- Smart Packaging

- Folding Boxboard Market

Folding Boxboard Market Size, Share, and Growth Forecast, 2025 - 2032

Folding Boxboard Market By Product Type (Virgin fiber FBB, Mechanical pulp-based, Chemical pulp-based, Recycled fiber FBB, and Specialty FBB), Surface Treatment (Uncoated FBB, Coated FBB, and Surface finishing), End-user, and Regional Analysis for 2025 - 2032

Folding Boxboard Market Size and Trends Analysis

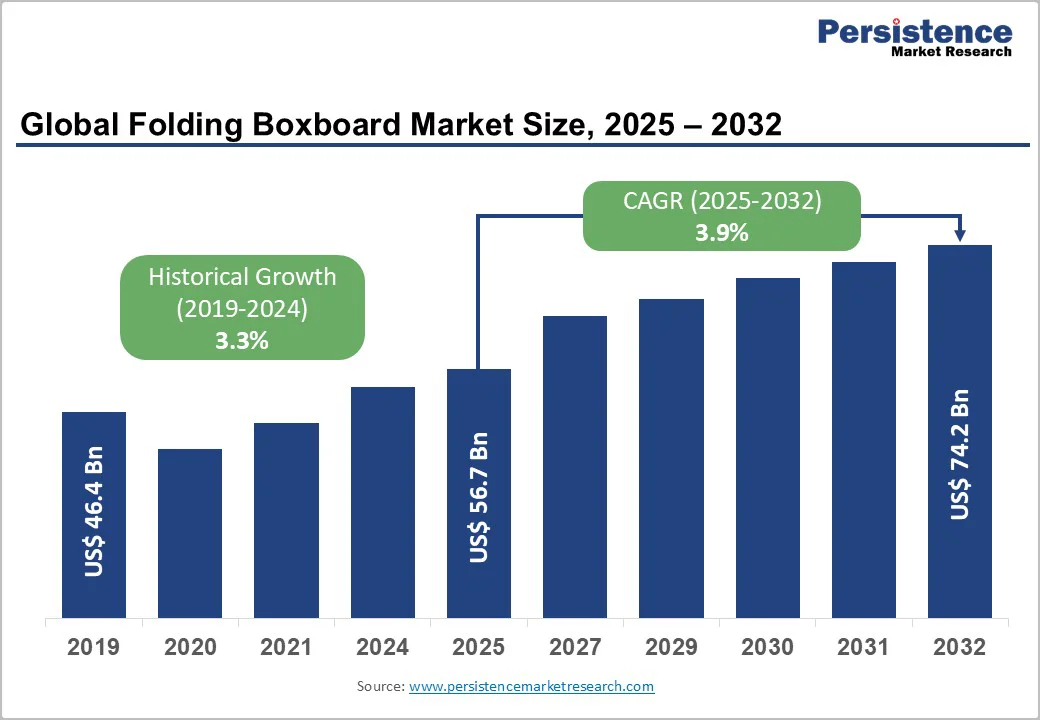

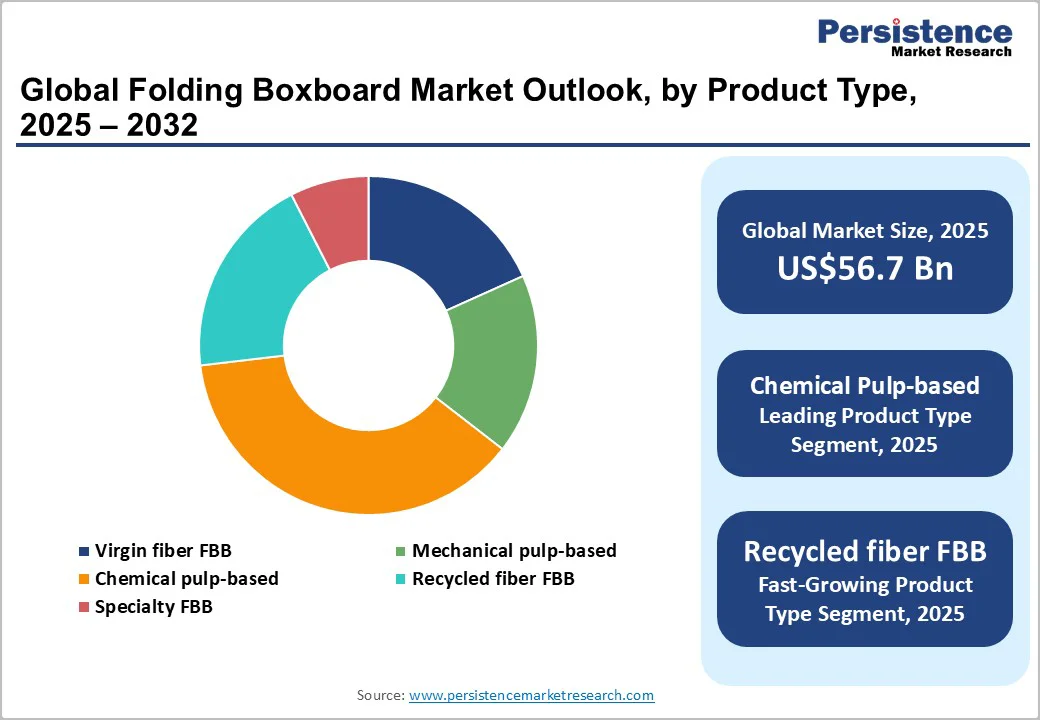

The global folding boxboard market is expected to reach US$56.7 billion in 2025. It is projected to reach US$74.2 billion by 2032, growing at a CAGR of 3.9% during the forecast period from 2025 to 2032, driven by the rising demand for sustainable and recyclable packaging solutions across various industries, particularly within the food and beverage sector.

