market share in 2025, due to its highly integrated interstate logistics infrastructure, surging e-commerce volumes, and early adoption of advanced telematics and autonomous trucking technologies.

- Fastest-growing Region: Asia Pacific, driven by large-scale cross-border trade and robust e-commerce logistics in China and India.

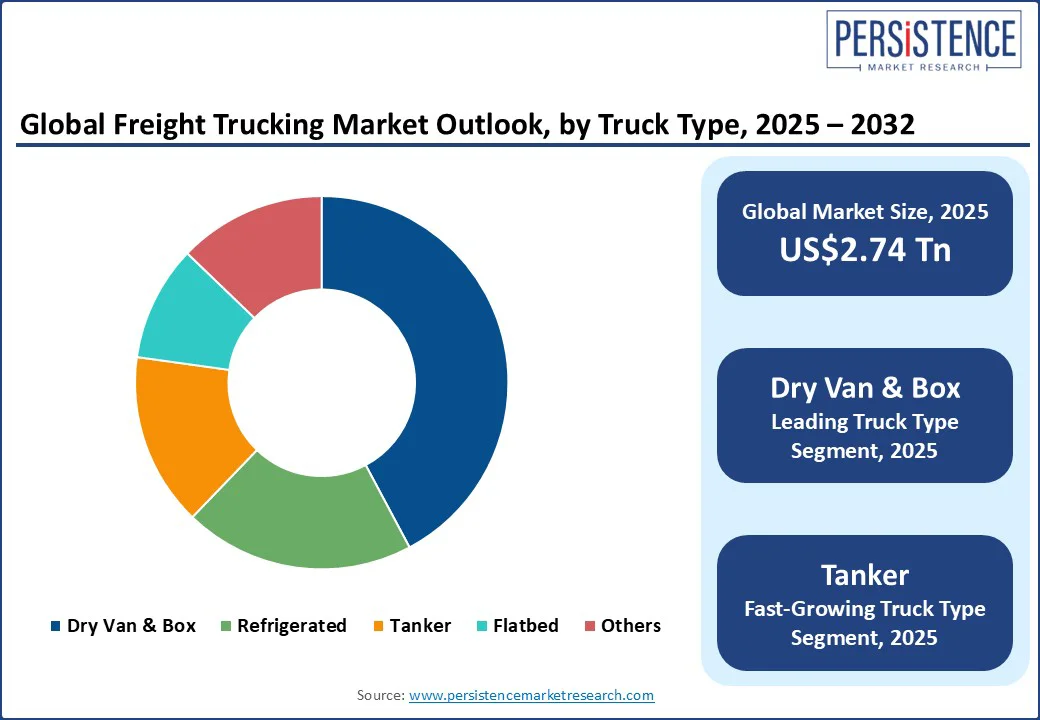

- Dominant Truck Type: Dry van & box trucks, nearly 44% share, reflecting their capacity and versatility for transporting consumer goods across long distances.

- Leading Application: Retail & e-commerce segment claims over 32.5% of the freight trucking market share on account of the soaring demand for last-mile delivery of goods and prolific expansion of omni-channel retail networks.

|

Global Market Attribute |

Key Insights |

|

Freight Trucking Market Size (2025E) |

US$2.74 Tn |

|

Market Value Forecast (2032F) |

US$3.70 Tn |

|

Projected Growth (CAGR 2025 to 2032) |

3.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.9% |

Market Dynamics

Driver - Fuel Price Fluctuations to Trigger Operational Innovation in Freight Trucking

The most critical driver for the freight trucking market is the fuel price volatility. Diesel accounts for around 15–30% of the total operating costs, making trucking companies acutely sensitive to fluctuations in crude oil prices. A 10% increase in diesel prices can result in a 6–7% hike in freight rates, a near proportional increase, illustrating the strong correlation between fuel costs and profitability in freight logistics. When oil prices spike due to geopolitical instability or supply shocks, smaller carriers without the necessary financial resources have their margins squeezed sharply, whereas larger fleets often absorb volatility through fuel surcharges or optimized purchasing strategies.

The erratic nature of fuel prices has triggered a wave of operational and technological innovation, such as the application of trailer skirts and rear fairings, to improve fuel efficiency and reduce emissions per trip. According to Michael Roeth, Executive Director of the North American Council for Freight Efficiency, trailer aerodynamics solutions can achieve fuel efficiency between 1% and 10%. Fleet operators are also deploying AI-powered route planning, load matching, and predictive maintenance tools to optimize fuel efficiency and reduce idling time and empty miles.

In June 2025, for example, ROSSMAN, a German drugstore chain, introduced an AI-powered route planning solution across its logistics network to enhance truck utilization and operational efficiency. The compounding effect of persistently high fuel prices is encouraging freight companies to pump investments in alternative fuel trucks, fleet electrification, and even hydrogen vehicles, especially with long-term transport economics increasingly favoring zero-emission models.

