- Smart Packaging

- Fluorinated Bottles Market

Fluorinated Bottles Market Size, Share, and Growth Forecast 2026 - 2033

Fluorinated Bottles Market by Fluorination Type (In-Mold Fluorination, Post-Mold Fluorination, Others), Material Type (High Density Polyethylene (HDPE), Low Density Polyethylene (LDPE), Polypropylene (PP)), Capacity (Up to 500 ml, 500 ml to 1000 ml, Above 1000 ml), End-user (Industrial Chemicals, Automotive, Agrochemicals, Pharmaceuticals, Personal Care), Regional Analysis, 2026 - 2033

Fluorinated Bottles Market Size and Trend Analysis

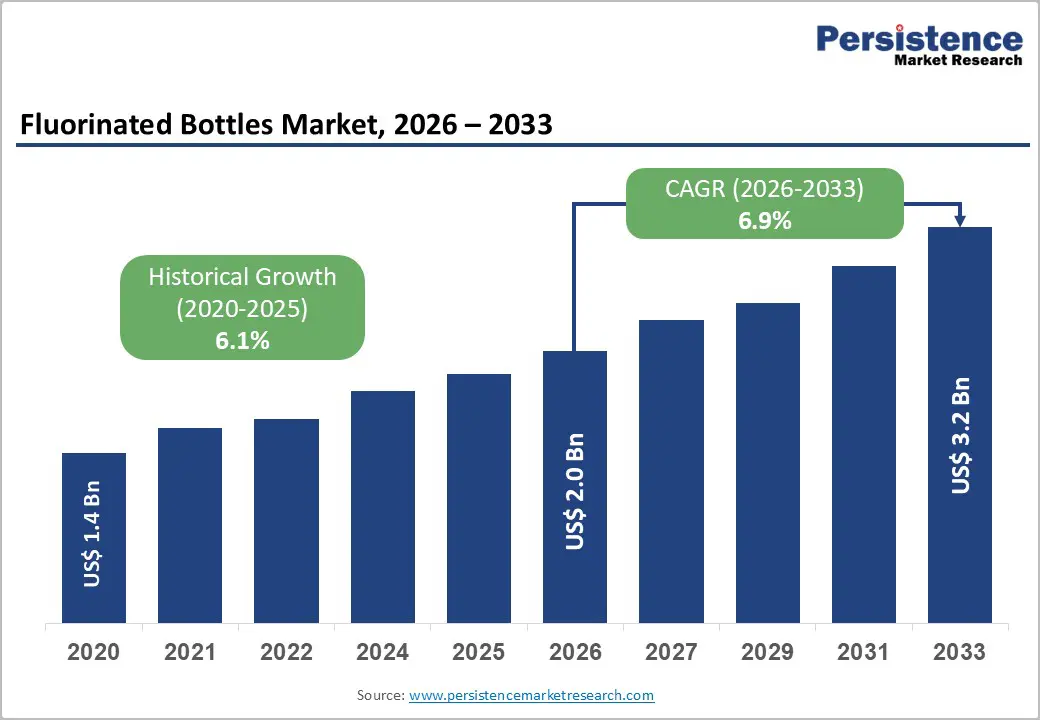

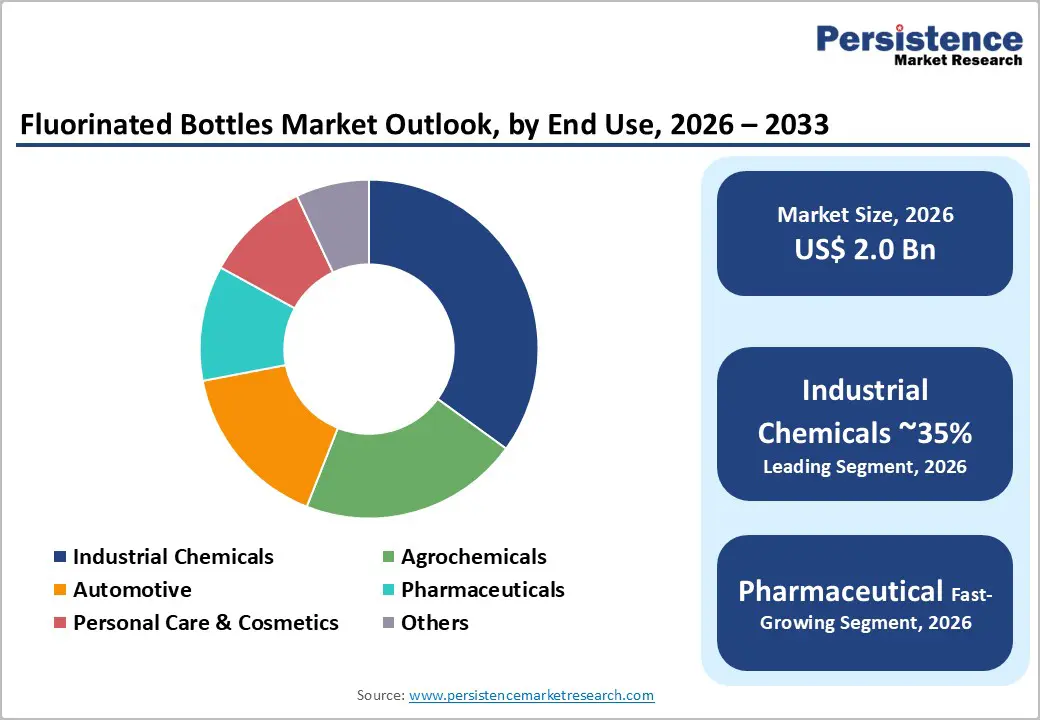

The global fluorinated bottles market size is likely to be valued at US$ 2.0 billion in 2026 and is expected to reach US$ 3.2 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 