This trend is strengthened by advances in manufacturing that improve the durability and printability of folding boxboard, enhancing branding and product protection. Rising adoption in e-commerce and consumer goods further reflects the industry’s shift toward sustainable packaging.

Key Market Highlights

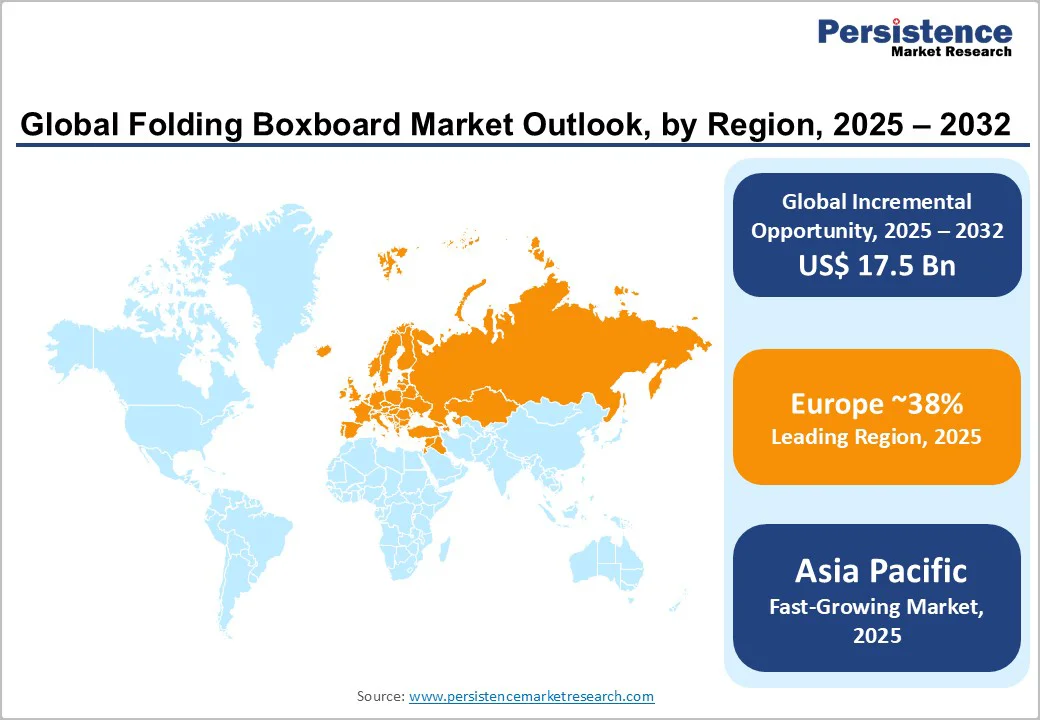

- Leading Region: Europe leads the market due to advanced regulatory frameworks and high adoption in premium packaging for cosmetics and food industries.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing region, driven by manufacturing expansions in China and India amid rising e-commerce and urbanization trends.