Restraint - Regulatory Complications Drain Profit Margins of Small Fleet Operators

The foremost issue hampering the freight trucking market expansion is complex regulations, which reduce efficiency and squeeze profits, especially for small operators. Fragmented regulations, ranging from EPA emissions mandates and state-wise labor rules to cross-border paperwork, have forced trucking companies to navigate costly administrative overheads. The intricate compliance ecosystem has considerably reduced asset utilization and scheduling flexibility, particularly for small- and medium-sized firms that lack the scale to absorb the added burden.

During periods of economic downturn, these complications become acute. In Australia, over 400 trucking firms went into voluntary administration in 2024–25 due to rising costs and regulatory pressures. In the U.S., when the federal government declared English the official language of the country in 2025, it increased the risk of disqualifying immigrant drivers. This has happened at a time when the driver pool is already fragile, further constraining capacity and inflating unit labor costs for freight trucking companies.

Opportunity - Concerted Movement Toward Zero-emission Freight Trucks to Produce Phenomenal Opportunities

The shift toward zero-emission vehicles (ZEVs) in the logistics & transport industry marks an inflection point that has the potential to unlock not only ESG-aligned logistics but also establish new profit centers in sustainable freight. Government mandates, industry decarbonization targets, and lower battery costs are driving the shift toward clean mobility in freight trucking. In India, the July 2025 debut of a domestically designed electric medium-haul truck, capable of cutting over 50 Tons of carbon dioxide emissions per year, testifies to how emerging economies are leapfrogging to electric freight and pioneering innovation in carbon-efficient transport, electric logistics, and green supply chain solutions.

Early adopters that integrate electric semi-trucks, battery-electric commercial vehicles, and hydrogen fuel-cell tractors into their fleet mix can accrue huge benefits from government incentives, lower total cost of ownership, and offer a variety of sustainable logistics services. Research from the International Council on Clean Transportation (ICCT) also shows that lifecycle costs of zero-emission trucks are converging with diesel trucks as battery and infrastructure costs decline, positioning electrified freight as both an opportunity for competitive differentiation and operational resilience.

Category-wise Analysis

Truck Type Insights

Dry van & box trucks are estimated to hold the largest revenue share at approximately 44.2% in 2025 within the truck type segment. These trucks play a crucial role in transporting non-perishable goods, particularly within retail, e-commerce, and manufacturing logistics, driven by the rapid expansion of e-commerce, just-in-time inventory strategies, and cost-efficient palletized shipping. Major carriers such as Knight-Swift and XPO have developed and maintained large dry-van fleets tailored to retail and manufacturing supply chains, as well as to support the high-volume demand for palletized goods transport and warehouse-to-retail distribution.

The tanker truck sub-segment is expected to register the highest CAGR through 2032, on account of the rapid expansion in liquid bulk transport, including oil, petrochemicals, and even hydrogen fuel logistics in emerging economies. Tanker trucks are widely used to support the extensive exploration, production, and distribution in the oil & gas sector, driven by global fossil fuel demand, growing liquid bulk logistics, and emerging hydrogen-capable tanker fleets for alternative energy transport. The soaring demand for these trucks is also evident in China, the UAE, and India for the transportation of fuels and chemicals, along with growing tanker truck adoption in agriculture.

End-user Insights

The retail & e-commerce sub-segment is expected to lead the revenue share in 2025, accounting for roughly 32.5%. Strong growth is driven by rising demand for palletized goods, rapid urban deliveries, and just-in-time inventory movement across fast-paced distribution channels. Its leading position is also attributable to the widening presence of e-commerce infrastructure and services, the soaring requirement for faster restocking cycles, and the meteoric rise of urban fulfillment centers. Brands investing in dry van fleets, digital freight forwarding, and less-than-truckload (LTL) services boost demand for reliable shipments of consumer goods in retail and e-commerce.

The oil & gas sector, where there is a consistent requirement for bulk liquid and industrial chemical transport, is poised to display the highest CAGR through 2032. This acceleration is driven by the expanding petrochemical production, shipment of agricultural liquids such as edible oils, and hydrogen fuel logistics in regions including the Middle East. Companies actively engaged in expanding their liquid bulk fleets, incorporating chemical-grade tanker trucks into their fleets, and collaborating in hydrogen freight logistics pilot programs are positioned to witness robust growth through 2032.

Regional Insights

North America Freight Trucking Market Trends

North America is anticipated to command a leading market share of 36% in 2025, driven by a highly developed logistics ecosystem and an active implementation of digital freight solutions featuring AI load matching, telematics, and predictive fleet maintenance. Significant investments in electric truck charging corridors, such as California’s zero-emission truck mandates, reinforce North America’s leading role.

Domestic freight volumes have fallen in 2025, with Q2 heavy-duty truck orders dropping sharply by over 40%, prompting cyclical caution among global carriers such as Volvo and J.B. Hunt. In spite of these fallouts, regulatory incentives have managed to sustain the adoption of zero-emission fleets and multimodal intermodal integration, anchoring the operational resilience of fleet operators in the region while also boosting the market.