and 2033. The market's accelerated growth trajectory is primarily propelled by stringent global regulations mandating safer packaging for hazardous materials and the robust expansion of the agrochemical and pharmaceutical sectors in emerging economies.

Key Industry Highlights:

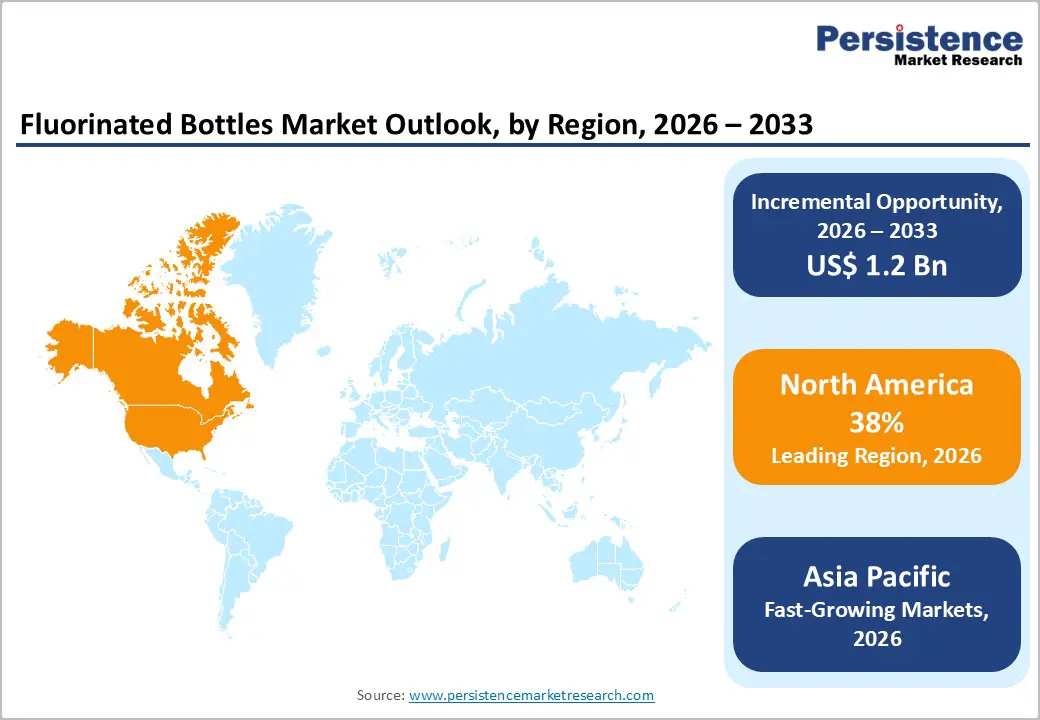

- Leading Region: North America dominates the market with a rising CAGR of 38%, due to its established industrial base and strict regulatory frameworks for hazardous material transport.

- Fastest Growing Region: Asia Pacific is projected to witness the highest growth rate, fueled by expanding agricultural and pharmaceutical manufacturing sectors.

- Dominant Segment: The Industrial Chemicals end-user segment holds the largest market share, driven by the essential need for safe solvent storage.