- Leading Category: Coated FBB dominates product types, offering superior printability and barrier properties essential for branding in consumer goods applications.

- Fastest-Growing Category: Recycled fiber. FBB is the fastest-growing segment, supported by sustainability policies and circular-economy initiatives, boosting demand in emerging markets.

- Key market opportunity lies in sustainable innovations such as plant-based coatings, enabling compliance with global regulations and capturing eco-conscious consumer segments.

| Key Insights | Details |

|---|---|

|

Folding Boxboard Market Size (2025E) |

US$56.7 Bn |

|

Market Value Forecast (2032F) |

US$74.2 Bn |

|

Projected Growth CAGR (2025-2032) |

3.9% |

|

Historical Market Growth (2019-2024) |

3.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability-Driven Shift Boosts Folding Boxboard Adoption Worldwide

The increasing focus on eco-friendly and recyclable materials is driving strong market growth. Both consumers and regulators are shifting away from plastic and choosing sustainable alternatives that align with global climate goals. With a paper packaging recycling rate of 82.5% in the EU (Eurostat), folding boxboard has become a preferred choice due to its biodegradability, renewability, and recyclability. Derived from wood pulp, it meets the rising sustainability standards for packaging.

International initiatives such as the European Green Deal encourage companies to use low-carbon and renewable materials. As a result, several leading brands are investing in environmentally friendly substrates to reduce their carbon footprint and enhance brand image. This growing shift toward circular and responsible packaging solutions is expected to significantly boost market demand and innovation in sustainable production processes over the coming years.

E-Commerce Expansion Accelerates Demand for Lightweight and Printable Boxboard

The rapid expansion of e-commerce and packaged consumer goods industries is a major factor fueling the demand for folding boxboard. The material’s lightweight, durable, and printable properties make it ideal for packaging products that require both protection and visual appeal during shipping and display. In Asia Pacific region, e-commerce packaging demand rose sharply, with total production reaching 26 million tons in 2024, reflecting a 1.6% annual increase.

Folding boxboard supports excellent branding opportunities through high-quality printing, allowing businesses to deliver eye-catching and convenient packaging for products such as cosmetics, snacks, and beverages. As consumers increasingly value sustainability and presentation, manufacturers are using FBB to achieve both, ensuring safety, appeal, and environmental responsibility. This trend, combined with growing online retail and demand for attractive consumer packaging, is expected to further accelerate folding boxboard adoption globally.

Barrier Analysis - Volatile Wood Pulp Costs Challenge Market Stability and Profit Margins

Volatility in raw material costs, especially pulp and wood fiber, remains one of the key restraints for the market. These materials form a major share of production expenses, making the market sensitive to supply chain disruptions and geopolitical events. Over the past few years, price fluctuations of up to 25% have been recorded due to factors such as changing weather conditions, trade restrictions, and rising transportation costs. Such instability directly impacts manufacturers’ profitability and makes it difficult to plan long-term investments or pricing strategies.

Smaller producers face even greater challenges, as they struggle to maintain consistent quality while absorbing higher costs. This price volatility further limits competitiveness against cheaper substitutes such as plastic and recycled cardboard, potentially slowing market penetration in cost-sensitive regions such as parts of Asia and Latin America.

Tightening Environmental Rules Increases Compliance Costs for Manufacturers

The tightening of environmental regulations around emissions, waste disposal, and energy use in paper production is another significant challenge for the market. Directives such as the EU Green Deal and the Packaging and Packaging Waste Directive require companies to adopt cleaner production technologies, advanced wastewater treatment, and energy-efficient machinery. These compliance efforts increase operational expenses by approximately 10–15%, placing financial strain on producers, especially in developing economies.