Asia Pacific Freight Trucking Market Trends

Asia Pacific is projected to be the fastest-growing regional market, outpacing the most mature economies of North America and Europe. Several factors are contributing to the market growth in this region, including the high rate of urbanization in India, China, and Southeast Asia, rising manufacturing output, and huge investments in large-scale infrastructure ventures. For example, the World Bank estimates that India’s urban areas will be home to nearly 600 million people, or around 40% of the country’s population, by 2036.

E-commerce expansion, electric truck pilots, and upgraded road networks are propelling the demand for efficient dry van freight, tank truck logistics, and widening of inter-regional distribution networks. Notably, in China, according to the ICCT, the sales of zero-emission trucks and tractor-trailers hit 230,000 in 2024 alone, while 4 million freight trucks were deployed on Indian roads in 2022, and this number is expected to swell to 17 million by 2050, laying the groundwork for market growth.

Europe Freight Trucking Market Trends

Europe is experiencing bright prospects on the back of robust freight volumes and a highly regulated logistics & transport industry environment. Fleet operators in the European Union (EU) have to meet stringent emissions standards and safety mandates, such as the European Agreement concerning the International Carriage of Dangerous Goods by Road (ADR). These regulations have pushed European freight trucking companies to ramp up investments in fleet electrification and automation.

Although freight volumes have declined to a certain extent due to macroeconomic uncertainty and geopolitical tensions, regulatory tailwinds in the form of zero-emission zones and digital tachograph mandates continue to stimulate innovation in sustainable trucking, logistics digitization, and fleet optimization strategies across the continent.

Competitive Landscape

The global freight trucking market landscape is highly competitive with giants such as DHL, XPO Logistics, FedEx, Yellow Corporation, and CEVA Logistics, who compete on fleet size, digital freight matching, and sustainability metrics. These players differentiate themselves through investments in real-time tracking, carbon reporting, and last-mile efficiency. For instance, DHL’s global network, combined with its advanced telematics systems, enables predictive maintenance and optimized dispatching. This intense competition is fueling demand for lightweight trailers, aerodynamic design innovations, and AI route optimization.

Autonomous trucking pioneers such as Aurora Innovation and Plus are disrupting the freight trucking space by leveraging cutting-edge technologies. Aurora’s Level 4 trucks ply between Dallas and Houston, while Plus is piloting across 48 U.S. states. These advancements illustrate how autonomy can reduce labor costs and empty miles, and accelerate the development of autonomous transfer hub networks (ATHNs). Sustainability-focused companies such as Einride are future-proofing freight operations by electrifying port-to-city freight lanes. They deliver pragmatic zero-emission logistics and carbon-efficient services by partnering with companies such as Mars and Maersk.

Key Industry Developments

- In July 2025, Flock Freight launched STL AddOns, a patent-pending technology that dynamically fills unused trailer space in its Shared Truckload (STL) service. It identifies compatible freight in real time to maximize truck utilization and boost profitability. Carriers get instant alerts and automatic route updates without delays.

- In June 2025, Descartes Systems Group acquired PackageRoute for around US$2 Mn. PackageRoute provides mobile and web-based tools for final-mile carriers, offering real-time delivery visibility, route optimization, and fleet management. The integration with Descartes’ GroundCloud solutions is expected to enhance safety, routing, and compliance for customers.

- In May 2025, XPO Logistics implemented advanced AI models to optimize its linehaul operations. Integrated into its TMS, the AI helps employees load trailers more efficiently, reducing freight handling and total miles driven. Handling 2.6 million linehaul miles daily, XPO has already seen gains in trailer utilization and expects further efficiency improvements as the models are refined.

Companies Covered in Freight Trucking Market

- United Parcel Service, Inc.

- FedEx Corporation

- J.B. Hunt Transport Services, Inc.

- Knight-Swift Transportation Holdings Inc.

- Schneider National, Inc.

- XPO Logistics, Inc.

- Old Dominion Freight Line, Inc.

- C.H. Robinson Worldwide, Inc.

- Landstar System, Inc.

- CEVA Logistics AG

- A.P. Moller‑Maersk Group

- Deutsche Post AG (DHL International GmbH)

- DSV Panalpina A/S

- DB Schenker (Schenker AG)

- Nippon Express Co., Ltd.

- Saia, Inc.

- YRC Worldwide Inc.

Frequently Asked Questions

The global freight trucking market is projected to reach US$2.74 Tn in 2025.

Volatile fuel prices and tightening regulations to curb emissions in the logistics sector are driving the market.

The freight trucking market is poised to witness a CAGR of 3.9% from 2025 to 2032.

The shift toward zero-emission vehicles (ZEVs) for freight transport and a growing urgency to decarbonize the logistics industry are key market opportunities.

United Parcel Service (UPS), FedEx Corporation, and J.B. Hunt Transport Services are the leading players.