- Fastest Growing Segment: The Pharmaceutical end-user segment is expected to grow rapidly, owing to increasing demand for high-purity, chemically inert drug packaging.

- Key Market Opportunity: Integrating Smart Packaging features like RFID and NFC for tracking high-value chemicals presents a significant untapped revenue stream.

| Key Insights | Details |

|---|---|

|

Fluorinated Bottles Market Size (2026E) |

US$ 2.0 Billion |

|

Market Value Forecast (2033F) |

US$ 3.2 Billion |

|

Projected Growth CAGR(2026-2033) |

6.9% |

|

Historical Market Growth (2020-2025) |

6.1% |

Market Dynamics

Drivers - Growing Pharmaceutical and Healthcare Needs for Contamination-Free, Chemically Stable Packaging are Sharply Increasing Demand for Fluorinated Bottles

The growing need for chemically stable and safe packaging in the pharmaceutical and healthcare industries is significantly driving the fluorinated bottles market. As manufacturers increase their production of biologics, vaccines, and aggressive APIs, they require containers that prevent chemical reactions with the packaging wall. Fluorinated bottles offer an inert barrier that reduces extractables and leachables, ensuring drug purity and patient safety while avoiding the fragility associated with glass. This trend is especially strong in developing regions, where resilient packaging is essential for complex supply chains.

In 2025, the sector’s rising demand is supported by Berry Global Inc.’s merger with Amcor, which aimed to expand their presence in pharmaceutical and consumer packaging. The company stated that its enhanced material-science capabilities would help meet healthcare industry needs for high-performance, contamination-free storage solutions.

Rising use of Aggressive Agrochemicals and Industrial Solvents is Driving Strong Adoption of Fluorinated HDPE Bottles for Safer, More Durable Storage

Demand for fluorinated HDPE bottles is also increasing across agricultural and industrial chemical sectors. Agrochemicals such as potent pesticides, herbicides, and liquid fertilizers contain solvents that can cause paneling, deformation, or leakage in standard plastic bottles. Fluorinated bottles provide stronger chemical resistance and structural stability, preventing product loss and ensuring safe transportation under varying environmental conditions. The industrial sector also relies heavily on these bottles for storing solvents, automotive additives, and high-corrosion fluids, especially under strict global regulations for hazardous goods. In 2025, Berlin Packaging promoted its “HDPE Fluorinated F-Style Bottles” specifically engineered for aggressive hydrocarbon-based chemicals. The company emphasized that fluorinated technology prevents container degradation and ensures long-term integrity for sensitive industrial contents.

Restraints - Regulatory Scrutiny over PFAS Risks is Creating Compliance Challenges and Pushing Manufacturers toward Costly, Improved Fluorination Controls

The fluorinated bottles market faces heightened scrutiny as environmental regulators examine potential PFAS formation during certain fluorination processes. Authorities such as the U.S. EPA and FDA are increasing inspections and compliance requirements for manufacturers to ensure fluorinated containers do not contribute to persistent environmental pollutants or unintentional migration into food or sensitive applications.

This tightening oversight is prompting many producers to adopt improved process controls, continuous monitoring systems, and advanced fluorination technologies that minimize risk but also raise operational costs. Companies attempting to enter the market must now invest more heavily in compliance certification, emissions control, and environmentally conscious production systems. These factors can slow production scale-up for smaller players and increase the cost structure across the industry.

High Investment and Operational Costs for Fluorination Technology Limit Adoption, Especially in Price-Sensitive and Emerging Markets

Establishing and operating a fluorination facility necessitates a substantial investment in specialized reactors, fluorine gas handling systems, and high-precision safety infrastructure to safeguard personnel and the environment. Because fluorine is highly reactive, strict controls and automatic safety mechanisms are essential, driving initial capital costs far beyond those of conventional plastic processing lines. These elevated setups and operating expenses result in a higher overall cost for fluorinated bottles, which limits their adoption among price-sensitive industries.

For some packaging suppliers, alternative barrier methods, such as co-extrusion or multilayer bottles, may appear more financially attractive despite offering lower chemical resistance. As a result, the cost gap between fluorinated and non-fluorinated packaging slows wider acceptance, especially in emerging markets where pricing plays a dominant role in procurement decisions.