Non-compliance can lead to heavy fines or temporary production shutdowns, discouraging new entrants from investing in the sector. While these rules encourage sustainable innovation, they also raise the cost of production and slow scalability in regions with limited technological advancement. As a result, manufacturers must balance regulatory compliance with profitability while continuously innovating to remain competitive in an increasingly sustainability-driven marketplace.

Opportunity Analysis - Circular Economy Push Opens Growth Opportunities in Recycled Fiber Boxboard

The growing global focus on circular economy principles is creating lucrative opportunities in recycled fiber-based folding boxboard (FBB). As more countries strengthen recycling systems and reduce landfill waste, the availability of recycled paper materials is increasing. Manufacturers can now utilize advanced recycling technologies to produce high-quality FBB from recovered fibers, reducing dependence on virgin wood pulp. This aligns with the EU’s goal of achieving a 75% packaging recycling rate by 2030.

In emerging economies, rising awareness of sustainable consumption and expanding e-commerce sectors are driving greater use of recycled materials. The adoption of recycled FBB not only lowers production costs but also appeals to eco-conscious brands and consumers. Companies investing in efficient recycling infrastructure and closed-loop production models stand to benefit from this growing segment of the market.

Asia Pacific and Latin America Emerge as High-growth Hubs for Folding Boxboard

The Asia Pacific and Latin American regions are emerging as powerful growth hubs for the market. Urbanization, expanding middle-class populations, and increasing disposable incomes are driving a strong demand for packaged goods such as food, cosmetics, and pharmaceuticals. China currently accounts for about 62% of the regional production share, benefiting from advanced manufacturing capabilities and government policies promoting local material sourcing. Countries such as India and Indonesia are also witnessing growing investments in sustainable packaging facilities.

Regional trade agreements and capacity expansions have made these markets more attractive for international players. The region’s competitive labor costs and improving infrastructure support large-scale production and export potential. With consumer preferences rapidly shifting toward sustainable and premium packaging, Asia Pacific presents significant opportunities for folding boxboard producers through 2032 and beyond.

Category-wise Analysis

Product Type Insights

Chemical pulp-based folding boxboard leads with approximately 35% market share, owing to its superior strength and printability suited for premium packaging. This segment's dominance stems from its use in high-volume applications such as food cartons, where consistent quality ensures product protection and branding appeal. Industry data indicates the prevalence of chemical pulp due to efficient processing from sustainable forestry, aligning with the global supply chain standards.

Surface Treatment Insights

Coated folding boxboard commands about 60% of the market, driven by its enhanced gloss and ink adhesion for vibrant graphics on consumer products. This treatment's popularity is justified by demand in cosmetics and pharmaceuticals, where visual appeal influences purchasing decisions. Authentic statistics show coated variants' higher adoption rate, supported by advancements in coating technologies that improve recyclability without compromising performance.

End-user Insights

Food & beverage holds the leading position in the end-user category with roughly 45% market share, driven by the need for hygienic and visually appealing packaging for dry goods, snacks, and beverages. This segment benefits from folding boxboard's ability to ensure freshness and comply with stringent regulations, such as those from the World Health Organization on food contact materials. Its adaptability to various formats, from cartons to trays, cements its dominance in this high-volume industry.

Regional Insights

North America Folding Boxboard Market Trends

North America, led by the U.S., holds a significant share in the folding boxboard market due to its focus on premium, sustainable packaging solutions. The region benefits from a well-developed converting and printing infrastructure that supports the production of high-quality FBB for e-commerce, consumer goods, and healthcare packaging. Strong EPA guidelines and corporate sustainability initiatives are promoting the use of recycled materials and eco-friendly substrates.

Investments in digital and 3D printing technologies have allowed manufacturers to offer customizable and visually appealing packaging options. Capacity expansions and modernization of mills across the U.S. and Canada are improving production efficiency and supply chain stability. North America’s innovation-driven ecosystem ensures continuous advancements in barrier and coating technologies, further strengthening its role as a leader in sustainable packaging trends.

