- Executive Summary

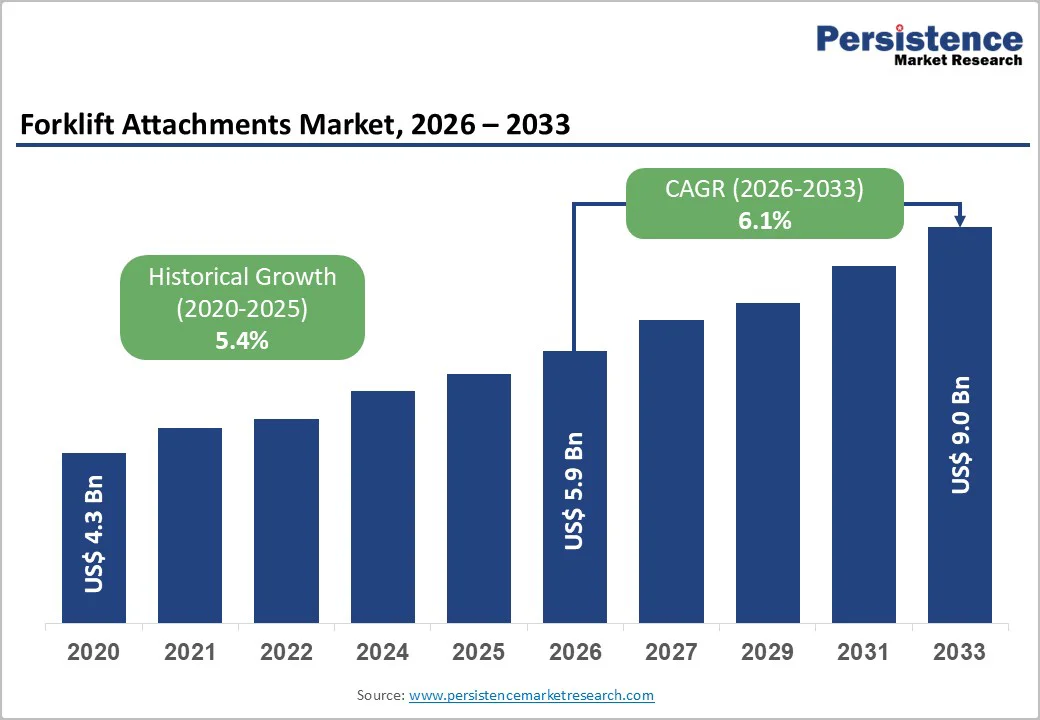

- Global Forklift Attachments Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Material Handling Equipment Sales by Region