Opportunity- Eco-Friendly, Recyclable Fluorination Technologies offer Strong Market Opportunities Aligned with Global Circular Economy Goals

The growing global focus on circular economy principles presents a strong opportunity for companies to innovate sustainable fluorination technologies. Manufacturers are increasingly working on barrier solutions that preserve recyclability, minimize environmental impact, and meet regulatory expectations for eco-friendly packaging. Developing fluorinated bottles that can be easily identified in recycling streams or incorporate PCR content can help companies build competitive advantages, especially in Europe and North America, where sustainability mandates are strict.

In May 2025, Greiner Packaging showcased its “ISBM bottles” designed for lightweight structure, excellent barrier performance, and exceptional recyclability. The company emphasized that its materials align with future recycling standards and circular-design requirements, reinforcing the market shift toward environmentally responsible packaging.

Smart Packaging Features such as RFID and Digital Watermarks Present High-Value Growth Potential by Enabling Tracking, Authentication, and Better Supply-Chain Visibility

Integrating digital and smart features into fluorinated packaging represents a high-growth opportunity in premium chemical and pharmaceutical segments. Companies are exploring IoT-enabled technologies such as RFID, NFC, digital watermarks, and QR coding to provide real-time tracking, anti-counterfeiting, and traceability. These features are especially valuable for sensitive or high-value liquids that require secure logistics and authenticated supply chains. Smart fluorinated bottles could deliver both chemical protection and digital visibility, creating strong differentiation for manufacturers. In 2025, this opportunity gained momentum when Greiner Packaging announced the successful completion of the “HolyGrail 2.0” project, proving that digital watermarks can be detected and sorted at an industrial scale. The initiative demonstrated how digital intelligence can support waste management, authenticity verification, and efficient recycling.

Category-wise Analysis

Fluorination Type Insights

The In-Mold Fluorination (IMF) segment represents about 45% of the fluorinated bottles market. IMF is preferred because it integrates the fluorination step into the blow-molding process, which enhances production efficiency and reduces handling costs. This method ensures consistent barrier performance for containers used in automotive fluids, lubricants, industrial chemicals, and household products. With excellent permeation resistance and suitability for high-volume manufacturing, IMF is increasingly favored as demand for sustainable, high-performance packaging rises globally.

Material Type Insight

HDPE remains the dominant material used in fluorinated bottle manufacturing, accounting for approximately 78% of market share due to its strong mechanical durability, lightweight structure, and excellent suitability for fluorination. Its ability to withstand impacts, temperature variations, and aggressive solvents makes it a popular replacement for heavier materials such as metal and glass in industries dealing with industrial chemicals, automotive fluids, and agrochemical formulations. The global recycling network for HDPE is also well-established, reinforcing its appeal to manufacturers focused on both performance and sustainability. Fluorinated HDPE bottles specifically address issues like permeation and paneling, which commonly occur in untreated plastics, thereby offering reliable protection for volatile or hazardous contents.

Capacity Insights

The 500 ml to 1,000 ml capacity range holds the largest share of the fluorinated bottles market, representing around 42% of global volume. This category aligns with standard packaging formats used widely in agriculture and automotive maintenance, including retail units for pesticides, liquid fertilizers, engine oils, and solvent-based products. The convenience, portability, and ease of handling offered by this capacity size make it an ideal choice for everyday consumer use as well as professional applications. Its dimensions also optimize shelf space, transport efficiency, and storage safety, encouraging manufacturers to prioritize this format for mass-market distribution.

Application Insights

The Industrial Chemicals segment leads the global market with an estimated 35% share, driven by high consumption of solvents, cleaning agents, coatings, and specialty chemicals that demand chemically resistant and compliant packaging. Fluorinated bottles are essential in this segment because they prevent vapor emissions, resist corrosion from aggressive contents, and comply with international standards for hazardous goods transport—including UN performance ratings. Industrial chemical producers favor fluorinated containers for maintaining product purity, extending shelf life, and ensuring safe long-distance shipping. Their durability under extreme handling conditions makes them indispensable in global chemical supply chains.

Regional Insights

North America Fluorinated Bottles Market Trends

North America shows strong adoption of fluorinated bottles due to strict regulations from the EPA, DOT, and FDA, which require robust packaging for hazardous, reactive, and sensitive materials. Companies across the U.S. and Canada continuously invest in high-quality fluorination processes to enhance barrier strength, limit emissions, and improve recyclability. The region’s large pharmaceutical, automotive, and industrial chemical industries depend on packaging that ensures safe handling during storage and transportation. Sustainability pressures are also reshaping packaging specifications.