Europe Folding Boxboard Market Trends

Europe demonstrates robust growth in the folding boxboard market, driven by strong environmental policies and technological advancements. Key countries such as Germany, the U.K., France, and Spain are leading the charge under the EU Packaging and Packaging Waste Directive, which enforces strict recyclability and circular economy standards. Germany, holding about 32% of the regional market share, is known for its advanced coating and converting facilities that cater to the luxury cosmetics and food packaging sectors.

France and Spain focus on premium and sustainable boxboard products, holding 17% and 10% shares, respectively. Continuous investments in capacity expansion, exceeding 1 million tonnes annually, are strengthening regional supply. The U.K.’s booming e-commerce market has also driven the adoption of cost-efficient uncoated FBB. Collectively, Europe’s well-regulated and innovation-oriented market environment ensures sustained growth and leadership in eco-friendly packaging materials.

Asia Pacific Folding Boxboard Market Trends

The Asia Pacific region is the fastest-growing market for folding boxboard, fueled by strong industrialization, expanding consumer markets, and sustainable manufacturing initiatives. China, Japan, and India are key contributors, benefiting from low-cost production and rapid technological upgrades. China’s market is expected to grow at a high CAGR through 2032, supported by rising consumer goods demand and investments in advanced paperboard facilities. India follows closely, driven by government programs promoting eco-friendly packaging and increasing use in the food and personal care industries.

Japan emphasizes high-quality coated FBB for electronics and premium products. ASEAN nations, including Indonesia and Vietnam, are showing a high growth potential, driven by regional trade expansion. Asia Pacific’s strong manufacturing base, cost advantages, and rising sustainability focus position it as a major driver of global market growth in the coming decade.

Competitive Landscape

The global folding boxboard market exhibits a consolidated structure, with top players controlling over 60% of capacity through integrated mills and strategic mergers. Companies pursue expansion via acquisitions and R&D in sustainable fibers, differentiating via eco-certified products and customized coatings for end-uses. Key leaders employ vertical integration for cost control, while emerging models focus on digital printing for personalization. Trends include partnerships for recycled content, enhancing resilience against raw material volatility and regulatory pressures, and fostering innovation in lightweight designs.

Key Industry Developments

- In April 2025: Mondi marked the start-up of its €200 million (US$232 Million) recycled containerboard mill in Duino, Italy, boosting annual capacity by 420,000 tonnes to serve e-commerce and food sectors with sustainable solutions.

- In September 2025: Mondi unveiled its eCommerce packaging lineup at eCommerce EXPO U.K., introducing paper-based mailers and boxes post-acquisition of Schumacher Packaging, targeting plastic-free alternatives.

- In April 2025, Huhtamaki launched plant polymer-coated delivery boxes via Lieferando in Germany, featuring Xampla’s biodegradable Morro coating for food transport, compliant with the single-use plastics directive.

Companies Covered in Folding Boxboard Market

- Huhtamaki OYJ

- DS Smith

- Coveris

- Sabert

- Wihuri

- Nippon Paper Industries Co., Ltd.

- South African Pulp & Paper Industries Limited

- Mondi

- Amcor Limited

- Sonoco Products Company

- Sealed Air Corporation

- Smurfit Kappa

- Mayr-Melnhof Karton

- WestRock Company

- International Paper

Frequently Asked Questions

The folding boxboard market is valued at US$56.7 Billion in 2025 and expected to reach US$74.2 Billion by 2032, reflecting steady growth in sustainable packaging demand.

Key drivers include the shift to sustainable materials and e-commerce expansion, with rising consumer preference for recyclable options boosting adoption across industries.

The food & beverage segment leads with 45% share, driven by needs for hygienic and branded packaging in snacks and dry goods.

Europe leads due to stringent sustainability regulations and advanced manufacturing in countries such as Germany and France.

Expansion in recycled FBB offers potential through policy support and circular economy trends, targeting high-growth areas including Asia Pacific.

Major players include Huhtamaki OYJ, Mondi, Smurfit Kappa, and DS Smith.