- Global Forklift Sales by Type

- Global e-Commerce & Warehouse Growth Outlook

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

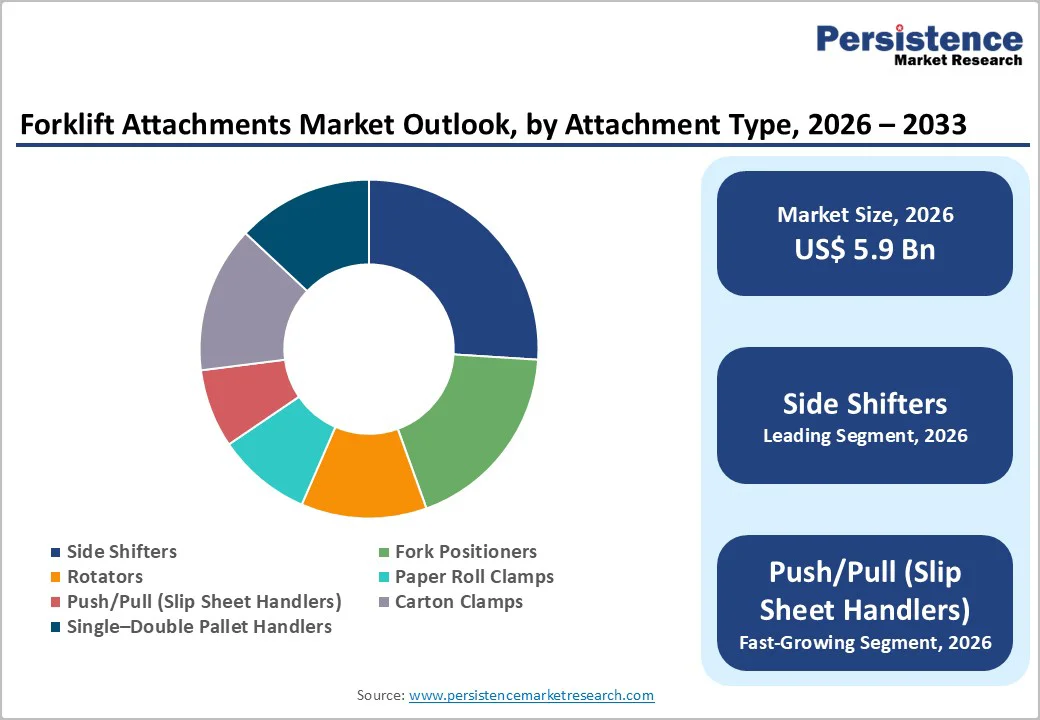

- Global Forklift Attachments Market Outlook: Attachment Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Attachment Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- Market Attractiveness Analysis: Attachment Type

- Global Forklift Attachments Market Outlook: End Use

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by End Use, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- Market Attractiveness Analysis: End Use

- Global Forklift Attachments Market Outlook: Forklift Truck Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Forklift Truck Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- Market Attractiveness Analysis: Forklift Truck Type

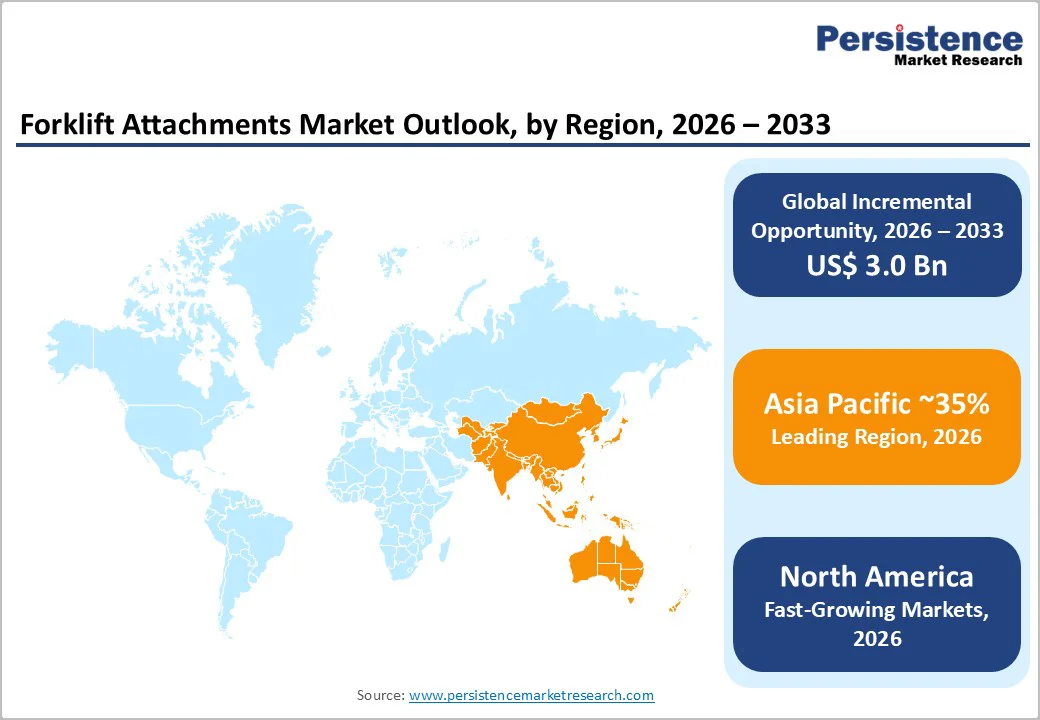

- Global Forklift Attachments Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- Europe Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- East Asia Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- South Asia & Oceania Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- Latin America Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- Middle East & Africa Forklift Attachments Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Attachment Type, 2026-2033

- Side Shifters

- Fork Positioners

- Rotators

- Paper Roll Clamps

- Push/Pull (Slip Sheet Handlers)

- Carton Clamps

- Single–Double Pallet Handlers

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by End Use, 2026-2033

- Rental Service Providers

- Individual Operators

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Forklift Truck Type, 2026-2033

- Counterbalance

- Walkie Trucks

- Reach Stackers

- Order Pickers

- Sideloaders

- Off-road Forklifts

- Telescopic Handlers

- Truck-mounted Forklifts

- Articulated Forklifts

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Toyota Industries Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- KION Group AG

- Crown Equipment Corporation

- Jungheinrich AG

- Linde Material Handling

- Cascade Corporation

- Bolzoni Auramo

- TVH Inc.

- Vestil Manufacturing

- Kalmar

- Clark Equipment

- Hyster-Yale Technologies

- Toyota Industries Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Loading page data

Please wait a moment