In December 2025, Berlin Packaging highlighted that new state-level rules in California and New Jersey are increasing minimum recycled-content requirements and strengthening reporting obligations, pushing brands toward more durable, compliant packaging formats. These developments reinforce the trend that fluorinated bottles must combine chemical resistance with sustainability as companies aim to meet both safety and environmental expectations.

Europe Fluorinated Bottles Market Trends

Europe remains a global leader in sustainable packaging, strongly influenced by the EU Green Deal and updated regulations under the Packaging and Packaging Waste Regulation (PPWR). These frameworks emphasize recyclability, circular design, and reduced environmental impact. As a result, industries such as chemicals, cosmetics, and specialty manufacturing are increasingly shifting toward fluorinated bottles that can deliver high chemical resistance while remaining compatible with recycling systems. Countries like Germany, France, and the U.K. are early adopters of advanced fluorination technologies that support these goals.

In April 2025, Greiner Packaging highlighted that future packaging in the EU will be scored using a recyclability-based traffic-light system, requiring strict compliance with design-for-recycling standards and higher use of PCR materials. This aligns directly with regional trends pushing manufacturers to combine barrier performance with regulatory conformity.

Asia Pacific Fluorinated Bottles Market Trends

Asia Pacific is rapidly becoming the fastest-growing region for fluorinated bottles due to accelerating industrialization in China and India and rising demand from agrochemicals, pharmaceuticals, and automotive fluids. India’s agricultural sector consumes large volumes of pesticides and fertilizers that require durable, chemically resistant packaging, boosting demand for fluorinated containers. Additionally, the region’s expanding pharmaceutical manufacturing base is creating new opportunities for advanced rigid packaging. Cost-effective production and growing domestic consumption further strengthen growth prospects.

Berry Global has emphasized Asia Pacific’s strategic importance through recent investments in healthcare packaging facilities in India. During CPHI India, the company showcased its new Bangalore plant designed for high-volume production of bottles, closures, and drug-delivery components using circular-design principles. This development illustrates how major players are building regional capacity to support the rising need for safe, compliant packaging, including fluorinated bottles.

Competitive Landscape

The global fluorinated bottles market exhibits a moderately consolidated structure, with a few major multinational players holding significant market share while numerous regional manufacturers cater to local demands. Leading companies utilize strategies such as vertical integration and strategic acquisitions to expand their global footprint and technological capabilities. There is a strong focus on research and development, particularly in enhancing barrier technologies and developing proprietary fluorination processes that offer superior consistency and safety. Key differentiators for market leaders include the ability to offer UN-certified packaging, custom mold designs, and comprehensive sustainability reports that appeal to eco-conscious multinational clients.

Key Market Developments:

- In October, 2024: Berry Global Inc. announced the launch of a new line of lightweight, high-barrier fluorinated bottles designed specifically for the e-commerce shipment of liquid chemicals, featuring enhanced impact resistance to reduce breakage during transit.

- In August, 2024: Greiner Packaging introduced a sustainable barrier bottle solution incorporating 30% recycled content, aimed at the European automotive aftermarket, demonstrating compliance with new EU packaging waste regulations.

Companies Covered in Fluorinated Bottles Market

- Berry Global Inc.

- Alpha Packaging

- Greiner Packaging

- Plastipak Holdings Inc.

- Graham Packaging Company

- Kaufman Container Company

- CL Smith Company

- O.Berk Company LLC

- Pretium Packaging LLC

- SKS Bottle & Packaging Inc.

- Scientific Commodities Inc.

- Fidel Fillaud

- Berlin Packaging

- The Cary Company

Frequently Asked Questions

The global fluorinated bottles market is projected to reach a value of US$ 3.2 Billion by 2033, growing from US$ 2.0 Billion in 2026.

The primary demand drivers include the stringent safety regulations for transporting hazardous chemicals and the growing needs of the pharmaceutical and agrochemical industries for chemically resistant packaging.

High Density Polyethylene (HDPE) is the dominant material segment, accounting for the majority of the market share due to its superior durability and compatibility with fluorination.

Asia Pacific is expected to be the fastest-growing region, driven by rapid industrialization and the expanding agricultural sectors in countries like China and India.

A key opportunity lies in the development of sustainable, recyclable fluorinated packaging solutions and the integration of smart tracking technologies for high-value applications.

Key players in the market include Berry Global Inc., Alpha Packaging, Greiner Packaging, Plastipak Holdings Inc., and Graham Packaging Company, among others.